Introduction

Singapore has emerged as a strategic offshore destination for Indian entrepreneurs, driven by robust bilateral trade ties valued at USD 34.3 billion in FY 2024-25 and approximately 9,000 Indian companies already registered in the city-state. The country serves as a proven gateway to Southeast Asian markets, offering 100% foreign ownership, a flat 17% corporate tax rate, and a business-friendly regulatory environment.

Most online guides overlook a critical two-jurisdiction challenge: before a single rupee is remitted, Indian founders must complete India-side FEMA and RBI Overseas Direct Investment (ODI) compliance.

The Singapore incorporation process is fast — typically 1–3 business days — but skipping the mandatory Form FC filing and UIN (Unique Identification Number) registration triggers penalties up to three times the amount involved under FEMA Section 13.

This guide covers the complete end-to-end process:

- India-side ODI obligations under FEMA and RBI rules

- Singapore registration mechanics and document requirements

- Actual costs beyond the S$315 government fee

- Realistic timelines, including banking setup

- Common pitfalls that trip up Indian founders

Key Takeaways

- Indian nationals can own 100% of a Singapore Pte Ltd, but must appoint a locally resident director and use a registered filing agent.

- India-side Form FC and RBI UIN filing must be completed before remitting capital; non-compliance triggers FEMA Section 13 penalties.

- Expect total startup costs of S$3,000–S$4,000, covering government fees (S$315), nominee director, company secretary, and registered address.

- Remote incorporation takes 1–3 business days; bank account setup adds 2–4 weeks to the timeline.

- Compliance obligations start immediately — annual ACRA/IRAS filings in Singapore plus RBI APR reporting back in India.

What Indian Founders Must Do Before Registering in Singapore

Unlike founders from most other countries, Indian residents face mandatory obligations under the Foreign Exchange Management Act (FEMA) and the RBI's Overseas Investment Regulations 2022. These requirements must be fulfilled before any outward remittance or equity acquisition in the Singapore entity—not after.

India-Side ODI Filing Requirements

Indian residents (both individuals and companies) must file Form FC with an Authorised Dealer (AD) bank to obtain a Unique Identification Number (UIN) before sending any funds to establish or capitalise the Singapore company. This framework is governed by FEMA 400/2022-RB, which replaced the older FEMA 120/2004-RB framework.

Skipping this step before remitting funds is a costly mistake. Under FEMA Section 13, violations can result in:

- Penalties up to three times the sum involved in the contravention

- Additional fines of Rs 5,000 per day for continuing violations

- Confiscation of overseas assets, with equivalent value seized in India

Beyond penalties, founders also need to stay within the LRS remittance ceiling. Liberalised Remittance Scheme (LRS) cap: Resident individuals can remit up to USD 250,000 per financial year for permitted purposes, including overseas direct investment. The RBI clarifies that this cap is cumulative across all capacities—if you remit USD 250,000 as an individual, you cannot remit another USD 250,000 as a proprietor in the same financial year.

Annual Reporting Obligations from Day One

Once the Singapore entity is operational, Indian founders must file Annual Performance Reports (APR) based on audited financials of the overseas entity. The APR deadline is December 31 each year.

Non-filing attracts a Late Submission Fee of Rs 7,500 per return and can prompt AD banks to block future overseas remittances.

Physical Presence vs. Remote Ownership

Indian nationals can fully own and operate a Singapore company remotely by appointing a nominee director—no physical relocation is required. The nominee arrangement does not give the nominee access to company funds; a formal agreement protects the founder's ownership and control.

For founders who want to relocate and act as resident director:

- EntrePass: Requires a 30% shareholding minimum, venture backing or innovative technology, and at least SGD 100,000 raised from qualified investors or incubator support

- Employment Pass: Minimum salary of S$5,600 per month from January 2025 (S$6,200 for financial services sector)

VJM Global provides FEMA advisory and ODI compliance services—including Form FC preparation, AD bank coordination, and documentation support—so that India-side filings are complete before your Singapore incorporation date, avoiding penalties and remittance blocks from day one.

Choosing the Right Business Structure

The choice of business structure affects tax treatment, liability exposure, fundraising ability, and the type of ODI/transfer pricing compliance required. Singapore offers several options:

- Private Limited Company (Pte Ltd)

- Sole Proprietorship

- Branch Office

- Limited Liability Partnership (LLP)

Of these, the Private Limited Company (Pte Ltd) is the dominant choice for Indian founders — it directly addresses the three main concerns: liability protection, tax efficiency, and clean fundraising structure.

