Introduction

If your Singapore company grants RSUs to employees based in India, Indian tax law treats you — or your Indian subsidiary — as the employer responsible for withholding tax at vesting. The fair market value of shares at vest is taxable perquisite income under Section 192 of the Income Tax Act 1961, and the deduction obligation falls on whoever pays the salary.

This guide covers the key obligations, timelines, and treaty considerations Singapore companies need to understand before the next vesting cycle. Getting this wrong carries real costs:

- TDS defaults and failure-to-deduct notices under Section 201(1A)

- Interest at 1% per month for non-deduction, 1.5% per month for late deposit

- Penalties up to ₹10 lakh per undisclosed foreign asset

- Double taxation risk without proper DTAA (India-Singapore) documentation

Key Takeaways

- RSUs are taxable in India at vesting: FMV of shares is treated as a salary perquisite, triggering TDS under Section 192

- The Indian subsidiary holds the withholding obligation even when the Singapore parent grants the RSUs

- Capital gains tax applies separately on sale: slab rates for holdings under 24 months, 12.5% LTCG beyond 24 months

- India-Singapore DTAA provides relief via Form 67, not exemption from withholding

- Indian entities must report RSU perquisites in Form 16 and file Form 24Q each quarter

- Employees are required to disclose foreign shares annually under Schedule FA

What Is RSU Withholding Tax in India?

RSU withholding tax is the TDS obligation arising under Section 192 of the Indian Income Tax Act when an employee's RSUs vest and shares of determinable fair market value are credited. The employer must deduct tax on the perquisite value before or at the time of delivering shares.

This is distinct from capital gains tax. Withholding applies at vesting on the full FMV — treated as salary income — meaning the employee does not need to sell shares to trigger this liability. A separate capital gains calculation applies only on any subsequent sale above the FMV at vesting.

How India's treatment compares to Singapore's approach:

| Treatment | Singapore | India |

|---|---|---|

| Tax at vesting | Employment income | Salary perquisite (TDS required) |

| Tax on sale | No capital gains tax | Capital gains tax applies |

| Employer obligation | Withhold and report | Deduct TDS, file returns |

This dual-stage tax structure — perquisite at vesting, then capital gains on sale — is what makes India compliance more complex for Singapore parent companies managing cross-border equity.

How RSU Withholding Works in India: A Step-by-Step Breakdown

The compliance flow runs through three distinct stages:

Grant Stage

No tax liability or withholding obligation arises at grant. The employee has no ownership or economic benefit yet, so neither the Singapore company nor the Indian entity needs to act from a tax withholding standpoint.

Vesting Stage

On the vesting date, the FMV of each vested share is converted from SGD to INR using the SBI Telegraphic Transfer Buying Rate. That value, multiplied by the number of shares vested, becomes the perquisite added to the employee's taxable salary.

Example calculation:

- 200 shares vest

- FMV per share: SGD 50

- SBI TTBR on vesting date: 1 SGD = ₹62

- Perquisite value: 200 × 50 × 62 = ₹6,20,000

The Indian employer deducts TDS at the employee's applicable income tax slab rate — up to 30% plus cess and surcharge. For high earners, the effective rate can reach 39–42.7%. TDS must be deposited by the 7th of the following month.

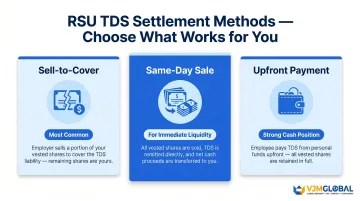

Three settlement methods:

| Method | Process | Best For |

|---|---|---|

| Sell-to-cover | Employer withholds and sells a portion of shares to fund TDS | Most common for cross-border RSU programs |

| Same-day sale | Employee converts all shares to cash, tax remitted, net proceeds transferred | Employees seeking immediate liquidity |

| Upfront payment | Employee pays TDS from other funds, retains all shares | Employees with strong cash position |

Sale Stage

Once vested shares are sold, a separate capital gains tax obligation arises — calculated from the FMV on the vesting date, not the original grant price.

| Holding Period | Classification | Tax Rate |

|---|---|---|

| Under 24 months | Short-Term Capital Gains (STCG) | Applicable income tax slab rate |

| 24 months or more | Long-Term Capital Gains (LTCG) | 12.5% without indexation (effective July 23, 2024) |

The cost basis for capital gains is the FMV on the vesting date. This means employees are taxed only on gains above that value — not on the perquisite income already taxed at vesting.

