Introduction

Singapore and the UAE share robust trade ties, with bilateral trade exceeding USD 10 billion annually and thousands of Singapore businesses operating through UAE free zones, distribution channels, and digital platforms. For these businesses, staying on top of UAE tax regulation is non-negotiable.

The UAE Federal Tax Authority (FTA) has issued multiple rounds of amendments to the VAT Executive Regulations under Cabinet Resolution No. (52) of 2017, with the most recent update gazetted on 12 August 2025 and effective from 29 September 2025. These amendments carry direct compliance consequences — spanning import/export documentation, free zone VAT treatment, input tax recovery rights, and digital service obligations.

Singapore companies supplying goods, services, or digital products to UAE customers — or operating through UAE entities — need to understand how these updates affect their VAT registration, invoicing, and reporting obligations.

TLDR:

- UAE VAT remains at 5%, but Executive Regulations governing compliance, invoicing, and input tax recovery were overhauled in August 2025

- Non-resident Singapore businesses making taxable UAE supplies must register regardless of revenue threshold

- Updated documentation rules for exports, digital services, and capital assets affect most Singapore-UAE trade arrangements

- E-invoicing (PEPPOL-based) becomes mandatory from July 2026, requiring immediate preparation

- Review UAE operations against amended regulations now to avoid penalties and protect input tax credits

Understanding the UAE VAT Framework: A Quick Primer for Singapore Businesses

UAE VAT is governed by Federal Decree-Law No. (8) of 2017 and operationalized through the Executive Regulations (Cabinet Resolution No. 52 of 2017). The Federal Tax Authority (FTA) administers enforcement. The law has been amended six times since its 1 January 2018 introduction. The latest amendment was gazetted on 12 August 2025 and takes effect from 29 September 2025.

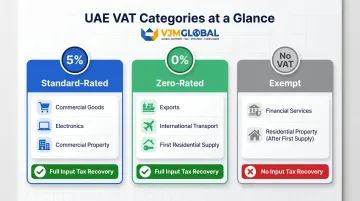

Three VAT Categories Singapore Businesses Must Know:

| Category | Rate | Examples | Impact on Input Tax Recovery |

|---|---|---|---|

| Standard-rated | 5% | Commercial goods/services, electronics, commercial property rent | Full input tax recovery allowed |

| Zero-rated | 0% | Exports, international transport, first supply of residential buildings | Full input tax recovery allowed |

| Exempt | No VAT | Financial services (no explicit fee), residential property (after first supply) | No input tax recovery allowed |

Critical Registration Thresholds:

- Mandatory registration: Taxable supplies and imports exceeding AED 375,000 over 12 months

- Voluntary registration: Taxable supplies exceeding AED 187,500 over 12 months

- Non-resident businesses (including Singapore companies): Must register for UAE VAT regardless of the AED 375,000 threshold if making taxable supplies in the UAE, even without a physical UAE presence

This non-resident registration rule is where many Singapore exporters, digital service providers, and professional firms get caught out: there is no minimum threshold exemption for foreign suppliers. If you're making taxable supplies in the UAE, registration obligations apply from the first dirham.

Recent Amendments to the UAE VAT Executive Regulations: What Changed?

The most recent round of amendments was enacted through Cabinet Decision No. 100 of 2025, issued 12 August 2025 and effective from 29 September 2025. The preceding major update was Cabinet Decision No. 100 of 2024, published in Official Gazette No. 783 on 16 September 2024 and effective from 15 November 2024. Together, these amendments restructure core compliance obligations across invoicing, input tax recovery, and digital reporting.

The five areas below cover the changes most relevant to Singapore businesses operating in or trading with the UAE.

Tax Invoice and Simplified Invoice Rules (Article 59)

Article 59 introduces the most operationally significant changes for businesses approaching the July 2026 e-invoicing rollout:

- Simplified tax invoices (previously allowed when consideration was under AED 10,000 or the recipient was not VAT-registered) will no longer be permitted for businesses within the UAE e-invoicing scope after July 2026

- The FTA is removing administrative exceptions that previously allowed businesses to skip issuing tax invoices or credit notes

- Businesses making wholly zero-rated supplies can no longer rely on "sufficient records"—they must issue UAE-schema-compliant e-invoices

For Singapore businesses, this means invoice templates need to be audited against full tax invoice requirements (supplier/recipient names, addresses, Tax Registration Numbers, detailed descriptions, tax breakdowns). Customer master data must also be complete — every invoice requires the recipient's TRN, including for zero-rated export customers.

