Introduction

Singapore ranks as India's 2nd-largest foreign direct investor, with cumulative FDI equity inflows totalling approximately USD 171.92 billion — representing nearly 24% of India's total FDI. Bilateral trade in goods reached S$35.01 billion in 2025 alone. Yet when Singapore companies earn income from Indian operations — dividends from an Indian subsidiary, royalties for licensed technology, interest on cross-border loans, or fees for technical services — many face an unwelcome surprise: the same income taxed twice.

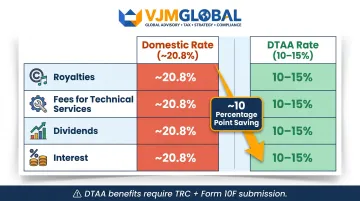

India's withholding tax regime under Section 195 of the Income Tax Act requires Indian payers to deduct TDS from payments to foreign companies at domestic rates as high as 20% (approximately 20.8% with surcharge and cess) before treaty relief is applied. Without proper planning and documentation, the same income is taxed again when remitted to Singapore. That double tax burden can erode profitability by 10 percentage points or more.

This guide covers what Singapore businesses need to claim treaty protection and stay compliant:

- The India-Singapore DTAA and its reduced withholding rates (10–15% vs. 20%+)

- Three methods to eliminate or reduce double taxation

- A step-by-step process to claim treaty benefits, including required documents

- Critical filing deadlines — miss Form 67 and you forfeit your credit for that entire year

- The most common compliance pitfalls that trigger avoidable tax liabilities

Key Takeaways

- India and Singapore maintain a comprehensive DTAA that caps withholding tax rates at 10-15% (vs. 20%+ domestic rates) on dividends, interest, royalties, and fees for technical services

- Singapore businesses must actively claim treaty benefits — obtain a Tax Residency Certificate from IRAS and file Form 10F on India's income tax portal before income is paid

- **Form 67 must be filed by 31 March of the relevant assessment year** to claim Foreign Tax Credit; missing this deadline forfeits relief entirely

- The 2016 Protocol ended capital gains exemption: shares in Indian companies acquired after 1 April 2017 are now taxable in India

- A 90-day service PE threshold (not 183 days) applies under the India-Singapore DTAA, so companies deploying personnel to India must track presence days carefully

Why Singapore Businesses Face Double Taxation on India Income

The Source vs. Residence Conflict

Double taxation arises because India taxes at source (where income arises) while Singapore taxes on remittance basis (when funds are brought into Singapore). When a Singapore company earns royalties from licensing technology to an Indian manufacturer, India claims taxing rights because the income "arises" in India. Singapore then taxes the same income on remittance.

Without the India-Singapore DTAA, the same ₹100 of income could face 20.8% Indian withholding tax plus Singapore's 17% corporate rate. This affects real money: bilateral trade in goods reached S$35.01 billion in 2025, with Singapore-based technology, financial services, and manufacturing companies deriving substantial passive income from Indian operations.

India's Withholding Tax Regime Under Section 195

Section 195 of the Indian Income Tax Act requires any person making a payment to a non-resident that is chargeable to tax in India to deduct tax at source (TDS). For foreign companies receiving dividends, interest, royalties, or fees for technical services, the domestic withholding rates before DTAA relief are:

| Income Type | Domestic WHT Rate (before surcharge/cess) | Effective Rate (approx.) |

|---|---|---|

| Royalties | 20% | ~20.8% - 21.84% |

| Fees for Technical Services (FTS) | 20% | ~20.8% - 21.84% |

| Dividends | 20% | ~20.8% - 21.84% |

| Interest (general) | 20% | ~20.8% - 21.84% |

The India-Singapore DTAA reduces these rates to 10-15% — a roughly 10 percentage point saving — but only if the Singapore company completes the procedural steps outlined later in this guide.

Permanent Establishment (PE) Exposure

If a Singapore company maintains employees, offices, or agents in India, it may trigger a Permanent Establishment under Article 5 of the India-Singapore DTAA. Once a PE is established, the company's Indian-attributable business profits become taxable in India at the full foreign company rate (which can reach 40%+ with surcharge and cess), not just withholding tax.

Two thresholds matter most for Singapore companies deploying staff in India:

- Service PE threshold: 90 days in any fiscal year (or just 30 days for services to related enterprises) — far shorter than the 183-day threshold in most treaties

- Passive income carve-out: Dividends, royalties, and interest without a PE are taxed only at DTAA withholding rates, not full business profit rates

Companies sending consultants, engineers, or technical staff to India must track presence days against these thresholds carefully.

