Introduction

UK businesses expanding into Asia-Pacific markets frequently encounter Singapore's corporate income tax system—a mandatory compliance obligation for all companies operating in the jurisdiction, including subsidiaries and branches of foreign enterprises. Governed by the Inland Revenue Authority of Singapore (IRAS), Singapore applies a flat 17% corporate income tax (CIT) rate on chargeable income, substantially lower than the UK's 25% main Corporation Tax rate.

While UK finance directors are familiar with HMRC's Corporation Tax framework, Singapore's system operates on entirely different timelines, return types, and terminology. Misunderstanding these differences—particularly the distinction between Estimated Chargeable Income (ECI) and the full Income Tax Return, or the implications of Singapore's preceding-year basis of assessment—is one of the most common sources of non-compliance penalties for foreign-owned companies.

UK businesses routinely overlook withholding tax obligations on payments to parent companies, apply UK financial reporting standards incorrectly, or fail to claim available tax exemptions. Under IRAS's Start-Up Tax Exemption (SUTE) scheme, eligible companies can reduce their effective tax rate by 50% or more in early years. This guide covers the key filing obligations, deadlines, and compliance pitfalls UK businesses need to understand before their first Singapore tax return.

Key Takeaways

- Singapore's flat 17% CIT rate delivers an 8-percentage-point advantage over the UK's 25% rate

- Two mandatory annual filings: ECI within 3 months of financial year end, and Form C/C-S/C-S (Lite) by 30 November

- UK-Singapore DTA reduces withholding tax on cross-border payments, but UK businesses must claim relief via a Certificate of Residence

- Start-Up Tax Exemption delivers up to S$125,000 relief for qualifying companies in their first 3 years

- Late filing triggers composition fines up to S$5,000 and potential prosecution by IRAS

What Is Singapore Corporate Tax Filing?

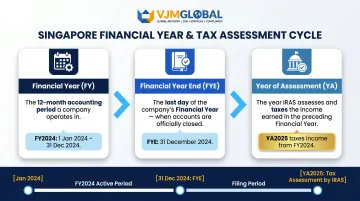

Corporate income tax filing in Singapore is the process by which a company registered or operating in the jurisdiction reports its taxable income to IRAS and fulfils its annual tax obligations. Singapore assesses tax on a preceding-year basis—income earned in financial year 2024 is taxed in Year of Assessment (YA) 2025, creating a one-year lag between earning income and paying tax.

Three Core Timing Concepts

UK businesses often confuse three fundamental concepts in Singapore's tax calendar:

| Concept | What It Means | Example |

|---|---|---|

| Financial Year (FY) | The 12-month accounting period for which a company prepares its accounts. Singapore companies can choose any year-end date — unlike the UK's fixed April-to-April cycle. | FY 2024 |

| Financial Year End (FYE) | The closing date of the financial year. | 31 December 2024 |

| Year of Assessment (YA) | The calendar year in which income from the preceding FY is assessed and taxed. | YA 2025 (for FY ending 31 Dec 2024) |

Practical Example:

Say your Singapore subsidiary closes its books on 31 December 2024. Those profits are assessed in YA 2025, with your ECI filing due by 31 March 2025 (three months after FYE) and your full Income Tax Return (Form C/C-S) due by 30 November 2025.

Singapore's Territorial Tax System vs. UK Worldwide Taxation

Singapore taxes income sourced in Singapore and foreign-sourced income received in Singapore. The UK taxes worldwide profits of UK-resident companies — a fundamental difference that creates separate obligations in each jurisdiction.

Your UK parent files with HMRC on worldwide profits (which may include Singapore subsidiary income, depending on structure), while your Singapore entity files with IRAS on Singapore-sourced and remitted foreign income. The UK-Singapore Double Taxation Agreement prevents double taxation on the same profits, but you must actively claim relief.

Why Singapore's Tax System Appeals to UK Businesses

Significant Rate Differential

Singapore's 17% flat CIT rate is 8 percentage points below the UK's 25% main Corporation Tax rate. For a UK business generating £1 million in profits through a Singapore subsidiary, this differential translates to £80,000 in annual tax savings — and that's before factoring in available exemptions and incentives.

One-Tier Taxation Eliminates Dividend Double Taxation

Under Singapore's one-tier corporate tax system, dividends paid by Singapore-resident companies are exempt from further tax in shareholders' hands. UK parent companies receiving dividends from Singapore subsidiaries face no additional Singapore-level tax on distributions—the 17% paid by the subsidiary is final.

