Introduction

US state tax compliance means fifty separate obligations — each with its own rules, rates, forms, and deadlines. A business can handle federal taxes perfectly and still face penalties or audit exposure. Missing a single state registration, or crossing an economic nexus threshold mid-year without catching it, is enough.

The businesses most at risk are often the ones growing fastest: companies hiring remote workers in new states, selling across state lines, storing inventory with third-party fulfillment centers, or expanding operations into new markets. Any one of these moves can trigger a filing obligation in a state where the business has never had a presence.

Q1 2026 e-commerce sales hit $326.7 billion — representing 16.9% of all US retail. Meanwhile, BLS data shows 27.5% of US establishments had employees teleworking some or all of the time in 2022. For businesses operating across state lines, these trends translate directly into more nexus triggers, more registration requirements, and more returns to file.

This guide covers what state tax compliance involves, which taxes matter most, how nexus works in practice, and a checklist businesses can use to assess and manage their obligations across states.

Key Takeaways

- Each of the 50 states independently administers its own tax laws — there is no unified state tax system.

- Economic nexus (triggered by sales volume, not physical presence) now applies in most states following the 2018 Wayfair decision.

- Remote employees automatically create multi-state payroll obligations in the states where they work.

- Non-compliance puts funding eligibility, M&A due diligence, and your right to operate in a state at risk.

- Voluntary Disclosure Agreements (VDAs) offer a structured path to resolve prior exposure before an audit.

What State Tax Compliance Involves — and Why It Matters

State tax compliance is the ongoing process of meeting all tax obligations imposed by state and local governments — registering in each applicable state, filing returns on time, collecting and remitting taxes correctly, and maintaining adequate records. It sits entirely separate from federal tax compliance, which is administered by the IRS.

Each state's Department of Revenue (or equivalent authority) independently sets its own tax laws. A business operating in five states must satisfy five different sets of requirements simultaneously. The Federation of Tax Administrators serves all 50 state tax agencies plus DC, Philadelphia, and New York City — a structure that reflects just how fragmented state tax administration is.

The Consequences Go Beyond Penalties

Most businesses think of non-compliance primarily in terms of fines. The actual exposure is broader:

- Late filing penalties: New York imposes 5% of tax due per month, up to 25%; Florida can trigger a 10% penalty for late payment

- Interest charges accrue from the original due date until payment is made — with no cap in most states

- Loss of good standing: California can suspend or forfeit a business entity for unmet tax requirements; Texas ties franchise tax account status to a business's right to transact in the state

- Unresolved state and local tax liabilities are a recognized deal risk in acquisitions, per a 2025 Journal of Accountancy analysis

- Audit exposure: Gaps in filing history or operating without registration are common triggers for state audit notices

Key State Taxes Every Business Must Know

State Income Tax

As of 2026, 41 states tax wage and salary income, while eight states — Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, and Wyoming — have no individual income tax (Washington taxes only capital gains). Separately, 44 states levy a corporate income tax.

Corporations operating in multiple states must apportion income across those states using state-specific formulas. As of 2026, 38 states and DC use a single-sales-factor formula; six states still use three-factor apportionment. Getting apportionment wrong is one of the most common multistate income tax errors — so confirming which formula each state requires is a necessary first step.

Sales and Use Tax

Businesses selling taxable goods or services must collect sales tax from customers and remit it to each applicable state. What counts as taxable varies significantly:

- Pennsylvania: Canned software, digital goods, and remotely accessed software are taxable

- Washington: Digital products and remote access software are subject to retail sales or use tax

- California: Electronically delivered data products are generally not taxable when no tangible property transfers

- Oregon: No general sales or use tax at all

Use tax applies when taxable goods are purchased tax-free but consumed in the state — a common gap for businesses buying equipment or supplies across state lines.

Payroll Taxes

Once a business employs workers in a state — including remote employees working from home — it must register for:

- State income tax withholding

- State unemployment insurance (SUTA)

- Disability insurance (required in select states)

Remote hires are the most commonly overlooked trigger for new payroll obligations. A single employee working from a new state creates registration requirements in that state, regardless of where the employer is headquartered.