Singapore's Territorial Tax System and Foreign-Sourced Income Exemption

Singapore's Income Tax Act follows a modified territorial system: foreign-sourced income is generally taxable only when remitted to and received in Singapore, provided three conditions are met under Section 13(8):

- The income was subject to tax in the foreign jurisdiction

- The headline corporate tax rate of the foreign jurisdiction is at least 15% at the time of receipt

- The Comptroller is satisfied the exemption is beneficial

India's headline corporate tax rate exceeds 15%, so dividends, branch profits, and service income from India typically qualify for this exemption when remitted to Singapore. That said, the exemption isn't automatic — and in some structures, claiming DTAA foreign tax credits produces a better outcome. Understanding both mechanisms is essential before deciding how to structure Indian income flows.

The India-Singapore DTAA: Key Rates and What It Covers

Background and Treaty Timeline

The India-Singapore DTAA was first signed on 24 January 1994 and entered into force on 27 May 1994. It has been amended through three major Protocols:

| Event | Date |

|---|---|

| Original treaty signed | 24 January 1994 |

| Entry into force | 27 May 1994 |

| 1st Protocol (amended) | 18 July 2005 |

| 2nd Protocol | 24 June 2011 |

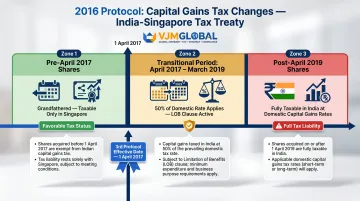

| 3rd Protocol (capital gains) | 30 December 2016 |

| MLI application | 1 October 2019 |

The 2016 Protocol fundamentally changed the treaty's capital gains provisions, ending Singapore's prior advantage of tax-free capital gains on Indian shares and closing a widely used routing structure for portfolio investments.

DTAA Withholding Tax Rates

| Income Type | Condition | DTAA Rate | Domestic Rate (comparison) |

|---|---|---|---|

| Dividends | Singapore company holds ≥25% of capital | 10% | 20% + surcharge/cess |

| Dividends | All other cases | 15% | 20% + surcharge/cess |

| Interest | Paid to a bank or financial institution | 10% | 20% + surcharge/cess |

| Interest | All other cases | 15% | 20% + surcharge/cess |

| Royalties | All cases | 10% | 20% + surcharge/cess |

| FTS | All cases | 10% | 20% + surcharge/cess |

Example: A Singapore technology company licenses software to an Indian enterprise for ₹10,00,000 in annual royalties. Without DTAA, the Indian payer would deduct approximately 20.8% withholding tax (₹2,08,000). Under the DTAA, withholding is capped at 10% (₹1,00,000) — a ₹1,08,000 cash flow saving in the first year alone.

2016 Protocol Capital Gains Changes

The 3rd Protocol (effective 1 April 2017) restructured Article 13 to end capital gains exemption:

- Article 13(4A): Shares acquired before 1 April 2017 remain grandfathered — capital gains taxable only in the State of residence (Singapore)

- Article 13(4B): Shares acquired on or after 1 April 2017 are taxable in India (source State)

- Article 13(4C): Transitional rate of 50% of domestic tax rate applied between 1 April 2017 and 31 March 2019 (subject to LOB)

Practical impact: Singapore investors holding Indian equity must track acquisition dates carefully. Pre-2017 shares retain tax exemption in India; post-2017 shares are subject to India's domestic capital gains regime (15% for short-term, 10% for long-term gains exceeding ₹1 lakh).

Limitation of Benefits (LOB) Clause

The India-Singapore DTAA contains strict anti-abuse provisions to deny benefits to shell or conduit companies.

Three tests determine whether a Singapore entity qualifies for treaty benefits:

- Expenditure threshold: Annual Singapore operations expenditure must be ≥S$200,000 or INR 50,00,000 in the 24 months before gains arise. Entities below this threshold are treated as shell/conduit companies.

- Listed company exception: Companies listed on a recognised stock exchange automatically satisfy the LOB condition.

- Principal Purpose Test (MLI): Benefits are denied if obtaining the treaty benefit was one of the principal purposes of any arrangement or transaction.

To demonstrate genuine Singapore residence, a company must show active business operations, adequate operational expenditure, and real substance — office space, employees, and decision-making located in Singapore. Public listing on a recognised exchange serves as an alternative path to treaty access.