UK-Singapore DTA Reduces Withholding Tax

The 1997 UK-Singapore DTA caps withholding tax rates on cross-border payments:

| Payment Type | Singapore Domestic Rate | DTA Rate |

|---|---|---|

| Interest | 15% | 10% |

| Royalties | 10% | 10% |

| Technical service fees | 17% | 0% (no PE) |

| Dividends | 0% (one-tier system) | N/A |

Critical requirement: UK businesses must obtain a Certificate of Residence (COR) from IRAS to claim these treaty benefits. Without a valid COR, domestic withholding tax rates apply, and IRAS may impose penalties of up to 20% of the tax due.

How to File Corporate Tax in Singapore: Step-by-Step

Singapore corporate tax filing requires two separate mandatory submissions each year: the Estimated Chargeable Income (ECI) and the Income Tax Return (Form C/C-S/C-S Lite). Both are filed electronically via IRAS's myTax Portal using your company's CorpPass account.

Step 1: Confirm Your Financial Year End and Year of Assessment

Your Financial Year End drives all filing deadlines. If your Singapore subsidiary closes books on 31 March 2025, your ECI is due by 30 June 2025 (3 months after FYE), and your Form C/C-S is due by 30 November 2025 for YA 2026.

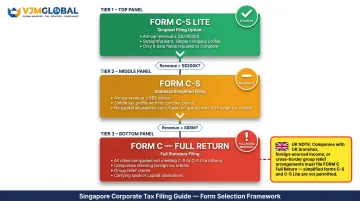

Step 2: Select the Correct Income Tax Return Form

Form C-S Lite: Singapore-incorporated companies with annual revenue ≤ S$200,000 and simple tax profile (only 6 fields required).

Form C-S: Revenue ≤ S$5 million with simple tax profile; not claiming group relief, carry-back, investment allowance, or foreign tax credit.

Form C (full return): All other companies, including those with revenue above S$5 million, claiming group relief, foreign tax credits, or investment allowances. Most UK branch offices or larger subsidiaries require Form C.

Critical for UK businesses: Any company claiming foreign tax credits to offset UK tax on the same profits must file Form C with full financial statements, even if revenue falls below S$5 million.

Step 3: File the Estimated Chargeable Income (ECI)

ECI must be submitted within 3 months of your FYE via myTax Portal. It is not the final tax computation — that comes later with your ITR.

ECI filing waiver: Companies with revenue ≤ S$5 million and nil ECI are exempt.

GIRO instalment benefit: Filing ECI within 1 month of FYE provides up to 10 monthly interest-free instalments; within 2 months provides 8 instalments; within 3 months provides 6 instalments.

Step 4: File the Income Tax Return (Form C/C-S/C-S Lite)

The ITR must be filed by 30 November of the YA, regardless of when the ECI was submitted. The two filings are independent.

Form C requirements:

- Full financial statements prepared under Singapore Financial Reporting Standards (SFRS), not UK GAAP or IFRS

- Complete tax computation

- Supporting schedules for all claims and deductions

Form C-S and C-S Lite: No attachments required at submission, though supporting documents must be retained for IRAS review.

Step 5: Respond to the Notice of Assessment and Pay

After review, IRAS issues a Notice of Assessment (NOA). Tax is due within 1 month of the NOA date. GIRO instalment plans can smooth cash flow. If you disagree with the NOA, a Notice of Objection must be filed within 2 months of the NOA date—but payment remains due during the objection period.

What UK Businesses Must Know: Exemptions, Incentives, and Withholding Tax

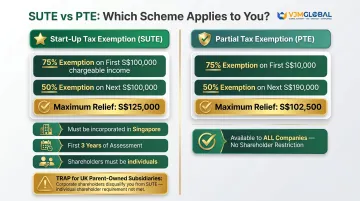

Start-Up Tax Exemption (SUTE)

Singapore-incorporated companies in their first 3 YAs qualify for substantial relief:

- 75% exemption on first S$100,000 of chargeable income

- 50% exemption on next S$100,000 of chargeable income

- Maximum exemption: S$125,000 per YA

Qualifying conditions:

- At least one individual shareholder holding 10% equity

- Total shareholders ≤ 20

- Not primarily engaged in property development or investment holding

Critical trap for UK businesses: A UK parent company fully owning a Singapore subsidiary typically does not qualify for SUTE if no individual shareholder holds 10% equity. Consider structuring shareholdings to meet this requirement—for example, a UK director holding 10% with the parent holding 90%.

Partial Tax Exemption (PTE)

Companies not qualifying for SUTE receive PTE:

- 75% exemption on first S$10,000 of normal chargeable income

- 50% exemption on next S$190,000 of normal chargeable income

- Maximum exemption: S$102,500 per YA

Withholding Tax on Cross-Border Payments

When your Singapore entity makes payments to the UK parent company, Singapore withholding tax (WHT) applies:

Standard WHT rates:

- Interest: 15% (reduced to 10% under DTA)

- Royalties: 10% (no reduction under DTA)

- Technical service fees: 17% (0% under DTA if no PE)

- Management fees: 17% (0% under DTA if no PE)

WHT filing and payment: Due by the 15th of the second month from payment date to the non-resident.