Input Tax Recovery Conditions (Article 52)

Two changes here affect how UAE-registered entities claim input tax:

- Documentation standards are tightened: businesses must hold a valid tax invoice and intend to make payment within 6 months of the agreed date to recover input tax

- Under Article 53, input tax on medical health insurance for employees and their dependents (one spouse and up to three children under 18) is now recoverable, effective 15 November 2024 — this change is not retroactive

- Entertainment and personal-use motor vehicle restrictions remain non-recoverable

UAE entities owned by Singapore companies should verify that all input tax claims meet the updated documentation and payment timing conditions. Employee benefit costs are also worth reviewing — health insurance is now a recoverable expense.

Export Documentation Requirements (Article 30)

UAE suppliers must now retain one or more of the following to support zero-rated treatment on exports:

- Customs declarations confirming exit from the UAE

- Commercial evidence (airway bills, bills of lading, certificates of shipment)

- Shipping certificates or official evidence (export certificates, certified destination documents)

For indirect exports — where an overseas customer or agent arranges the export — that party must obtain and pass documentation back to the UAE supplier.

Singapore companies importing UAE goods should ensure their UAE suppliers receive proper export evidence. A gap in documentation can result in the UAE supplier charging 5% VAT retrospectively.

Agent and Intermediary Supplies

Cabinet Decision 100/2024 introduced new conditions for invoices issued by agents on behalf of principals. Agents may still issue tax invoices in this capacity, but additional compliance requirements now apply. Singapore trading companies selling into the UAE via UAE-based distributors or agents should review their agency agreements and invoicing arrangements against these updated requirements.

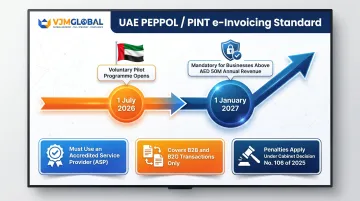

E-Invoicing Implementation Roadmap

The UAE is implementing a PEPPOL-based e-invoicing framework using a 5-corner model and the UAE PINT (Peppol International Invoice) standard. Articles 59 and 60 of the Executive Regulations have been restructured to prepare for this digital reporting obligation.

Key Timeline:

- 1 July 2026: Pilot phase / voluntary enrollment opens

- 1 January 2027: Mandatory for large businesses (annual revenue above AED 50 million)

Three operational requirements stand out for businesses planning ahead:

- Businesses cannot connect to the e-invoicing network directly — they must appoint an Accredited Service Provider (ASP)

- The mandate initially covers B2B and B2G transactions only; B2C is expected to follow within five years

- E-invoicing penalties fall under a separate instrument — Cabinet Decision No. 106 of 2025

Key Articles That Directly Affect Singapore Businesses

Article 28 — Place of Supply Rules for Services

Article 28 determines where a service is legally supplied for VAT purposes — which country's VAT rules apply depends entirely on this classification.

Under the general rule, the place of supply is the supplier's residence. For B2B services, however, the rule shifts: if the supplier is a non-resident (for example, a Singapore company) and the UAE recipient is VAT-registered, the place of supply moves to the recipient's location in the UAE. This triggers the reverse charge mechanism under Article 48 of the VAT Decree-Law — the UAE business, not the Singapore supplier, accounts for the VAT.

Certain service categories follow their own place of supply rules under Articles 21-23:

- Real estate services: where the property is located

- Transportation: where transport commences

- Cultural, sporting, and educational events: where performed

- Restaurant, hotel, and catering services: where performed

- Telecommunications and electronic services: where used and enjoyed

Impact for Singapore businesses:

- Singapore professional services firms (consulting, legal, accounting) providing B2B services to UAE-registered clients do not charge UAE VAT — the UAE client self-accounts under reverse charge

- Singapore digital service providers (SaaS, content platforms) selling to UAE consumers must register for UAE VAT and charge 5%, since the place of supply is where services are used and enjoyed

Article 52 — Conditions for Input Tax Recovery

Article 52 sets out the conditions a registered business must meet to reclaim VAT paid on purchases and expenses. All four conditions must be satisfied simultaneously:

