Introduction

UAE businesses exploring UK market entry face a genuine choice between company structures — and most default immediately to a Private Limited Company without understanding what the alternative offers. The Public Limited Company (PLC) is a distinct legal structure with specific advantages, stricter requirements, and a very different compliance profile.

There are roughly 3,943 active PLCs on the UK register — a small fraction of the nearly 5 million registered companies. PLC status carries real weight precisely because so few businesses qualify for — or need — it.

What follows is a practical breakdown of PLC requirements, how they compare to a Private Limited Company, and the specific factors UAE founders should weigh before committing to either structure.

Key Takeaways

- A UK PLC can offer shares to the general public and requires a minimum share capital of £50,000 before trading begins

- PLCs face stricter compliance obligations than Private Limited Companies: mandatory audits, AGMs, and tighter filing deadlines

- UAE nationals and companies can hold shares in a UK PLC with no nationality or residency restrictions

- PLC status suits businesses planning a public listing or institutional fundraising — most UAE SMEs are better served starting with a Private Limited Company

What Is a UK Public Limited Company (PLC)?

Under the Companies Act 2006 (Section 4), a public company is a company limited by shares whose certificate of incorporation states it is a public company. The key distinction: a PLC can offer and trade its shares publicly. A Private Limited Company cannot.

Core Legal Features

Three features underpin every UK PLC:

- Separate legal identity — registration creates a distinct legal entity capable of entering contracts, holding assets, and incurring liabilities in its own name

- Limited liability — shareholders' exposure is capped at the amount unpaid on their shares

- Public share issuance — unlike a Private Ltd, a PLC can raise capital directly from members of the public or institutional investors

The name itself signals this status. Under Section 58 of the Companies Act 2006, a PLC must end its registered name with "public limited company" or "p.l.c." — making its public status visible at a glance.

That naming requirement sets the stage for a distinction UAE founders frequently get wrong.

PLC vs Stock Exchange Listing

This distinction matters for UAE founders: holding PLC status does not mean being listed on a stock exchange. A PLC simply has the legal right to offer shares publicly. Many well-known FTSE 100 and FTSE 250 constituents — Barclays PLC, NatWest Group PLC — are listed PLCs, but a company can hold PLC status and remain entirely unlisted, raising capital through private placements instead.

Clearing Up a Common Misconception

UAE founders sometimes assume "PLC" means government-owned or reserved for large corporations. Neither is true. PLC is a legal structure, not a size indicator. Small and medium businesses can technically form one — though the ongoing compliance obligations often make this impractical at early stages.

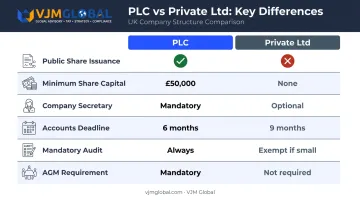

PLC vs Private Limited Company: Key Differences for UAE Founders

The gap between a PLC and a Private Ltd is wider than many founders expect — and the differences carry real operational and financial consequences.

| Feature | PLC | Private Ltd |

|---|---|---|

| Public share issuance | ✅ Permitted | ❌ Prohibited |

| Minimum share capital | £50,000 (25% paid up) | None |

| Company secretary | Mandatory (qualified) | Optional |

| Annual accounts deadline | 6 months from year-end | 9 months from year-end |

| Mandatory audit | Always required | Exempt if small |

| AGM requirement | Mandatory | Not required |

Governance and Administrative Complexity

PLCs must hold an Annual General Meeting within six months of the accounting reference date. They must appoint a qualified company secretary — someone who meets specific professional criteria set out in Section 273 of the Companies Act, such as membership of a recognised accountancy or governance body.

For UAE founders managing a UK entity remotely, these obligations add a real administrative layer. AGM minutes, secretary appointments, and accelerated filing deadlines all require coordination with UK-based professionals.

