This is one of the most common and costly misunderstandings for UAE businesses entering the UK market. The £90,000 registration threshold is a rule for UK-based businesses. For overseas companies — classified by HMRC as non-established taxable persons (NETPs) — the rules are fundamentally different, and the obligations kick in immediately.

This article covers how UK VAT works, what the £90,000 threshold actually means, why it doesn't protect UAE businesses, and exactly what you need to do to stay compliant.

Key Takeaways

- The £90,000 UK VAT threshold applies only to UK-established businesses — not UAE companies

- UAE businesses are NETPs and must register for UK VAT from their very first taxable UK sale

- B2B services under the reverse charge mechanism can shift the VAT obligation to the UK buyer, removing your registration requirement

- Late registration triggers backdated VAT liability plus penalties of 5–15% of VAT owed

- Making Tax Digital (MTD) applies from day one of UK VAT registration, requiring quarterly digital submissions via compatible software

What Is UK VAT and How Does It Work?

UK Value Added Tax (VAT) is a consumption tax applied at each stage of production and sale. Businesses collect it from customers on behalf of HMRC and can reclaim the VAT they've paid on their own inputs. The end consumer bears the final cost — the business acts as a collection agent for HMRC.

The Three UK VAT Rates

UK VAT rates fall into three bands:

| Rate | Percentage | Examples |

|---|---|---|

| Standard | 20% | Most goods and services |

| Reduced | 5% | Children's car seats, home energy |

| Zero | 0% | Most food, children's clothing |

Zero-rated sales are still taxable supplies — they count towards your VAT registration threshold and appear on VAT returns. This distinction matters when calculating whether a business has crossed any registration trigger.

UK VAT vs. UAE VAT: Two Separate Systems

UAE businesses already operate under a 5% VAT regime introduced in 2018, so indirect tax isn't new territory. Operating across both jurisdictions, however, means managing two distinct regimes with different rates, thresholds, place-of-supply rules, and filing obligations. UAE compliance does not reduce your UK obligations, and vice versa.

The £90,000 UK VAT Threshold: What It Actually Means (and Who It Applies To)

As of 1 April 2024, the UK VAT registration threshold increased to £90,000 in taxable turnover within any rolling 12-month period. UK-established businesses must monitor their turnover monthly and register once they breach this figure — or when they expect to exceed it within the next 30 days.

What Counts as Taxable Turnover

Taxable turnover includes:

- Standard-rated sales (20%)

- Reduced-rated sales (5%)

- Zero-rated sales (0%)

It excludes VAT-exempt supplies (such as financial services or insurance) and out-of-scope supplies. For example, a UK retailer selling £60,000 of standard-rated goods and £35,000 of zero-rated food has £95,000 in taxable turnover and must register — even though the food attracted no VAT.

The Critical Exception: NETPs Have No Threshold

For UAE businesses, the threshold is irrelevant. HMRC's VAT Notice 700/1 is explicit: the £90,000 registration threshold does not apply to non-established taxable persons (NETPs).

An NETP is any business without a fixed UK establishment — meaning no UK-based presence with permanent staff and operational resources. If a business meets that definition, it must register for UK VAT the moment it makes taxable supplies of any value in the UK, or expects to do so within the next 30 days. There is no minimum turnover. There is no grace period.

A UAE company qualifies as an NETP when it has:

- No UK office or fixed place of business

- No UK-based staff or permanent human resources

- No UK fixed establishment of any kind

That describes most UAE businesses selling into the UK — which means the registration obligation kicks in from the very first sale.

When UAE Businesses Must Register for UK VAT

The registration trigger for a UAE business is its first taxable UK sale. That's it. No rolling 12-month calculation, no threshold monitoring — just the moment a taxable supply is made to a UK customer.

B2B Services: The Reverse Charge Exception

For business-to-business service supplies, the reverse charge mechanism changes the equation. Under HMRC's place of supply rules (VAT Notice 741A), the reverse charge mechanism applies to most B2B services. Under this mechanism, the UK business customer accounts for VAT on the supply — the overseas supplier does not charge UK VAT, and may not need to register.

This applies when:

- The customer is a VAT-registered UK business

- The supply is a taxable service (not exempt)

- The reverse charge procedure applies to that service category

Crucially, this does not eliminate all registration obligations. If a UAE business also makes any B2C supplies, or supplies services where the reverse charge does not apply, registration is still required.

Digital Services to UK Consumers (B2C)

UAE businesses selling digital services — software, e-books, online courses, streaming content — directly to UK consumers must register for and charge UK VAT. The reverse charge only applies between businesses. HMRC's digital services guidance confirms that supplies of digital services to UK consumers are liable to UK VAT from the first transaction.

Physical Goods Shipped from the UAE

Unlike services, selling physical goods to UK customers routes VAT through customs rather than standard VAT registration. The rules depend on consignment value:

- £135 or under: The overseas seller collects and remits VAT at point of sale

- Above £135: Import VAT and customs duty apply at the UK border, collected on arrival

- Key distinction: These import-based obligations are separate from service-based VAT registration requirements

The Cost of Late Registration

Late registration carries real financial consequences. HMRC backdates VAT liability to the date the obligation arose, meaning any VAT you should have collected from customers becomes your debt — whether you charged it or not.

