Introduction

Singapore companies face two distinct annual corporate tax filing obligations set by the Inland Revenue Authority of Singapore (IRAS): the Estimated Chargeable Income (ECI) within 3 months of financial year-end, and the Corporate Income Tax Return (Form C / C-S / C-S Lite) by 30 November in the Year of Assessment. Missing either deadline triggers penalties ranging from composition fines to court prosecution of directors.

Many businesses struggle with dual compliance requirements — especially newly incorporated startups in their first filing season, and foreign companies from the US, UK, and Australia with Singapore operations. In 2025, IRAS expects approximately 300,000 companies to file, including 37,000 new entities.

Directors bear personal legal responsibility for timely compliance. That makes understanding deadlines, tax rates, exemption schemes, and penalty frameworks a non-negotiable part of running a Singapore company.

This guide covers:

- Both ECI and Form C filing obligations with key 2025 dates by financial year-end

- Singapore's territorial tax system, current rates, and available exemptions

- The YA 2025 Corporate Income Tax (CIT) Rebate

- GST and ACRA filing requirements

- What happens after submission

Who this guide is written for:

- Directors and business owners of Singapore-incorporated companies

- Newly incorporated startups navigating their first Year of Assessment

- Foreign companies with Singapore operations needing to understand local compliance timelines

- US, UK, and Australian businesses managing cross-border tax obligations

TLDR: Singapore Corporate Tax Filing Deadlines 2025 at a Glance

- ECI must be filed within 3 months of your financial year-end — for FYE 31 Dec 2024, the deadline is 31 Mar 2025

- 30 November 2025 is the deadline for Form C / C-S / C-S Lite (YA 2025), filed via IRAS myTax Portal

- Singapore's corporate tax rate is 17%; effective rates are often as low as 4.25% in Year 1 after Start-Up Tax Exemption (SUTE) or Partial Tax Exemption (PTE)

- All Singapore-incorporated companies must file, including dormant and zero-revenue companies, unless IRAS grants a specific waiver

- Late filing triggers composition fines up to S$5,000 per offence and possible court summons

- Directors face personal penalties, including potential imprisonment, for non-compliance

How Singapore Corporate Tax Works: Key Terms to Know

Three terms define how Singapore's corporate tax system works — and getting them straight prevents costly filing errors:

| Term | What It Means |

|---|---|

| Financial Year (FY) | The 12-month accounting period (basis period) during which your company earns income |

| Year of Assessment (YA) | The calendar year IRAS taxes that income — typically the year after the FY ends |

| Financial Year-End (FYE) | The last day of your FY; determines when ECI and annual return deadlines fall |

Example: A company with FYE 31 December 2024 earned income during FY 2024. This income is assessed and taxed in YA 2025.

Who Must File

Under Singapore's Income Tax Act, all companies incorporated or tax-resident in Singapore must file corporate tax returns regardless of whether they generated revenue. This includes:

- Active trading companies

- Dormant companies (unless IRAS has granted a specific waiver)

- Companies that incurred losses

- Foreign companies carrying on trade or business in Singapore

Non-tax-resident companies are taxed only on Singapore-sourced income and cannot claim certain exemptions available to tax residents. Even companies qualifying for tax exemption schemes must file to claim the exemption.

Singapore's Territorial Tax System

Singapore taxes companies on income accrued in or derived from Singapore. Foreign-sourced income is generally taxable only when remitted to and received in Singapore, with one important exception: if that foreign income arises from a trade or business carried on in Singapore, it becomes taxable upon accrual regardless of remittance.

Section 13(8) exemption provides tax relief on three types of foreign-sourced income received by Singapore tax-resident companies:

- Foreign-sourced dividends

- Foreign branch profits

- Foreign-sourced service income

To claim this exemption, all three qualifying conditions must be satisfied:

- Income was subject to tax in the foreign jurisdiction

- The headline corporate tax rate in the foreign jurisdiction is at least 15%

- The Comptroller of Income Tax is satisfied the exemption is beneficial to the taxpayer

This exemption is available only to Singapore tax-resident companies — non-residents cannot claim it. For US, UK, and Australian companies with Singapore operations, this matters directly: all three jurisdictions exceed the 15% headline rate threshold, meaning foreign income remitted to Singapore from these countries may qualify for the exemption.

