Getting this right matters more than many employers realise. Research from CIPP and Zellis found that 59% of employees experienced a negative impact on their mental health due to payroll errors, with mistakes costing UK firms approximately £700 million annually. That figure covers HMRC penalties, admin overhead, and the harder-to-quantify cost of eroded staff trust.

This guide is written for UK employers, HR managers, and foreign businesses establishing operations in the UK. It covers what UK payroll processing involves, how each step works, the compliance obligations you must meet, and how to choose the right delivery model for your business.

Key Takeaways

- UK payroll runs through HMRC's PAYE system — registration is required before your first payday

- Every pay run requires a Full Payment Submission (FPS) sent to HMRC on or before payday

- Employers are responsible for minimum wage, NICs, pension auto-enrolment, SSP, and statutory holiday pay

- Compliance responsibility stays with the employer, whether payroll is run in-house or outsourced

- Late or missing FPS submissions carry penalties from £100 to £400 per month, depending on headcount

What Is UK Payroll Processing?

UK payroll processing is the end-to-end cycle of calculating employee wages, applying correct tax codes and deductions, issuing payslips, and reporting to HMRC on or before each payday.

It covers two sides of the employer's obligation:

- What employees receive: net pay after Income Tax, National Insurance, and other deductions

- What the business owes: Employer NICs, pension contributions, and any statutory payment adjustments

When handled correctly, payroll keeps employees paid on time, satisfies HMRC's reporting requirements, and keeps the business compliant with UK employment and tax law.

How the UK System Differs

The defining feature of the UK system is Real-Time Information (RTI). Since HMRC introduced RTI in April 2013, every employer must submit payroll data each time employees are paid. This replaced the old P35/P14 annual return model, shifting from once-a-year reporting to submission on or before every payday.

The practical result: HMRC holds up-to-date pay data at all times, rather than waiting until tax year-end to reconcile records.

A few terms useful to know when navigating the UK system:

- Payroll software — the tool used to calculate and submit payroll

- A payroll bureau — a third-party provider that runs payroll on your behalf

- Payroll year-end — the annual reporting cycle, including issuing P60s

Setting Up UK Payroll: What You Need Before You Start

Getting payroll wrong from the start can trigger HMRC penalties — so completing these setup steps before your first payday matters.

PAYE Registration

Employers must register with HMRC as an employer before their first payday. You can register up to two months in advance but no earlier. Upon registration, HMRC issues:

- An employer PAYE reference number — required for all payroll submissions

- A 13-character Accounts Office reference number — used for making PAYE payments

Employee Data Required

Before the first payroll run, collect the following for each employee:

- P45 from their previous employer (or a completed New Starter Checklist if no P45 exists)

- National Insurance number

- Tax code (from P45 or HMRC notification)

- Bank account details

- Signed employment contract

- Pension enrolment status

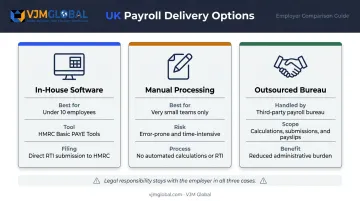

Choosing How to Run Payroll

There are three main options:

- In-house software — Use HMRC-compatible payroll software to calculate and submit directly. HMRC's free Basic PAYE Tools is available for employers with fewer than 10 employees.

- Manual in-house processing — Possible for very small teams but error-prone and time-intensive.

- Outsourced payroll bureau or accountant — A third party handles calculations, submissions, and payslips on your behalf.

Outsourcing payroll does not transfer legal responsibility. GOV.UK confirms that you remain legally responsible for all PAYE tasks, even when a third party handles them.

Auto-Enrolment Pension Duties

From day one, eligible employees must be enrolled in a workplace pension scheme. Eligibility applies to workers aged 22 to State Pension Age earning over £10,000 per year (or £833/month, £192/week).

Current minimum contribution rates (in effect since April 2019):

| Contributor | Minimum Rate |

|---|---|

| Employer | 3% |

| Employee | 5% |

| Total | 8% |

Pension contributions are calculated on qualifying earnings and must be deducted as part of every payroll run.

How UK Payroll Processing Works: Step by Step

Here is the full payroll cycle, from data collection to HMRC payment.

Step 1: Collect and Verify Employee Data

Each pay period begins with gathering accurate inputs: hours worked, confirmed salaries, bonuses, overtime, absences, and any mid-period changes to tax codes or personal details. Errors at this stage flow through every subsequent calculation. A verification checkpoint here catches mistakes before they affect deductions, net pay, and HMRC submissions.