Key Factors That Affect a Singapore Company's RSU Withholding Obligation

Who Grants the RSU vs. Who Withholds the Tax

If the Singapore parent grants RSUs but services are rendered in India, the Indian subsidiary remains responsible for withholding under Indian tax law. This distinction catches many Singapore finance teams off guard at audit time.

Employee Residential Status Determines Tax Scope

Residential status determines how much of the RSU income falls within India's tax net:

- Resident and Ordinarily Resident (ROR): Full withholding applies on global RSU income

- Non-Resident (NR) or Resident but Not Ordinarily Resident (RNOR): Taxed only on India-sourced perquisite income

An employee becomes resident after 182+ days in India during a financial year. ROR status requires residency in 2 or more of the preceding 10 financial years and 730+ days in the preceding 7 years.

FMV Valuation Requirements for Foreign Shares

SGX-listed and unlisted Singapore company shares are not traded on Indian exchanges, so their fair market value must be independently certified. The requirements under Rule 3(8)(b) of the Income Tax Rules are:

- Valuation must be performed by a SEBI-registered Category I merchant banker

- The report must be dated within 180 days prior to the vesting date

- Share value must be converted to INR using the SBI Telegraphic Transfer Buying Rate (TTBR)

Vesting frequency and advance tax: Multiple vesting tranches across a financial year require the payroll team to re-estimate tax liability after each event, which flows through to quarterly TDS filing obligations under Form 24Q.

Cross-charge and transfer pricing: Reimbursement between the Singapore parent and Indian subsidiary for RSU costs affects the Indian entity's deductibility position. These arrangements should be documented through intercompany agreements benchmarked at arm's length.

The India-Singapore DTAA and Avoiding Double Taxation

Under Article 15 (Dependent Personal Services) of the India-Singapore DTAA, employment income — including RSU perquisite income — earned by an Indian resident employee is taxable in India. Since Singapore does not impose tax on RSU income for employees who were never employed in Singapore, double taxation at vesting is rare for India-based employees.

That said, employees who did pay tax in Singapore on the same RSU income — for example, during a prior employment stint there — can claim Foreign Tax Credit (FTC) in India by filing Form 67 before submitting their Indian Income Tax Return (ITR). The credit is limited to the lower of:

- Tax paid in Singapore, or

- Indian tax on the same income

Form 67 requirements:

- Deadline: End of the assessment year (March 31), per CBDT Notification No. 100/2022

- Verification: Via Aadhaar OTP or Electronic Verification Code (EVC)

- Attachments: Certificate specifying nature of income, foreign tax amount, and proof of payment

Critical clarification: The India-Singapore DTAA does not exempt the Indian entity from its TDS withholding obligation. It only provides relief to the employee against double taxation after the fact. Singapore companies that instruct their Indian payroll teams to skip TDS on RSUs citing DTAA protection are in violation of domestic withholding rules — the treaty does not override that obligation.

