Introduction

Picture this: a business owner receives an unexpected letter from the ATO — not a routine notice, but a penalty assessment for a missed BAS deadline and underpaid superannuation. The amounts owed, including the General Interest Charge at 11.43% per annum (compounding daily), have grown well beyond the original liability. The business was profitable, well-run, and genuinely unaware of what it had missed.

This scenario is far more common than most business owners realise. Australian tax compliance isn't a single annual task — it means managing GST, PAYG withholding, superannuation, income tax returns, and more, each running on its own reporting cycle.

This guide covers five practical strategies to help you avoid penalties, manage deadlines, and keep your business compliant — whether you're an established SME or navigating Australian tax obligations for the first time.

Key Takeaways

- Know your business structure — it determines every registration and reporting obligation you have

- Accurate, separated financial records are your first line of defence against ATO scrutiny

- Plan cash flow around tax deadlines proactively — missed lodgements compound penalties fast

- Accounting software and a dedicated business account reduce errors and save time at every lodgement

- A registered tax agent provides a legal compliance safeguard, not just administrative convenience

What Is Business Tax Compliance — and Why It Matters

Business tax compliance means fulfilling all ATO-imposed obligations accurately and on time. For Australian businesses, that covers:

- Income tax returns (individual, company, trust, or partnership)

- Business Activity Statements (BAS) for GST and PAYG withholding

- Superannuation guarantee contributions

- Payroll tax (state-level obligations)

- PAYG instalment payments

That's a fundamentally different challenge from personal tax compliance. An individual files one return per year; a business juggles multiple obligations running on separate deadlines — quarterly, monthly, and annually — at the same time.

The Real Cost of Getting It Wrong

The ATO's compliance reach is substantial. The small business tax gap alone reached $27.2 billion in 2022-23, representing a significant share of uncollected tax from businesses that either misreported or failed to lodge at all.

When the ATO does act, the financial consequences stack quickly:

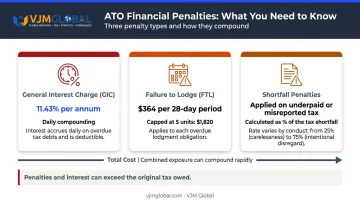

- General Interest Charge (GIC): Currently 11.43% per annum (daily compounding) on unpaid liabilities

- Failure to Lodge (FTL) penalties: 1 penalty unit ($364 from 1 July 2026) per 28-day period overdue, capped at 5 units — with multipliers applied to medium and large businesses

- Penalties on shortfall amounts: Applied where tax has been underpaid or incorrectly reported

In many cases, the penalties and interest charges exceed the original tax owed — which means a missed lodgement or reporting error can cost far more than the underlying liability itself.

Strategy 1: Understand Your Business Structure and Its Tax Obligations

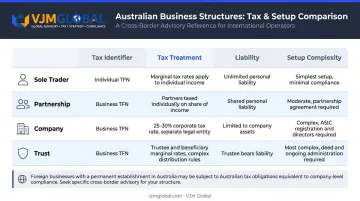

Australia has four main business structures: sole trader, partnership, company, and trust. Each carries distinct obligations, and getting the wrong setup — or misunderstanding what your structure requires — creates compliance gaps from day one.

| Structure | TFN Required | Company Tax Rate | Key Feature |

|---|---|---|---|

| Sole Trader | Individual TFN | Marginal rates | Simplest; personal liability |

| Partnership | Business TFN | Partners pay individually | Shared liability |

| Company | Business TFN | 25–30% | Separate legal entity |

| Trust | Business TFN | Trustee/beneficiary rates | Complex distribution rules |

Core Registrations Every Business Needs

Before trading, confirm you have:

- ABN — an 11-digit identifier required for invoicing and GST registration

- TFN — sole traders use their individual TFN; all other structures need a business TFN

- GST registration — mandatory once annual turnover reaches $75,000 ($150,000 for non-profits)

- PAYG withholding registration — required before paying wages or salaries to employees

Superannuation as a Compliance Obligation

Super is not optional. The Superannuation Guarantee (SG) rate reached 12% on 1 July 2025 — the final legislated increase. Employers must pay the correct amount by quarterly deadlines (28 October, 28 January, 28 April, 28 July). Missing those dates triggers the Superannuation Guarantee Charge (SGC), which includes additional penalties and interest on top of the unpaid amount.

