This article breaks down clear definitions, the legal frameworks that govern each path (including Chapter 11 and IRC §368), when each approach applies, and the tax and compliance implications US businesses must account for.

Key Takeaways

- Restructuring covers broad operational, financial, or organizational changes—often pursued proactively outside of court

- Reorganization is a formally defined legal process under Chapter 11 bankruptcy or IRC §368, with regulatory requirements attached

- In Chapter 11 proceedings, the two terms overlap: restructuring is the mechanism that produces the legal reorganization outcome

- Out-of-court restructuring may trigger taxable cancellation of debt (COD) income, while IRC §368 reorganizations can qualify as tax-free

- The right path depends on solvency, creditor dynamics, and whether court-specific tools like the automatic stay are needed

What Is Business Restructuring?

Business restructuring is a broad process in which a company makes significant changes to its operations, finances, workforce, assets, or business model. It is not always a distress signal—many companies restructure proactively to sharpen competitiveness or realign strategy.

The Three Primary Types

- Financial restructuring — Modifying debt obligations, renegotiating loan terms, or changing the capital structure through debt-for-equity swaps or refinancing

- Operational restructuring — Simplifying processes, eliminating underperforming divisions, reducing overhead, or downsizing the workforce

- Organizational restructuring — Changing management hierarchy, merging departments, or shifting ownership and governance models

How Common Is It?

The scale of restructuring activity in the US is substantial. According to Moody's Ratings, roughly 65% of all corporate defaults in 2025 were distressed restructurings—including workouts, indenture modifications, and debt-for-equity swaps.

On the operational side, Challenger, Gray & Christmas reported that restructuring drove 133,611 US job cuts in 2025 alone.

Restructuring is generally out-of-court. It does not require judicial oversight unless it escalates to a formal insolvency proceeding. Companies often pursue informal "workout" agreements with creditors: a faster, less public alternative to formal filing. Restructuring can occur before, during, or entirely independently of any bankruptcy process.

What Is Business Reorganization?

Business reorganization is a formal process of changing a corporation's structure, finances, ownership, or management within a defined legal or regulatory framework. Unlike restructuring, reorganization is not simply a management decision—it involves court or regulatory oversight and carries specific legal consequences.

Reorganization Under US Law: Two Distinct Frameworks

Chapter 11 Bankruptcy

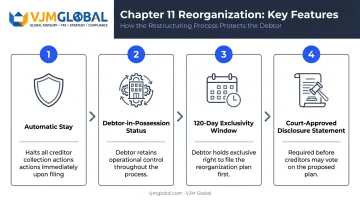

Under the US Bankruptcy Code, Chapter 11 is synonymous with "reorganization bankruptcy." When a company files, it submits a Plan of Reorganization detailing how it will address its debts while continuing to operate. Key features include:

- Automatic stay under 11 U.S.C. §362 — immediately halts creditor collection actions, lawsuits, and foreclosures

- Debtor-in-possession status — management retains control, with trustee-equivalent powers under 11 U.S.C. §1107

- 120-day exclusivity window — the debtor has the initial right to file the plan before creditors can propose alternatives

- Court-approved disclosure statement — required under 11 U.S.C. §1125 before the plan can be circulated to creditors for a vote

According to Epiq, there were 7,879 commercial Chapter 11 filings in 2024, up 20% from 2023—and 7,940 filings in 2025.

Tax-based reorganizations follow a separate path entirely.

IRC §368 Tax-Free Reorganizations

The Internal Revenue Code defines seven types of corporate reorganizations under 26 U.S.C. §368 that can qualify for tax-free treatment:

| Type | Description |

|---|---|

| A | Statutory merger or consolidation |

| B | Stock acquisition giving acquirer control |

| C | Asset acquisition for voting stock |

| D | Asset transfer with required stock distribution |

| E | Recapitalization |

| F | Change in identity, form, or place of organization |

| G | Asset transfer in a Title 11 or similar case |

These reorganizations are distinct from bankruptcy. A real-world example: the 2022 AT&T/WarnerMedia/Discovery transaction was structured to qualify as a reorganization under IRC §368(a)(1)(D). The distribution was tax-free to AT&T stockholders, with narrow exceptions for cash received in lieu of fractional shares.

