This article explains when Singapore's audit busy season falls, how to time your preparation based on your financial year-end, what to avoid during peak season, and how year-round readiness keeps you ahead of the rush.

Key Takeaways

- Singapore's audit busy season runs January to April, driven by the concentration of December 31 financial year-ends

- Start audit preparation 2–3 months before your FYE — 3–4 months ahead if your year-end falls on December 31

- Engage your auditor before peak season to avoid scheduling delays, capacity shortfalls, and rushed fieldwork

- Maintain consistent monthly bookkeeping and interim reviews year-round to minimize peak-season stress

- Companies have 6 months from FYE to hold their AGM — missing early auditor engagement puts that deadline at risk

What Is the Audit Peak Period in Singapore?

Singapore's audit peak period isn't a fixed regulatory date — it's an industry-driven surge. Because a substantial majority of Singapore-incorporated companies choose December 31 as their financial year-end, audit firms face their heaviest workload between January and April each year. ACRA's own regulatory reports acknowledge this "bunching" effect, noting that the concentration of December year-ends — particularly among SGX-listed companies — creates a predictable but unavoidable capacity crunch.

How Statutory Deadlines Compress the January–April Window

The Companies Act sets clear deadlines that force all audit activity into Q1:

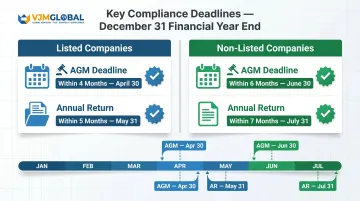

For December 31 FYE companies:

- Listed companies: AGM within 4 months (by April 30), annual return within 5 months (by May 31)

- Non-listed companies: AGM within 6 months (by June 30), annual return within 7 months (by July 31)

Audited financial statements must be presented at the AGM — or sent to members if the AGM is dispensed with under Section 175A — and attached to the annual return filing. That means audit work must be completed well before these deadlines, compressing the entire audit cycle into Q1.

Secondary Peak Periods and FYE Diversity

Not every company follows the December 31 calendar. Companies with March 31, June 30, or September 30 year-ends create secondary peak periods for audit firms — but the January–April window remains the most congested by volume. Regulatory commentary confirms that the majority of Singapore companies use December 31 as their FYE, which is precisely what intensifies competition for audit resources during this period.

How Peak Period Pressure Affects Your Business

During peak season, audit firms prioritize existing clients who booked early. New or late-starting engagements face:

- Longer response times from audit teams stretched across simultaneous engagements

- Assignment to junior staff rather than senior personnel

- Pushed-back fieldwork schedules that compress your timeline

- Risk of being declined entirely if capacity is fully booked

These pressures hit harder for foreign-incorporated companies operating in Singapore or reporting to a global parent. Group consolidation deadlines add a second layer of urgency on top of ACRA's statutory requirements — leaving very little room for a late start.

Why Early Preparation Matters in Singapore's Audit Season

Auditor Availability Is the Primary Constraint

During peak season, reputable audit firms in Singapore are fully booked months in advance. Companies that delay engagement risk:

- Receiving junior staff assignments instead of experienced audit teams

- Getting pushed to later slots that compress your filing timeline

- Being denied timely service altogether if firm capacity runs out

This affects both audit quality and turnaround time. Well-established firms allocate their most experienced teams to clients who engage early and maintain year-round readiness.

Workforce Challenges Compound Peak-Season Strain

The Accountancy Workforce Review Committee (AWRC) report (May 2024) identified long, unpredictable working hours and declining interest in accountancy careers as structural challenges facing the profession. These constraints worsen sharply during peak periods — firms begin hitting staffing ceilings well before January, meaning companies that wait until Q4 to engage an auditor may find their options already narrowed.

Late Audits Create a Chain of Missed Deadlines

A delayed audit triggers cascading compliance failures:

- Late AGM: Composition sum of at least S$500; court fines up to S$5,000 per charge

- Late annual return filing with ACRA: S$300 penalty if filed within 3 months of deadline; S$600 beyond 3 months; risk of striking-off action for persistent non-compliance

- Late corporate tax filing with IRAS: ECI must be filed within 3 months of FYE; Form C-S/C due by November 30; composition amounts up to S$5,000 per offence

ACRA's enforcement escalates quickly: companies that miss deadlines receive a Striking Off Notice, giving 30 days to object before the company is struck off and gazetted.