Other Key DTAA Provisions

Several additional provisions affect how Singapore businesses operate in India day-to-day.

Permanent Establishment (Article 5) sets the threshold for when Indian-source business profits become taxable:

- Construction/installation PE: >183 days

- Service PE: >90 days in any fiscal year (30 days for related enterprises)

- Dependent/independent agent PE also applies

Article 8 exempts Shipping & Air Transport profits — these are taxable only in the enterprise's State of residence. Article 26 (Non-Discrimination) prevents India from imposing more burdensome tax on Singapore companies with Indian PEs than on comparable Indian enterprises. Where dual-residency is in question, Article 4's Place of Effective Management (POEM) test determines which country's tax treatment applies.

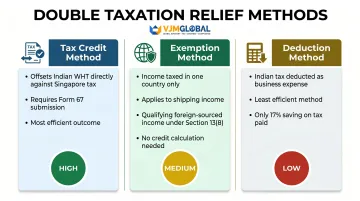

How Double Taxation Relief Works: Methods Singapore Businesses Can Use

Tax Credit Method (Most Common)

The Foreign Tax Credit (FTC) method is the primary relief mechanism for Singapore companies. India levies withholding tax at DTAA rates, and Singapore then allows the company to claim a credit against Singapore corporate tax payable on the same income.

Credit calculation: The credit is the lower of:

- The actual foreign tax paid (Indian withholding tax), or

- The Singapore tax attributable to that foreign income

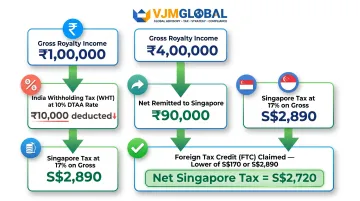

Example:

- Singapore company receives ₹1,00,000 in royalties from an Indian licensee

- India deducts 10% WHT (₹10,000) under DTAA

- Company remits ₹90,000 to Singapore

- Singapore taxes the gross income (₹1,00,000) at 17% corporate rate = S$2,890 tax payable (assuming ₹1 = S$0.017)

- FTC claimed: Lower of ₹10,000 paid to India (S$170) or S$2,890 Singapore tax = S$170

- Net Singapore tax payable: S$2,890 - S$170 = S$2,720

When the credit falls short: If Singapore's effective tax rate (after partial exemptions) is lower than India's treaty rate, the FTC cap limits relief. For instance, a start-up with a 6.4% effective rate would only get credit for 6.4% of the foreign income, not the full 10% Indian withholding tax.

Exemption Method

Certain income is wholly taxed in only one country and exempt in the other under specific DTAA articles:

- Shipping and air transport income (Article 8): Taxable only in the State of residence

- Foreign-sourced income exemption (Singapore): Dividends, branch profits, and service income from India may be exempt when remitted to Singapore if the three conditions under Section 13(8) are met

For Singapore businesses with qualifying income streams, this is the most straightforward outcome — no credit calculations required, and no residual tax liability in either country.

Deduction Method

Where neither the credit nor the exemption method applies cleanly, Singapore companies may elect to deduct Indian tax paid as a business expense, reducing taxable income in Singapore. This is the least efficient of the three methods.

Why this is least favourable: Deducting ₹10,000 of Indian tax saves only 17% of ₹10,000 = S$170 in Singapore tax, whereas the credit method offsets the same S$170 directly against tax owed (up to the Singapore tax attributable to that income). Companies typically use this route only when Singapore tax liability is too low to absorb the credit — making the deduction the only available offset.

Understanding these three methods sets the foundation for applying India's domestic relief provisions, which govern how these claims are formally structured under Indian tax law.

India's Domestic Relief Provisions (Sections 90, 90A, 91)

| Section | Scope | Relief Type |

|---|---|---|

| Section 90 | Where India has a DTAA with the other country | Bilateral relief — taxpayer may apply DTAA provisions if more beneficial than the Income Tax Act |

| Section 90A | Agreements adopted between specified associations | Bilateral relief under adopted agreements |

| Section 91 | Where no DTAA exists | Unilateral relief — deduction at the lower of Indian or foreign rate of tax |

Sections 90 and 90A are the primary DTAA relief provisions. To claim benefits, the Singapore company must furnish a Tax Residency Certificate (TRC) and Form 10F to the Indian payer.