- The claimant must be a registered Taxable Person

- The tax must have been paid or be payable

- The claimant must hold a valid tax invoice

- The claimant must intend to make payment for the supply within 6 months of the agreed date

Impact for Singapore businesses:

- UAE entities owned by Singapore companies must audit input tax claims to confirm documentation is valid and payment falls within the 6-month window

- Expenses with a dual business/personal purpose — for example, motor vehicles available for personal use — remain non-recoverable

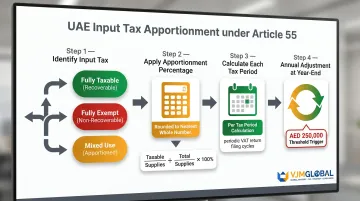

Article 55 — Apportionment of Input Tax

Article 55 applies to businesses making both taxable and exempt supplies (partially exempt businesses), requiring input tax to be split between the two categories. The apportionment methodology works as follows:

- Input tax wholly tied to taxable supplies: recoverable in full

- Input tax wholly tied to exempt or non-business supplies: not recoverable

- Input tax attributable to both: apportioned using a percentage calculation, rounded to the nearest whole number

- Calculations run each tax period, with a mandatory annual adjustment at year-end

- Where the gap between calculated recovery and actual use exceeds AED 250,000, an adjustment is required

Cabinet Decision 100/2024 extended these rules explicitly to government entities and charities.

Impact for Singapore businesses:

- Singapore financial services companies and holding companies with UAE operations must apply apportionment rules rigorously when making both taxable and exempt supplies

- Annual adjustments can produce significant VAT payables or refunds — year-end reconciliation is not optional

Articles 56-57 — Capital Assets Scheme

The Capital Assets Scheme requires businesses to monitor VAT recovered on major capital assets and adjust it if the asset's use changes over time.

The scheme applies to any single item of expenditure — or staged payments for construction and assembly — of AED 5,000,000 or more (excluding tax). Monitoring periods are:

- 10 years for immovable property (buildings)

- 5 years for all other capital assets

If the proportion of taxable vs. exempt use shifts during the monitoring period, the input tax originally recovered must be adjusted to reflect actual use.

Impact for Singapore businesses:

- Singapore companies that have purchased UAE property or significant equipment must track these assets throughout the monitoring period and report any change in use to the FTA

- Selling, transferring, or repurposing capital assets — for example, shifting from taxable to exempt activities — can trigger VAT adjustments and unexpected liabilities

Article 14 / Article 14 bis — Deregistration and FTA Cancellation Powers

Article 14 governs mandatory deregistration when a business no longer makes taxable supplies and has no intent to do so within 12 months. Article 14 bis, introduced under Cabinet Decision 100/2024, gives the FTA authority to cancel registrations proactively to protect tax system integrity.

Cabinet Decision 100/2024 adds two requirements to the deregistration process:

- All tax liabilities and penalties must be paid before deregistration is granted

- Deemed supplies must be reported on the final VAT return

Impact for Singapore businesses:

- Singapore businesses winding down UAE operations or restructuring their UAE entity must clear all VAT obligations before deregistration can proceed

- Deemed supplies — such as goods on hand or assets retained at closure — must be reported and VAT accounted for on the final return

How These Changes Impact Different Singapore Business Models

Goods Exporters and Importers

Zero-Rating for Exports: Singapore companies exporting goods to the UAE are generally zero-rated under Article 30, but must meet updated documentation conditions to preserve zero-rating.

Required Documentation (post-Cabinet Decision 100/2024):

- Customs declarations from the local Customs Department confirming exit

- Commercial evidence (airway bills, bills of lading, certificates of shipment)

- Shipping certificates or official evidence (export certificates, certified destination documents)

Concrete Scenario: A Singapore electronics distributor sells AED 500,000 worth of semiconductors to a UAE buyer. The UAE buyer arranges freight and provides a bill of lading confirming shipment from Singapore to Dubai. Under Article 30, this qualifies as an export, and the UAE buyer can import the goods VAT-free under customs relief.

If the Singapore company fails to retain proper export documentation, however, the UAE customs authority may treat the transaction as a domestic UAE supply and charge 5% VAT retrospectively.