Step 2: Calculate Gross Pay

Gross pay includes:

- Basic salary or hourly rate × hours worked

- Overtime, bonuses, and commissions

- Statutory payments (Statutory Sick Pay, Statutory Maternity Pay where applicable)

Each payment type carries different tax treatment — categorise each correctly before moving to deductions.

Step 3: Calculate Deductions

Mandatory deductions for most employees include:

- Income Tax — calculated using the employee's HMRC-assigned tax code and the UK's progressive rate bands

- Employee NICs — Class 1 contributions based on the employee's NI category letter

- Pension contributions — auto-enrolment deductions (note: salary sacrifice arrangements are pre-tax; standard contributions are post-tax)

- Student loan repayments — where applicable based on plan type and earnings threshold

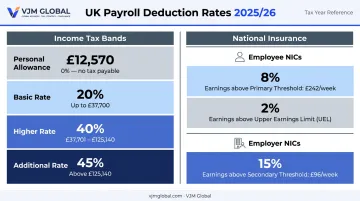

Current 2025/26 rates:

| Deduction | Rate / Threshold |

|---|---|

| Personal Allowance | £12,570 |

| Basic rate Income Tax (20%) | Up to £37,700 above allowance |

| Higher rate (40%) | £37,701–£125,140 |

| Additional rate (45%) | Above £125,140 |

| Employee NICs (Category A) | 8% from Primary Threshold (£242/week) to Upper Earnings Limit; 2% above |

| Employer NICs | 15% above Secondary Threshold (£96/week) from April 2025 |

Step 4: Calculate Net Pay and Approve

Net pay = gross pay minus all deductions. Before releasing payments, a payroll manager or HR lead should review:

- Net pay figures for every employee

- Total payroll cost including Employer NICs

- Confirmation that all data inputs are accurate and up to date

Step 5: Issue Payslips and Make Payments

Under the Employment Rights Act 1996, every worker has the right to an itemised pay statement at or before payday. Payslips must show:

- Gross pay and net pay

- Each deduction itemised (variable and fixed)

- Hours worked where pay varies by time

- Tax code

Payments are typically made via Bacs Direct Credit, which follows a three-working-day processing cycle — so payment runs need to be initiated ahead of the contractual payday.

Step 6: Submit FPS and Pay HMRC

Two key submissions and one payment deadline:

- Full Payment Submission (FPS): Must reach HMRC on or before payday — not after. This reports each employee's pay, tax, and NICs in real time.

- Employer Payment Summary (EPS): Filed by the 19th of the following month to claim statutory payment reductions, Employment Allowance, or report nil payment.

- PAYE/NICs payment: Due by the 22nd of the following month for electronic payment (19th if paying by post).

With the cycle complete, the next step is understanding what can go wrong — and how to stay compliant when it does.

Key UK Payroll Laws and Compliance Requirements

National Minimum Wage and National Living Wage

Rates are age-dependent and updated each April. Current rates (April 2025–March 2026):

| Age Group | Hourly Rate |

|---|---|

| 21 and over (National Living Wage) | £12.21 |

| 18–20 | £10.00 |

| Under 18 | £7.55 |

| Apprentice | £7.55 |

Employers must track hours to demonstrate compliance. Violations carry significant financial penalties.

Statutory Sick Pay (SSP)

From 6 April 2026, SSP rules change in a meaningful way. Key figures to know:

- First-day eligibility: SSP is now paid from day one of sickness — the previous three waiting days rule no longer applies

- Weekly rate: £123.25 or 80% of average weekly earnings, whichever is lower

- Maximum duration: Employers pay SSP for up to 28 weeks

- Lower Earnings Limit: Employees must earn at least £129/week to qualify

Holiday Entitlement

Almost all workers are entitled to 5.6 weeks paid holiday per year — 28 days for a standard five-day-week worker. Part-time entitlement is calculated pro-rata.

For irregular-hours and part-year workers, reforms effective from 1 April 2024 apply holiday accrual at 12.07% of actual hours worked per pay period. Holiday pay is one of the most frequently miscalculated elements in UK payroll — double-check accrual rates every time you run payroll for variable-hours staff.

Record Keeping

Employers must retain payroll records — including pay data, HMRC reports, tax code notices, and employee absence records — for a minimum of three years from the end of the relevant tax year. HMRC can request inspection at any time.

Common UK Payroll Mistakes and Misconceptions

Three Persistent Misconceptions

- Outsourcing does not transfer compliance liability. The employer remains legally responsible for PAYE accuracy regardless of who processes payroll.

- There is no statutory 13th-month bonus in the UK. Bonuses are either contractual or entirely discretionary, per ACAS guidance.