Singapore Corporate Tax Rates and Exemptions for YA 2025

Singapore's corporate income tax rate is a flat 17% of chargeable income. However, this is a ceiling, not the effective rate most companies pay — tax exemption schemes significantly reduce the burden for qualifying businesses.

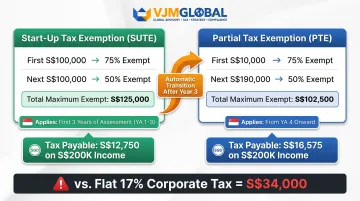

Partial Tax Exemption (PTE)

The Partial Tax Exemption is available to all qualifying companies not claiming SUTE:

| Chargeable Income Band | Exemption Rate | Maximum Exempt Amount |

|---|---|---|

| First S$10,000 | 75% | S$7,500 |

| Next S$190,000 | 50% | S$95,000 |

| Total maximum exempt | S$102,500 |

Example: A company with S$200,000 chargeable income under PTE:

- Exempt amount: S$7,500 + S$95,000 = S$102,500

- Taxable amount: S$200,000 - S$102,500 = S$97,500

- Tax payable: S$97,500 × 17% = S$16,575 (versus S$34,000 at flat 17%)

Start-Up Tax Exemption (SUTE)

Newly incorporated companies may qualify for a more generous scheme. SUTE offers a higher exemption ceiling, applying during the first three consecutive YAs:

| Chargeable Income Band | Exemption Rate | Maximum Exempt Amount |

|---|---|---|

| First S$100,000 | 75% | S$75,000 |

| Next S$100,000 | 50% | S$50,000 |

| Total maximum exempt | S$125,000 |

Eligibility conditions (all must be met):

- Incorporated in Singapore

- Tax-resident in Singapore for that YA

- No more than 20 shareholders throughout the basis period

- All shareholders are individuals, OR at least one individual holds 10% or more of issued ordinary shares

Excluded companies: Investment holding companies and property development companies cannot claim SUTE.

Worked example — S$200,000 chargeable income under SUTE:

- Exempt: (75% × S$100,000) + (50% × S$100,000) = S$125,000

- Taxable: S$200,000 - S$125,000 = S$75,000

- Tax payable: S$75,000 × 17% = S$12,750

- Tax saving versus flat 17%: S$21,250 (approximately 62.5% reduction)

SUTE applies for the first three consecutive YAs from incorporation — the clock starts from the first YA even if the company has no income. From the 4th YA onward, companies automatically transition to PTE.

YA 2025 CIT Rebate

The Singapore Government announced in Budget 2025 a Corporate Income Tax Rebate of 50% of corporate tax payable for YA 2025, with combined benefits (rebate plus cash grant) capped at S$40,000.

Key features:

- Active companies that employed at least one local employee in 2024 receive a minimum S$2,000 cash grant, even if not profitable

- IRAS computes the rebate automatically in the tax assessment — no separate application needed

- This is the second consecutive year the Government has provided a CIT rebate

Two Filing Obligations Every Singapore Company Must Meet

Obligation 1: Estimated Chargeable Income (ECI)

What is ECI? The Estimated Chargeable Income is a preliminary estimate of your company's taxable income for a financial year, calculated after deducting tax-allowable expenses and accounting for capital allowances and loss reliefs. IRAS uses it to raise a provisional tax assessment and determine GIRO instalment eligibility.

Critical: ECI is a separate obligation from the annual income tax return. Filing ECI does not substitute for filing Form C/C-S/C-S Lite.

Filing deadline: Within 3 months from the end of your financial year.

ECI filing exemption: Companies are exempt from filing ECI if both conditions are met:

- Annual revenue is S$5 million or below

- ECI is nil for the YA

Companies qualifying for exemption do not need to notify IRAS — they simply do not file. However, if a company misses the 3-month window, it forfeits the right to pay assessed taxes by instalments, resulting in full payment due within 1 month of the NOA.

