This applies to a wide range of people: Australian startups testing a new market, established SMEs building international footprint, and Australian-based founders of non-Australian origin looking to establish in a familiar English-speaking economy.

What this guide covers: business structure decisions, Companies House registration, HMRC tax setup, banking, employment obligations, cross-border tax considerations, and visa implications for relocating founders. The goal is to give you a clear picture of the full process before you begin — not halfway through.

Key Takeaways

- Australians can legally own and operate a UK company without being a UK resident — most steps are completed remotely

- A UK private limited company (subsidiary) is the preferred structure for most Australian founders

- Registration with Companies House takes 24–48 hours online; full operational readiness takes 2–6 weeks

- Cross-border tax decisions — IP placement, transfer pricing, the AU-UK Double Tax Agreement — must be addressed before registration

- Physical relocation triggers visa requirements and an Australian CGT liability on assets deemed disposed at departure

Why Australian Businesses Are Expanding to the UK Right Now

The Australia-UK relationship offers one of the most accessible paths to international expansion available to any country. Shared language, common law legal systems, compatible business culture, and a long bilateral trade history mean Australian businesses aren't starting from scratch when they cross into the UK market.

The AU-UK Free Trade Agreement, which entered into force on 31 May 2023, has made the current moment particularly relevant. Key benefits include:

- Tariff elimination on more than 99% of Australian goods by value entering the UK duty-free

- Non-discrimination rules ensuring UK markets can't favour domestic service suppliers over Australian ones

- Professional qualifications — a framework for faster recognition across key sectors, with Australian lawyers guaranteed the right to provide legal advisory services in the UK

- Services access improvements across professional services, IT, and financial services

The scale of existing commitment underscores the opportunity. According to DFAT, Australian foreign direct investment in the UK reached AUD $210 billion in 2024 — up 11.5% on the previous year.

Two-way goods and services trade hit AUD $35.9 billion that same year, with the UK ranking as Australia's second-largest destination for total investment stock abroad. For businesses weighing whether to move, those numbers represent a well-worn path worth following.

What You Need to Know Before You Start

Starting a UK business from Australia is genuinely achievable. Company registration takes less than 48 hours — but cross-border banking, tax compliance, and structural decisions made before you register will define how smoothly the business operates from day one.

Realistic Timeline

| Stage | Approximate Timeframe |

|---|---|

| Companies House registration (online) | 24–48 hours |

| Corporation Tax registration with HMRC | 2–3 weeks (activation code takes up to 21 days for overseas applicants) |

| VAT registration | Variable — HMRC sends confirmation by post; check gov.uk for expected response times |

| UK business banking (digital platforms) | 1–2 weeks |

| Full operational readiness | 2–6 weeks depending on complexity |

Cost Categories to Plan For

- Companies House registration fee: £100 (online)

- Registered UK address: Required by law; mail-forwarding services typically cost £50–£200/year

- Professional advisory fees: Variable depending on complexity of cross-border structure

- Ongoing annual compliance: Confirmation statement filing, annual accounts, accountancy fees

Physical Presence: What's Required vs. What's Beneficial

You don't need to be in the UK to own or run a UK company. Certain activities do benefit from in-market presence — particularly hiring local staff, building client relationships, and accessing some funding programmes. Remote ownership is fully legal; it's a practical question, not a legal one.

Decisions That Are Hardest to Reverse

Three decisions need to be made before registration:

- IP ownership — should intellectual property sit in the Australian parent or the UK subsidiary?

- Business structure — branch versus subsidiary (more on this below)

- Intercompany arrangements — any transactions between the Australian and UK entities need to be structured and documented from day one

Getting these wrong creates two problems: ongoing compliance complexity and restructuring costs that far exceed the advisory fees required to set them up correctly from the start.

How to Set Up Your Business in the UK from Australia — Step by Step

Most steps can be completed remotely. The order matters: getting structure and tax registration right before opening bank accounts or hiring prevents rework.