Return/Replacement Flows:

- Goods returned from UAE to Singapore or replacement shipments may create UAE VAT events depending on how the original transaction was treated

Digital Services and E-Commerce Providers

UAE VAT Obligation for Non-Residents: Singapore-based digital service providers (SaaS, content platforms, e-learning) selling to UAE consumers face UAE VAT obligations under the non-resident supplier rules.

Place of Supply:

- Telecommunications and electronic services are supplied where used and enjoyed (Article 23)

- If the end-user is in the UAE, the place of supply is the UAE

Registration Trigger:

- Non-resident digital service providers must register for UAE VAT immediately—there is no revenue threshold exemption

Impact:

- A Singapore SaaS company selling to UAE businesses (B2B) does not charge UAE VAT if the recipient is VAT-registered (reverse charge applies)

- The same Singapore SaaS company selling to UAE consumers (B2C) must register for UAE VAT, charge 5%, and file quarterly or monthly VAT returns

UAE Free Zone Entities Owned by Singapore Businesses

Designated Zones vs. Non-Designated Zones:

- A "Designated Zone" meeting the conditions of Article 51 is treated as outside the UAE for VAT purposes (goods supplies only)

- Services supplied in Designated Zones are treated as supplied inside the UAE—standard VAT rules apply

Conditions for Designated Zone Status (Article 51):

- Specific fenced geographic area with security measures

- Customs controls for entry/exit of individuals and goods

- Internal storage/processing procedures

- Operator must comply with FTA procedures

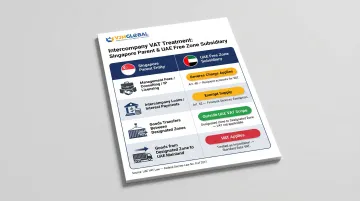

Intercompany Transactions (Singapore Parent to UAE Free Zone Subsidiary):

| Transaction Type | VAT Treatment |

|---|---|

| Management fees, consulting services, IP licensing | Services supplied inside the UAE (Art 51(6))—reverse charge applies on the UAE subsidiary under Art 48 |

| Intercompany loans (interest-bearing) | May fall under financial services exemption (Art 42) if no explicit fee/commission charged |

| Goods transfers between Designated Zones | Generally outside UAE VAT scope if goods not altered/used and follow GCC Common Customs Law suspension rules |

| Goods moving from Designated Zone to mainland UAE | Treated as an importation subject to VAT |

Compliance Risk:

- Singapore parent companies must ensure their UAE free zone subsidiaries correctly apply reverse charge on intercompany services

- Failure to self-account for VAT on reverse charge transactions is a common compliance error

Service Companies and Professional Firms

B2B Services (Singapore Firm to UAE-Registered Client):

- Under Article 28, when the supplier (Singapore firm) is a non-resident and the recipient is UAE-registered, the place of supply shifts to the UAE

- The UAE client must self-account for VAT under the reverse charge (Article 48 Decree-Law)

- The Singapore firm does not charge UAE VAT

B2C Services (Singapore Firm to UAE Unregistered Consumer):

- The place of supply is the supplier's residence (Singapore), meaning UAE VAT does not apply under the general rule

- Exception: If the service falls under a special place of supply category (for example, services performed physically in the UAE or services related to UAE real estate), UAE VAT applies

Example: Scenario 1 — B2B: A Singapore management consultancy invoices a UAE-registered company for USD 50,000 (approx. AED 183,650) with no UAE VAT charged. The UAE client self-accounts for AED 9,182.50 (5%) VAT under reverse charge on their VAT return.

Scenario 2 — B2C: The same consultancy provides advisory services to an individual UAE resident (not VAT-registered). Under the general rule, the place of supply is Singapore, and no UAE VAT applies. If the consultancy sends staff to the UAE to deliver on-site training, however, the service is performed in the UAE — triggering UAE VAT obligations.

