Introduction

A Singapore-based IT services company routinely deployed its engineers to India to manage client projects, confident that the India-Singapore Double Taxation Avoidance Agreement (DTAA) shielded it from Indian taxes. That confidence proved costly: the Indian tax authority assessed it for an unregistered Permanent Establishment (PE) and issued a tax demand exceeding SGD 500,000, including interest and penalties spanning three financial years.

Cases like this are becoming more frequent. Singapore is India's largest source of Foreign Direct Investment (FDI), accounting for USD 174.9 billion over 25 years — nearly 24% of total FDI inflows — and bilateral trade reached USD 34.3 billion in FY 2024-25. As Singapore companies across IT services, trading, manufacturing, and financial services expand their India-facing operations, many underestimate the tax exposure created by physical footprints, employee deployments, and agent relationships.

The Finance Act 2024 reduced foreign company tax rates from 40% to 35%, but the effective rate still reaches 38.22% — more than 13 percentage points higher than the rate for domestic Indian companies.

Key Takeaways

- Under the India-Singapore DTAA, a PE arises through fixed presence, dependent agents, or service delivery — each with different triggers

- Service PE is triggered if Singapore employees work in India for more than 30 days (related parties) or 90 days (unrelated parties) in any fiscal year

- PE-attributable profits face effective tax rates of 36.40%–38.22%, depending on income type

- Day-count tracking, clear agent mandates, and proactive PE risk reviews are the primary tools for managing exposure

What Is Permanent Establishment Under the India-Singapore DTAA?

A Permanent Establishment is the threshold that determines whether India has the right to tax a foreign enterprise's profits derived from Indian operations. Under the India-Singapore DTAA (which entered into force on 27 May 1994), Article 5 governs this definition, overriding India's domestic Income Tax Act where the treaty terms are more favorable to the taxpayer.

Treaty vs. Domestic Law: Singapore businesses can elect to use the more favorable DTAA definition, but this protection only applies if:

- The entity qualifies as a tax resident of Singapore under the DTAA

- Specific conditions of the treaty are met

- The Principal Purpose Test (PPT) introduced via the Multilateral Instrument (MLI) in 2019 is satisfied

Business Connection vs. PE: Under Indian domestic law (Section 9 of the Income-tax Act, 1961), the concept of "business connection" applies a broader standard than treaty-based PE definitions. The DTAA shields Singapore entities from this broader domestic standard, but only if they maintain genuine Singapore tax residence and comply with treaty conditions.

Significant Economic Presence (SEP): The DTAA framework above addresses traditional PE exposure — but a separate domestic-law concept requires independent assessment. Since April 2022, India taxes non-resident digital businesses that cross either of these thresholds, even without any physical presence:

- INR 20 million in aggregate payments from Indian transactions

- 300,000 Indian users engaged during the year

This SEP rule operates under domestic law and may be overridden by DTAA provisions for treaty-eligible entities. Singapore-based e-commerce, SaaS, and digital platform companies should assess SEP exposure as a distinct risk from traditional PE analysis.

The Three Types of PE That Can Trap Singapore Businesses

Fixed Place PE

A Fixed Place PE arises when a Singapore company maintains a fixed, geographically defined location in India (such as an office, branch, factory, warehouse, or place of management) from which business is wholly or partly carried on. The location must be at the disposal of the entity, meaning the company has the right to use and control it.

The Disposal Test in Practice: If Singapore company employees use a dedicated floor of an Indian affiliate's office, work under the Singapore company's operational direction, and the space is not freely available to the Indian entity for other purposes, this is likely "at the disposal" of the Singapore entity. The Supreme Court's 2017 ruling in ADIT vs. E-Funds IT Solution Inc. established that mere access to premises is insufficient. The enterprise must have effective control over them, with sustained and substantive operational authority.

Common Trigger: Singapore companies establishing "coordination offices" or "project management hubs" in Indian coworking spaces or client premises risk Fixed Place PE if they maintain consistent, exclusive use over time.