Quality of Audit Suffers Under Deadline Pressure

Well-prepared records allow auditors to focus on substantive review rather than chasing missing documents. Early preparation gives finance teams time to:

- Resolve account discrepancies before fieldwork begins

- Reconcile all accounts to trial balance

- Address prior-year audit findings

- Discuss complex accounting treatments (revenue recognition, related party transactions, new SFRS standards) with auditors in advance

The contrast is stark for companies that arrive unprepared. Incomplete records produce rushed reviews and a higher likelihood of regulatory findings.

ACRA's Financial Reporting Surveillance Programme (FRSP) Report 2024 found the average number of non-compliance findings per case doubled from 0.70 to 1.40, with smaller companies showing the highest rates of non-compliance.

When to Start Preparing Based on Your Financial Year-End

Preparation timing is tied directly to your financial year-end (FYE) date. Each FYE carries its own statutory deadlines — and working back from those deadlines gives you a concrete schedule of when to act.

Based on a December 31 Financial Year-End

For companies on Singapore's most common FYE, preparation should begin by October:

October–November:

- Reconcile all bank accounts, trade receivables, and payables

- Update fixed asset register with current-year additions and disposals

- Confirm auditor engagement for Q1 fieldwork

- Request pre-audit checklist tailored to your industry

November–December:

- Conduct interim audit work to reduce year-end fieldwork volume

- Review and reconcile GST returns to general ledger

- Compile documentation for major transactions (asset purchases, financing arrangements, significant contracts)

- Hold pre-audit coordination meeting with department heads to assign document responsibilities

January–March:

- Complete year-end fieldwork

- Resolve any audit queries or discrepancies

- Finalise audited financial statements for AGM presentation

Based on a March 31 Financial Year-End

March FYE companies face double pressure: their pre-year-end preparation window (January–February) overlaps with peak season for December FYE companies. This means audit firms are already at maximum capacity when you need them most.

Critical timeline:

- November–December (prior year): Engage auditor and confirm availability

- January–February: Complete account reconciliations and interim audit work

- March–May: Year-end fieldwork and finalization

- By September 30: AGM deadline (non-listed companies)

- By October 31: Annual return filing deadline

For March FYE companies, engaging your auditor by November–December of the prior year is critical. Waiting until January means competing for capacity that December FYE clients have already claimed.

Based on June 30 and September 30 Financial Year-Ends

Mid-year FYEs offer a structural advantage: companies on these schedules fall outside the January–April peak, giving them better access to audit firm capacity and more room to negotiate scheduling.

Recommended timeline:

- 3 months before FYE: Engage auditor and confirm availability

- 2 months before FYE: Begin account reconciliations and interim review

- Month of FYE: Finalise year-end close and begin fieldwork

For June 30 FYE: AGM by December 31, annual return by January 31 (following year) For September 30 FYE: AGM by March 31 (following year), annual return by April 30

Based on Special Business Triggers

Certain events during the financial year require immediate documentation to avoid peak-period scrambles:

- Major asset purchases or disposals

- New financing arrangements or loan agreements

- Significant contracts or revenue arrangements

- Government grants received

- Changes in shareholding structure or related party transactions

Auditors will request these records regardless of when the audit falls. Keeping them current prevents last-minute document hunts and avoids delays that push back audit completion.

Signs You're on Track — And Red Flags to Watch For

Indicators You're Well-Positioned Heading Into Audit Season

Financial records current and reconciled:

- All bank accounts reconciled to general ledger

- Trade receivables and payables confirmed and balanced

- Fixed asset register updated with current-year activity

- Inventory counts completed (if applicable)

Payroll and compliance records complete:

- Payroll records including CPF contributions fully documented

- CPF contributions paid by the 14th of each month (late payment attracts 1.5% monthly interest)

- IR8A forms prepared for year-end filing

GST compliance up to date:

- All quarterly GST F5 returns filed within 1 month of period-end

- GST returns reconciled to general ledger

- Any corrections filed using Form F7

Auditor engagement confirmed:

- Auditor already engaged with confirmed timetable

- Pre-audit checklist received and reviewed

- Internal teams briefed on audit timeline and document requirements

Red Flags That Signal Dangerous Under-Preparation

Accounts not closed since prior quarter:

- Trial balance not prepared or reconciled in months

- Bank reconciliations incomplete or missing

- Unresolved discrepancies accumulating

Late or missing auditor engagement:

- Auditor not yet contacted within 2 months of FYE

- No confirmed fieldwork schedule or pre-audit planning meeting

Incomplete compliance documentation:

- Fixed asset register not updated for current year

- Prior-year audit findings from ACRA or auditor remain unresolved

- GST returns not reconciled to general ledger

What Happens When You Wait Too Long

Each red flag above carries heavier consequences during peak season, when audit firms are already at capacity and won't accommodate last-minute requests. Companies that delay risk:

- Being unable to secure an auditor at all

- Missing ACRA filing deadlines and incurring financial penalties

- Facing striking-off action for persistent non-compliance

Non-compliance doesn't stall indefinitely. ACRA can issue a Striking Off Notice, giving companies just 30 days to object — after which the company is removed from the register.

