Introduction

Singapore businesses earning income from India — through IT services, consulting, technical fees, or royalties — face a critical compliance question: does their activity create a Permanent Establishment (PE) in India, and if not, how do they prove it to Indian payers?

The stakes are real. Without proper documentation, Indian clients must deduct tax at source at domestic rates of 20% or more — rates that doubled in April 2023 under India's Finance Act. A Singapore consultancy receiving S$500,000 annually from Indian clients could face S$25,000 in additional withholding tax for missing the right paperwork.

The India-Singapore Double Taxation Avoidance Agreement (DTAA) offers meaningful protection, but those benefits require a specific documentation package: a Tax Residency Certificate from Singapore's IRAS, Form 10F filed with Indian tax authorities, and a No PE Declaration confirming absence of taxable presence.

Understanding each of these requirements is what this guide covers — including the No PE Declaration itself, how the DTAA sets PE thresholds, what documents to prepare, and what's at stake financially if you get it wrong.

TLDR

- A No PE Declaration confirms no taxable India presence, allowing Indian payers to apply reduced DTAA withholding rates instead of full domestic rates of 20–40%

- Without this declaration, Indian clients will deduct significantly higher tax from every payment, reducing your net revenue by 5-10 percentage points or more

- You need three documents: Tax Residency Certificate from IRAS, Form 10F filed electronically on India's tax portal, and a signed No PE Declaration on company letterhead

- The India-Singapore DTAA provides a 90-day threshold for Service PE and reduced withholding rates, but these benefits require proper documentation

- India's MLI adoption introduced the Principal Purpose Test, making genuine commercial substance in Singapore more important than ever

What Is a No PE Declaration and Why It Matters for Singapore Businesses

A No PE Declaration is a written statement by a non-resident entity confirming that its activities in India do not constitute a Permanent Establishment under the Income Tax Act, 1961 (Section 92F(iiia)) and the applicable DTAA. This declaration allows Indian payers to apply treaty-reduced withholding tax rates instead of domestic rates.

The core principle: foreign enterprise profits are exempt from Indian tax unless attributable to a PE within India. Without PE, income such as fees for technical services (FTS), royalties, or business profits can be taxed only in Singapore under treaty provisions.

Section 90 of the Income Tax Act lets taxpayers apply whichever rate — domestic or treaty — is more beneficial. That choice is where the No PE Declaration earns its value.

When a Singapore company receives payment from an Indian client for software development, consulting, or financial advisory services, the Indian payer must deduct tax at source (TDS). The No PE Declaration, along with a Tax Residency Certificate (TRC) and Form 10F, is the mechanism to trigger DTAA rates instead of the default 20–40% domestic rates.

The rate difference is significant — as the table below shows:

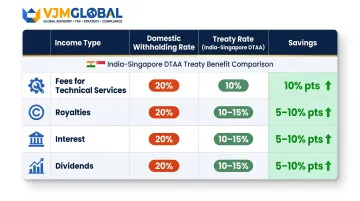

Domestic vs. Treaty Rates (AY 2026-27):

| Income Type | Domestic Rate | Treaty Rate (India-Singapore) | Savings |

|---|---|---|---|

| Fees for Technical Services | 20% | 15% | 5 percentage points |

| Royalties | 20% | 10-15% | 5-10 percentage points |

| Interest | 20% | 10-15% | 5-10 percentage points |

| Dividends | 20% | 10-15% | 5-10 percentage points |

India's Finance Act 2023 doubled the domestic withholding tax rate on royalties and FTS from 10% to 20%, effective April 1, 2023, making DTAA treaty rates significantly more valuable.

Critical clarification: The No PE Declaration is not a government-issued certificate. It is a self-declaration on company letterhead submitted to the Indian payer and tax authorities. It must be consistent with actual operations — no fixed office in India, no dependent agents with contract authority, and services performed entirely outside India.

A January 2026 Supreme Court ruling reversed an earlier Delhi High Court position that TRCs are "sacrosanct," establishing that Indian tax authorities can inquire into commercial substance beyond the documentation itself. Your No PE Declaration must therefore reflect genuine operational reality — not just paperwork. VJM Global works with Singapore and other foreign businesses to prepare and file No PE declarations, Form 10F, and related India compliance documentation that holds up under scrutiny.

Types of PE That Singapore Businesses Must Understand

Indian law and the India-Singapore DTAA recognize multiple PE types, each with different triggers. Singapore companies must assess their exposure against each type before submitting a No PE Declaration.

Fixed Place PE

Fixed Place PE arises when a Singapore company has a fixed geographical location in India — office, branch, workshop, factory, or even a habitually used co-working space — through which it wholly or partly carries on business.