Dependent Agent PE (DAPE)

A Dependent Agent PE arises when a person in India (individual, distributor, or company) habitually acts on behalf of the Singapore company and either:

- Has and habitually exercises authority to conclude contracts in India on the Singapore company's behalf, or

- Habitually maintains a stock of goods for delivery on its behalf

The word "habitually" is critical : a one-off contract does not create DAPE.

Singapore-Specific Risk: Indian distributors or commission agents operating under exclusive arrangements with Singapore companies frequently trigger DAPE. If the agent does not bear genuine entrepreneurial risk and acts solely for the Singapore principal, independence cannot be claimed.

The 2019 ITAT Delhi ruling in Hitachi High Technologies Singapore Pte Ltd confirmed this: liaison offices conducting pricing negotiations, order procurement, and contract execution constituted a PE, as those activities exceeded preparatory or auxiliary functions and represented core trading operations.

Post-MLI Clarification: The MLI added the Principal Purpose Test but did not modify Article 5's DAPE provisions for the India-Singapore DTAA. The standard remains "authority to conclude contracts" — not the broader "principal role leading to conclusion of contracts" found in newer treaties.

Service PE

A Service PE is created when a Singapore enterprise provides services in India through its own employees or other personnel for a specified period. Under the India-Singapore DTAA, the thresholds are:

| Relationship | Threshold | Measurement Period |

|---|---|---|

| Related/Associated Enterprise | More than 30 days | Any fiscal year |

| Unrelated Enterprise | More than 90 days | Any fiscal year |

Critical Clarification: Many assume the threshold is 183 days based on other treaties. For the India-Singapore DTAA, the 90-day threshold applies to unrelated parties; the 30-day threshold applies to intra-group arrangements. A Singapore software firm deploying engineers to support its Indian subsidiary's client delivery team for just five weeks (35 days) triggers the 30-day related-party service PE threshold.

Physical Presence Required: The Delhi High Court ruled in 2025 that physical presence of employees in India is mandatory for a Service PE under the India-Singapore DTAA. Remote service delivery from Singapore, without personnel physically present in India, should not by itself trigger Service PE, offering a meaningful safe harbor for remote and digital delivery models.

High-Risk Business Activities That Commonly Trigger PE for Singapore Companies

IT and Technology Services Exposure

Singapore hosts many regional IT, ITES, and software companies that regularly deploy technical staff or project managers to Indian clients or subsidiaries. Each visit is tracked cumulatively over the fiscal year, and the 30-day threshold for related-party services is easier to breach than most companies realize:

- A three-person team spending two weeks in Bangalore = 42 days

- Adding one follow-up visit = threshold exceeded

The Netflix case (2023) demonstrates real enforcement: Indian tax authorities attributed approximately INR 552.5 million (USD 6.73 million) to Netflix's PE in India for streaming services.

Trading and Distribution Risk

Technology services aren't the only exposure point. Singapore companies selling goods to India through exclusive Indian agents must also evaluate Dependent Agent PE (DAPE) risk if:

- The Indian counterpart maintains stock owned by the Singapore entity

- Orders are routed through the Indian party before Singapore confirmation

- The Indian agent's pricing authority extends beyond mere quotation

An "independent distributor" label offers no protection if the Indian party bears no genuine entrepreneurial risk.

Holding Company and Subsidiary Structure Risk

A common misconception is that a Singapore holding company with an Indian subsidiary is automatically protected. A subsidiary is not automatically a PE — but it becomes one if:

- Singapore-based directors make operational decisions for the Indian company

- Shared employees perform dual roles across both entities

- The Indian entity is effectively managed from Singapore (triggering Place of Effective Management residency risk)

Remote Work and Cross-Border Employee Risk

Post-2020, many Singapore companies have India-based employees working remotely who previously performed their roles in Singapore. This shift created PE exposure that most entities haven't fully assessed.