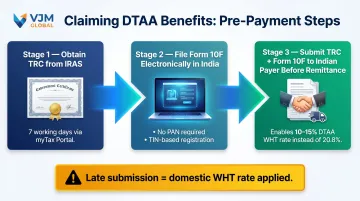

How Singapore Companies Claim DTAA Benefits: A Step-by-Step Guide

Before Income is Paid: Pre-Payment Steps

Step 1: Obtain a Tax Residency Certificate (TRC) from IRAS

The Certificate of Residence (COR) confirms the Singapore company is a tax resident of Singapore for the relevant year. Without a valid COR, the Indian payer is legally required to deduct TDS at the higher domestic rate (20%+ vs. 10-15% DTAA rate).

How to obtain:

- Apply through IRAS's myTax Portal

- Processing time: 7 working days for online applications

- A digital copy is made available in the portal upon approval

- The COR must contain mandatory fields per Rule 21AB of the Indian Income Tax Rules (name, status, TIN, residential status, period of validity, address)

Step 2: File Form 10F Electronically in India

Form 10F is a self-declaration form required under Sections 90(4)/90A(4) alongside the TRC to claim DTAA benefits.

Key requirements:

- Electronic filing is mandatory per DGIT(Systems) Notification No. 03/2022 (16 July 2022)

- PAN is no longer required for non-residents: DGIT(Systems) notification dated 28 March 2023 allows non-residents without a PAN to register on the income tax e-filing portal using TIN and other identification details

- Registration details required: Name, date of incorporation, TIN, country of residence, key person details, valid ID proof, address proof, and copy of TRC

Step 3: Provide TRC and Form 10F to the Indian Payer Before Remittance

The Singapore company must furnish the approved COR and Form 10F to the Indian payer before income is paid so the Indian company can deduct TDS at the lower DTAA rate rather than the domestic withholding rate.

Consequence of delay: If TRC and Form 10F are not submitted in time, the Indian payer deducts TDS at approximately 20.8% (domestic rate). You can recover the excess by filing an Indian Income Tax Return (ITR) and claiming a refund — but this creates cash flow delays, additional compliance work, and currency risk.

After Filing: Claiming Foreign Tax Credit

Step 4: File Form 67 for Foreign Tax Credit

Form 67 is a mandatory statement for claiming Foreign Tax Credit in India under Sections 90/90A/91.

Critical deadline: Form 67 must be filed electronically on or before the end of the relevant Assessment Year. For FY 2024-25 income, the deadline is 31 March 2026.

Consequence of non-filing: The Income Tax Department may disallow the Foreign Tax Credit claim for that year, resulting in double taxation with no remedy.

Required information:

- Details of foreign income offered to tax

- Foreign taxes paid/deducted

- Jurisdiction and applicable DTAA provisions

- Proof of payment

- Currency conversion details

Managing these filings remotely adds compliance risk — missed deadlines or incorrect submissions can result in disallowed credits with no recourse. VJM Global's Chartered Accountants bring 30+ years of India-specific tax experience, helping international businesses navigate DTAA filings, Form 10F submissions, ITR compliance, and Form 67 from a single point of contact.

Key Documents Singapore Businesses Need

Tax Residency Certificate (TRC) — Mandatory Fields

Under Rule 21AB of the Indian Income Tax Rules, a TRC must contain:

- Name of the taxpayer

- Status (individual, company, firm, etc.)

- Nationality (for individuals) or country of incorporation (for entities)

- Tax Identification Number (TIN) in Singapore

- Residential status for tax purposes

- Period of validity of the certificate

- Address of the taxpayer for the applicable period

If the TRC does not contain all mandated fields, the missing information must be furnished separately via Form 10F.

The TRC typically needs to be renewed each tax year to maintain continuous DTAA eligibility.

Form 10F (Electronically Filed)

Form 10F is filed on India's income tax e-filing portal and contains residency and taxpayer details. Following the DGIT(Systems) notification dated 28 March 2023, non-resident companies without an Indian PAN can now register on the portal using their TIN and home-jurisdiction identification details, eliminating the need for an Indian PAN.

Supporting Income and TDS Documents

Form 16A (TDS Certificate): Issued quarterly by the Indian payer under Section 203(1) for non-salary payments to non-residents. Form 16A contains:

- Details of TDS deducted

- Nature of payment

- PAN/TIN of the payee

- Amount of income and tax withheld

Form 16A serves as proof of TDS and is required to support DTAA benefit claims and refund applications.