Three tests apply:

- The place must be at the entity's disposal (not just visiting a client's office)

- It must be fixed in character, not temporary or preparatory

- Commercial business activities must be conducted from it

Article 5(2) of the India-Singapore DTAA provides an inclusive list: place of management, branch, office, factory, workshop, mine, oil/gas well, quarry, or extraction site.

Construction and installation sites lasting more than 183 days in any fiscal year constitute PE under Article 5(3). Supervisory activities connected to such projects also create PE if they continue beyond 183 days. Installations used for exploration or exploitation of natural resources create PE only if used for more than 120 days.

Exclusions: Article 5(7) provides that facilities solely for storage, display, occasional delivery, purchasing goods, or auxiliary activities like advertising or information collection do not create PE.

Service PE

Service PE arises when a Singapore company's employees or contractors provide services in India beyond a treaty-specified duration. Under Article 5(6) of the India-Singapore DTAA, this threshold is 90 days in any fiscal year (April-March). For services performed for a related enterprise, the threshold drops to just 30 days.

Singapore IT firms and consulting companies frequently trigger this threshold by regularly deploying personnel to Indian client sites. The Delhi High Court confirmed in December 2025 that physical presence in India is required for the 90-day threshold to be met under this treaty.

Key considerations:

- The threshold is measured per Indian fiscal year, not a rolling 12-month period

- Days are counted cumulatively across all personnel

- Even one day of presence counts as a full day

- Travel logs and assignment records are critical evidence

Agency (Dependent Agent) PE

Agency PE arises when a person in India — employee, agent, or subsidiary — habitually concludes contracts on behalf of the Singapore company or plays a principal role in contract conclusion.

Article 5(8) defines Agency PE as arising where a person acting on behalf of an enterprise:

- Has and habitually exercises authority to conclude contracts

- Habitually maintains stock from which goods are regularly delivered

- Habitually secures orders wholly or almost wholly for the enterprise

Critical distinction: Even if no physical office exists, an active sales representative or India-based director with contract authority can create PE. This risk is especially relevant for Singapore companies using Indian business development resources.

MLI impact: One important nuance affects how broadly Agency PE applies under this treaty. The Multilateral Instrument (MLI) protocol effective October 1, 2019 did not adopt the expanded Agency PE definition for the India-Singapore treaty (IRAS MLI Protocol).

The original "authority to conclude contracts" language remains in force. This is a narrower test than the "principal role leading to conclusion of contracts" standard adopted in some of India's other treaties — meaning Singapore businesses face a higher bar for Agency PE to be triggered than counterparts operating under those treaties.

India-Singapore DTAA: Critical PE Thresholds and Protections

The India-Singapore Double Taxation Avoidance Agreement (DTAA) is your primary shield against Indian taxation — but only if you stay within its thresholds. Article 5 defines PE and sets the limits Singapore businesses must respect to maintain No PE status. Both countries are signatories to the Multilateral Instrument (MLI), which has tightened several treaty provisions since 2020.

Treaty Income Protections

Singapore companies with No PE status benefit from significantly reduced withholding tax rates:

Article 12 (Royalties and FTS):

- Royalties and FTS: 15% (vs. 20% domestic rate)

- Royalties on industrial, commercial, or scientific equipment: 10% (vs. 20% domestic rate)

Article 11 (Interest):

- Bank loans: 10% (vs. 20% domestic rate)

- Other interest: 15% (vs. 20% domestic rate)

Article 10 (Dividends):

- 25%+ ownership: 10% (vs. 20% domestic rate)

- Other dividends: 15% (vs. 20% domestic rate)

Article 7 (Business Profits):

- Taxable in India only if PE exists — full exemption without PE

For a Singapore IT services company receiving S$1 million annually in FTS from Indian clients, the difference between 20% domestic TDS (S$200,000) and 15% treaty TDS (S$150,000) represents S$50,000 in annual savings — but only with proper documentation.

Principal Purpose Test (PPT)

The MLI introduced Article 29A (Prevention of Treaty Abuse) to the India-Singapore DTAA, effective January 1, 2020 for withholding taxes. Treaty benefits can be denied if one of the principal purposes of an arrangement is to obtain those benefits without sufficient commercial substance.

What this means for Singapore businesses:

- Your operations must have genuine substance in Singapore

- Actual decision-making must occur in Singapore (Board meetings, strategic decisions)

- Real contracts must be performed offshore, not routed through Singapore as a paper entity

- Simply having a Singapore address and TRC is no longer sufficient

The Supreme Court's January 2026 Tiger Global ruling reinforced this principle, establishing that TRCs do not bar inquiry into substance, control, or beneficial ownership.

