This guide covers not just the mechanics of company registration, but the strategic decisions that precede it: choosing the right legal structure, leveraging the India-Singapore tax treaty, managing transfer pricing obligations, and maintaining ongoing compliance. India offers a combination of factors—1.4 billion consumers, deep engineering and technology talent, and improving regulatory ease—that no other market in Asia currently matches for Singapore businesses ready to scale beyond ASEAN.

TLDR

- Singapore accounts for 23.87% of all FDI equity into India (USD 171.92 billion cumulative), establishing a mature investment corridor

- The India-Singapore DTAA reduces withholding taxes, but capital gains treaty benefits are now fully phased out for shares acquired post-March 2019

- Private Limited Company structure is the most common route for Singapore investors, qualifying for 100% FDI under automatic route in most sectors

- End-to-end incorporation via SPICe+ takes 10-15 working days from DSC application to Certificate of Incorporation

- Ongoing compliance includes MCA annual filings, GST returns, TDS obligations, and mandatory transfer pricing documentation for intercompany transactions

Why Singapore Companies Are Expanding to India

Market Size and Growth Fundamentals

India's economy is projected to grow at 6.5% annually through 2026 according to the IMF, significantly outpacing China's expected deceleration to approximately 4%. With a population of 1.45 billion and approximately 68% in working age, India represents the world's largest addressable consumer market still in early-stage development.

The talent advantage is equally compelling. India offers access to a deep pool of engineering, technology, finance, and operations professionals at costs 40-60% lower than Singapore, making it attractive not just for market entry but for building global capability centers.

Validated Investment Corridor

Singapore contributed USD 14.94 billion in FDI to India in FY2024-25, marking its seventh consecutive year as India's top annual FDI source. Cumulative FDI equity from Singapore totals USD 171.92 billion as of December 2024, accounting for nearly one-quarter of all foreign investment into India.

The scale reflects sustained institutional confidence — grounded in regulatory familiarity, treaty protections, and a well-tested dispute resolution framework under CECA.

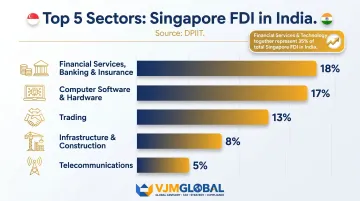

High-Priority Sectors for Singapore Capital

Based on DPIIT data covering January 2000 through December 2024, Singapore FDI concentrates in five primary sectors:

- Financial services, banking, and insurance: 18% of total Singapore FDI

- Computer software and hardware: 17%

- Trading: 13%

- Infrastructure and construction: 8%

- Telecommunications: 5%

Financial services and technology together account for 35% of all Singapore investment, reflecting the complementary strengths of both economies.

Companies like DBS Bank (wholly-owned subsidiary, 530+ branches), STT Global Data Centres, and Singtel (strategic investor in Bharti Airtel) show that Singapore companies are building for the long term — not testing the waters.

Institutional Support Reduces Entry Friction

The Singapore Business Federation launched SEC@Bengaluru in November 2025—its first SEC outside Southeast Asia. The centre targets engagement with 470+ companies over two years and provides market advisory, business matching, incorporation assistance, priority banking, and HR support.

For Singapore SMEs entering India for the first time, SEC@Bengaluru offers a ready-made starting point — from company registration guidance to connecting with vetted local partners.

Business Entry Structures: Choosing the Right Vehicle

Your choice of legal entity shapes everything downstream — which sectors you can enter, how profits flow back to Singapore, and what compliance obligations follow. The right structure depends primarily on your sector, revenue intent, and how quickly you plan to scale.

Private Limited Company (Wholly Owned Subsidiary)

This is the most common and flexible route for Singapore companies. Under the DPIIT Consolidated FDI Policy, 100% FDI is permitted under the automatic route in most sectors, meaning no prior government approval is required.