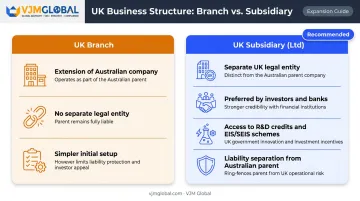

Step 1: Choose Your Business Structure

Two options exist for Australian businesses entering the UK:

UK Subsidiary (Private Limited Company)

- Separate legal entity incorporated in the UK, wholly owned by the Australian parent

- Preferred by most Australian businesses for liability separation, easier profit repatriation, and access to UK-specific incentives

- Required to access UK R&D tax credits, SEIS/EIS investor schemes, and most government grants

UK Branch of the Australian Company

- Not a separate legal entity; an extension of the Australian company

- Simpler initial setup, but complicates liability, tax treatment, and investor relationships

- UK customers, banks, and investors generally prefer dealing with a locally incorporated entity

Most Australian startups and SMEs choose the subsidiary route. Three practical reasons make this the default choice: UK investors expect a local entity, UK banks are more cooperative with locally incorporated companies, and accessing UK incentive schemes almost always requires incorporation.

Step 2: Register with Companies House

Companies House is the UK equivalent of ASIC. Every UK company must register before trading. What you'll need:

- Company name

- Director details (at least one director aged 16+; does not need to be a UK resident)

- A registered UK address — legally required, even if the business operates entirely remotely

- Articles of association

Registration is completed online and typically takes 24–48 hours. Mail-forwarding services provide compliant registered addresses for businesses without physical premises.

Ongoing Companies House obligations (non-negotiable):

- Annual accounts filing

- Confirmation statement (annually)

- Notifying Companies House of any director or shareholder changes

Failure to file on time triggers automatic penalties and, if unresolved, company strike-off.

Step 3: Register with HMRC for Tax

HMRC is the UK equivalent of the ATO. Three registrations to understand:

| Registration | When Required | Key Deadline |

|---|---|---|

| Corporation Tax | From the day you start trading | Register within 3 months of trading start |

| VAT | Once UK taxable turnover exceeds £90,000 (from 1 April 2024) | Within 30 days of month-end when threshold is crossed |

| PAYE | Before paying your first UK employee | Before first payroll run |

Corporation Tax activation codes from HMRC take up to 21 days if you're overseas-based, so register early. VAT voluntary registration below £90,000 is worth considering if your UK suppliers are VAT-registered.

Getting these registrations sequenced correctly from the start avoids costly corrections later. A cross-border adviser familiar with both HMRC and ATO obligations is worth engaging at this stage.

Step 4: Open a UK Business Bank Account

Traditional UK bank account opening for foreign-incorporated companies is slow and often requires a registered address, a resident director, and in-person verification — none of which may apply in the early stages.

Practical approach:

- Start with digital platforms — Airwallex or Wise Business support multi-currency accounts, local UK account details (sort code and account number), and remote setup

- Pursue a traditional UK bank account later — once physical presence is established, some capital raising requirements, supplier relationships, or government programmes may require a traditional account

Step 5: UK Employment Obligations (If Hiring Locally)

If you're hiring UK employees, three obligations apply immediately:

- PAYE — income tax withheld through payroll and reported to HMRC on or before each payday

- National Insurance Contributions (NICs): the UK equivalent of payroll tax. Class 1 contributions apply to employees earning more than £242 per week from a single job, deducted from wages

- Workplace pension auto-enrolment — employees aged 22 to State Pension age earning at least £10,000 per year must be enrolled automatically unless they opt out

UK employment law around contracts, leave entitlements, and termination differs meaningfully from Australian law. Get local HR or employment legal advice before making your first UK hire.

Cross-Border Tax, IP, and Ongoing Compliance

The AU-UK Double Tax Agreement

Australia and the UK have had a Double Taxation Convention in force since 17 December 2003. In plain terms: income isn't taxed twice. If a UK subsidiary pays UK corporation tax on its profits, the Australian parent can typically claim an offset against Australian tax on the same income.

Understanding how this works before intercompany transactions begin matters. The treaty affects how dividends, interest, royalties, and service fees flow between the two entities — and structuring those flows correctly from day one avoids costly restructuring later.