The Fundraising Advantage

That added compliance overhead unlocks something a Private Ltd cannot offer: public capital access. A PLC can list on the London Stock Exchange's AIM (Alternative Investment Market), designed for growth-oriented companies seeking equity financing. This makes the PLC structure genuinely suited for UAE businesses planning:

- A future IPO on the London Stock Exchange

- Institutional investment rounds requiring publicly tradeable shares

- Commercial credibility with large UK or European counterparties

Cost Drivers to Factor In

Incorporation fees from Companies House are modest — £100 online, £124 by paper. The heavier costs come from ongoing obligations:

- Mandatory independent audit (regardless of company size)

- Qualified company secretary fees

- Accelerated accounts preparation and filing

- Potential AIM adviser or listing fees if pursuing public markets

For an early-stage operation, audit and secretary fees alone can add £5,000–£15,000 annually before any listing costs. A Private Ltd sidesteps most of these until the company scales past the small company audit threshold — typically £10.2 million turnover under UK rules.

Requirements to Form a UK PLC from the UAE

The legal prerequisites are specific. Meet all of them before beginning the application process.

Formation Requirements

- Two directors minimum — at least one must be a natural person (Companies Act 2006, Sections 154–155)

- One qualified company secretary — must meet professional qualification criteria under Section 273

- At least one shareholder — no nationality or residency restrictions; UAE individuals and companies can hold majority or 100% of shares

- UK registered office address — required at all times under Section 86

- Minimum share capital of £50,000 — at least £12,500 (25%) must be paid up before the company can trade

The Trading Certificate Requirement

This is the key procedural step that separates PLC formation from Private Ltd formation. A PLC cannot begin trading or borrowing until Companies House issues a Trading Certificate.

To obtain one, the company must apply using Form SH50 and demonstrate that:

- The allotted share capital meets the £50,000 minimum

- At least 25% of the nominal value of each share (plus any premium) has been paid up

- A statement of compliance confirms all formation requirements are satisfied

Unlike a Private Ltd, which can begin operating the day incorporation is confirmed, a PLC sits in a holding pattern until this certificate arrives.

Key Incorporation Documents

- Memorandum of Association

- Articles of Association (bespoke drafting is standard practice for a PLC)

- Details of all directors and the company secretary

- UK registered office address

- Statement of capital showing share structure and paid-up amounts

Share Capital Planning for UAE Founders

UAE companies should plan their share structure before filing — not after. Decisions to make upfront:

- Share types: Ordinary shares are standard; preference shares may suit investors who want fixed returns or priority on wind-up

- Nominal value: Commonly £1 per share, but there's no legal minimum

- Documentation: Cross-border capital transfers require proper records for compliance with both UAE and UK regulatory requirements

Getting the documentation right at this stage matters. Errors in share capital statements or compliance filings are among the most common reasons Trading Certificates are delayed. VJM Global works with UAE companies on cross-border capital structuring and UK compliance filings, helping founders avoid the procedural gaps that hold up trading approval.

Step-by-Step: How to Register a UK PLC from the UAE

Incorporation Process

- Choose a company name — must end in "PLC" or "public limited company"; check availability on the Companies House register

- Appoint directors and company secretary — minimum two directors (one natural person); secretary must meet qualification criteria

- Draft Memorandum and Articles of Association — bespoke articles are standard for PLCs

- Submit Form IN01 — the incorporation application covering company type, registered office, officers, statement of capital, and shareholder details

- Receive Certificate of Incorporation — Companies House confirms the company exists as a legal entity

- Apply for Trading Certificate (Form SH50) — confirm paid-up capital meets requirements before commencing any business activity

Post-Incorporation Essentials

Receiving your Certificate of Incorporation is only the starting point. These four obligations kick in immediately:

- UK business bank account — non-resident directors often need to start with FinTech or EMI providers, as high-street banks impose stricter onboarding requirements for overseas-owned companies

- Corporation Tax registration — HMRC requires registration within three months of starting business activities

- VAT assessment — registration is mandatory if UK-taxable turnover exceeds £90,000

- Tax residency documentation — UK-incorporated companies are generally UK tax resident, but HMRC also applies the central management and control rule. UAE founders should document board meeting locations and decision records carefully to avoid unintended UK tax exposure

Ongoing Compliance Obligations for UK PLCs

The compliance calendar for a PLC is demanding. Missing deadlines triggers automatic financial penalties, and for UAE-based owners managing remotely, administrative gaps can escalate costs quickly.