It offers the strongest foundation for companies planning to grow, hire locally, or raise capital in India:

- Separate legal entity with limited liability protection for the Singapore parent

- Full profit repatriation after applicable taxes

- Ability to raise equity funding or list on Indian exchanges

- Cleanest structure for scaling operations or eventual exit

To incorporate, you'll need:

- Minimum two directors (at least one must be an Indian resident who has stayed in India for 182+ days in the prior year)

- A registered office address in India

- No minimum paid-up capital — this requirement was removed under the Companies Amendment Act 2015

Branch Office

A branch office is an extension of the parent company — it does not have a separate legal identity. Prior RBI approval is required, and the branch can only undertake specific permitted activities:

- Export/import of goods

- Rendering professional or consultancy services

- Research work in areas where the parent company is engaged

- Promoting technical or financial collaborations

- Acting as buying/selling agent

This structure is not suitable for manufacturing, retail, or activities requiring separate entity status. Critically, the parent company remains fully liable for all branch operations — there is no liability shield.

Liaison Office

Where a branch office still carries commercial intent, a liaison office goes further in the other direction — it is strictly non-revenue-generating. Permitted activities are limited to:

- Representing the parent company in India

- Promoting exports/imports between India and the home country

- Facilitating technical or financial collaborations

- Acting as a communication channel

Initial RBI approval is valid for three years and must be renewed. This structure works well for companies in an exploratory phase — gathering market intelligence before committing to full operations.

Limited Liability Partnership (LLP)

FDI is permitted in LLPs under the automatic route only in sectors where 100% FDI is allowed with no performance conditions. For professional services firms that don't need venture capital or debt financing, it offers a lighter compliance footprint than a Private Limited Company.

| Factor | LLP | Private Limited Company |

|---|---|---|

| Compliance burden | Lower | Higher |

| Administrative overhead | Minimal | Moderate |

| External Commercial Borrowings (ECB) | Not permitted | Permitted |

| Convertible instruments | Cannot issue | Can issue |

| VC / institutional investor appeal | Limited | Strong |

| FDI reporting | Form FDI-LLP(I) within 30 days | FC-GPR within 30 days |

The LLP works best for professional services or consulting operations that are self-funded and have no plans to raise institutional capital.

Step-by-Step: How to Register Your Company in India from Singapore

The Ministry of Corporate Affairs (MCA) governs company incorporation through the SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus) system. The entire process can be completed remotely, but requires at least one Indian resident director and a registered India address.

Step 1: Obtain Digital Signature Certificates (DSC)

All proposed directors must obtain a DSC from an MCA-empanelled certifying authority. This digital signature is required for filing all e-forms on the MCA21 portal.

Typical processing time: 2 working days

Step 2: Apply for Director Identification Numbers (DIN)

Each director requires a unique DIN. Foreign nationals apply through Form DIR-3, which requires:

- Passport-size photograph

- Self-attested copy of passport

- Self-attested address proof

- PAN card (if applicable for Indian nationals)

Typical processing time: 1 working day

Step 3: Reserve Company Name

File Part A of SPICe+ to reserve a unique company name. The name must:

- Not be identical or similar to existing registered names

- Comply with MCA naming guidelines

- Not suggest government patronage without permission

Typical processing time: 1-2 working days

Step 4: Draft Constitutional Documents

Prepare the Memorandum of Association (MOA) and Articles of Association (AOA). These are the foundational documents that govern your company's purpose and internal rules. They define:

- Objects and scope of business

- Authorized and paid-up share capital

- Rights and obligations of shareholders

- Governance structure and board powers

Step 5: File SPICe+ Part B for Incorporation

The integrated SPICe+ form covers:

- Company incorporation

- PAN (Permanent Account Number)

- TAN (Tax Deduction Account Number)

- GST registration (GSTIN)

- EPFO and ESIC registration

- Bank account opening linkage via AGILE-PRO

Filing requires the following supporting documents:

- Registered office address proof (utility bill <2 months old or rent agreement + NOC)

- Identity and address proof of all directors and shareholders

- MOA and AOA signed by subscribers

- Declaration and consent forms (DIR-2, INC-9)

Typical processing time: 5-7 working days

Step 6: Certificate of Incorporation and Post-Incorporation Compliance

Upon approval, the RoC issues a Certificate of Incorporation along with PAN and TAN. Two immediate actions are required before operations begin:

- Open a business bank account — Deposit share capital and obtain a Foreign Inward Remittance Certificate (FIRC) to document your FDI inflow.

- File Form FC-GPR within 30 days — Submit through the RBI's FIRMS portal to report the foreign investment. Missing this deadline triggers late fees and potential compounding proceedings under FEMA.

Realistic end-to-end timeline: 10-15 working days from DSC application to Certificate of Incorporation. Sectors not covered under the automatic FDI route require prior government approval, which extends this timeline — confirm your sector's status before starting.