Private Limited Company (Pte Ltd) vs. Branch Office or Subsidiary

A Pte Ltd gives Indian founders a clean slate with several structural advantages:

- Separate legal entity with limited liability protection

- 100% foreign ownership permitted with no minimum local shareholding

- 1–50 shareholders allowed

- Flat 17% corporate tax, with startup exemptions reducing the effective rate to 4.25%–8.5% on the first S$200,000

- Eligible for Singapore tax residency when control and management are exercised locally

Within the Pte Ltd structure, Indian founders typically choose between two configurations — a fresh Pte Ltd or a Singapore subsidiary of an existing Indian company:

| Feature | Fresh Pte Ltd | Singapore Subsidiary |

|---|---|---|

| Ownership | Individual Indian founders | Indian parent company as shareholder |

| ODI Filing | Individual Form FC via LRS route | Corporate ODI route through parent entity |

| Transfer Pricing | No intra-group transactions | Form 3CEB required for intercompany transactions |

| Profit Repatriation | Direct to individual founders | Dividend from subsidiary to Indian parent |

| Tax Complexity | Lower | Higher due to DTAA structuring |

The decision comes down to your starting point. The subsidiary structure suits founders with an established Indian parent company already in place. A fresh Pte Ltd is the simpler path for individual entrepreneurs launching a new venture. Both qualify for startup tax exemptions — however, the subsidiary route triggers mandatory transfer pricing documentation the moment intercompany transactions begin.

How to Register a Company in Singapore from India: Step by Step

Step 1: Complete India-Side ODI and FEMA Compliance

Complete this before anything else. File Form FC with your AD bank, obtain the UIN, and document the capital remittance plan. This step typically adds 2–4 weeks to the overall timeline — rushing past it creates downstream compliance problems.

Documents typically required:

- Resolution or letter of authority from parent company (if applicable)

- Certificate of incorporation of Indian entity

- Latest audited financial statements for past 3 years

- KYC documents for all shareholders with >10% stakes

- Banker's certificate and account details

- Details of proposed Singapore entity (address, business activities, funding amount)

- Certified identity and address proofs of all directors

VJM Global handles Form FC preparation, document compilation, and AD bank coordination on your behalf.

Step 2: Choose the Business Structure and Reserve the Company Name

Name reservation runs through ACRA's BizFile+ portal:

- Fee: S$15

- Reservation period: 120 days

- Naming rules: No offensive words, no names identical to existing entities, no restricted terms without approval

Critical limitation: Indian nationals cannot self-register on BizFile+. The system requires Singpass login tied to NRIC or FIN (available only to Singapore citizens, PRs, or work pass holders). You must engage a registered filing agent or Corporate Service Provider (CSP) to complete the reservation and incorporation.

Step 3: Appoint a Resident Director and Company Secretary

Singapore law requires **at least one ordinarily resident director** — a Singapore citizen, Permanent Resident, or valid work pass holder. Indian founders staying in India typically resolve this through a nominee director arrangement.

How nominee director arrangements work:

- Founder retains full ownership and control via shareholders' agreement

- Nominee has no access to bank accounts or company funds

- Formal agreement protects founder's decision-making authority

- Nominee signs statutory documents required by ACRA

A qualified company secretary must be appointed within six months of incorporation. The secretary handles annual compliance filings, maintains statutory registers, and ensures regulatory adherence.

Step 4: Prepare and Submit Incorporation Documents

Documents needed:

- Passport copies of all directors and shareholders

- Proof of residential address for all directors

- Company constitution (standard ACRA model or customised version)

- Registered Singapore office address

- Share structure details and issued capital amount

- SSIC (Singapore Standard Industrial Classification) code for business activity

Document legalisation: Singapore acceded to the Apostille Convention in September 2021, simplifying document legalisation for Indian founders. Indian documents are accepted with apostille; no further embassy legalisation is needed.

The filing agent submits the complete application through BizFile+. ACRA approves straightforward applications within 1–3 business days and issues a Unique Entity Number (UEN) and Certificate of Incorporation electronically.

Step 5: Open a Corporate Bank Account

Major Singapore banks (DBS, OCBC, UOB) require extensive KYC documentation:

- Certificate of incorporation and UEN

- BizFile company profile

- Identity documents for all directors and beneficial owners

- Proof of residential address

- Company constitution (Memorandum & Articles)

- Business plan or description of activities

- Expected transaction volumes and source of funds

Remote/video KYC options: OCBC explicitly offers online applications with "no branch visit needed" for foreign-owned companies. UOB provides online forms for foreign incorporation. DBS requires an assisted account opening process with a Relationship Manager at office locations.

Realistic timeline: Banking setup typically takes 2–4 weeks and is frequently underestimated. Start the process immediately after incorporation approval.

Step 6: Register for GST and Obtain Business Licenses

GST registration is mandatory once annual taxable turnover exceeds S$1 million. The current GST rate is 9%, effective January 1, 2024. Voluntary registration is available below the threshold — useful for B2B companies that can claim input tax credits.

Industry-specific licenses may be required for regulated sectors:

- Financial services

- Education and training

- Healthcare and medical services

- Food and beverage

- Import/export licenses

Verify license requirements through Singapore's GoBusiness portal using your SSIC code.