Penalties for non-compliance:

- 5% late payment penalty if not received by due date

- Additional 1% per month up to maximum 15% for tax unpaid beyond 30 days

- Combined maximum penalty: 20% of unpaid tax

UK businesses with Singapore subsidiaries making regular intra-group payments (management fees, royalties, interest on loans) must set up clear WHT compliance processes and obtain a valid COR to claim DTA benefits.

VJM Global's Cross-Border Compliance Expertise

VJM Global has advised 250+ UK businesses on international tax matters, including WHT compliance, DTA claims, and transfer pricing documentation. The firm helps UK parent companies coordinate their obligations between HMRC and IRAS — so nothing falls through the gap between two tax systems.

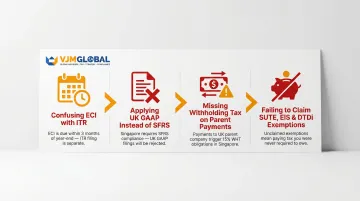

Common Mistakes UK Businesses Make When Filing Corporate Tax in Singapore

Conflating ECI with the Income Tax Return

Many UK businesses assume filing the ECI satisfies their annual tax obligation—it does not. ECI is an estimate submitted within 3 months of FYE. The Income Tax Return (Form C/C-S/C-S Lite) must still be filed by 30 November. Both filings are mandatory and independent.

IRAS enforcement data shows that late or non-filing remains a persistent compliance issue, with penalties escalating rapidly for companies that miss multiple years.

Applying UK Financial Reporting Standards

Financial statements submitted with Form C must be prepared under Singapore Financial Reporting Standards (SFRS), not IFRS or UK GAAP. Differences in treatment—particularly depreciation versus capital allowances, revenue recognition, and provisions—affect taxable income calculations. UK finance teams applying familiar UK methods incorrectly risk assessment adjustments and penalties.

Missing Withholding Tax Obligations on UK Parent Payments

Payments from a Singapore entity to the UK parent trigger WHT obligations in Singapore — a recurring compliance gap flagged by IRAS. Non-compliance consequences include:

- Penalties of up to 20% of the tax due

- Appointment of recovery agents (banks, solicitors) to collect overdue amounts

Failing to Claim Available Exemptions and Deductions

Businesses unfamiliar with Singapore-specific schemes frequently miss legitimate deductions that reduce taxable income significantly:

- Enterprise Innovation Scheme (EIS) — 400% tax deductions on up to S$400,000 per activity per YA for qualifying R&D, IP registration, IP acquisition, and training expenditure (YA 2024–2028)

- Double Tax Deduction for Internationalisation (DTDi) — 200% deduction on up to S$150,000 (increasing to S$400,000 from YA 2027) for international market expansion expenses

- Capital allowances — qualifying fixed assets reduce taxable income under Singapore rules, similar in concept to UK capital allowances but calculated differently

Frequently Asked Questions

When is the deadline to file a corporate tax return in Singapore, and what if I file late or need an extension?

Form C/C-S/C-S Lite is due by 30 November each YA; ECI is due within 3 months of financial year end. Late filing results in composition fines up to SGD 5,000 and potential prosecution. IRAS does not routinely grant extensions, though requests can be submitted via myTax Portal in limited circumstances.

Does Singapore have corporate income tax?

Yes, Singapore levies corporate income tax at a flat rate of 17% on chargeable income, with partial exemptions available that effectively reduce the rate on the first SGD 200,000 of chargeable income for most companies.

Who pays corporate tax in Singapore?

All companies carrying on business in Singapore—including Singapore-incorporated subsidiaries of UK companies and registered foreign branches—are subject to Singapore CIT on Singapore-sourced income and foreign-sourced income received in Singapore.

How do I pay corporate tax in Singapore?

Payment is due within 1 month of the Notice of Assessment. Companies can pay via GIRO (with instalment plans up to 10 months if ECI is filed on time), internet banking, PayNow QR, or other IRAS-approved payment channels via myTax Portal.

Does the UK-Singapore Double Taxation Agreement affect what UK businesses pay in Singapore?

The UK-Singapore DTA can reduce or eliminate withholding taxes on cross-border payments and prevent double taxation on the same profits. UK businesses must actively claim DTA relief by submitting a Certificate of Residence (COR) to IRAS. Relief is not applied automatically.

Do UK businesses need to file corporate tax in both the UK and Singapore?

Yes. A UK business with a Singapore subsidiary must file separately in each jurisdiction: Singapore CIT for the Singapore entity with IRAS, and UK Corporation Tax for the UK parent with HMRC (which may include overseas income depending on structure). The DTA helps prevent double taxation on the same profits.