Where these employees work exclusively for the Singapore employer, their India-based activities can trigger PE if they:

- Conclude contracts or negotiate deals on behalf of the Singapore entity

- Service Indian customers directly in the role of a representative

- Work from a fixed home office location on a sustained, regular basis

Tax Consequences When a PE Is Established in India

Applicable Tax Rate

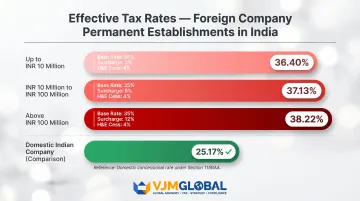

Profits attributable to a PE in India are taxed as foreign company income at the following rates:

| Income Slab | Base Rate | Surcharge | Health & Education Cess | Effective Rate |

|---|---|---|---|---|

| Up to INR 10 million | 35% | 0% | 4% | 36.40% |

| INR 10M to INR 100M | 35% | 2% | 4% | 37.13% |

| Above INR 100 million | 35% | 5% | 4% | 38.22% |

Indian domestic companies under Section 115BAA pay an effective rate of 25.17%—a gap of 13 percentage points. New manufacturing companies under Section 115BAB pay just 17.16%, widening that differential to over 21 percentage points.

Profit Attribution

PE taxation applies only to profits directly and effectively connected to the Indian PE—not the Singapore company's global profits. The arm's length principle governs transactions between the PE and its Singapore head office. India's Transfer Pricing rules under Chapter X of the Income-tax Act apply in full, with tax authorities closely scrutinizing inter-entity arrangements.

Common Pitfalls:

- Inflated management fees paid to Singapore

- Understated service charges from India

- Lack of economic substance in Singapore head office functions

Compliance Obligations Triggered

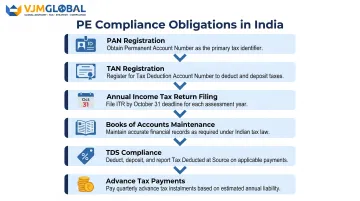

Once PE status is established, the Singapore entity must:

- Register with Indian tax authorities and obtain a Permanent Account Number (PAN)

- Obtain a Tax Deduction Account Number (TAN)

- File annual income tax returns as a foreign company (due 31 October)

- Maintain books of accounts as required under Indian law

- Comply with TDS (Tax Deducted at Source) obligations

- Pay advance tax in quarterly installments

Failure to register and file carries:

- Penalties under Section 271 (up to 200% of tax for concealment)

- Interest under Sections 234A, 234B, 234C (1% per month on unpaid tax)

- Heightened scrutiny in future Indian tax assessments and audits

Double Taxation Risk and Treaty Relief

The India-Singapore DTAA provides a credit mechanism to prevent double taxation. In practice, credit claims require close coordination between advisors in both jurisdictions. Singapore advisors must analyze the participation exemption and foreign tax credit rules carefully to confirm that Indian tax paid qualifies as creditable in Singapore.

How Singapore Businesses Can Mitigate PE Exposure

Structural Safeguards

- Use a properly registered Indian subsidiary rather than branch-like arrangements

- Ensure Indian agents or distributors bear real entrepreneurial risk and serve multiple clients

- Implement strict day-count monitoring for employee visits to India

- Limit the contracting authority of India-based staff through clear employment terms

Structural controls reduce PE exposure at the organizational level — but they need to be backed by consistent operational tracking.

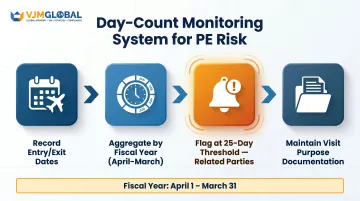

Day-Count Monitoring System

Implement a centralized tracking system that:

- Records each employee's entry/exit dates from India

- Aggregates days by fiscal year (April 1 – March 31)

- Flags when cumulative days approach 25 days (for related-party services)

- Maintains visit purpose documentation

Internal tracking gives you early warning — but for certainty on specific arrangements, a formal ruling may be appropriate.