Annual Compliance Calendar

| Obligation | Deadline |

|---|---|

| Annual accounts filing | 6 months from financial year-end |

| AGM | Within 6 months of accounting reference date |

| Confirmation statement | Within 14 days of review period end (annually) |

| Corporation Tax return | As directed by HMRC after year-end |

Independent Audit: No Exemptions Available

Section 478 of the Companies Act 2006 explicitly excludes PLCs from the small-company audit exemption. Every PLC must have its financial statements independently audited, regardless of size or turnover. This is a fixed cost of maintaining PLC status.

Corporation Tax and the UK–UAE Treaty

The current UK Corporation Tax main rate is 25% for companies with profits over £250,000. For UAE-based PLCs operating internationally, two additional considerations apply:

- The UK–UAE Double Taxation Convention (in force since 25 December 2016) governs how profits, dividends, and interest are taxed across both jurisdictions — and can reduce withholding tax on payments between a UAE parent and UK subsidiary

- Transfer pricing rules apply where connected parties transact; HMRC will scrutinise whether intercompany pricing reflects arm's length terms, making proper documentation essential

Late Filing Penalties

Companies House penalties for PLCs filing accounts late are considerably steeper than those for Private Ltd companies:

- Up to 1 month late: £750

- 1–3 months late: £1,500

- 3–6 months late: £3,000

- Over 6 months late: £7,500

- Penalties double if accounts are late in two successive years

For UAE-based owners, having a UK-based accounting and compliance partner is a practical safeguard against penalties that compound quickly. VJM Global has supported 250+ UK businesses across cross-border compliance scenarios and can provide ongoing assistance for UAE companies managing UK PLC obligations.

Frequently Asked Questions

What is a public limited company in the UK?

A UK PLC is a company that can legally offer its shares to the public, governed by the Companies Act 2006. It must have at least £50,000 in allotted share capital and obtain a Trading Certificate before trading — distinguishing it from a Private Limited Company, which cannot offer shares publicly to the general public.

Does the UK have LLCs (Limited Liability Companies)?

The UK does not use the term "LLC." The closest equivalent is the Private Limited Company (Ltd), which offers limited liability protection for shareholders — though the UK also has LLPs (Limited Liability Partnerships), which are structurally distinct from both US LLCs and UK Ltd companies.

What is the minimum share capital for a UK PLC?

UK PLCs must have a minimum allotted share capital of £50,000. At least 25% of that — £12,500 — must be paid up before Companies House will issue a Trading Certificate allowing the company to begin operations.

Can a UAE company own shares in a UK PLC?

Yes. UK company law imposes no general nationality or residency restrictions on PLC shareholders. UAE individuals, companies, and investment vehicles can hold shares — including majority or 100% ownership — subject to any sector-specific or sanctions-related rules that apply outside the standard PLC framework.

Do UK PLCs have to be listed on a stock exchange?

No. Listing on the London Stock Exchange or AIM is not a legal requirement for maintaining PLC status. A PLC simply has the right to offer shares publicly — many PLCs remain unlisted and raise capital through private placements.

Is a UK PLC suitable for a small UAE business expanding internationally?

For most UAE SMEs, a Private Limited Company is more practical — lower costs, no minimum share capital, and simpler compliance. A PLC becomes relevant when the business is planning a public listing, seeking institutional investment, or requires public company status to win large-scale commercial contracts.