The risk escalates at the director level. Under the director penalty regime, directors can be held personally liable for unpaid PAYG withholding, GST, and superannuation guarantee charge — meaning the company's compliance failures become individual financial liabilities.

For foreign-owned businesses, the compliance picture is more layered. A US or UK company with an Australian branch may trigger local tax obligations through a permanent establishment, meaning Australian tax applies to profits attributable to that branch.

Transfer pricing rules also apply to related-party transactions crossing borders. Identifying which Australian laws govern your structure before you begin trading — not after — is the clearest way to avoid costly retrospective corrections.

Strategy 2: Maintain Accurate and Up-to-Date Financial Records

The ATO requires businesses to keep all records explaining their transactions for a minimum of five years. Records must be in English (or easily convertible) and available on request during an audit or compliance check.

In practice, accurate record-keeping means:

- Keeping business and personal finances in completely separate accounts

- Recording every income source — sales, investments, grants, and asset disposals

- Retaining receipts and documentation for all claimed deductions

- Maintaining an asset register for capital gains tax purposes

Why the ATO Will Notice Discrepancies

The ATO collects over 600 million transactions annually through data matching — cross-referencing business income against bank data, industry benchmarks, and third-party reports from financial institutions and government agencies. It also publishes small business benchmarks by industry, which it uses to identify businesses reporting outside the expected range.

Common record-keeping failures that trigger scrutiny:

- Claiming deductions without supporting documentation

- Mixing personal and business expenses in a single account

- Leaving reconciliation until the end of the financial year

- Inconsistencies between reported income and bank deposits

The Broader Value of Good Records

Avoiding these failures isn't just about passing an audit. Monthly or quarterly reconciliations give businesses a practical edge year-round:

- Meeting BAS deadlines accurately without last-minute scrambling

- Catching errors early, before they flow through to tax returns

- Presenting credible financials to lenders or investors when it counts

The cost of ongoing bookkeeping support is almost always lower than the professional fees and penalties involved in reconstructing records under ATO scrutiny.

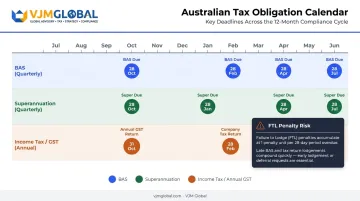

Strategy 3: Meet Deadlines and Plan Ahead for Tax Payments

Key Australian Tax Deadlines

| Obligation | Frequency | Standard Due Date |

|---|---|---|

| BAS (quarterly) | Quarterly | 28 Oct / 28 Feb / 28 Apr / 28 Jul |

| BAS (monthly) | Monthly | 21st of following month |

| Superannuation | Quarterly | 28 Oct / 28 Jan / 28 Apr / 28 Jul |

| Company tax return (self-lodged) | Annual | 28 February |

| Annual GST return | Annual | 31 October (if income tax return required) |

Note: Registered tax agents access extended deadlines through the ATO's lodgement program — a practical advantage for businesses using professional support.

PAYG Instalments: Prepaying Your Tax

PAYG instalments require businesses to prepay estimated income tax throughout the year. For companies and super funds, the ATO will typically enrol you if your instalment income reaches $2 million or more, or your notional tax is $500 or more. Businesses with instalment income above $20 million must lodge and pay monthly.

This spreads tax payments across the year, making cash flow predictable and avoiding a large lump sum at lodgement time. Failing to participate when required attracts penalties.

Cash Flow Planning as a Compliance Tool

Treat tax as a fixed operating cost, not a year-end surprise. Businesses that reserve funds throughout the year consistently avoid payment shortfalls at lodgement time.

Build these amounts into your cash flow forecast as firm line items:

- GST collected — held separately, not treated as revenue

- PAYG instalments — calculated from your instalment notice and set aside each quarter

- Income tax — estimated from prior-year liability and adjusted as the year progresses

The FTL Penalty Compounds Quickly

The Failure to Lodge (FTL) penalty accumulates at one penalty unit per 28-day period the return remains outstanding, capped at five units before size multipliers apply. At $364 per unit from 1 July 2026, a small business with one overdue quarterly BAS can accumulate $1,820 in FTL penalties alone, with the GIC running separately on any unpaid amount.

