Introduction

Singapore's business environment demands financial accuracy — especially when revenue figures directly affect tax obligations, rental agreements, and regulatory standing. Preparation quality determines whether a sales audit proceeds smoothly or surfaces costly surprises.

Many businesses discover too late that Singapore's dual compliance environment creates unique pressure points: IRAS expects accurate revenue reporting for tax purposes, while commercial landlords require certified Gross Turnover (GTO) reports to validate rent calculations.

IRAS completed more than 2,800 GST audits in FY 2024/2025, recovering $205 million in taxes and penalties. Under-reporting, poor record-keeping, and data inconsistencies carry real costs — financial and reputational.

This article covers what a sales audit in Singapore involves, who needs it, what to prepare, and how to get ready — whether you're a retail tenant in a CapitaLand mall or an F&B franchisee operating across delivery platforms.

Key Takeaways

- A sales audit in Singapore verifies reported revenue for IRAS tax compliance, GTO/turnover-based lease obligations, and financial accuracy

- Retail, F&B, and franchise businesses face mandatory audits tied to revenue-based landlord and franchisor agreements

- Preparation centers on reconciling POS and bank data with GST filings and organized financial records

- Missing or inconsistent records are the most common cause of complications and can trigger IRAS penalties or landlord disputes

- Engaging an ACRA-registered auditor early simplifies the process significantly

What Is a Sales Audit in Singapore?

The term "sales audit" in Singapore covers two distinct concepts. First, a sales performance audit evaluates a company's sales processes, team efficiency, and pipeline effectiveness — this is an internal management tool. Second, a Gross Turnover (GTO) audit examines reported revenue to certify accuracy for tax and contractual compliance. This article focuses on the GTO audit given its regulatory and contractual significance.

What a GTO Audit Involves

An independent auditor reviews your business's sales records, POS data, bank deposits, and GST filings to certify that reported gross turnover is accurate. Unlike internal performance reviews, a GTO audit is a compliance exercise tied to contractual obligations in retail leases and franchise agreements.

According to CapitaLand Integrated Commercial Trust's FY 2024 annual report, GTO rent comprised approximately 7% of average retail portfolio gross rent, with tenants required to submit monthly GTO reports and annual audited statements. Frasers Centrepoint Trust and Mapletree operate similar structures, making GTO audit compliance a contractual and regulatory requirement.

The Regulatory Context

IRAS does not use the term "sales audit" in its published guidance. Instead, it refers to enforcement activities as audit reviews and compliance reviews, selecting businesses through both risk-based profiling and random sampling.

Key regulatory frameworks:

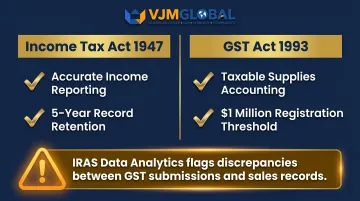

- Income Tax Act 1947: Companies must report all income accurately and maintain proper records for at least 5 years

- Goods and Services Tax Act 1993: GST-registered businesses must account for all taxable supplies; compulsory registration triggers when taxable turnover exceeds $1 million

IRAS applies data analytics to identify compliance risk across its taxpayer base. While IRAS reports that about 90% of corporate taxpayers filed their Corporate Income Tax Returns for YA 2024 on time, businesses with discrepancies between GST submissions and sales records draw closer examination.

Who Needs a Sales Audit in Singapore?

Certain businesses are contractually or regulatorily obligated to undergo a sales turnover audit — regardless of company size. Even companies that qualify for statutory audit exemptions under ACRA's criteria may still need a GTO audit if their lease or franchise agreement requires it.

Business Types Requiring GTO Audits

Retail tenants in GTO-based mall leases:

- Landlords like CapitaLand, Frasers, and Mapletree typically require certified turnover reports

- GTO rent provides landlords with upside participation when tenant sales are strong

- Applies regardless of company size

Franchisees on revenue-linked royalty agreements:

- Franchise agreements mandate accurate revenue reporting for royalty calculations

- Turnover verification protects both franchisor and franchisee interests

F&B operators in revenue-sharing venues:

- Hotels, food courts, and co-working spaces often use turnover-based rent structures

- Multi-channel operations (dine-in, takeaway, delivery platforms) require comprehensive reconciliation

**Licensed operators with revenue-linked fees (entertainment venues, childcare centres, healthcare providers):

- Sector-specific licenses often include certified turnover reporting as a condition of renewal

Statutory Audit Exemption vs. GTO Audit Requirements

Under Section 205C of the Companies Act, private companies meeting 2 of 3 criteria for two consecutive financial years qualify for statutory audit exemption:

- Total annual revenue of $10 million or less

- Total assets of $10 million or less

- 50 employees or fewer

This exemption applies strictly to financial statement audits under the Companies Act — it does not override contractual GTO audit obligations. A small F&B tenant exempt from statutory audit must still engage an ACRA-licensed auditor if the tenancy agreement requires a GTO Certification Report.