Significant Economic Presence (SEP)

Beyond the PPT, Singapore businesses face a separate challenge under Indian domestic law. India's Finance Act 2018 introduced the Significant Economic Presence (SEP) concept under Section 9(1)(i), expanding the definition of "business connection." The CBDT notified thresholds effective April 1, 2022:

- Aggregate payments exceeding INR 2 crore (approximately S$320,000) in a year, OR

- Systematic engagement with 300,000 or more users in India

DTAA provisions override SEP for Singapore residents. A Singapore company exceeding these thresholds can still avoid Indian taxation by demonstrating absence of PE under Article 5 of the treaty. For digital, e-commerce, and software services companies — where SEP exposure is highest — that protection only holds with documented, defensible PE analysis.

Form 10F and No PE Declaration: The Documentation Singapore Businesses Need

Form 10F is a statutory form required under Section 90(5) of the Income Tax Act and Rule 21AB. It must be filed electronically on India's Income Tax portal by the non-resident (the Singapore company). Indian payers cannot legally apply DTAA rates without it.

Required Documents Package

1. Tax Residency Certificate (TRC) from IRAS

Confirms Singapore tax residency for the relevant financial year. The IRAS Certificate of Residence (COR) certifies that control and management of the business is exercised in Singapore. Online applications are processed within 7 working days and are free of charge.

2. Certificate of Incorporation

From Singapore's Accounting and Corporate Regulatory Authority (ACRA), confirming legal entity status.

3. Executed Contracts with Indian Clients

Contracts must explicitly state that services are performed outside India, specifying offshore delivery and Singapore-based project management.

4. No PE Declaration on Company Letterhead

Signed by an authorized director or officer, confirming:

- No fixed place of business in India

- No dependent agents with contract authority

- No personnel in India beyond treaty thresholds

- Services performed outside India

5. Activity Report

Describing the nature, duration, and location of services — including deliverables and confirmation that all core activities occur outside India.

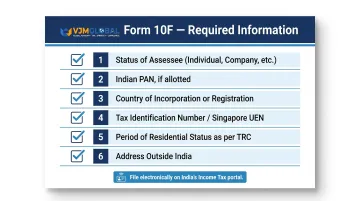

6. Form 10F

The form requires six categories of information:

- Status of the assessee (company, firm, etc.)

- Indian PAN if allotted

- Country of incorporation

- Tax Identification Number (Singapore UEN)

- Period of residential status as mentioned in TRC

- Address outside India

Electronic Filing Requirements

Once your documents are in order, the filing itself follows a defined process. DGIT Notification No. 03/2022 mandated electronic filing from July 16, 2022, and the relaxation for non-PAN holders expired September 30, 2023 with no further extension.

Singapore companies without Indian PAN must:

- Register on incometax.gov.in under "Non-Residents not holding and not required to have PAN"

- Verify mobile and email via OTP

- Upload TRC, address proof, and identification proof

- Set password and file Form 10F using foreign TIN (Singapore UEN)

File Form 10F for each financial year — ideally before the first payment is received.

How to Obtain a No PE Declaration: Process and Risks of Non-Compliance

Practical Process for Singapore Businesses

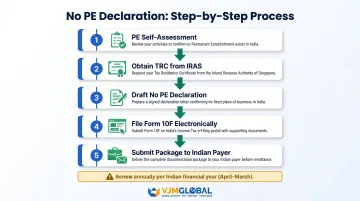

Step 1: Conduct PE Self-Assessment

Evaluate exposure against all PE types:

- Do you have any office, branch, or fixed location in India?

- Will any personnel spend 90+ days (or 30+ for related parties) in India?

- Do any India-based persons have authority to conclude contracts on your behalf?

Step 2: Obtain TRC from IRAS

Apply via mytax.iras.gov.sg for the relevant calendar year. Processing takes 7 working days. Ensure the TRC covers the period during which Indian payments will be received.

Step 3: Draft No PE Declaration

Prepare on company letterhead, signed by an authorized director. The declaration should state:

- Company name, registration number, and Singapore address

- Nature of services provided to Indian clients

- Confirmation that no PE exists in India under Article 5 of the India-Singapore DTAA

- Confirmation that services are performed outside India

- Statement that the company is a tax resident of Singapore

Step 4: File Form 10F Electronically

Register on the Indian Income Tax portal (if not already registered) and file Form 10F using your Singapore UEN. The form must be filed for each financial year.

