Most incorporation guides steer Indian businesses toward a Private Limited (Pte Ltd) structure. That works for startups and SMEs. But for companies planning large-scale public capital raising, an SGX listing, or access to more than 50 investors, the Public Limited Company (Ltd) is the structure that actually fits.

This guide covers what a Singapore Public Limited Company is, how it compares to a Pte Ltd, what India-side FEMA and RBI obligations apply, and how the India-Singapore DTAA affects your tax position.

Key Takeaways

- A Singapore Public Limited Company (Ltd) allows unlimited shareholders and can offer shares to the public

- Any public share offering requires a prospectus registered with the Monetary Authority of Singapore (MAS) under the Securities and Futures Act

- Indian companies must complete FEMA/RBI ODI filings and obtain a UIN before remitting capital to Singapore

- 100% foreign ownership is permitted — no sector restrictions for most commercial activities

- The India-Singapore DTAA caps dividend withholding at 15% (reduced to 10% if the Singapore entity holds at least 25% equity in the Indian company)

What Is a Public Limited Company in Singapore?

A Singapore Public Limited Company is incorporated under the Singapore Companies Act and carries the suffix "Ltd." It is regulated by the Accounting and Corporate Regulatory Authority (ACRA).

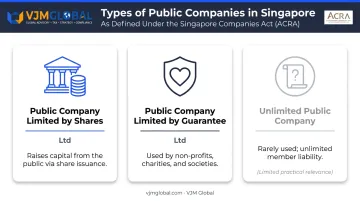

The Three Types of Singapore Public Companies

ACRA recognises three public company classifications:

- Public Company Limited by Shares (Ltd) — commercial companies seeking public capital; the focus of this guide

- Public Company Limited by Guarantee (Ltd) — non-profits and charities without share capital

- Unlimited Public Company — rarely used

Key Legal Characteristics

A Public Company Limited by Shares carries these defining features:

- Separate legal entity with perpetual succession

- Limited liability for shareholders (personal assets protected)

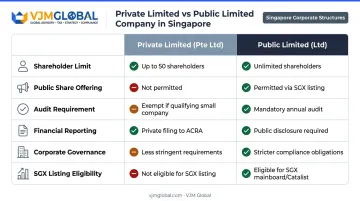

- No cap on the number of shareholders (versus a 50-member ceiling for Pte Ltd)

- Ability to pursue a listing on the Singapore Exchange (SGX)

- Mandatory prospectus registration with MAS before any public share offering

The MAS Prospectus Requirement

Before a Singapore Public Limited Company can invite public investment — through an IPO, public bond offering, or any offer of shares to retail investors — it must register a prospectus with MAS under Section 240 of the Securities and Futures Act. This is a pre-offer condition, not a post-incorporation formality.

The prospectus must include:

- Material information about the company and its business

- Audited financial statements

- Identified risk factors

- Intended use of proceeds

MAS can require amendments or reject the prospectus before approving it. This regulatory layer is specifically designed to protect retail investors, and it marks the clearest structural difference from a Pte Ltd.

When an Indian Company Needs This Structure

- Large conglomerates using Singapore as a regional holding vehicle

- Companies planning a dual listing on NSE/BSE and SGX

- Businesses raising capital from more than 50 investors or institutions in Singapore

- REITs and business trusts operating through a Singapore platform

Singapore Public Limited Company vs. Private Limited Company

Most incorporation resources targeting Indian entrepreneurs focus exclusively on the Pte Ltd. That structure suits startups and early-stage businesses — but it has hard statutory limits that make it unsuitable for public capital markets.

Side-by-Side Comparison

| Parameter | Private Limited (Pte Ltd) | Public Limited (Ltd) |

|---|---|---|

| Shareholder limit | Maximum 50 | No limit |

| Public share offering | Prohibited | Permitted with MAS-registered prospectus |

| Audit requirement | Small company exemption possible | Mandatory — auditor within 3 months |

| Financial reporting | Less stringent | Full public disclosure required |

| Corporate governance | Standard | Board committees, greater disclosure obligations |

| SGX listing eligibility | Not applicable | Compatible structure for Singapore-incorporated issuers |

Compliance Intensity

A Public Limited Company carries stricter ongoing disclosure, financial reporting, and governance obligations than a Pte Ltd. For Indian businesses already operating within the framework of an Indian public limited company under the Companies Act 2013, the structural logic will feel familiar — though Singapore's specific ACRA and MAS requirements operate under a distinct regulatory framework and demand separate compliance planning.

Those compliance obligations come with a direct payoff: access to public capital.

The Fundraising Advantage

The absence of a shareholder cap is significant. An Indian parent company can use the Singapore entity as a capital-raising vehicle, issue public bonds, or attract institutional and retail shareholders across ASEAN markets. None of that is possible through a Pte Ltd.