Leveraging CECA and the India-Singapore DTAA

Comprehensive Economic Cooperation Agreement (CECA)

CECA, which entered into force in 2005, provides Singapore companies with structural advantages:

- Tariff reductions: More than 3,000 tariff lines eliminated and another 2,000+ reduced, improving price competitiveness for Singapore products

- Preferential services access: Enhanced market access for Singapore service providers in engineering, banking, telecommunications, and real estate development

- Investment protection: Clear dispute resolution mechanisms and safeguards for Singapore investments

- Strategic positioning: Makes Singapore an attractive hub for global companies targeting the Indian market

India-Singapore Double Taxation Avoidance Agreement (DTAA)

The DTAA prevents the same income from being taxed in both countries and sets maximum withholding tax rates on cross-border payments.

Key withholding tax rates under DTAA:

| Income Type | DTAA Rate | Conditions |

|---|---|---|

| Dividends | 10% | Beneficial owner holds ≥25% shares |

| Dividends | 15% | All other cases |

| Interest (banks/financial institutions) | 10% | Paid to qualifying institutions |

| Interest (others) | 15% | All other cases |

| Royalties and Fees for Technical Services | 10% | Uniform rate |

Capital gains treatment has also shifted significantly under the 2016 Protocol amendments, now fully in effect:

- Shares acquired before April 1, 2017: Grandfathered—taxable only in Singapore (0% in India)

- Shares acquired April 1, 2017 to March 31, 2019: Taxed at 50% of domestic rate

- Shares acquired on or after April 1, 2019: Fully taxable in India at domestic rates

Singapore investors must now factor source-based capital gains taxation into all new equity positions.

Transfer Pricing Compliance: Non-Negotiable Requirement

Beyond treaty benefits, the structure of intercompany transactions carries its own compliance weight. All dealings between a Singapore parent and its Indian subsidiary—management fees, IP licensing, intercompany loans, cost allocations—must be priced at arm's length under Chapter X (Sections 92-92F) of the Income Tax Act.

Penalties for non-compliance are severe:

| Section | Violation | Penalty |

|---|---|---|

| 271AA | Failure to maintain documentation or incorrect reporting | 2% of transaction value |

| 271G | Failure to furnish information to tax authorities | 2% of transaction value |

| 271BA | Failure to file Form 3CEB (accountant's report) | ₹1,00,000 |

VJM Global supports Singapore companies through the full transfer pricing cycle — benchmarking studies, master file and local file preparation, Form 3CEB filing, and representation before tax authorities — so documentation is in place before the first intercompany invoice is raised.

Ongoing Compliance and Tax Obligations for Singapore Companies in India

Annual MCA Compliance

| Requirement | Due Date | Legal Basis |

|---|---|---|

| Form AOC-4 (Financial Statements) | Within 30 days of AGM | Companies Act, 2013 |

| Form MGT-7 (Annual Return) | Within 60 days of AGM | Companies Act, 2013 |

| Statutory Audit | Mandatory for all companies | Companies Act, 2013 |

| Board Meetings | Minimum 4 per year, max gap 120 days | Section 173 |

Corporate Income Tax

Under the new tax regime (Section 115BAA), domestic companies including foreign-owned subsidiaries pay:

22% base + 10% surcharge + 4% cess = 25.17% effective rate

Companies opting for this regime are exempt from Minimum Alternate Tax (MAT). This rate is competitive with major Asian markets and is the right default choice for most new subsidiaries.

Goods and Services Tax (GST)

Registration threshold: INR 40 lakh for normal category states; INR 20 lakh for special category states.

Filing frequency:

- Monthly (GSTR-1 and GSTR-3B) for turnover above INR 5 crore

- Quarterly under QRMP scheme for turnover up to INR 5 crore

VJM Global handles GST registration, return filing (monthly and quarterly), input tax credit reconciliation, and representation before GST authorities.

Tax Deducted at Source (TDS)

Section 195 mandates TDS on all payments to non-residents if the income is chargeable to tax in India. There is no minimum threshold—TDS applies from the first rupee.

Covered payments include:

- Interest on loans from Singapore parent

- Royalties and fees for technical services

- Dividends (withholding applies when the subsidiary pays dividends to the Singapore parent)

- Management fees and cost allocations

Failure to deduct or deposit TDS results in disallowance of the expense under Section 40(a)(i) and attracts interest and penalties.