GIRO instalment tiers:

| Filing Timing | Number of Instalments |

|---|---|

| Within 1 month of FYE (by the 26th) | 10 instalments |

| Within 2 months of FYE (by the 26th) | 8 instalments |

| Within 3 months of FYE (by the 26th) | 6 instalments |

| After 3 months from FYE | 0 instalments |

Filing early maximises instalment flexibility and eases cash flow management.

Once ECI is handled, every company must also satisfy its annual return obligation — a separate filing with its own deadline and form requirements.

Obligation 2: Corporate Income Tax Return (Form C / C-S / C-S Lite)

All companies must file an annual return by 30 November in the Year of Assessment. Three form types apply, determined by company size and complexity:

| Feature | Form C-S Lite | Form C-S | Form C |

|---|---|---|---|

| Revenue threshold | S$200,000 or below | S$5 million or below | All other companies |

| Number of fields | 6 essential fields | More than C-S Lite | Full return |

| Financial statements required? | No* | No* | Yes |

| Tax computation required? | No | No | Yes |

*Must be prepared and kept, but not submitted with the return.

To qualify for Form C-S, a company must meet all four conditions:

- Incorporated in Singapore

- Annual revenue S$5 million or below

- Income taxed only at the 17% corporate rate

- Not claiming carry-back of losses, group relief, investment allowance, or foreign tax credits

Companies that fall outside any one of these conditions must use Form C, regardless of revenue size.

Filing process via myTax Portal:

- Set up CorpPass access — ensure the user has the "Approver" role for "Corporate Tax (Filing and Applications)"; only Approvers can submit, not Preparers

- Finalise financial statements — audited if required under the Companies Act

- Complete tax computation — including allowable deductions and capital allowances

- Log in to mytax.iras.gov.sg — select "Corporate Tax" then "File ECI" or "File Form C-S/C"

- Submit — follow IRAS instructions and confirm submission

E-filing has been mandatory since YA 2020 — paper returns are no longer accepted.

Key Corporate Tax Filing Deadlines for Singapore in 2025

Singapore companies face multiple filing obligations across different government agencies — each with its own deadlines and consequences for non-compliance. Here's a breakdown of every key deadline for 2025.

ECI Deadlines by Financial Year-End

| Financial Year-End (FYE) | ECI Filing Deadline |

|---|---|

| 31 December 2024 | 31 March 2025 |

| 31 March 2025 | 30 June 2025 |

| 30 June 2025 | 30 September 2025 |

| 30 September 2025 | 31 December 2025 |

Rule: ECI is always due within 3 months of FYE. GIRO plan holders should file by the 26th of the relevant month to maximise instalment eligibility.

Corporate Income Tax Return Deadline

Fixed annual deadline: All companies must file Form C, C-S, or C-S Lite for YA 2025 by 30 November 2025 via IRAS myTax Portal. This deadline applies regardless of your FYE.

IRAS typically issues the Notice of Assessment (NOA) within 4–6 months of filing, and tax must be paid within 1 month of the NOA date.

GST Filing Deadlines for Singapore Companies

GST and corporate income tax are separate obligations governed by different legislation. GST applies only if your company's taxable turnover exceeds S$1 million in a 12-month period (or is expected to). The current GST rate is 9% (effective 1 January 2024).

GST quarterly filing schedule:

| Quarter Ending | Filing & Payment Due | GIRO Deduction Date |

|---|---|---|

| 31 March | 30 April | 15 May |

| 30 June | 31 July | 15 August |

| 30 September | 31 October | 15 November |

| 31 December | 31 January | 15 February |

Even "Nil" returns must be filed if your company is GST-registered.

ACRA Annual Return Deadlines

The Accounting and Corporate Regulatory Authority (ACRA) annual return is a separate obligation from IRAS tax filing. All Singapore companies must file an Annual Return with ACRA via BizFile+:

| Company Type | Deadline |

|---|---|

| Listed company | Within 5 months of FYE (6 months if share capital + overseas branch) |

| Non-listed company | Within 7 months of FYE (8 months if share capital + overseas branch) |

Penalty for late filing: Up to S$600. Filing with IRAS does not satisfy the ACRA obligation — both must be done separately.