SGX Context

SGX Group reports that approximately 40% of SGX-listed companies originate outside Singapore, making it one of Asia's most accessible exchanges for foreign issuers. A Singapore-incorporated entity pursuing a public offer requires public company capacity — a Pte Ltd's private-company restrictions make it incompatible with that route.

Key Requirements to Register a Public Limited Company in Singapore

Statutory Requirements Under ACRA

| Requirement | Detail |

|---|---|

| Shareholders | Minimum 1; no upper limit |

| Resident director | At least 1 director ordinarily resident in Singapore |

| Registered office | Physical Singapore address — PO Boxes not accepted |

| Paid-up capital | Minimum S$1 (practical capital for public companies will be considerably higher) |

| Company secretary | Qualified Singapore resident; must be appointed within 6 months of incorporation |

| Auditor | Must be appointed within 3 months of incorporation; small company audit exemption does not apply to public companies |

The Auditor Requirement in Practice

Unlike a Pte Ltd (which may qualify for ACRA's small company audit exemption), a Singapore Public Limited Company must appoint a registered public accountant from the outset. Financial statements must comply with the Singapore Financial Reporting Standards (SFRS), which align with IFRS. For Indian parent companies, this creates a parallel reporting obligation alongside Indian GAAP or Ind AS: a detail worth factoring into your finance function planning early.

The audit obligation addresses your ongoing compliance posture. But raising capital from the public introduces a separate regulatory layer entirely.

MAS Prospectus Requirements

Before any public fundraising, the company must prepare and register a prospectus with MAS.

Under Section 243 of the Securities and Futures Act, the prospectus must contain:

- Material information that investors and their advisers would reasonably require

- Audited financial statements for recent years

- Identified risk factors

- Intended use of proceeds

- Full details on the company's business and management

Incorporation and MAS prospectus approval are entirely separate tracks. Registering with ACRA does not authorise a public share offer.

India-Side FEMA and ODI Obligations Before Setting Up

Many Indian companies get the sequence wrong here, and the consequences under FEMA can be severe.

The Pre-Remittance Obligation

Under the Foreign Exchange Management Act (FEMA) and the RBI Overseas Investment Directions 2022, the Indian entity must file Form FC through an authorised dealer (AD) bank and obtain a Unique Identification Number (UIN) before making any outward remittance. Both Singapore registration and capital transfer must come after this step — reversing the order creates compliance risk under FEMA Section 13.

FEMA Section 13 penalties are significant:

- Up to 3× the sum involved if quantifiable

- Up to ₹2 lakh if not quantifiable

- ₹5,000 per day for continuing contraventions

Ongoing India-Side Annual Obligations

Once the Singapore entity is operational, the Indian parent carries these recurring obligations:

- Annual Performance Report (APR): Filed with the RBI by 31 December each year, based on audited financials of the Singapore entity

- FEMA compliance for profit repatriation: Dividends flowing back to the Indian parent must follow capital account transaction rules

- Transfer pricing documentation: Intra-group transactions (management fees, IP licensing, services) between the Indian parent and the Singapore entity require documentation under Section 92E of the Income Tax Act

Section 92E requires an accountant's report — Form 3CEB — for every international transaction, regardless of value. Penalties for non-compliance include ₹1,00,000 under Section 271BA for failure to furnish Form 3CEB, plus separate documentation penalties under Sections 271AA and 271G that can reach 2% of the transaction value.

VJM Global's FEMA advisory and ODI compliance practice handles each of these obligations — Form FC and UIN filing, APR submissions, and transfer pricing documentation for cross-border intra-group transactions.

How to Register a Public Limited Company in Singapore: Step-by-Step

Singapore Registration Steps

- Reserve the company name via ACRA's BizFile+ portal — S$15 fee, valid for 120 days; the name must end in "Ltd" for public companies

- **Appoint at least one locally resident director** and a company secretary — Indian companies without a Singapore-based individual typically engage a nominee director through a licensed corporate service provider

- Prepare incorporation documents — company constitution, director and shareholder details, registered Singapore office address, SSIC business activity code, and share structure

- Submit through a registered filing agent — foreign nationals cannot self-register on BizFile+; a licensed Corporate Service Provider (CSP) must file on your behalf

- Receive Certificate of Incorporation and Unique Entity Number (UEN) from ACRA — most straightforward applications are processed within minutes to a few hours of payment; applications referred to another agency may take up to 15 working days

Once incorporated, public limited companies face additional compliance obligations that private companies do not.

Post-Incorporation Steps Specific to a Public Ltd

- Appoint an auditor within 3 months of incorporation

- Prepare and register a prospectus with MAS before any public share offering

- Open a corporate bank account — DBS, OCBC, and most Singapore banks require the company's UEN

- Register for GST if expected annual taxable turnover exceeds S$1 million — current rate is 9%

These steps run parallel to your Indian regulatory obligations, which is where sequencing becomes critical.