Strategy 4: Use Technology and Maintain a Separate Business Account

Start With a Dedicated Business Bank Account

A separate business account is the simplest structural decision a business owner can make for compliance purposes. The Australian Government's business guidance confirms that keeping private and business transactions separate saves time and money when preparing financial documents, activity statements, and tax returns.

Practically, it means:

- Cleaner income and expense tracking without manual separation

- A clear audit trail if the ATO requests records

- No risk of personal expenditures being questioned as business deductions

Accounting Software Reduces Errors

Cloud-based tools like Xero, MYOB, and QuickBooks connect directly to business bank feeds, categorise transactions automatically, and generate BAS-ready reports. For businesses with employees, Single Touch Payroll (STP) has been mandatory since 2019 — meaning payroll data (wages, PAYG withholding, and superannuation information) reports to the ATO automatically each pay cycle.

Key compliance functions that good accounting software handles:

- Real-time bank reconciliation

- Automatic GST coding on transactions

- BAS preparation and lodgement

- Super calculation and payment tracking

- PAYG withholding calculations

Manage Compliance Online with the ATO's Digital Services

The ATO's Online Services for Business platform allows businesses to lodge BAS, track payment status, update registrations, and access lodgement history in one place. Going digital also matches the ATO's broader push toward fully online compliance. In practice, it eliminates the risk of paperwork being lost or submitted with errors.

Strategy 5: Engage a Qualified Tax Professional for Ongoing Compliance Support

Tax legislation in Australia is not static. Rates change, thresholds shift, and your obligations depend heavily on your business structure, turnover, and transaction types. A qualified registered tax agent or chartered accountant keeps your lodgements correct, your deductions legitimate, and your penalty exposure low.

Practical Advantages of Using a Registered Tax Agent

Australia had 63,865 registered tax practitioners as of 30 June 2025, regulated by the Tax Practitioners Board (TPB). Working with one gives your business:

- Extended lodgement deadlines through the registered agent program

- Representation during ATO audits or compliance reviews

- Access to private rulings for complex or uncertain transactions

- Proactive updates on legislative changes that affect your obligations

- Tax deductibility — the cost of managing your tax affairs is itself a deductible business expense- Tax deductibility: the cost of managing your tax affairs is itself a deductible business expense

Cross-Border Operations Need Specialist Support

For businesses operating across jurisdictions — foreign companies with an Australian branch, or Australian businesses with international related-party transactions — compliance obligations multiply quickly. Key areas requiring specialist advice include:

- Transfer pricing rules — ensuring related-party transactions are priced at arm's length

- Permanent establishment assessments — determining your Australian tax presence

- International Dealings Schedule (IDS) — mandatory disclosure for cross-border transactions

- DTAA considerations — applying double tax agreement relief correctly

Each of these requires advisors who understand both the Australian framework and the relevant foreign tax system.

VJM Global's team of Chartered Accountants supports businesses managing multi-country compliance, with a particular focus on cross-border structures involving Australia, the US, and the UK. For businesses expanding into India, the firm provides integrated compliance support covering Indian GST, income tax, transfer pricing, and FEMA advisory — built on over 30 years of international tax experience.

Frequently Asked Questions

What is business tax compliance?

Business tax compliance means meeting all obligations imposed by the ATO — filing returns, paying GST, managing PAYG withholding, and meeting superannuation duties — accurately and on time. Falling short triggers financial penalties, interest charges, and potential legal exposure.

What are the taxation requirements for a business in Australia?

At minimum, Australian businesses must meet these core obligations:

- Obtain an ABN and TFN

- Register for GST once turnover exceeds $75,000

- Lodge BAS and pay PAYG withholding

- Pay superannuation for employees

- Lodge an annual income tax return suited to their structure

What happens if a business is not tax compliant in Australia?

Non-compliance triggers ATO-imposed financial penalties, daily compounding interest on overdue amounts, and heightened scrutiny. In serious cases, the ATO can pursue legal prosecution, and the total cost often exceeds the original tax owed.

What records should a business keep for tax compliance?

Businesses must retain all financial records for a minimum of five years. This includes receipts, invoices, bank statements, payroll records, and asset registers. The ATO can request these during an audit or compliance check at any point during that period.

What is the difference between tax compliance and tax planning?

Tax compliance is about meeting current legal obligations correctly and on time. Tax planning is a forward-looking strategy to legally structure your finances and reduce future tax liability. Both matter — compliance prevents penalties, planning improves outcomes.