Best Practices for Navigating Singapore's Audit Busy Season

Treat Monthly Bookkeeping as Year-Round Audit Preparation

Companies that maintain current, accurate records throughout the year enter the audit process with a substantial head start. Consistent monthly or quarterly closings:

- Reduce year-end reconciliation burden from weeks to days

- Allow internal teams to flag issues early rather than under deadline pressure

- Provide real-time visibility into financial performance

- Create a foundation for management decision-making beyond compliance

Engage Your Auditor Before Peak Season Opens

For December FYE companies:

- Confirm audit firm and preliminary timetable by September or October at the latest

- Request pre-audit checklist tailored to your industry

- Discuss complex accounting treatments before fieldwork begins (revenue recognition, related party transactions, new SFRS standards)

For other FYEs:

- Engagement should occur at least 3 months before year-end

- March FYE companies should engage by November–December of the prior year

- Mid-year FYEs (June, September) have more flexibility but should still engage 3 months ahead

Adopt a Cross-Department Preparation Approach

Audit preparation is not solely a finance function. Hold a pre-audit coordination meeting with department heads from:

- Sales: Revenue contracts, delivery documentation, customer confirmations

- Procurement: Purchase orders, supplier invoices, vendor confirmations

- HR: Employment contracts, payroll summaries, CPF documentation

- Operations: Inventory records, stock count sheets, lease agreements

Assign document responsibilities with internal deadlines that feed into the finance team's timeline ahead of fieldwork. Clear ownership means audit queries get answered quickly — not chased down under pressure.

Prioritize High-Risk Accounting Areas Flagged by ACRA

ACRA's FRSP Report 2024 identified the most common non-compliance areas during 2022–2024:

- Consolidation/equity accounting: 12 occurrences

- Impairment of assets: 9 occurrences

- Financial instruments: 9 occurrences

Companies with subsidiaries, complex asset structures, or financial instruments should prioritize these areas in pre-audit preparation:

- Review control assessments for consolidated entities

- Update impairment calculations with supportable cash flow projections and discount rates

- Ensure Expected Credit Loss (ECL) assessments under SFRS(I) 9 are complete and documented

- Verify fair value measurements use observable market inputs as required under SFRS(I) 13

ACRA's key recommendation: "Directors and management should ensure that their finance teams possess a thorough understanding of core accounting concepts and their practical application."

Frequently Asked Questions

When is the audit busy period in Singapore?

Singapore's audit busy season typically runs from January to April, driven by the high proportion of companies with December 31 financial year-ends. Statutory ACRA filing deadlines fall in the first half of the following year, compressing audit activity into Q1.

How early should I engage an auditor in Singapore?

Companies should engage their auditor at least 2–3 months before their financial year-end. December FYE companies should engage even earlier — by September or October — to secure availability before the January–April peak. March FYE companies should engage by November–December of the prior year.

How does my financial year-end affect when I experience audit peak pressure?

December 31 FYE companies face the highest pressure because they compete for auditor time during the busiest window. Companies with March FYEs face secondary pressure as their preparation overlaps with the December peak. June and September FYEs benefit from better audit capacity and scheduling flexibility outside the January–April rush.

What documents should be ready before the audit peak period?

Key documents to prepare include:

- Reconciled bank statements and confirmed trade receivables/payables

- Updated fixed asset register and complete payroll records with CPF filings

- Reconciled GST F5 returns for all periods

- Signed copies of major contracts, lease agreements, and financing arrangements

What penalties apply if my audit is late in Singapore?

Late ACRA annual return filing incurs S$300–S$600 in fees, with court prosecution carrying fines up to S$5,000 per charge. Late IRAS tax filing attracts composition amounts up to S$5,000 per offence; filing failure spanning 2+ years results in twice the tax assessed plus additional fines.

Can I change my financial year-end to avoid the audit peak period in Singapore?

Yes. Companies can change their FYE with ACRA's approval, though no change is permitted within 5 years of a prior change made after August 31, 2018, and extensions beyond 18 months require approval. Shifting away from December 31 can reduce peak-season pressure, but weigh tax planning and stakeholder reporting needs before deciding.