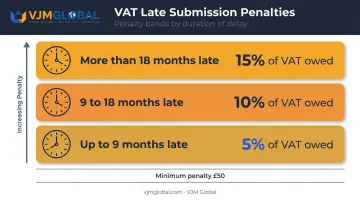

The penalty rates for late VAT registration are:

- Up to 9 months late: 5% of VAT owed

- 9–18 months late: 10% of VAT owed

- More than 18 months late: 15% of VAT owed

- Minimum penalty: £50

The VAT liability is calculated from when registration was due to when HMRC became aware. On meaningful UK revenue, the unpaid VAT plus penalties can add up to a significant sum — especially if the gap spans multiple trading periods.

How to Register for UK VAT as a UAE Business

UAE businesses register as NETPs using the VAT1 form, submitted online or by post to HMRC. There is no requirement for a physical UK presence to register — HMRC processes NETP applications from overseas.

What HMRC Requires

You will need to provide:

- Business name, address, and legal structure

- Description of UK supplies being made

- Expected turnover from UK sales

- Details of any UK fiscal representative (if applicable)

Under section 48 of the VAT Act 1994, HMRC can direct an NETP to appoint a UK VAT representative with joint and several liability. For UAE businesses with no other UK presence, this is a real risk. A qualified VAT agent handles HMRC correspondence, maintains compliant records, and manages filing deadlines on your behalf.

After Registration

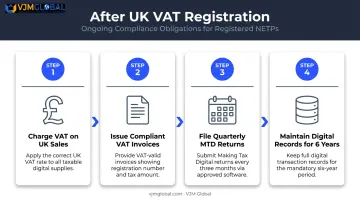

Once registered, HMRC issues a VAT registration number and an effective date. From that date, you must:

- Charge UK VAT on applicable sales

- File quarterly VAT returns through Making Tax Digital (MTD)-compatible software

- Issue compliant UK VAT invoices for every taxable supply

- Maintain digital VAT records

MTD compliance is mandatory — returns must be submitted via software connected directly to HMRC's API platform, not through manual entry or spreadsheets.

Managing NETP registration, MTD filings, and ongoing returns from the UAE means working across multiple layers of HMRC guidance at once. VJM Global has supported 250+ UK businesses across 15+ industries with international tax compliance, including VAT registration and ongoing filing obligations for overseas entities.

UK VAT Compliance Obligations After Registration

Filing VAT Returns

VAT returns are typically filed quarterly. Each return details:

- Output VAT: VAT charged on your UK sales

- Input VAT: VAT paid on UK business purchases

- The net difference is either paid to HMRC or reclaimed as a refund

Returns must be filed digitally through MTD-compatible software. HMRC's Making Tax Digital for VAT rules require digital record-keeping and submission — manual spreadsheet submissions are not compliant.

VAT Invoice Requirements

Every UK VAT invoice must include:

- Your UK VAT registration number

- A unique sequential invoice number

- The date of supply and date of issue

- Customer name and address

- Description, quantity, and net value of goods or services

- Applicable VAT rate and the VAT amount charged

HMRC can disallow input VAT claims on non-compliant invoices — meaning your customers may lose the right to recover VAT they've paid you.

Record-Keeping

Since invoices form part of your mandatory records, HMRC requires all VAT documentation to be kept for at least six years in digital format under MTD rules. This covers:

- Sales and purchase records

- VAT account summaries

- All VAT invoices issued and received

Voluntary VAT Registration: Is It Worth Considering?

Once a UAE business makes any taxable UK supply, registration is mandatory. There is, however, one narrow scenario where voluntary registration becomes relevant: a UAE business making only zero-rated UK supplies (such as certain exported goods) may qualify for exemption from mandatory registration.

In that case, voluntary registration may still be worthwhile to:

- Reclaim input VAT on eligible UK business expenses — professional services, UK goods purchased for business use

- Build credibility with UK B2B clients who expect a VAT number on invoices

- Recover past costs — HMRC permits backdating voluntary registration by up to four years to reclaim input VAT on earlier purchases

Voluntary registration does come with a cost. It introduces quarterly MTD filings, ongoing compliance management from overseas, and potential penalties for late or inaccurate returns. For UAE businesses with minimal UK expenses to reclaim, it's worth calculating whether the recoverable VAT actually justifies the administrative burden before registering.

Frequently Asked Questions

What is the VAT threshold in the UK?

The UK VAT registration threshold is currently £90,000 in taxable turnover within any rolling 12-month period. However, this threshold only applies to UK-established businesses — UAE companies classified as NETPs have no threshold and must register from their first taxable UK sale.

Is the VAT threshold based on turnover or profit?

The threshold is based on taxable turnover — the total value of VATable sales — not profit. A business generating £95,000 in revenue with very thin margins still triggers registration once taxable turnover crosses £90,000.

How can I avoid exceeding the VAT threshold in the UK?

UK-established businesses can monitor rolling 12-month turnover and may apply for temporary exemption if a one-off spike caused the breach. For UAE businesses operating as NETPs, there is no threshold to monitor or avoid — registration is required from the first taxable UK sale.

Do UAE businesses need to register for UK VAT even if their turnover is below £90,000?

UAE businesses supplying taxable goods or services to UK customers must register regardless of turnover. As NETPs, the £90,000 threshold does not apply to them at all.

What is the penalty for late UK VAT registration?

HMRC charges 5% of VAT owed if up to 9 months late, 10% if 9–18 months late, and 15% if more than 18 months late, with a minimum penalty of £50. The business also remains liable for any VAT it failed to collect during the unregistered period.

Can UAE businesses reclaim UK VAT on business expenses?

Yes. Once registered for UK VAT, a UAE business can reclaim input VAT on eligible UK business expenses (such as UK professional services or goods purchased in the UK), provided compliant VAT invoices are held and the expenses relate to taxable supplies.