- Casual or self-employed workers are not automatic PAYE exemptions. Classification determines liability. Under IR35 off-payroll working rules (revised April 2021), medium and large private-sector clients must determine a worker's employment status for tax purposes — not the worker.

Where Operational Errors Happen

These misconceptions create the conditions for real operational mistakes. The most common ones are:

- Wrong tax code on new starters — without a P45, the wrong default code gets applied and can persist for months

- Missed employee change notifications — failing to update HMRC about pay changes, new starters, or leavers mid-year creates reconciliation problems at year-end

- Late FPS submissions — even one missed submission can trigger an HMRC late filing penalty

- Worker misclassification — treating an employee as a contractor to avoid PAYE is the highest-risk mistake, carrying potential back-tax liability and penalties

Timing Confusion

Two deadlines consistently catch employers off guard:

- FPS submission: Must be filed on or before payday in most cases — not the day after.

- HMRC payment deadline (22nd): This is not a payday. It is the deadline to pay the tax and NICs owed for the previous tax month.

In-House vs. Outsourced UK Payroll

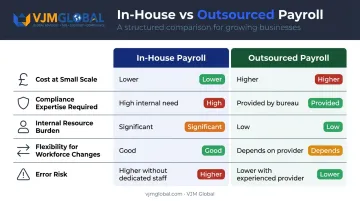

Side-by-Side Comparison

| Factor | In-House | Outsourced |

|---|---|---|

| Cost at small scale | Lower | Higher |

| Compliance expertise required | High | Provided by bureau |

| Flexibility for workforce changes | Good | Depends on provider |

| Internal resource burden | Significant | Low |

| Error risk | Higher without dedicated staff | Lower with experienced provider |

When Outsourcing Makes Sense

Outsourcing is typically the right call for:

- Foreign companies entering the UK with no prior exposure to PAYE, RTI, or UK employment law

- Businesses without dedicated HR or finance staff who can monitor compliance consistently

- Operations with seasonal or contractor-heavy workforces, where headcount changes frequently

- Growing companies whose compliance burden is outpacing their internal capacity

VJM Global has supported 250+ UK businesses across 15+ industries, providing accounting and payroll compliance services tailored to companies establishing UK operations for the first time. This includes PAYE registration, RTI submissions, and pension auto-enrolment — areas where first-time errors carry real penalties.

Knowing when to outsource is only half the equation. The quality of the provider matters just as much.

What Good Outsourced Payroll Looks Like

When evaluating a payroll provider, ask:

- Are they CIPP-accredited or do they hold equivalent payroll compliance credentials?

- How do they handle GDPR and employee data security? ISO 27001 certification is a meaningful benchmark.

- When an error occurs, what is their rectification process — and who is accountable?

- Do they proactively communicate regulatory changes, such as April NMW rate updates or new HMRC thresholds, before they take effect?

Frequently Asked Questions

What is the payroll system in the UK?

The UK uses the Pay As You Earn (PAYE) system, administered by HMRC. Employers deduct Income Tax and National Insurance from employee wages each pay period and report all payments to HMRC in real time via Full Payment Submissions.

How long does payroll take to process in the UK?

Small businesses using payroll software can complete a run in minutes to a few hours. Manual payroll for larger teams typically takes one to three days. Data accuracy and employee headcount are the biggest factors affecting speed.

What documents are required to process payroll in the UK?

You need the following for each employee:

- P45 or completed New Starter Checklist

- National Insurance number

- Bank details and employment contract

- Pension enrolment information

At tax year-end, employers must also issue P60s to all employees still in employment on 5 April.

What is Real-Time Information (RTI) and why does it matter?

RTI is HMRC's system requiring a Full Payment Submission on or before every payday. Missing this deadline triggers late filing notices and financial penalties. It can also affect employees' Universal Credit payments or tax status, since HMRC uses FPS data to update those records.

Can a foreign company run payroll in the UK?

Yes: any foreign company employing staff in the UK must register as an employer with HMRC, obtain a PAYE reference number, and comply with all UK payroll obligations including RTI, NMW, and auto-enrolment pension duties. Where the parent company is based is irrelevant.

What are the penalties for missing HMRC payroll deadlines?

Late or missing FPS submissions attract monthly penalties based on scheme size:

| Employees | Monthly Penalty |

|---|---|

| 1–9 | £100 |

| 10–49 | £200 |

| 50–249 | £300 |

| 250+ | £400 |

HMRC generally waives the first failure in a tax year. For late PAYE and NIC payments, penalty rates escalate from 1% (1–3 defaults) to 4% (10+ defaults). A further 5% surcharge applies to amounts unpaid after six months, and another 5% after twelve months. Interest accrues daily at the Bank of England base rate plus 4%.