Advance Ruling Option

The Board for Advance Rulings (BAR) replaced the Authority for Advance Rulings in September 2021. It allows foreign companies to obtain rulings on whether a proposed arrangement constitutes a PE. Unlike AAR rulings, BAR rulings are non-binding — significantly reducing their value as a certainty mechanism. Companies should combine BAR applications with Advance Pricing Agreements (APAs) for PE profit attribution certainty.

VJM Global's PE Risk Advisory

Singapore businesses already operating in India or planning to scale should conduct a formal PE risk assessment before the next financial year. VJM Global's Chartered Accountants and international tax professionals specialize in PE exposure reviews and India entry strategy — covering everything from activity mapping and structural restructuring to ongoing compliance monitoring.

Reach out at info@vjmglobal.com to schedule a PE risk review ahead of the next financial year.

Compliance Obligations Once Your PE Is Confirmed

| Obligation | Requirement | Deadline |

|---|---|---|

| PAN Registration | Mandatory for all income | Before first filing |

| TAN Registration | Required if making TDS payments | Before first TDS filing |

| Income Tax Return | Annual filing for foreign company | 31 October |

| Form 3CEB (TP Report) | International transactions (no threshold) | 31 October |

| GST Registration | Mandatory for Non-Resident Taxable Persons | Before commencing business |

Of these, transfer pricing documentation tends to be the most demanding obligation — and the one most commonly under-prepared.

Transfer Pricing Documentation

Where cross-border intra-group transactions exceed INR 10 million (1 crore), detailed TP documentation under Rule 10D (Local File) is required. The Singapore entity must annually:

- Determine profits attributable to its Indian PE

- Apply arm's length pricing to intra-entity transactions

- Maintain real-time documentation (prepared during the transaction year)

- File certified Form 3CEB through a Chartered Accountant

How VJM Global Supports PE Compliance

VJM Global handles the full compliance cycle for Singapore companies with confirmed PE in India, including:

- PAN and TAN registration

- GST registration for Non-Resident Taxable Persons

- Income tax return filing and TDS compliance

- Bookkeeping and management reporting

- Transfer pricing documentation and Form 3CEB filing

This means Singapore businesses can meet their Indian obligations without building a local finance team from the ground up.

Frequently Asked Questions

Frequently Asked Questions

What is a permanent establishment in India?

A PE in India is a taxable presence created when a foreign enterprise operates in India through a fixed place of business, a dependent agent, or by providing services for a specified duration. This gives India the right to tax profits attributable to those Indian operations.

How to determine PE in India?

PE determination involves applying the relevant DTAA provisions (such as India-Singapore DTAA Article 5) to the specific facts of the business, examining physical presence, agent relationships, and employee deployment duration. Indian domestic law is then compared against the treaty, and whichever is more favorable to the taxpayer applies.

What is the tax rate for permanent establishment in India?

Foreign company PEs in India are taxed at effective rates of 36.40% to 38.22% depending on income slab (including base rate of 35%, surcharge, and cess). Confirm current rates with a tax advisor — rates update with each Finance Act.

What is the 183-day rule for permanent establishment?

The 183-day threshold applies to construction/installation PEs under certain treaties. For the India-Singapore DTAA Service PE, the thresholds are 90 days for unrelated parties and 30 days for related parties in any fiscal year, which is much shorter than most businesses assume.

How to avoid permanent establishment risk in India?

Key mitigation approaches include:

- Using a registered Indian subsidiary rather than unstructured branch operations

- Ensuring Indian agents are genuinely independent

- Strictly monitoring employee day-counts in India

- Limiting contracting authority of India-based staff

- Seeking a formal PE risk review from qualified advisors

What happens if you have a permanent establishment?

Once a PE is established, the foreign entity must register with Indian tax authorities, file income tax returns on attributable profits, and comply with TDS, GST, and local accounting obligations. Non-compliance attracts penalties of up to 200% of tax, interest at 1% per month, and reputational consequences.