Compliance and Reporting Obligations for Singapore Companies

Indian Employer Filing Responsibilities

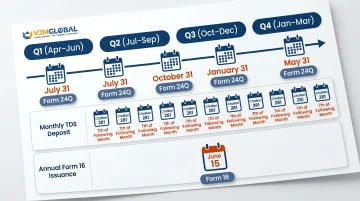

TDS deposit and quarterly returns:

| Obligation | Form | Deadline |

|---|---|---|

| Q1 TDS Return (Apr-Jun) | Form 24Q | July 31 |

| Q2 TDS Return (Jul-Sep) | Form 24Q | October 31 |

| Q3 TDS Return (Oct-Dec) | Form 24Q | January 31 |

| Q4 TDS Return (Jan-Mar) | Form 24Q | May 31 |

| TDS Deposit | Challan 281 | 7th of following month (April 30 for March) |

| TDS Certificate to Employee | Form 16 | June 15 of assessment year |

Non-filing or incorrect filing attracts penalties under Section 234E (₹200 per day, capped at total TDS amount) and Section 271H (₹10,000 to ₹1,00,000).

Employee Reporting Obligations

Singapore companies should communicate these requirements clearly to their Indian staff:

- Include RSU perquisite income in ITR-2 or ITR-3 under "Income from Salary"

- Report vested shares held in Singapore brokerage accounts in Schedule FA annually — even if not yet sold

- Report share sale proceeds in Schedule CG when shares are disposed of

Black Money Act penalty: Non-disclosure of foreign assets attracts a flat penalty of ₹10 lakh per year per undisclosed asset under the Black Money Act 2015.

Given the layered obligations involved, Singapore companies without an in-house India tax team often work with a specialist to manage these requirements. VJM Global handles the end-to-end process — perquisite and FMV computation, Form 24Q filing, Form 16 issuance, and DTAA position advisory — so nothing falls through the gaps.

Common Misconceptions Singapore Companies Make About RSU Withholding

Misconception 1: Singapore Parent Grants = No Indian Withholding Obligation

Indian tax law requires the employer in India — the entity paying salary and providing employment — to withhold TDS on all salary income including perquisites from parent-company RSU grants. Ignoring this exposes the Indian entity to TDS default interest under Sections 201 and 220.

Misconception 2: DTAA Eliminates the Need to Withhold

DTAA provisions operate as relief mechanisms for the employee and do not override the employer's statutory withholding obligation. TDS must be deducted first, and the employee then claims credit separately via Form 67.

Misconception 3: Unvested RSUs Need No Tracking

While unvested RSUs are not taxable, Singapore companies should maintain records from the grant date onward. Indian tax authorities may scrutinise these during assessment. A change in the employee's residential status between grant and vesting can also alter the withholding calculation significantly.

At minimum, track the following for each grant:

- Grant records and original award documentation

- Vesting schedules with milestone dates

- Fair market value (FMV) data as of the grant date

Frequently Asked Questions

Are RSUs taxable in India?

Yes, RSUs are taxable at two stages: at vesting (as perquisite income added to salary, taxed at slab rates up to 30%) and at sale (as capital gains). No tax arises at grant.

What is RSU withholding tax in India?

RSU withholding tax is TDS deducted by the Indian employer under Section 192 at vesting, calculated on the fair market value of vested shares converted to INR. This must be deposited with Indian tax authorities and reported in Form 24Q.

How are US RSUs taxed in India?

US RSUs follow the same framework (perquisite income at vesting, capital gains on sale), with FMV converted using SBI TTBR. Indian employees can claim Foreign Tax Credit under the India-US DTAA by filing Form 67 if US taxes were withheld. For Singapore companies, the same mechanics apply under the India-Singapore DTAA instead.

Do I pay double tax on RSUs?

Double taxation risk exists but is mitigated under the India-Singapore DTAA. Indian residents can claim Foreign Tax Credit for Singapore taxes paid on the same RSU income. The credit is capped at the lower of foreign tax paid or Indian tax on that income, and must be claimed via Form 67 filed along with the ITR.

Do I need to declare RSU in ITR?

Yes, Indian resident employees must declare RSU perquisite income under salary in their ITR and report vested shares held in foreign brokerage accounts under Schedule FA of ITR-2 or ITR-3. Failure to disclose foreign assets attracts a penalty of ₹10 lakh per year under the Black Money Act, 2015.