FEMA and RBI Reporting

TDS governs the tax on outbound payments — FEMA governs the foreign exchange side of the same transactions. Foreign-owned companies must comply with Foreign Exchange Management Act (FEMA) regulations:

- FC-GPR filing within 30 days of share allotment

- Annual FEMA returns for FDI reporting

- FC-TRS filing for share transfers involving non-residents

- Compliance with ECB (External Commercial Borrowing) guidelines if borrowing from Singapore parent

Common Challenges Singapore Companies Face in India

Multi-Layered Regulatory Environment

India's regulatory framework operates at both central and state levels. Singapore companies must navigate:

- FEMA regulations for foreign exchange and investment

- Companies Act for corporate governance and MCA filings

- GST laws varying by state for indirect taxation

- Labor codes differing across states for employment matters

- Sector-specific regulations (SEBI for capital markets, RBI for financial services, DPDP for data protection)

EY India's 2025 compliance analysis highlights heightened scrutiny from multiple regulators simultaneously, tightened FEMA oversight aligned with FATF standards, and uncertainty from pending Digital Personal Data Protection rules.

Resident Director Requirement

Section 149(3) of the Companies Act mandates at least one director who has stayed in India for 182+ days in the previous year. This can be a practical bottleneck for Singapore founders without India-based contacts.

VJM Global provides resident director services and registered office address solutions specifically for Singapore companies without an established India presence — keeping you compliant while you build your local team.

Cultural and Market Localization

Beyond regulatory compliance, market entry success depends on how well you adapt to India's diversity. The country is far from a uniform market — success requires:

- Product localization: Adapting features, pricing, and messaging to regional preferences

- State-level logistics variation: Infrastructure, tax treatment, and ease of doing business differ significantly across states

- Relationship-driven business culture: Trust-building with local talent, vendors, and partners takes time and cultural sensitivity

Singapore companies that treat India as a long-term investment — not a quick revenue play — tend to build stronger distribution networks, retain local talent better, and navigate regulatory friction with less friction over time.

Frequently Asked Questions

Which Singapore companies are operating in India?

Notable Singapore companies operating in India include DBS Bank (banking, 530+ branches), Olam Agro India (agribusiness, since 1989), Singtel (telecom, strategic investor in Bharti Airtel), STT Global Data Centres (data centers), and APL Logistics. Together they represent a broad cross-section of sectors from financial services to infrastructure.

Can a Singapore company open a branch office in India?

Yes, but prior RBI approval is required, and permitted activities are limited to export/import, consultancy, and research. Because the branch carries no separate legal identity, the Singapore parent remains fully liable — most companies find a wholly-owned subsidiary more practical.

Does India have a double taxation agreement with Singapore?

Yes, the India-Singapore DTAA prevents double taxation on income earned in both countries. It reduces withholding tax rates on dividends (10-15%), interest (10-15%), and royalties/FTS (10%). However, capital gains treaty benefits are now fully phased out for shares acquired after March 31, 2019.

How long does it take to register a company in India from Singapore?

The realistic timeline is 10-15 working days from DSC application to Certificate of Incorporation under the automatic FDI route, assuming all documentation is complete. Sectors requiring government approval for FDI can add several weeks to this timeline.

What is the minimum capital requirement to register a company in India from Singapore?

India has no statutory minimum paid-up capital for a Private Limited Company (removed under Companies Amendment Act 2015) — incorporation with as little as INR 1 is permitted. Authorized share capital must still be declared in the MOA, and all FDI must be reported to RBI within 30 days via Form FC-GPR.

What taxes does a Singapore company's Indian subsidiary need to pay?

Core tax obligations include corporate income tax (25.17% effective rate), GST above the turnover threshold, and TDS on non-resident payments. Cross-border payments to the Singapore parent are taxed at DTAA withholding rates, and all intercompany transactions require transfer pricing documentation.

VJM Global helps Singapore companies navigate India market entry — from choosing the right entity structure and completing incorporation to handling GST compliance, transfer pricing documentation, and FEMA reporting. With 30+ years of experience and a 100+ strong team of Chartered Accountants and business setup professionals, we provide the on-ground expertise to establish and scale operations in India.

Contact us at info@vjmglobal.com or call +91 9213397070 to discuss your India expansion strategy.