Franchise and Business Privilege Taxes

Some states charge a tax simply for the right to operate there, independent of profitability. Common examples include:

- Texas: Franchise tax calculated on taxable margin

- Delaware: Annual franchise tax due March 1

- Alabama: Business privilege tax assessed regardless of revenue

These taxes apply even in unprofitable years, which catches many businesses off guard during early-stage operations or economic downturns.

Understanding Tax Nexus: When Are You Obligated to File?

Nexus is the legal connection between a business and a state that creates a tax obligation. Without nexus, a business has no obligation to register or file in that state. Two categories apply:

- Physical nexus: Offices, employees, inventory, equipment, or other property located in the state

- Economic nexus: Crossing a state's sales volume or transaction threshold without any physical presence

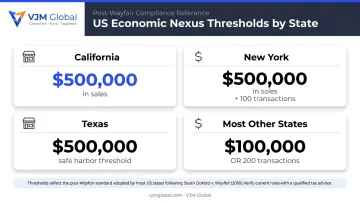

Economic Nexus After Wayfair

The 2018 South Dakota v. Wayfair Supreme Court decision eliminated the physical presence requirement for sales tax collection. States can now require remote sellers to collect and remit sales tax based purely on sales volume. Most states use a threshold of $100,000 in annual sales or 200 transactions.

These thresholds differ by state — here's how the major ones break down:

| State | Economic Nexus Threshold |

|---|---|

| California | $500,000 in annual sales |

| New York | $500,000 in sales + 100+ transactions |

| Texas | $500,000 safe harbor (below = no permit required) |

| Most other states | $100,000 in sales OR 200 transactions |

Nexus Triggers Businesses Often Miss

Physical presence isn't just an office. These activities commonly create nexus without businesses realizing it:

- Storing inventory with a third-party logistics provider or Amazon FBA warehouse

- A remote employee working from the state, even part-time

- Attending trade shows or providing on-site services in the state

- Working with in-state affiliates, resellers, or referral partners

- Having equipment or property temporarily located in the state

State Tax Compliance Checklist

Use this checklist annually, and revisit it any time your business hires in a new state, crosses a new sales threshold, or begins storing inventory in a new location. It covers three core areas: nexus and registration, filing obligations, and record-keeping.

Assess Nexus and Registration Requirements

- Conduct a nexus review for every state where you sell, employ workers, store inventory, or use third-party logistics providers

- Document which states require registration based on physical presence, economic nexus thresholds, or affiliate relationships

- Register with the state's Department of Revenue before collecting sales tax or running payroll in that state

- Check if the state participates in the Streamlined Sales Tax (SST) program — 24 states participate, and registration is free through the SSTRS system

Understand and Meet Filing Obligations

- Identify filing frequency for each state: sales tax returns may be due monthly, quarterly, or annually depending on volume

- Confirm income tax return deadlines: most align with the federal April 15 deadline for C corporations; pass-through entities (partnerships and S corporations) typically have a March 15 deadline

- Calculate income apportionment if operating in multiple states — use the correct formula (single-factor vs. three-factor) for each state

- If selling to wholesalers or tax-exempt buyers, collect and retain valid exemption or resale certificates — missing documentation during an audit results in assessed tax liability

Maintain Records and Respond to Notices

- Keep organized records of all filed returns, payment confirmations, exemption certificates, and correspondence with state authorities

- Retain records for a minimum of four years — Washington and Texas both have four-year assessment statutes of limitations; some states extend this further

- Respond to all state tax notices promptly; most carry short deadlines and escalate if ignored

- Follow each notice through to confirmed resolution and keep written confirmation on file

Common State Tax Compliance Mistakes to Avoid

Failing to Recognize New Nexus Triggers

Most businesses don't discover a state tax obligation until an audit notice arrives. Common triggers that go unnoticed include:

- A single remote hire in a new state

- Inventory stored with a fulfillment center across state lines

- Sales crossing an economic nexus threshold mid-year with no monitoring in place

The Multistate Tax Commission's National Nexus Program data from its voluntary disclosure initiative recorded 3,087 executed agreements and over $18.6 million in collections in FY 2018 alone — a clear indicator of how widespread unfiled obligations are.