Common Mistakes Indian Founders Make When Registering in Singapore

Three errors account for most of the delays, penalties, and banking rejections Indian founders encounter:

1. Reversing the compliance order

Registering the Singapore entity or opening a bank account before completing India-side ODI filings triggers FEMA penalties and capital remittance problems that are difficult to unwind after the fact. The Form FC filing with the RBI-designated AD bank must happen before any outward remittance — skipping this step can freeze your ability to fund the Singapore company legally.

2. Selecting a vague or mismatched SSIC code

The Singapore Standard Industrial Classification (SSIC) code is a 5-digit number that classifies your business activity. A mismatch creates friction during banking KYC, with licensing authorities, and in regulatory classification. You can update the code post-registration via BizFile+, but ACRA must be notified within 14 days of any change.

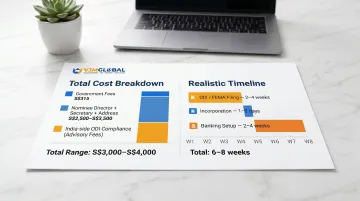

3. Underestimating total cost and timeline

The S$315 government fee (S$15 name reservation + S$300 incorporation) covers only registration itself. Factor in:

- Nominee director, company secretary, and registered address: typically S$2,500–S$3,500/year through a CSP

- Bank account setup: 2–4 weeks, often requiring in-person verification or video KYC

- India-side ODI compliance: another 2–4 weeks for Form FC processing

The complete process realistically takes 6–8 weeks. Founders who plan for a few days are routinely caught off guard.

Post-Registration: Managing Compliance on Both Sides

Running a Singapore company from India creates a dual compliance burden that most Indian founders underestimate. Missing deadlines on either side can trigger penalties, forced deregistration, or blocked profit repatriation.

Singapore-Side Obligations

Ongoing Singapore compliance requirements:

- Annual returns filing with ACRA (fee: S$60)

- Corporate income tax returns with IRAS (deadline: November 30 for companies with December 31 year-end)

- GST returns if registered (quarterly or monthly depending on turnover)

- Maintenance of proper accounting records and statutory registers

- Industry-specific regulatory filings where applicable

Singapore's corporate tax rate is 17%, with significant startup exemptions: 75% exemption on the first S$100,000 of chargeable income and 50% on the next S$100,000 for the first three years of assessment. This reduces the effective tax rate to approximately 4.25%-8.5% on the first S$200,000 of profit.

India-Side Ongoing Obligations

Continuing India-side requirements:

- APR filing: Annual Performance Reports filed through AD bank by December 31 each year based on audited Singapore entity financials

- FEMA compliance: Documentation for any repatriation of profits from Singapore to India

- Transfer pricing documentation: Form 3CEB required for any intra-group transactions between Indian and Singapore entities

Penalty for failure to file Form 3CEB is ₹1,00,000 under Section 271BA of the Income Tax Act, 1961.

Profit Repatriation and DTAA Benefits

The India-Singapore Double Taxation Avoidance Agreement (DTAA) affects dividend repatriation:

- Singapore side: No withholding tax on dividends under the one-tier corporate tax system

- India side: Dividends received from Singapore are taxable as income in India at applicable slab rates; proper DTAA documentation required to avoid double taxation

- Capital gains: Shares acquired on or after April 1, 2017 are taxable in the source country under the amended treaty protocol

Claiming DTAA benefits requires a Tax Residency Certificate (TRC) and Form 10FA from the Singapore entity.

VJM Global handles India-side ODI reporting, DTAA advisory, transfer pricing documentation, and cross-border accounting so Indian founders stay compliant in both jurisdictions without managing two separate compliance tracks.

Frequently Asked Questions

How much does it cost to register a company in Singapore from India?

Mandatory government fees total S$315 (S$15 name reservation + S$300 incorporation). Typical total startup costs run S$3,000–S$4,000 when including nominee director services, company secretary appointment, registered address, and CSP filing fees required for non-resident founders.

How can someone in India register a company in Singapore?

Start with FEMA/ODI compliance in India (Form FC and UIN). From there, a registered filing agent in Singapore handles name reservation, resident director appointment, document preparation, and the BizFile+ incorporation submission. The entire process can be completed remotely from India.

Can an Indian register a company in Singapore?

Yes, Indian nationals can own 100% of a Singapore company. However, they must appoint at least one locally resident director and use a registered filing agent, as foreigners cannot self-register on BizFile+ (which requires Singpass tied to Singapore NRIC or work pass).

Is 100% foreign ownership allowed in Singapore?

Singapore allows 100% foreign ownership with no restrictions on shareholding or profit repatriation, making it one of the most open jurisdictions for foreign entrepreneurs globally. The only local requirement is appointing at least one ordinarily resident director.

Can a foreign company register in Singapore?

An existing Indian company can enter Singapore as a Subsidiary (a separate legal entity with limited liability and local tax residency) or a Branch Office (an extension of the parent, which remains fully liable for Singapore operations). Each structure carries distinct ODI, transfer pricing, and tax consequences worth reviewing before committing.