Introduction

Many foreign businesses and individuals operating in Singapore underestimate the gravity of missing tax deadlines — until they face enforcement action. The Inland Revenue Authority of Singapore (IRAS) enforces strict filing obligations with a penalty structure that escalates fast: from monetary fines to criminal prosecution.

Whether you're managing individual income tax or corporate compliance, the consequences of late filing can include:

- Estimated tax assessments issued by IRAS

- Composition amounts up to S$5,000

- Bank account restrictions

- Criminal prosecution and imprisonment

This guide covers the key filing deadlines for individual and corporate income tax in Singapore, the exact penalty structure for late filing and late payment, how IRAS escalates enforcement against persistent non-filers, and practical steps to protect yourself from costly missteps.

Key Takeaways

- Late individual income tax filing triggers composition amounts up to S$5,000 and potential court prosecution with matching fines

- Corporate non-filing draws estimated Notices of Assessment and S$5,000 composition amounts; directors face personal fines up to S$10,000 or imprisonment

- Late payment of assessed tax attracts an initial 5% penalty, followed by 1% per month for up to 12 months (maximum total: 17%)

- Continued non-compliance can lead to bank account freezes, Travel Restriction Orders barring departure, and court summons

- Voluntary disclosure programmes reduce penalties to 5% for taxpayers who self-report errors before IRAS detects them

Key Tax Filing Deadlines in Singapore

Individual Income Tax Deadlines

Singapore taxpayers must file their individual income tax returns by 18 April each year, regardless of whether they submit via paper or e-filing through the myTax Portal. This unified deadline applies to all taxpayers required to file Form B1, B, P, or M.

Taxpayers who receive a No-Filing Service (NFS) notification from IRAS are generally exempt — IRAS auto-assesses their tax using employer and third-party data. You must still file by the deadline if you need to:

- Claim additional reliefs not captured automatically

- Correct pre-filled income details

- Report income sources IRAS doesn't already have on record

Corporate Income Tax Deadlines

Companies operating in Singapore face two separate corporate tax filing obligations:

- Estimated Chargeable Income (ECI): Due within 3 months of the financial year-end. This preliminary estimate helps IRAS assess tax liability before the company submits the detailed return.

- Form C-S / Form C-S (Lite) / Form C: The comprehensive corporate tax return is due by 30 November each year. Missing this deadline triggers immediate enforcement actions, including composition offers (monetary penalty settlements) and court summons.

GST Filing Deadlines

Beyond income tax, GST-registered businesses face their own filing clock. Form F5 must be submitted within one month of the end of each accounting period (typically quarterly). GST penalties run on a separate track from income tax penalties — but missing both deadlines in the same period draws enforcement attention from multiple IRAS channels simultaneously.

| Tax Type | Filing Deadline | Applies To |

|---|---|---|

| Individual Income Tax | 18 April | All individuals required to file |

| Corporate ECI | Within 3 months of FY-end | All companies unless exempted |

| Corporate Tax Return (Form C-S/C) | 30 November | All companies |

| GST (Form F5) | Within 1 month of quarter-end | GST-registered businesses |

Penalties for Late Filing of Income Tax in Singapore

Late income tax filing is a punishable offence under Part 20 of Singapore's Income Tax Act 1947. Miss the deadline and IRAS moves fast — from estimated assessments to court summons to criminal prosecution, each step escalates if you don't act.

Individual Income Tax: Late Filing Penalties

When you miss the 18 April deadline, IRAS immediately gains the authority to issue an estimated Notice of Assessment (NOA) based on prior year income or other available information. This estimate often assumes an income increase from the previous year, meaning you may face a higher tax bill than your actual liability.

Critical requirement: You must pay the estimated tax within 1 month of the NOA date, even if you disagree with the assessment. Failure to pay leads to separate late payment penalties on top of late filing consequences.

Composition Offer: Instead of immediate prosecution, IRAS typically offers a composition amount—an out-of-court settlement—of up to S$5,000 per offence. The exact amount depends on your past compliance record. To avoid court action, you must:

- Pay the full composition amount by the specified deadline (GIRO is not accepted)

- File the outstanding tax return and all required documents

Court Summons: If you ignore the composition offer or fail to file the return, IRAS issues a Notice to Attend Court. Conviction can result in:

- Fine of up to S$5,000 per offence

- For taxpayers who fail to file for 2 or more years: a penalty of twice the tax assessed plus a fine of up to S$5,000

- Imprisonment of up to 6 months if you fail to pay court-ordered penalties

Corporate Income Tax: Late Filing Penalties

Companies face the same escalation path as individuals — but with one critical addition: IRAS can hold directors personally liable if the company continues to ignore its filing obligations.