Missing Filing Deadlines or Filing in the Wrong Frequency

States assign filing frequencies based on tax volume. A business that grows quickly may be automatically reassigned to a more frequent schedule without being notified. Missing the new frequency results in late penalties — even if the business filed on time under its previous schedule.

Minnesota ties filing frequency to average tax reported. Florida imposes a 10% penalty for late filing or payment. Neither state automatically waives penalties due to frequency confusion.

Treating All States the Same

A compliance approach built around one state's rules will break in another. Some consistent errors:

- Assuming digital products are exempt everywhere (they're taxable in Pennsylvania and Washington; generally exempt in California when electronically delivered)

- Applying one state's filing deadline to another

- Using a three-factor apportionment formula in a state that requires single-factor (or vice versa)

These mistakes share a common root: treating compliance as a one-size-fits-all process. The sections below outline what a state-by-state review should actually cover.

How to Stay Compliant Across States: Practical Tips

Staying current across multiple states takes more than good intentions — it takes systems. Here are four practical areas to lock down.

Build a Centralized Compliance Calendar

Capture all state filing deadlines, estimated payment due dates, registration renewals, and nexus review checkpoints in one place. Assign each obligation to a specific person and update the calendar after every filing cycle. Without clear ownership, deadlines slip.

Use Nexus Monitoring and Tax Automation Tools

Software platforms track sales and transaction counts by state, flag when you're approaching a threshold, calculate correct rates at checkout, and automate return filing. Two commonly used platforms:

- Avalara — an official SST Certified Service Provider with broad multi-state coverage

- TaxJar — acquired by Stripe for its cloud-based automated sales tax capabilities, well-suited for e-commerce businesses

Bring in Multi-State Specialists

If you operate in more than two or three states, or are scaling rapidly, generalist tax support often isn't enough. VJM Global's team of CPAs and US-compliant professionals handles multi-state compliance end to end — registration, return preparation, apportionment, and notice resolution — adjusting as your footprint grows.

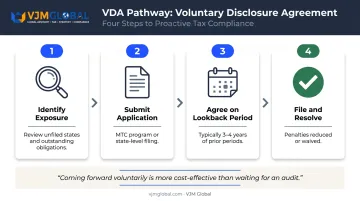

Explore Voluntary Disclosure Agreements for Prior Non-Compliance

The Multistate Tax Commission's Voluntary Disclosure Program coordinates VDAs across multiple states simultaneously using a uniform procedure. State-level programs typically limit the lookback period — Georgia uses 36 months for sales/use and withholding tax; Washington uses four years plus the current year — and reduce or waive penalties in exchange for coming forward voluntarily. Coming forward proactively is almost always more cost-effective than waiting for an audit.

Frequently Asked Questions

What is tax compliance and what does it include?

Tax compliance is the process of meeting all required tax obligations — including registering with relevant authorities, filing returns on time, paying taxes owed accurately, and maintaining supporting records. It applies at the federal, state, and local level, with each layer governed by separate rules and administered by separate agencies.

Who regulates taxes in the United States?

The IRS administers federal taxes. Each state independently runs its own Department of Revenue or equivalent authority that sets and enforces state and local tax laws. These agencies operate separately from the IRS, meaning a business must satisfy both federal and state obligations simultaneously.

What happens if a business fails to comply with state tax requirements?

Consequences include interest charges on unpaid taxes, late filing and late payment penalties (up to 25% in some states), audit exposure, and potential loss of good standing — restricting the business's legal right to operate or enter contracts in that state.

How does economic nexus affect multi-state tax obligations?

Since the 2018 Wayfair decision, businesses can owe sales tax in a state based purely on sales volume, even without a physical presence there. Most states use $100,000 in annual sales or 200 transactions as the trigger, so tracking revenue and transaction counts by state is essential.

Do all US states have the same tax filing requirements?

No. Each state sets its own rules on which taxes apply, filing frequency, deadlines, and thresholds. Nine states have no individual income tax, Oregon has no sales tax, and digital product taxability varies widely — compliance must be researched state by state.

When should a business register for state taxes in a new state?

A business should register before it starts collecting sales tax, running payroll, or conducting ongoing business activity in a state. Collecting tax without proper registration creates legal complications, and retroactive registration typically still triggers back-filing requirements.