Introduction

The Resale Price Method (RPM) is one of India's prescribed transfer pricing methods under the Income Tax Act, used to determine whether transactions between related entities reflect arm's length pricing. For UK companies operating Indian subsidiaries, distribution arms, or joint ventures, getting RPM right matters.

India's tax authorities impose penalties of 2% of transaction value for inadequate transfer pricing documentation. Disputes between India and the UK now average 28.67 months to resolve through mutual agreement procedures — making prevention far less costly than resolution.

Many UK finance and tax teams apply RPM without fully understanding how India's domestic rules differ from OECD guidance or HMRC expectations. Indian law prescribes specific computation steps under Rule 10B(1)(b) that go beyond the OECD framework, requiring mandatory functional and accounting adjustments that are easy to overlook.

The gap creates exposure on both sides. An RPM position defensible under OECD principles may fail Indian scrutiny — and an India-compliant approach may contradict the position filed with HMRC, triggering double taxation.

This guide walks through what RPM is, how Indian law defines and applies it under Rule 10B(1)(b), how to compute it correctly, when it's the right method to use, and where UK companies most often go wrong.

Key Takeaways

- RPM benchmarks the reseller's gross profit margin against comparable transactions to set arm's length prices

- Apply Rule 10B(1)(b)'s four-step computation, which requires functional and accounting adjustments that go beyond standard OECD guidance

- RPM works best when the Indian entity performs limited distribution functions without significant value addition

- UK companies must align their Indian RPM documentation with HMRC positions to avoid double taxation

- India's 1%/3% tolerance band offers a safe harbour if your pricing falls within the applicable range

What Is the Resale Price Method?

RPM takes the price at which an associated enterprise resells a product to an unrelated customer (the resale price), deducts an appropriate gross profit margin benchmarked against comparable uncontrolled transactions, and treats the result as the arm's length purchase price paid to the related party supplier. RPM focuses exclusively on the distributor's gross margin — unlike the Comparable Uncontrolled Price (CUP) method, which works directly from transaction prices, or the Cost Plus method, which starts from the supplier's cost base.

The method ensures the reselling entity earns a gross margin consistent with what an independent distributor performing similar functions would earn, rather than allowing profits to accumulate artificially at either the supplier or reseller level.

RPM is particularly suitable for straightforward distribution arrangements — specifically where the Indian entity imports finished goods from its UK parent and resells them without substantial modification. In practice, this covers a wide range of UK-India structures:

- Finished goods imported and sold through an Indian subsidiary with limited value-add

- Distribution arrangements where the Indian entity bears routine selling and marketing risks

- Structures where the UK parent retains ownership of intangibles and product IP

- Low-risk distributors operating under a principal model

That suitability hinges on one technical requirement that catches many companies off guard. Gross margin, not net margin: RPM benchmarks gross margin (revenue minus cost of goods sold), not operating profit. The Delhi ITAT in Swarovski India v. ACIT held that "comparable companies should be restricted to such companies for which Gross Profit Margin can be computed without allocations/truncations." This accounting consistency requirement is frequently misapplied — UK companies using net-margin comparables risk having their benchmarking rejected outright by Indian tax authorities during transfer pricing audits.

RPM Under Indian Transfer Pricing Regulations

India codifies RPM under Rule 10B(1)(b) of the Income Tax Rules, 1962, applicable to any "international transaction" or "specified domestic transaction" involving an associated enterprise. UK companies with Indian subsidiaries, liaison offices, or distribution entities fall within scope if they meet any of the 13 deemed-association criteria under Section 92A, including:

- Direct or indirect holding of 26% or more of voting power

- Advance of a loan constituting 51% or more of total book value of the borrower's assets

- Appointment of more than 50% of the board of directors

- Total dependence on intellectual property licensed by the other enterprise

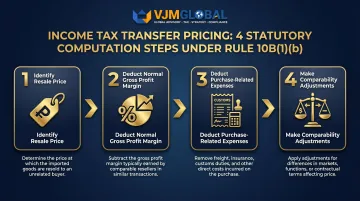

Statutory Computation Steps Under Rule 10B(1)(b)

Rule 10B(1)(b) prescribes a sequential four-step computation:

- Identify the resale price — the price at which property purchased or services obtained from an associated enterprise are resold to an unrelated party

- Deduct the normal gross profit margin — the margin that would be earned if the same or similar product were purchased from and resold to unrelated parties

- Deduct purchase-related expenses — expenses incurred in connection with the purchase (e.g., customs duty, freight, insurance)

- Make comparability adjustments — adjust for material differences between the controlled and uncontrolled transactions affecting gross margin

Where the same Indian entity also trades with unrelated parties, those internal comparables take priority over external database comparables. If internal comparables are unavailable, external comparables from databases must undergo detailed comparability screening.

Before applying the gross margin benchmark, several adjustment categories must be identified, quantified, and resolved:

- Credit terms — differences in payment periods between controlled and uncontrolled transactions

- Inventory risk — which party bears obsolescence or holding risk

- After-sales warranties — whether warranty obligations differ across comparable transactions

- Cost classification — whether transport or discount costs are treated as COGS or operating expenses

Failure to perform these adjustments is one of the most common triggers for transfer pricing disputes in India.