Estimated NOA: IRAS issues an estimated assessment that may inflate the company's income based on industry benchmarks or prior year data. The company must pay this amount within 1 month, regardless of whether it disputes the assessment.

Composition Amount: Companies face composition amounts up to S$5,000 per offence, depending on compliance history. Filing the outstanding Form C-S or Form C after payment prompts a reassessment and potential refund of any overpaid tax.

Director Liability Under Section 65B(3): If the company continues to ignore filing obligations, IRAS can issue a notice to directors requiring them to provide company information. Directors who fail to comply face:

- Personal fines of up to S$10,000 per offence

- Imprisonment of up to 12 months

- Warrant of arrest for failure to attend court

For foreign-owned companies, the consequences extend further. Repeated non-compliance can damage banking relationships, block access to government grants, and affect your standing with regulators in Singapore and your home jurisdiction.

Penalties for Late Payment of Income Tax in Singapore

Filing and payment penalties are entirely separate. Even if you file your return on time, late payment after the NOA is issued triggers a distinct penalty structure.

The 5% Initial Penalty

If full payment is not received within 1 month of the NOA date and you are not on an approved GIRO instalment plan, IRAS automatically imposes a 5% penalty on the unpaid tax amount.

Example: If your NOA shows S$20,000 in tax due and you miss the payment deadline, the 5% penalty adds S$1,000 to your liability, bringing the total to S$21,000.

The Escalating 1% Monthly Penalty

If tax remains unpaid 60 days after the initial 5% penalty notice, IRAS imposes an additional 1% penalty for each completed month the tax remains outstanding, up to a maximum of 12 months.

Maximum combined penalty: 5% + 12% = 17% of the unpaid tax

Example:

- Original tax due: S$20,000

- Initial 5% penalty: S$1,000

- After 6 months unpaid: additional 6% = S$1,200

- Total owed after 6 months: S$22,200

Recovery Actions: Agent Appointments and Travel Restrictions

Once penalties have escalated without resolution, IRAS can initiate serious recovery measures:

Agent Appointments: IRAS appoints third parties who owe you money—banks, employers, tenants, lawyers handling property sales—to deduct and remit your overdue tax directly. When your bank is appointed as agent, you may lose access to your accounts until you pay in full.

Travel Restriction Order (TRO): For individuals, IRAS can issue a TRO preventing you from leaving Singapore until tax is paid in full. The IRAS late payment page explicitly warns that "overstaying in Singapore is an offence"—creating compounded legal risk for foreign nationals whose visas may expire while they're barred from departing.

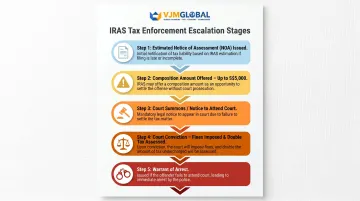

How IRAS Escalates Enforcement for Persistent Non-Compliance

The Full Enforcement Escalation Sequence

IRAS follows a deliberate escalation path from administrative action to criminal prosecution:

- Estimated NOA issued → taxpayer must pay within 1 month

- Composition amount offered → up to S$5,000, payment and filing required to avoid court

- Notice to Attend Court / Summons issued → if composition unpaid or return not filed

- Court conviction → fines up to S$5,000 per offence; twice the tax assessed for 2+ years non-filing

- Warrant of arrest → for failure to attend court or pay court-ordered penalties

Each step compounds financial and legal consequences. Paying the composition or even the court-ordered penalty does not waive the filing obligation. You must still submit the outstanding return or face further prosecution.

What Happens When You Object to an Estimated NOA

Many taxpayers mistakenly believe that filing an objection suspends their payment obligation. It does not. IRAS requires you to pay the full estimated amount shown on the NOA even if you intend to dispute it. Only after you:

- Pay the estimated tax in full

- File the complete tax return with supporting documents

- Submit a formal objection

...will IRAS review and potentially revise the assessment downward. If the assessment is reduced, excess payment is refunded. Late payment penalties still apply to any amount that remained unpaid beyond the original due date.

Implications for Foreign Individuals and Companies

Foreign individuals subject to a TRO face a dual legal trap: they cannot leave Singapore until tax is paid, but overstaying beyond their visa expiry is a separate immigration offence carrying penalties of up to S$6,000 in fines, six months' imprisonment, caning, deportation, and re-entry bans.