Penalties for Late Filing and What Happens After You File

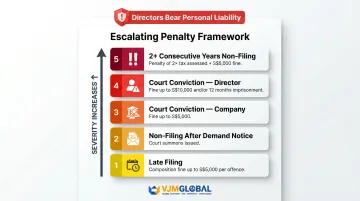

Late Filing Penalty Framework

IRAS enforces strict penalties for late or non-filing of corporate tax returns:

| Scenario | Consequence |

|---|---|

| Late filing (initial) | Composition fine up to S$5,000 per offence |

| Non-filing after demand notice | Court summons issued |

| Court conviction (company) | Fine up to S$5,000 per offence |

| Court conviction (director - Section 65B(3)) | Fine up to S$10,000 and/or up to 12 months imprisonment |

| Non-filing for 2+ consecutive years | Penalty of 2× the tax assessed plus fine up to S$5,000 |

| Failure to attend court summons | Warrant of arrest issued against director |

Directors bear personal legal responsibility for corporate tax compliance. Engaging a tax agent does not transfer this obligation. According to IRAS enforcement data, close to 4,500 companies were prosecuted for late or non-filing in a recent year, resulting in S$3.4 million in penalties collected.

If ECI is filed late (after 3 months from FYE), the company forfeits GIRO instalment eligibility and must pay the full tax liability within 1 month of the NOA.

What Happens After Filing

Notice of Assessment (NOA): IRAS reviews the tax return and issues a NOA specifying the company's tax liability. Tax must be paid within 1 month of the NOA date, even if the company plans to object to the assessment.

Accepted payment methods include:

- GIRO (recommended for automatic deduction)

- PayNow QR

- Internet banking

- AXS (credit card, S$20,000 limit)

Late payment penalties:

- 5% surcharge on unpaid tax if payment is not received by the due date

- Additional 1% per month after 60 days, capped at 12% additional penalty

If there is a significant discrepancy between the ECI and the final income declared in Form C/C-S, IRAS may request a written explanation.

Foreign companies — particularly those from the US, UK, and Australia — often face added complexity managing Singapore tax obligations alongside home-country requirements. Firms like VJM Global, with cross-border tax expertise spanning multiple jurisdictions including India and Singapore, can help multinationals navigate dual-compliance obligations and avoid costly filing errors.

Frequently Asked Questions

How are Singapore corporate tax filing deadlines structured?

Singapore companies have two key deadlines: ECI must be filed within 3 months of the financial year-end, and the Corporate Income Tax Return (Form C / C-S / C-S Lite) must be filed by 30 November in the Year of Assessment. All filings must be completed electronically via IRAS myTax Portal.

What is the corporate tax filing deadline in Singapore for 2025?

For YA 2025, Form C / C-S / C-S Lite must be filed by 30 November 2025. ECI deadlines vary by FYE — for companies with FYE 31 December 2024, ECI is due by 31 March 2025. Refer to the deadline calendar in this guide for your specific FYE.

How do I file a corporate tax return in Singapore?

Your company's CorpPass account holder must have the "Approver" role to file. Log in to IRAS myTax Portal, select "Corporate Tax," then choose "File ECI" or "File Form C-S/C" depending on what's due.

How does corporate tax work in Singapore?

Singapore taxes companies at a flat 17% on income accrued in or derived from Singapore (territorial basis). Income earned in a financial year is assessed in the following Year of Assessment. Tax exemptions — including SUTE for new startups and PTE for qualifying companies — reduce the effective rate significantly for most businesses.

What is the GST filing deadline for corporations in Singapore?

GST is a separate obligation from corporate income tax. GST-registered companies file quarterly returns due one month after each quarter-end — for example, the quarter ending 31 March is due by 30 April. The current GST rate is 9%, and registration is mandatory once taxable turnover exceeds S$1 million over any 12-month period.