Transfer Pricing

The Double Tax Agreement covers how profits are allocated between countries — but it doesn't govern how the two related entities price transactions with each other. That's where transfer pricing rules apply.

When the Australian parent and UK subsidiary transact, both the ATO and HMRC require those transactions to be priced at arm's length: the same price an unrelated party would pay. Common intercompany transactions that trigger this obligation include:

- Shared services arrangements

- IP licensing between parent and subsidiary

- Intercompany loans

Documentation needs to be in place from the start. Reconstructing transfer pricing records retrospectively is far more difficult and expensive than maintaining them correctly from the beginning. This is a common area where Australian businesses underestimate the compliance burden until it becomes a problem.

IP Ownership: Decide Before You Register

Before setting up the UK entity, decide where intellectual property sits:

- IP in the Australian parent: UK subsidiary licenses it under a formal licensing arrangement — generates a royalty flow that needs arm's-length pricing

- IP in the UK subsidiary: May be appropriate if primary commercialisation occurs in the UK, but creates complexity if the IP was originally developed in Australia

Getting this wrong creates both tax exposure and structural complexity. For example, IP developed in Australia but commercially exploited in the UK without a formal licensing arrangement leaves the arrangement open to challenge by both tax authorities. This decision requires legal and tax advice before registration, not after.

Visa and Personal Tax Considerations for Relocating Founders

Visa Options

No visa is required to own a UK company while remaining in Australia. However, if a founder or team member plans to live or work in the UK for more than six months, a visa is required. The most relevant options for Australian founders are:

- Innovator Founder visa — for founders with an innovative, viable, and scalable business idea, endorsed by an approved body

- Global Talent visa — for leaders or potential leaders in digital technology, arts, sciences, humanities, or engineering

- Skilled Worker visa — for working in a specific skilled role with a licensed UK employer

Eligibility criteria and application requirements change periodically — check the UK government's official immigration pages for current rules before making any decisions.

Australian Capital Gains Tax on Departure

For relocating founders, Australian CGT on departure is the most frequently overlooked financial risk. When an individual ceases to be an Australian tax resident, the ATO treats them as having disposed of their CGT assets at market value on the departure date. This includes shares in a startup or operating business. It's a deemed disposal — the shares don't need to be sold for a tax liability to arise.

Key points:

- The deemed disposal does not apply to assets classified as taxable Australian property

- Individuals can elect to disregard the capital gain or loss on departure; if they do, the asset is treated as taxable Australian property until a later CGT event occurs or residency resumes

- The timing of the move, the share structure, and the election choice all affect the outcome materially

Get professional tax advice before departing Australia. The liability can reach six figures for founders with appreciated equity, and the options narrow considerably once residency changes.

Frequently Asked Questions

Can Australians start a business in the UK?

Yes. Australians can start and own a UK business without being a UK resident or citizen. The most common route is registering a private limited company (Ltd) with Companies House, which can be done entirely online from Australia.

Do I need a UK director to register a company in the UK?

A local UK director is not legally required by Companies House — directors don't need to live in the UK. However, having one can simplify banking and add credibility with UK customers and investors..

What is the difference between a UK branch and a UK subsidiary for Australian businesses?

A branch is an extension of the Australian company (not a separate legal entity), while a subsidiary is a separately incorporated UK company. Most Australian businesses choose the subsidiary route for liability protection, easier banking, and access to UK investor schemes.

How long does it take to register a company in the UK from Australia?

Online registration with Companies House typically takes 24–48 hours. Full operational readiness — including HMRC tax registration, banking setup, and a registered address — generally takes 2–6 weeks.

What taxes does an Australian-owned UK company need to pay?

UK corporation tax on UK profits, VAT once turnover exceeds £90,000, and employer NICs if staff are hired. The AU-UK Double Tax Agreement prevents the same income from being taxed in both countries.

Do I need a visa to run a UK business from Australia without relocating?

No visa is required to own a UK company while remaining in Australia. A visa is only needed if the founder or employees plan to physically live or work in the UK for more than six months.