Step 5: Submit Package to Indian Payer

Provide TRC, Form 10F acknowledgment, No PE Declaration, and supporting contracts to the Indian payer before receiving payment.

Annual Renewal: No PE Declarations are renewed annually (per Indian financial year: April-March). Update documentation if business activities or personnel deployments in India change materially.

VJM Global assists Singapore businesses with end-to-end preparation and filing of No PE declarations, Form 10F, and India compliance — so documentation holds up under assessment scrutiny.

Once the documentation package is in place, the bigger risk shifts to what happens if it isn't.

Consequences of Non-Compliance

Missing or defective documentation triggers two categories of exposure:

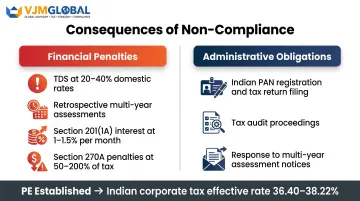

Financial penalties can compound quickly:

- Indian payers deduct TDS at domestic rates (20–40%) on gross payments

- Retrospective assessments covering multiple years with compounded interest

- Section 201(1A) interest: 1% per month for failure to deduct, 1.5% per month for late deposit

- Section 270A penalties: 50% of tax for under-reporting, 200% for misreporting

Administrative obligations follow immediately:

- File Indian tax returns and obtain an Indian PAN

- Undergo tax audit proceedings

- Respond to assessment notices, which can span multiple financial years

Beyond penalties, the tax rate exposure itself is significant. If PE is established, income attributable to India becomes subject to Indian corporate tax at 35% (foreign companies), with surcharge and cess bringing the effective rate to 36.40–38.22% depending on income level.

Best Practices to Avoid Inadvertent PE Creation

Proactive structuring is far less costly than retroactive remediation. The four areas below cover where PE risk most commonly materialises for Singapore businesses.

Personnel and Travel

- Keep India client-facing personnel below treaty thresholds (90 days; 30 days for related parties)

- Maintain detailed travel logs recording dates, purpose, and client names

- Track cumulative days across all employees per fiscal year

Contract and Service Structure

- Sign contracts in Singapore; specify offshore performance explicitly

- Include clauses confirming no fixed base in India

- Document that decision-making and strategic control remain in Singapore

Agents and Subsidiaries

- Do not grant India-based staff or agents authority to conclude contracts

- Ensure Indian subsidiaries (if any) operate independently with arm's-length arrangements

- Avoid habitual stock maintenance or order processing in India

Infrastructure and Presence

- Do not maintain inventory or dedicated server infrastructure in India

- Ensure any temporary presence qualifies as preparatory or auxiliary only

- Review PE position annually, given evolving MLI provisions and SEP rules, and update documentation when the business model changes

Frequently Asked Questions

What is a declaration for no permanent establishment in India?

It is a self-declaration by a non-resident entity (such as a Singapore company) submitted to Indian tax authorities or an Indian payer, confirming that its activities do not constitute a Permanent Establishment under the Income Tax Act or the India-Singapore DTAA, so the Indian payer can apply treaty-reduced withholding tax rates.

When does a Singapore company need to submit a No PE Declaration to an Indian payer?

Submit the declaration (with TRC and Form 10F) before receiving payment from an Indian client, so the payer can apply DTAA rates when deducting TDS. Renew it for each Indian financial year (April–March) or each new contract period.

What documents does a Singapore business need to file for a No PE Declaration in India?

Required documents include:

- TRC from IRAS

- Form 10F filed on the Indian Income Tax portal

- Company incorporation certificate

- Executed client contracts confirming offshore service delivery

- Activity report describing service location and nature

- Signed No PE Declaration on company letterhead

What is Form 10F and how does it relate to the No PE Declaration?

Form 10F is a statutory filing under Section 90(5) of the Income Tax Act that a non-resident must submit to claim DTAA treaty benefits. It works alongside the No PE Declaration and TRC — all three documents together enable Indian payers to legally apply reduced withholding tax rates instead of domestic rates.

How does the India-Singapore DTAA protect Singapore companies from PE-related taxation?

The DTAA sets specific PE thresholds — a Service PE typically requires 90+ days of personnel presence in India in any fiscal year. Singapore residents who document No PE status qualify for reduced withholding rates: FTS (15%), royalties (10–15%), and interest (10–15%).

What happens if a Singapore company's activities create a Permanent Establishment in India?

Once PE is established, India-attributable income is taxed at an effective corporate rate of 36.40–38.22% (including surcharge and cess), with compliance obligations covering PAN registration, annual returns, and tax audit. Retrospective assessments for prior years may also follow, carrying interest of 1–1.5% per month and penalties of 50–200% of the tax due.