The Overlap Zone

In Chapter 11, the terms "restructuring" and "reorganization" are functionally inseparable: restructuring the business is how the reorganization is achieved. Outside of bankruptcy, however, they diverge sharply. A company can restructure operations, cut costs, and realign its workforce without ever filing under the Bankruptcy Code or triggering a tax event under the IRC—making the distinction critical when choosing the right legal path.

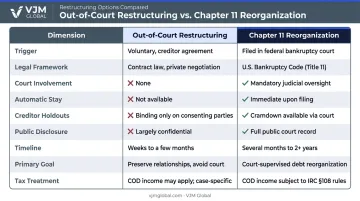

Restructuring vs. Reorganization: Key Differences at a Glance

| Dimension | Out-of-Court Restructuring | Chapter 11 Reorganization |

|---|---|---|

| Trigger | Financial strain or strategic pivot | Inability to service debt; creditor pressure |

| Legal framework | No formal legal process required | US Bankruptcy Code, 11 U.S.C. Chapter 11 |

| Court involvement | None | Full court supervision; major actions require approval |

| Automatic stay | Not available | Yes, under 11 U.S.C. §362 |

| Creditor holdouts | Can block the deal | Court can bind dissenting classes via cramdown |

| Public disclosure | Generally private and informal | Schedules, court filings, and disclosure statements required |

| Timeline | Often faster if creditors agree | Can take months to years |

| Primary goal | Operational or financial efficiency | Legal and financial rehabilitation |

| Tax treatment | COD income may be taxable | IRC §368 reorganizations can be tax-free |

These distinctions matter beyond terminology. Restructuring can be targeted and partial — addressing only the debt load, for example, without touching governance or existing contracts. Reorganization under US law tends to affect the entire corporate entity: creditors, equity holders, and existing contracts all fall within scope.

Many business owners treat these terms as synonyms, but the IRS and the Bankruptcy Code do not. The IRS assigns specific definitions under IRC §368 that determine whether a transaction is tax-free. The Bankruptcy Code assigns procedural rights and obligations that govern what creditors can and cannot do. Choosing the wrong path — or simply mislabeling it — carries real financial consequences.

When Does a US Business Need Restructuring vs. Reorganization?

The choice between the two paths often comes down to whether informal negotiation can realistically work—or whether court tools are necessary to compel creditor compliance.

Signals That Point Toward Out-of-Court Restructuring

- Cash flow is tightening, but the business remains solvent

- Debt is concentrated among a manageable group of identifiable creditors

- Creditors are willing to negotiate informally

- The company wants to avoid the reputational impact of a public filing

- The restructuring primarily addresses funded debt rather than operational or contractual complexity

Signals That Indicate Chapter 11 May Be Necessary

- The company cannot service its debt obligations

- Creditor lawsuits, foreclosures, or collection pressure require the automatic stay

- Holdout creditors can block an out-of-court deal

- The business needs to reject burdensome leases or executory contracts—a right only available in bankruptcy

- Multi-creditor negotiations are too complex for a private workout

- Asset sales need court approval to transfer free and clear of liens

Both paths above assume a primarily domestic creditor base. For foreign companies operating in the US—subsidiaries of businesses based in India, the UK, or Australia, for example—the picture gets more complex.

Cross-Border Considerations: Chapter 15

Chapter 15 of the Bankruptcy Code (11 U.S.C. §§1501–1532) provides mechanisms for recognizing foreign insolvency proceedings in US courts. US courts reported 273 Chapter 15 filings for the 12-month period ending March 2025—up 26% year-over-year—reflecting the growing volume of multinational restructurings with a US nexus.

Tax and Compliance Implications for US Businesses

The tax treatment of restructuring versus reorganization can differ dramatically—and the difference often runs into the millions.