Knowing where you stand on exemption status helps set the right audit timeline. Most GTO audits run annually, tied to the financial year-end and lease cycle.

Timing and Filing Deadlines

For tax purposes, align audit preparation with IRAS filing deadlines:

- ECI filing: All companies must file Estimated Chargeable Income within 3 months from the end of their financial year

- Waiver conditions: Companies with annual revenue of $5 million or below and nil ECI qualify for waiver

- Late filing consequence: IRAS may issue estimated assessments with no instalment payment option

What to Prepare Before Your Sales Audit in Singapore

The most common cause of audit delays and adverse findings is incomplete or poorly reconciled records. Get your documentation in order before the auditor arrives — not after.

Financial and Sales Records

Core financial documents needed:

- All sales invoices and receipts for the audit period

- Daily and monthly POS system reports and Z-reports

- Bank statements showing sales deposits, with entries matched to reported revenue

- Credit card and e-payment merchant statements (GrabPay, PayNow, Stripe, etc.)

- Management accounts or trial balance

POS records and bank statements must reconcile with each other. Any gaps between system-reported sales and actual deposits will be a primary auditor focus. Cash-heavy businesses (e.g., hawker-style F&B) require extra diligence. Without digital transaction trails, reconciliation is harder and auditor scrutiny increases.

GST and Tax Filing Records

Once your bank and POS records are reconciled, cross-check them against your GST filings. Singapore's IRAS GST submissions must align with the turnover figures reported in the audit — discrepancies are a significant red flag.

Action required:

- Pull your GST returns (F5 or F8) for the relevant period

- Verify that total taxable supplies align with the gross turnover figure

- Explain or correct any discrepancies before the audit begins

GST late payment penalties escalate rapidly: an initial 5% penalty, followed by an additional 2% per month for continued non-payment, capped at 50% of the unpaid tax amount.

Contractual and Agreement Documents

Auditors must first understand the terms of any tenancy agreement, franchise agreement, or revenue-sharing contract to determine how "gross turnover" is defined. Definitions vary by lease:

| Item | Typical Treatment |

|---|---|

| POS sales (dine-in, takeaway) | Included |

| Online/e-commerce sales from premises | Included |

| Delivery platform sales (GrabFood, Foodpanda) | Included (varies by lease) |

| Voucher and loyalty redemptions | Included (varies by lease) |

| GST collected | Excluded |

| Refunds and returns | Excluded |

| Staff meals and complimentary items | Excluded |

| Staff discounts | Excluded |

Retrieve and review your agreements ahead of time so you understand what is and isn't counted as reportable GTO.

Internal Records and Operational Data

Supporting records that auditors may cross-reference:

- Inventory and stock movement records (to validate that goods sold align with turnover)

- Payroll data (relevant for F&B to correlate staff activity with revenue)

- Records from third-party platforms like GrabFood, Shopee, or Lazada

- Void and refund logs with proper approval trails

Step-by-Step: How to Prepare for a Sales Audit in Singapore

Sales audit preparation moves through distinct stages — and businesses that work through each one systematically are far less likely to face findings, disputes, or delays when the auditor arrives.

Step 1: Review Your Contractual Obligations

Begin by reading your tenancy agreement, franchise contract, or revenue-sharing arrangement carefully.

Key elements to identify:

- Exact definition of "gross turnover" in your contract

- Reporting period and required submission format

- Specific exclusions allowed (e.g., GST, voids, refunds)

- Deadline for submitting audited GTO statement

Misunderstanding contractual definitions is a leading cause of GTO underreporting findings. Knowing what to include or exclude upfront prevents post-audit disputes.

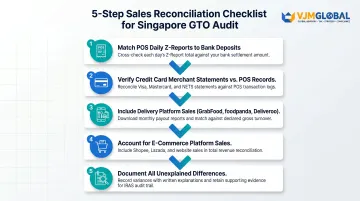

Step 2: Reconcile Your Sales Records

Cross-check all sales channels — POS data, online platforms, cash sales — against bank deposits and accounting records.

Reconciliation checklist:

- Match POS daily Z-reports to bank deposits

- Verify credit card merchant statements align with POS records

- Include delivery platform sales (GrabFood commission structures can create confusion)

- Account for e-commerce platform sales (Shopee, Lazada)

- Document any unexplained differences with clear explanations

Any discrepancies should be investigated and documented before the auditor reviews them.

Step 3: Verify GST Filings Against Sales Data

Once your sales records are reconciled, the next check is confirming that GST returns filed with IRAS throughout the year match the sales figures being reported in the audit.

Verification process:

- Pull GST filings (F5/F8) for the audit period

- Confirm that total taxable supplies align with gross turnover figure

- Address any discrepancies — either explain or correct them before the audit begins

According to IRAS guidance on compliance priorities, businesses in the digital economy — particularly those with multiple income streams — face heightened risk of GST audit selection.