Beyond Form 16A, claimants should also retain:

- Copies of relevant agreements (licensing agreement for royalties, loan agreement for interest, service contract for FTS)

- Bank statements confirming remittance and tax deduction

- Singapore-side documents confirming income was reported in Singapore

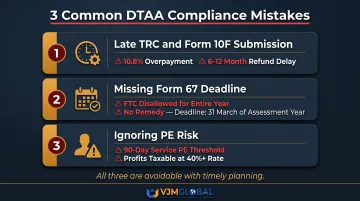

Common Mistakes Singapore Businesses Make with DTAA

Mistake 1: Waiting Too Long to Submit TRC and Form 10F

If TRC and Form 10F are not submitted to the Indian payer before income is remitted, the payer deducts TDS at the higher domestic rate:

- Royalties and FTS: approximately 20.8% vs. 10% DTAA rate (10.8 percentage point overpayment)

- Dividends (≥25% holding): approximately 20.8% vs. 10% DTAA rate

- Interest (bank): approximately 20.8% vs. 10% DTAA rate

Excess TDS can sometimes be reclaimed via an Indian ITR refund process, but recovery requires obtaining a PAN, filing an ITR as a non-resident, waiting for assessment, and managing currency risk. That process typically takes 6-12 months — and is entirely avoidable with timely documentation.

Mistake 2: Missing the Form 67 Filing Deadline

Many Singapore businesses are unaware that Form 67 must be filed before the income tax return for that year. If the ITR is filed without Form 67, the FTC claim is generally disallowed for that year with no remedy.

Deadline: End of the relevant assessment year — for example, 31 March 2026 for FY 2024-25.

Claiming DTAA benefits also requires all three of the following conditions to be met:

- Valid TRC from IRAS

- Form 10F filed electronically

- LOB clause conditions satisfied (expenditure threshold; entity must not be a shell company)

Mistake 3: Ignoring PE Risk

Singapore businesses that send employees to India for extended periods, or that have agents or subsidiary operations in India, may inadvertently create a Permanent Establishment.

The India-Singapore DTAA sets the service PE threshold at just 90 days in any fiscal year — or 30 days for services to related enterprises. That is far lower than the commonly assumed 183-day rule, which applies only to construction/installation PEs and supervisory activities.

Once a PE is triggered, Indian-attributable business profits become taxable at the full foreign company rate — which can reach 40%+ with surcharge and cess — rather than the standard withholding tax rates.

For Singapore companies sending employees or agents to India, VJM Global's international taxation team can assess PE exposure — reviewing business activities against DTAA thresholds, evaluating POEM compliance, and building documentation to support any discussions with Indian tax authorities.

Frequently Asked Questions

What is double taxation relief in India?

Double taxation relief in India refers to mechanisms under the Income Tax Act (Sections 90, 90A, and 91) and bilateral DTAA treaties that prevent the same income from being taxed in both India and another country. Relief is typically provided through tax credits, exemptions, or deductions.

How do I claim double taxation relief (DTAA benefits) in India?

The process involves four steps:

- Obtain a Tax Residency Certificate (TRC) from IRAS

- Submit Form 10F electronically on India's income tax portal

- Provide both documents to your Indian payer before income is remitted

- File Form 67 before your Indian ITR deadline to claim Foreign Tax Credit

How can I avoid double taxation in India?

Determine if India has a DTAA with Singapore (it does), then actively claim treaty benefits by submitting the required documents (TRC + Form 10F) to ensure income is taxed at the lower DTAA withholding rate (10-15%) rather than the higher domestic rate (20%+).

How can NRIs avoid double taxation on income or investments in India?

NRIs can use the applicable DTAA between India and their country of residence to claim reduced withholding tax rates or exemptions on India-sourced income such as dividends, interest, and capital gains. They can also claim Foreign Tax Credit in their country of residence for taxes paid in India.

Does India's DTAA with the United States affect Singapore businesses with US connections?

Yes — Singapore entities with US parent companies or US-sourced income should be aware that the India-US DTAA caps withholding on dividends (15-25%), interest (10-15%), and royalties (10-15%). The treaty's Saving Clause allows the US to tax its citizens on worldwide income regardless of treaty provisions, which adds complexity for Singapore businesses with US shareholders or funding structures.

For Singapore businesses: India-Singapore DTAA benefits don't apply automatically — each step must be completed in sequence. Missing a filing deadline or skipping Form 10F can cost 10+ percentage points of India-sourced income. For support with DTAA filings, PE assessments, and cross-border tax planning in India, contact VJM Global at info@vjmglobal.com.