Section 92C of the Income Tax Act requires RPM to be selected only where it produces the most reliable arm's length result. Rule 10C sets out six selection factors, covering the nature of the transaction, functional analysis, data availability, degree of comparability, and the reliability of any adjustments made.

Transfer pricing documentation is mandatory where the international transaction value exceeds INR 1 crore (approximately £95,000). Form 3CEB must be filed by 31 October of the assessment year.

How to Calculate the Arm's Length Price Using RPM

Core formula:

Arm's Length Price = Resale Price − Comparable Gross Profit Margin − Directly Related Purchase Expenses

Step 1: Determine the Resale Price

The starting point is the actual price at which the Indian entity sells the product to an unrelated Indian or international customer — supported by sales invoices. Where multiple sales exist, clearly state whether you are using a per-transaction price or a weighted average.

Example: UK-based GlobalTech Ltd supplies finished electronics to its Indian subsidiary, GlobalTech India Pvt Ltd, which resells to Indian retailers. GlobalTech India's average resale price is INR 10,000 per unit.

Step 2: Identify and Benchmark the Gross Profit Margin

This step requires a comparability analysis. You must identify comparable uncontrolled distributors operating in the same or similar product category, performing similar functions, and assuming similar risks.

Indian transfer pricing regulations permit use of an arm's length range when multiple comparables are identified. If the tested party's gross margin falls within this range, no adjustment is required.

CBDT Notification No. 116/2024 confirms the applicable tolerance bands:

- 1% for wholesale trading transactions (where purchase cost of finished goods is 80%+ of total cost)

- 3% for all other cases

Example: After screening external comparables, you identify five independent electronics distributors in India with gross margins ranging from 18% to 24%, with a median of 21%. The 3% tolerance band means GlobalTech India's actual gross margin must fall within this comparables range of 18–24% to avoid adjustment. At 22%, it does.

Step 3: Deduct Expenses and Adjust for Differences

With the benchmark gross margin established, deduct directly associated purchase expenses — customs duty, freight, insurance — and make functional or accounting adjustments for any material differences between the tested party and comparables.

Worked Example:

| Line Item | Amount (INR) |

|---|---|

| Resale Price to Indian customer | 10,000 |

| Less: Benchmarked Gross Margin (21%) | (2,100) |

| Less: Customs Duty | (500) |

| Less: Freight and Insurance | (200) |

| Arm's Length Purchase Price from UK Parent | 7,200 |

Actual Purchase Price from UK Parent: INR 7,400

Variance: INR 200 (2.7% difference)

Conclusion: The actual purchase price of INR 7,400 exceeds the arm's length price of INR 7,200 by INR 200. This falls within the 3% tolerance band and would not require adjustment.

Adjustment scenarios: Where the Indian entity's actual gross margin exceeds the benchmarked arm's length range, the transfer price paid to the UK parent was likely understated. Where the margin falls below the range, the transfer price may have been overstated. In either case, the Indian tax authority can impose a transfer pricing adjustment — and where the deviation is material, penalty exposure under Section 271AA or 271G of the Income Tax Act follows.

When Should UK Companies Use RPM in India?

Ideal UK-India Scenario for RPM

RPM works best in a classic distribution model: a UK company (manufacturer or brand owner) supplies finished goods to an Indian subsidiary or related party that resells them to Indian customers without significant modification. The Indian entity performs only selling and marketing functions and does not add value through processing, manufacturing, or development of intangibles.

Key conditions for RPM reliability:

- Indian entity operates as a limited-risk distributor

- No substantial product modification or value addition

- No ownership of trademarks or proprietary branding

- Limited R&D functions

- Straightforward buy-sell arrangement

When RPM Loses Reliability

RPM becomes unreliable when:

- The Indian entity holds trademarks or develops proprietary branding — the gross margin reflects those value-added activities, not simple resale

- The Indian entity substantially modifies the product through processing, assembly, or customisation — Cost Plus or TNMM may be more appropriate in these cases

- The Indian entity performs R&D functions — intangible value created cannot be captured in a straightforward reseller margin

- A significant time-lag exists between purchase and resale — the OECD Transfer Pricing Guidelines confirm that "a resale price margin is more accurate where it is realised within a short time of the reseller's purchase." GBP/INR exchange rate fluctuations, market condition changes, and cost structure shifts can materially distort the analysis.

UK-India DTAA Considerations

The India-UK Double Taxation Avoidance Agreement does not specify transfer pricing methods but establishes the arm's length principle as the governing standard in Article 10.

Any RPM-based position adopted in India must be consistent with the position filed with HMRC. Contradictory adjustments in the two jurisdictions can trigger double taxation — making dual-jurisdiction documentation a practical necessity, not just a compliance formality.