Step 4: Implement or Tighten Internal Controls

Review and tighten existing processes for recording and reporting sales, focusing on these key control points:

- POS systems properly integrated with accounting software

- Void/refund processes documented and approved

- Daily cash-up procedures consistent and recorded

- Multi-channel sales aggregation automated where possible

- Regular (quarterly) internal reconciliation reviews

Auditors specifically look for control weaknesses during fieldwork. Businesses that demonstrate systematic, well-controlled processes give auditors more confidence and typically experience faster, cleaner audits.

Foreign companies with limited Singapore compliance experience often benefit from working with a cross-border advisory firm to structure their controls and reconcile financial records before engaging a local auditor. VJM Global supports international businesses navigating Singapore's regulatory requirements as part of broader cross-border compliance work.

Step 5: Engage a Qualified ACRA-Registered Auditor

In Singapore, only public accountants registered with the Accounting and Corporate Regulatory Authority (ACRA) can issue certified sales turnover reports acceptable to landlords and regulatory bodies.

Selection criteria:

- Specific experience in GTO audits for your industry (retail, F&B, franchise)

- Familiarity with Singapore's IRAS and ACRA requirements

- Track record of producing reports accepted by major mall operators

- Clear engagement terms and timeline expectations

Critical timing: Engage your auditor before the audit period ends — early engagement allows time for proper planning, document requests, and resolving any issues before fieldwork begins.

Common Mistakes That Derail Sales Audit Preparation

Most sales audit complications are self-inflicted. The three patterns below account for the majority of discrepancies auditors flag — and each one is avoidable.

Mistake 1: Waiting Until the Last Minute to Organize Records

Businesses that attempt to reconstruct months of sales data in the days before an audit often discover:

- Missing key documents (daily Z-reports, bank statements)

- Inconsistencies between sources (POS vs. bank deposits)

- Inability to explain discrepancies (cash shortfalls, unexplained adjustments)

This delays the audit and signals poor internal controls, triggering deeper scrutiny from auditors.

Mistake 2: Misunderstanding What "Gross Turnover" Includes

Many businesses misreport GTO simply by not reading the contractual definition — either excluding items that should be included, or counting items that should be stripped out.

Frequent errors:

- Excluding third-party delivery platform sales (GrabFood, Foodpanda) without lease authorization

- Treating GST collected as part of turnover

- Omitting service charges or online marketplace sales

- Failing to deduct authorized exclusions (staff meals, refunds)

Misreading the GTO clause — even once — can mean underreporting or overreporting revenue, leading to disputes with landlords or franchisors.

Mistake 3: Neglecting to Reconcile Digital and Offline Sales Channels

Businesses operating across multiple channels frequently:

- Report only one channel's data (e.g., physical store but not e-commerce)

- Fail to aggregate all revenue sources correctly

- Miss delivery platform sales that don't flow through the POS system

- Exclude cash sales or offline transactions

Auditors test every channel. Any omission without documented justification is treated as a discrepancy.

IRAS enforcement data confirms the risk: Between July 2020 and June 2023, IRAS recovered $79 million in taxes and penalties from companies with erroneous CIT returns, with cases selected using advanced data analytics achieving approximately 3 times the recovery per case compared to random samples.

Frequently Asked Questions

What is the difference between a sales audit and a GTO audit in Singapore?

A sales audit covers both performance (evaluating sales processes and team effectiveness) and financial dimensions, while a GTO audit specifically verifies the accuracy of gross turnover figures for tax compliance and contractual obligations like rent calculations. The GTO audit is a compliance-driven financial examination required by landlords and franchisors.

Who can conduct a sales audit in Singapore?

Only public accountants registered with ACRA are authorised to issue certified GTO audit reports in Singapore. Check your auditor's ACRA registration and confirm they have GTO audit experience in your industry — retail, F&B, or franchising.

Do small companies exempt from statutory audit still need a sales turnover audit?

Yes. Statutory audit exemptions under Singapore's Companies Act are separate from GTO audit requirements, which are driven by tenancy or franchise agreement terms. Even a small retailer qualifying for ACRA's audit exemption must still engage an auditor if the lease requires a GTO certification.

What happens if discrepancies are found during a sales audit in Singapore?

The auditor will note findings in the report, and the business may need to revise financial statements or GST filings. Landlords or franchisors may seek back payments for underreported turnover. Repeated or serious discrepancies can also trigger IRAS scrutiny — penalties reach up to 2x the tax undercharged, with criminal prosecution possible for fraud.

How long does a sales audit typically take in Singapore?

A straightforward GTO audit for a single-outlet retailer typically takes one to three weeks. Businesses with multiple revenue channels, cash-heavy operations, or incomplete records should expect three to six months from engagement to final report delivery.

How often should a business in Singapore conduct a sales audit?

Most GTO audits are required annually under tenancy or franchise agreements, timed to the financial year-end. Quarterly internal reconciliations reduce the formal audit burden and catch discrepancies early — when they're far easier to resolve.