Out-of-Court Restructuring: COD Income Risk

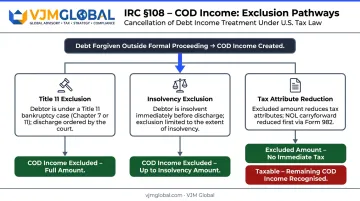

When a creditor forgives or reduces debt outside of a formal proceeding, the forgiven amount generally constitutes cancellation of debt (COD) income taxable to the debtor. Under IRC §108, exclusions are available in specific circumstances:

- Title 11 — COD income is excluded if the discharge occurs in a bankruptcy case

- Insolvency — COD income is excluded to the extent the taxpayer is insolvent at the time of discharge (up to the insolvency amount only)

- Tax attribute reduction — When COD income is excluded, the debtor must reduce tax attributes (such as net operating loss carryforwards) under IRC §108(b), reported on IRS Form 982

Debt-for-equity swaps carry their own complexity: under IRC §108(e)(8), the debtor is treated as satisfying the debt with money equal to the fair market value of the stock transferred. If that value is less than the debt, COD income results.

IRC §368 Reorganizations: Tax-Free Potential

Reorganizations that qualify under IRC §368 can be structured as tax-free transactions, provided they meet two critical tests:

- Continuity of interest — A meaningful portion of the consideration must consist of the acquirer's stock

- Continuity of business enterprise — The acquiring corporation must continue the target's historic business or use a significant portion of its historic business assets

Meeting both tests allows the transaction to avoid immediate recognition of gain—often the decisive factor when comparing transaction structures to taxable asset sales or out-of-court debt forgiveness.

Compliance Obligations: A Clear Contrast

| Obligation | Out-of-Court Restructuring | Chapter 11 Reorganization |

|---|---|---|

| Amended tax filings | May be required for debt modifications | Required; coordinated with US Trustee |

| Financial statement updates | Possible depending on modification terms | Monthly operating reports to US Trustee |

| Public disclosures | Generally none | Court-supervised disclosure statements |

| IRS reporting | Form 982 if COD income is excluded | Ongoing compliance through the case |

The compliance picture grows more complex for US businesses with cross-border structures. Companies with Indian subsidiaries or foreign parent companies face obligations under both US tax law and Indian regulatory frameworks—including FEMA, RBI reporting requirements, transfer pricing rules, DTAA application, and withholding tax obligations that restructuring events can trigger.

VJM Global's international taxation practice works with US-based businesses managing these multi-jurisdictional demands, helping coordinate cross-border compliance across both US and Indian regulatory requirements.

Frequently Asked Questions

Is restructuring the same as reorganization?

Not precisely. Restructuring refers broadly to operational or financial changes a company makes to improve viability. Reorganization is a formal legal process under the US Bankruptcy Code (Chapter 11) or IRC §368, with specific regulatory requirements attached.

What are the three types of restructuring?

The three main types are financial restructuring (modifying debt and capital structure), operational restructuring (streamlining processes, cutting costs, eliminating divisions), and organizational restructuring (changing management hierarchy, ownership structure, or corporate governance arrangements).

What is another term for restructuring?

Common alternatives include "turnaround," "business transformation," and "workout" (specifically for informal out-of-court debt negotiations). In a bankruptcy context, "rehabilitation" describes the same process.

What typically triggers a company to consider restructuring or reorganization?

Common triggers include declining revenues, unsustainable debt, loss of key customers, economic downturns, and strategic shifts like mergers or divestitures. Formal reorganization typically follows when informal options are exhausted or creditors require court oversight.

How does Chapter 11 reorganization differ from Chapter 7 liquidation?

Chapter 11 allows the business to keep operating while restructuring its debts under court supervision, with the goal of long-term viability. Chapter 7 results in the business ceasing operations entirely—a trustee collects and liquidates assets to pay creditors in order of priority.

Does business reorganization affect shareholders?

Yes, significantly. Under the absolute-priority rule (11 U.S.C. §1129), shareholders sit last in the repayment waterfall and cannot receive value until senior creditors are paid in full. In most Chapter 11 cases, existing equity is substantially diluted or eliminated entirely.