Documentation Obligations

Indian transfer pricing rules require contemporaneous documentation. Key requirements include:

- Contemporaneous transfer pricing study documenting method selection rationale

- Form 3CEB certification from a Chartered Accountant in India (due 31 October)

- Functional analysis of the Indian entity (FAR analysis)

- Benchmarking study using comparable distributor margins

- Master File (where consolidated group revenue exceeds INR 500 crore and aggregate international transactions exceed INR 50 crore)

Indian penalties for non-compliance include:

- 2% of transaction value for failure to maintain documentation (Section 271AA)

- 2% of transaction value for failure to furnish information (Section 271G)

- INR 100,000 for failure to file Form 3CEB (Section 271BA)

- 100-300% of tax on adjustment amounts

VJM Global's transfer pricing team has helped 250+ UK businesses navigate these obligations, aligning India filings with HMRC positions to avoid contradictory adjustments across jurisdictions.

Key Factors and Limitations of RPM in India

Factors Affecting RPM Reliability

Functional comparability: The more functions the Indian entity performs beyond basic distribution (e.g., marketing, after-sales service, warranty support), the harder it is to find reliable comparables. Independent distributors with similar functional profiles are scarce in many industries.

Accounting consistency: Differences in how costs such as freight, discounts, and warranties are classified between COGS and operating expenses can distort gross margin comparisons. The Swarovski ITAT ruling requires that comparables permit clean gross margin computation "without allocations/truncations."

Product similarity: While RPM tolerates more product variation than CUP, significant differences in product value, brand recognition, or intangible content can undermine comparability. This is particularly challenging where the UK parent owns a valuable trademark and the Indian entity benefits from brand-driven demand.

The One-Sided Analysis Limitation

RPM focuses solely on the reseller's gross margin, which can produce extreme results for the related supplier. The Indian entity may appear to earn an arm's length margin while the UK parent is implicitly earning either too much or too little. Indian authorities may examine the supplier's implied margin to verify overall transaction reasonableness, even though RPM does not formally benchmark the supplier.

Common Misconceptions

RPM vs. TNMM — not interchangeable: OECD Transfer Pricing Guidelines (paragraph 2.68) note that "net profit indicators are less affected by transactional differences than gross profit margins." RPM benchmarks gross margins; TNMM benchmarks operating margins. Swapping the two requires a full re-run of the comparability analysis.

Single comparable is not accepted: Indian rules require an arm's length range derived from multiple comparables, not reliance on a single comparable.

UK parent's margin is not irrelevant: Indian authorities can and do examine the economic substance of the overall transaction structure, including the reasonableness of the supplier's implied margin.

Conclusion

The Resale Price Method is a well-defined, statutorily prescribed method under Indian transfer pricing rules. It works reliably when the Indian entity performs straightforward distribution functions without significant value addition.

For UK companies, the key risk lies in correct application within India's specific regulatory framework under Rule 10B(1)(b) — and in maintaining consistency with UK transfer pricing positions filed with HMRC.

The Mumbai ITAT's recent ruling in Netflix India, which deleted a INR 444.93 crore transfer pricing adjustment, demonstrates that limited-risk distributor characterisations are defensible when supported by robust functional analysis — but only where documentation meets Indian standards.

VJM Global supports UK businesses with full-cycle transfer pricing compliance in India, including RPM documentation, Form 3CEB preparation, benchmarking studies, and coordination with UK group transfer pricing policies. With 30+ years of experience and a track record serving 250+ UK businesses, our transfer pricing team understands both Indian regulatory requirements and HMRC expectations.

Frequently Asked Questions

What is the resale price method in transfer pricing in India?

RPM is a traditional transaction method under Rule 10B(1)(b) of India's Income Tax Rules. It determines the arm's length price for distribution transactions by benchmarking the Indian reseller's gross profit margin against comparable uncontrolled transactions.

How is the resale price method calculated for transfer pricing in India?

The calculation follows four steps:

- Identify the resale price charged to the unrelated customer

- Deduct the benchmarked gross profit margin from comparable uncontrolled transactions

- Deduct directly related purchase expenses such as customs duty and freight

- Adjust for functional and accounting differences to arrive at the arm's length price

How does the Resale Price Method differ from the Cost Plus Method in India?

RPM starts from the resale price and works back to the transfer price by deducting the distributor's gross margin. The Cost Plus Method, by contrast, starts from the supplier's cost base and adds a mark-up. RPM suits distribution entities; Cost Plus suits manufacturers or service providers.

What documentation do UK companies need to support an RPM transfer pricing position in India?

UK companies need the following documentation ready before the 31 October filing deadline:

- Contemporaneous transfer pricing study

- Comparability and benchmarking analysis of gross margins

- Functional analysis of the Indian entity

- Form 3CEB certification from a qualified Indian Chartered Accountant

Does the India-UK DTAA affect how the Resale Price Method is applied?

The DTAA upholds the arm's length principle but does not specify transfer pricing methods — method selection is governed by Indian domestic law under Section 92C. UK companies must ensure their Indian RPM position aligns with their HMRC filing to avoid contradictory adjustments and double taxation.

What are the most common mistakes UK companies make when applying RPM in India?

Common errors include:

- Using a single comparable instead of an arm's length range

- Failing to adjust for accounting differences between comparables and the tested party

- Applying RPM to entities that perform significant value-added functions

- Not aligning the Indian transfer pricing position with the UK group's consolidated documentation