Foreign-owned companies face consequences that extend well beyond Singapore's borders. Persistent non-compliance triggers:

- Banking disruptions when IRAS appoints banks as agents to freeze accounts

- Blocked access to future government grants and incentive schemes

- Reputational damage with investors and partners across Asia-Pacific who treat Singapore tax failures as a signal of broader governance risk

Voluntary Disclosure Programme: A Mitigation Option

IRAS operates a Voluntary Disclosure Programme (VDP) that offers reduced penalties for taxpayers who correct errors before IRAS detects them:

- Within 1 year of the statutory filing deadline: No penalty

- After the 1-year grace period: Reduced penalty of 5% of the undercharged amount per year (versus standard enforcement penalties)

To qualify, your disclosure must be accurate, complete, and voluntary — meaning you must come forward before receiving any IRAS query or audit notification. If you've missed a filing or underreported income, acting before IRAS makes contact is the single most effective way to reduce your penalty exposure.

How to Avoid Late Income Tax Filing Penalties in Singapore

Maintain Year-Round Compliance Discipline

Prevention requires systematic record-keeping and proactive deadline management:

- Organise financial records continuously: Don't wait until filing season to gather receipts, invoices, and income statements

- Set multiple calendar reminders: 18 April for individuals; 3 months post-FY-end for corporate ECI; 30 November for Form C-S/C

- Monitor myTax Portal regularly: IRAS sends critical reminders and notices electronically; missed notifications don't excuse late filing

Engage Qualified Tax Advisory for Cross-Border Operations

Foreign businesses and individuals new to Singapore's tax system face a higher risk of missing deadlines due to unfamiliarity with local obligations and terminology. Multinational companies managing obligations across Asia-Pacific jurisdictions — India, Singapore, and Australia — benefit from advisors who know each market's specific enforcement approach.

VJM Global works with international businesses to coordinate tax filing obligations across jurisdictions, helping prevent the compliance gaps that trigger penalties in markets like Singapore.

Apply for GIRO Instalment Plans Early

If you anticipate difficulty paying the full assessed tax in one payment, Singapore offers interest-free instalment plans:

- Individual taxpayers: Up to 12 monthly instalments via GIRO

- Corporate taxpayers: Up to 10 monthly instalments

Critical timing requirement: Your GIRO application must be approved before the payment due date (1 month from NOA date) to avoid the 5% late payment penalty being triggered. Apply as soon as you receive your NOA, not after the deadline passes.

Understand Penalty Waiver Eligibility Before You Need It

IRAS offers limited penalty waivers, but strict conditions apply:

Late payment penalty waiver:

- You must pay the overdue tax in full by the due date stated in the penalty notice

- No waiver has been granted in the past 2 calendar years

Composition waiver (late filing):

- You must file the outstanding return before the composition due date

- You must have filed tax returns on time for the past 2 years

These are one-time relief mechanisms — not a fallback for repeat non-compliance.

Frequently Asked Questions

What is the penalty for filing income tax late in Singapore?

IRAS can issue an estimated NOA based on prior year income and impose a composition amount of up to S$5,000 per offence. Court prosecution can follow, with fines up to S$5,000 per offence. Failing to file for 2 or more years can result in twice the assessed tax plus up to 6 months' imprisonment.

What is the penalty for late payment of income tax in Singapore?

A 5% penalty applies immediately on unpaid tax after the due date. If still unpaid 60 days later, an additional 1% per completed month (capped at 12%) brings the maximum total to 17%. IRAS can also freeze bank accounts or issue a Travel Restriction Order.

What is the deadline for filing taxes in Singapore?

Individual income tax returns are due by 18 April. For companies, ECI must be filed within 3 months of the financial year-end, while Form C-S, Form C-S (Lite), or Form C is due by 30 November each year.

Can I appeal against a late filing or late payment penalty in Singapore?

Waiver requests are submitted through myTax Portal. IRAS will only consider them if all outstanding returns are filed and no waiver was granted in the past 2 calendar years. For late payment penalties, the full overdue tax must be settled before the appeal is assessed.

What happens if I ignore notices from IRAS in Singapore?

Ignoring IRAS notices leads to escalating enforcement: estimated NOAs are raised (often higher than actual liability), composition amounts are imposed, and eventually a court summons is issued. Bank accounts can be frozen through agent appointments, and a Travel Restriction Order may prevent your departure from Singapore. For foreign nationals, this can also jeopardize work pass renewals and legal stay in Singapore.