VAT Compliance Checklist for Singapore Companies Operating in UAE

Core Actions to Take:

Assess UAE VAT Registration Requirement

- Calculate taxable supply value over the past 12 months

- Non-resident businesses: Registration is required regardless of threshold if making taxable supplies in the UAE

- Digital service providers: Immediate registration required

Review Existing Contracts with UAE Counterparties

- Confirm VAT treatment is correctly documented (zero-rated, standard-rated, reverse charge, exempt)

- Update contract language to reflect current Executive Regulation requirements

Audit Invoicing Templates

- Ensure full tax invoice requirements are met (supplier/recipient names, addresses, TRNs, detailed descriptions, tax breakdowns)

- Remove reliance on simplified invoices if within e-invoicing scope (mandatory from July 2026)

Verify Input Tax Recovery Documentation

- Confirm all input tax claims meet Article 52 standards (valid tax invoice, payment within 6 months)

- Review employee benefit costs—health insurance is now recoverable (effective 15 November 2024)

Track Capital Assets Under the Capital Assets Scheme

- Identify all capital assets exceeding AED 5,000,000 threshold

- Implement monitoring over the required period (10 years for property, 5 years for other assets)

- Report any change in use or proportion of taxable vs. exempt activities

Key VAT Filing Obligations

Filing Cycles:

- VAT returns are filed quarterly or monthly, depending on the business's registration tier as determined by the FTA

VAT Return Format:

- Submitted via the EmaraTax portal

- Penalties appear automatically once deadlines pass

- Voluntary disclosures must be submitted via EmaraTax to correct errors

Penalty Schedule (Current as of 2026):

| Violation | Penalty Amount |

|---|---|

| Late VAT registration | AED 10,000 |

| Late VAT return filing | AED 1,000 (first offense); AED 2,000 (repeat within 24 months) |

| Incorrect/underpaid VAT return | AED 1,000 (first); AED 2,000 (repeat within 24 months) |

| Voluntary disclosure (taxpayer-initiated correction) | 1% per month of unpaid tax from original due date |

| FTA audit-initiated underpayment | 15% fixed penalty on unpaid tax + late payment interest |

| Late payment (post-14 April 2026) | Flat 14% per annum, calculated monthly |

Important: Cabinet Decision No. 129 of 2025 overhauled the late payment penalty framework effective 14 April 2026. It replaces the old compounding structure (2% immediate + 4% monthly, capped at 300%) with a simpler flat 14% per annum rate.

Expert Support for Complex Compliance

Most Singapore businesses don't have dedicated UAE tax resources internally, which makes these regulatory changes easy to miss until a penalty lands. VJM Global offers international taxation advisory services—including UAE VAT exposure assessments, cross-border compliance structuring, and transfer pricing documentation—for businesses operating across jurisdictions. As a member of EAI International, the firm brings a coordinated global network to engagements that span multiple tax regimes. The practical starting point for most clients is a scoping review: mapping which UAE activities trigger registration, which contracts need updating, and where current invoicing falls short of FTA requirements.

Frequently Asked Questions

What are the new rules for VAT in UAE?

The UAE VAT rate remains 5%, but the Executive Regulations covering compliance, invoicing, input tax recovery, and place-of-supply rules have been amended several times since 2018. The most recent update took effect 29 September 2025, restructuring tax invoice requirements and setting the stage for mandatory e-invoicing from July 2026.

What is Article 52 of the UAE VAT Executive Regulations?

Article 52 sets out the conditions a registered business must satisfy to reclaim (recover) input VAT on its purchases. Key conditions include possession of a valid tax invoice, payment or intent to pay within 6 months, and the expenditure must relate to a taxable business purpose.

What is Article 55 of the Executive Regulations of the UAE VAT Law?

Article 55 deals with the apportionment of input tax for businesses that make a mix of taxable and exempt supplies. Businesses must recover only the proportion of input VAT attributable to taxable activities, calculated as a percentage that is subject to annual adjustment.

What are Articles 56-57 of the Executive Regulations?

Articles 56-57 establish the Capital Assets Scheme, requiring businesses to monitor VAT recovered on capital assets above the AED 5,000,000 threshold. If an asset's business use changes, the original VAT recovery must be adjusted over a monitoring period — 10 years for property, 5 years for other assets.

What is Article 14 of the Executive Regulations of the UAE VAT Law?

Article 14 governs mandatory VAT deregistration when a business no longer makes taxable supplies and has no intent to resume within 12 months. Under Cabinet Decision 100/2024, deregistration also requires settling all tax liabilities and penalties, and reporting any deemed supplies on the final return.

What is Article 28 of the UAE VAT Executive Regulations?

Article 28 governs place-of-supply rules for services, determining whether UAE VAT applies to a given transaction. For cross-border B2B services between Singapore and UAE entities, it establishes whether the reverse charge mechanism applies, shifting the VAT obligation from supplier to recipient.