Critical Sequencing Point

Complete FEMA/ODI filings and obtain your UIN from the RBI before initiating Singapore registration or remitting any capital. The Indian regulatory clock starts the moment funds leave India, regardless of when the Singapore entity is formally incorporated.

Tax Benefits and DTAA Implications for Indian Companies

Singapore's Corporate Tax Regime

Singapore applies a flat 17% corporate income tax rate. The partial tax exemption scheme provides:

- 75% exemption on the first S$10,000 of chargeable income

- 50% exemption on the next S$190,000

- Maximum exemption of S$102,500 on the first S$200,000 of chargeable income

The Start-up Tax Exemption (SUTE) scheme — which offers more generous relief in the first three years — is generally unavailable to a large Public Limited Company. SUTE eligibility requires no more than 20 shareholders meeting specific individual-shareholder tests; a Public Ltd with broad investor participation will typically fail this condition.

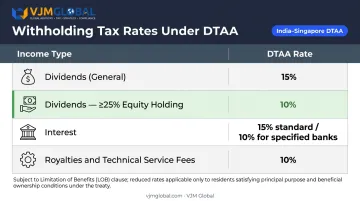

India-Singapore DTAA: Key Rates

The India-Singapore Double Taxation Avoidance Agreement provides the following withholding tax caps:

| Income Type | DTAA Rate |

|---|---|

| Dividends (general) | 15% |

| Dividends (beneficial owner holds ≥25% equity) | 10% |

| Interest | 15% (10% for specified banks/financial institutions) |

| Royalties and fees for technical services | 10% |

Singapore does not tax incoming foreign-sourced dividends received by a Singapore entity, subject to IRAS conditions being met.

The Limitation of Benefits Clause — Non-Negotiable

The 2016 Protocol to the India-Singapore DTAA explicitly denies treaty benefits to shell and conduit arrangements. To access treaty rates, the Singapore entity must demonstrate genuine economic substance, including at least S$200,000 in Singapore operating expenditure over a specified 24-month period.

This is not a technicality. Indian companies must structure the Singapore Public Ltd as a genuinely active business: real employees on payroll, documented operating expenditure, and commercial activity that can withstand IRAS scrutiny.

Annual Compliance Calendar

Maintaining treaty eligibility goes hand-in-hand with meeting annual filing deadlines on both sides of the corridor. Key obligations include:

- AGM: Within 4 months of financial year-end for listed companies; 6 months for unlisted

- Corporate income tax return (IRAS): By 30 November each year

- ACRA annual return: Filed after AGM

- GST returns: If registered

- RBI APR (India side): By 31 December each year

VJM Global supports Indian companies managing these dual-jurisdiction obligations, covering ODI reporting, transfer pricing documentation, and DTAA advisory for the India-Singapore corridor.

Frequently Asked Questions

What is a public limited company in India?

Under the Companies Act 2013, a public limited company in India requires a minimum of 7 shareholders and 3 directors, with no cap on maximum shareholders. It can offer shares to the general public and must use "Limited" as a name suffix, making it a conceptual parallel to Singapore's Public Ltd — though the two structures operate under distinct statutory frameworks.

Why do MNCs choose Singapore?

Singapore offers a 17% corporate tax rate, 100% foreign ownership, zero capital gains tax, and a broad treaty network. Its strategic location gives direct access to ASEAN's market of over 684 million consumers, and company registration is typically completed quickly through ACRA's BizFile+ system.

What is the difference between a Public Limited Company and a Private Limited Company in Singapore?

A Pte Ltd is capped at 50 shareholders and cannot offer shares to the public. A Public Ltd (Ltd) has no shareholder ceiling, can invite public investment via a MAS-registered prospectus, and is subject to mandatory audits and stricter ongoing reporting requirements.

Can an Indian company own 100% of a Singapore Public Limited Company?

Yes. Singapore permits 100% foreign ownership of a Public Limited Company across most commercial sectors, though regulated industries such as financial services and media may have additional requirements. The company must appoint at least one locally resident director, and the Indian parent must complete FEMA/ODI filings before remitting any capital.

Does a Singapore Public Limited Company need to register a prospectus with MAS?

Before offering shares or debentures to the public, a Singapore Public Ltd must register a prospectus with MAS under the Securities and Futures Act. This requirement does not apply when raising funds exclusively from institutional or accredited investors under SFA exemptions.

What are the ongoing compliance requirements for a Singapore Public Limited Company?

Core obligations for the Singapore entity include:

- Mandatory annual audit

- AGM within the required period after financial year-end

- Annual return filing with ACRA

- Corporate income tax return with IRAS by 30 November

- GST returns if registered

The Indian parent must also file an annual RBI APR by 31 December and maintain transfer pricing documentation — including Form 3CEB — for all cross-border intra-group transactions.