Introduction

Many Singapore businesses discover UAE VAT obligations only after their first filing deadline passes — sometimes alongside a penalty notice. UAE VAT return filing is a mandatory periodic obligation for every VAT-registered business in Dubai, including Singapore-incorporated companies with taxable operations in the Emirates.

UAE VAT compliance cannot be assumed to mirror Singapore's GST framework. Registration thresholds, reporting granularity, penalty structures, and filing platforms operate under entirely separate rules.

Singapore businesses that treat UAE VAT as a simple extension of GST risk costly errors, escalating penalties, and FTA audit exposure.

That's exactly what this guide addresses. We'll walk Singapore business owners and finance teams through the UAE VAT return filing process step-by-step, highlight the critical differences from Singapore GST, and identify the compliance gaps that most commonly catch Singapore businesses off-guard.

Key Takeaways

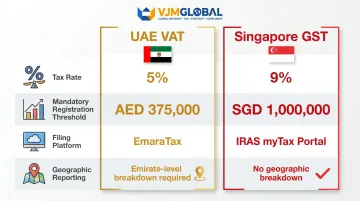

- UAE VAT runs at 5% — Singapore businesses exceeding AED 375,000 in taxable supplies must register

- Registration triggers an obligation to file returns; no threshold exemption once registered

- Returns use Form VAT 201 on the FTA's EmaraTax portal—fully digital, no paper option

- Most businesses file quarterly; those above AED 150 million annual turnover file monthly

- Returns and payments due 28 days after tax period ends

- Late filings attract AED 1,000 penalties; late payments carry 14% per annum interest under 2026 rules

What Is a UAE VAT Return — and How It Differs from Singapore GST

The UAE VAT return (Form VAT 201) is a formal declaration submitted to the Federal Tax Authority (FTA) that summarises your business's taxable sales, purchases, output VAT collected, and input VAT paid during a given tax period. The net difference is either payable to the FTA or claimable as a refund.

Rate and Threshold Differences

Two critical structural differences matter most for Singapore businesses:

| UAE VAT | Singapore GST | |

|---|---|---|

| Rate | 5% | 9% (increased January 2024) |

| Mandatory registration threshold | AED 375,000 (~SGD 140,000) | SGD 1,000,000 |

The UAE threshold is roughly one-seventh of Singapore's. A Singapore business's GST registration does not exempt it from UAE VAT obligations. The two systems operate independently.

Emirate-Level Reporting Requirement

The most operationally challenging difference: UAE VAT requires sales to be reported at the individual Emirate level (Abu Dhabi, Dubai, Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, Fujairah) within the return. Singapore GST has no geographic breakdown requirement.

This means your accounting system must capture point-of-sale Emirate data for every transaction, a level of granularity most Singapore ERP systems don't natively support.

When Does Dubai VAT Apply to Your Singapore Business?

Taxable Supply Threshold

A Singapore business becomes liable to register for UAE VAT when taxable supplies of goods or services in the UAE exceed AED 375,000 annually, regardless of incorporation location. This applies to entities with:

- A UAE branch

- A subsidiary in Dubai

- A fixed establishment (office, warehouse, staffed operations)

Critical exception: Non-resident entities making taxable supplies in the UAE must register regardless of supply value—there is no threshold. If your Singapore company provides services to UAE clients without a UAE entity accounting for the tax, you must register before your first taxable supply.

Reverse Charge Mechanism

When a Singapore business receives services from a foreign supplier, or provides certain services to UAE businesses, the UAE entity must self-account for VAT under reverse charge provisions. Singapore businesses entering the UAE market often miss this obligation entirely.

How it works:

- Singapore supplier provides services to UAE-registered client

- Singapore supplier does not charge UAE VAT

- UAE recipient self-accounts for both output VAT (Box 3) and input VAT (Box 10) on their return

Voluntary Registration

Beyond mandatory registration, businesses with UAE taxable supplies between AED 187,500 and AED 375,000 may choose voluntary registration. This allows you to recover input VAT on costs incurred during setup. Evaluate this option early, especially if you're facing significant pre-launch expenses.

How to File a Dubai VAT Return: Step-by-Step Guide

All VAT returns in the UAE must be filed electronically through the FTA's EmaraTax portal. There is no offline or XML upload option. Form VAT 201 covers seven sections:

- Taxpayer details

- Return period

- VAT on sales and all other outputs

- VAT on expenses and all other inputs

- Net VAT due

- Additional reporting requirements

- Declaration

Step 1: Log In and Select the Tax Period

- Access EmaraTax using UAE Pass or registered credentials

- Navigate to VAT → My Filings

- Select the correct return period (quarter or month being filed)

- The system auto-populates your TRN and taxpayer details

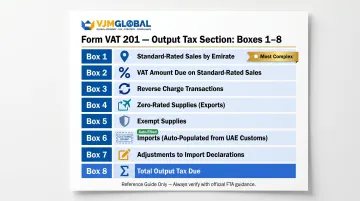

Step 2: Complete VAT on Sales and All Other Outputs (Boxes 1–8)

Box 1 requires Emirate-level breakdown:

- Enter standard-rated sales separately for each Emirate (Dubai, Abu Dhabi, etc.)

- Amount, VAT amount, and adjustments must be specified per Emirate

- This is where most Singapore businesses struggle—ensure your invoicing system captures Emirate data

Other output boxes:

- Box 3: Reverse charge sales (services received from non-UAE suppliers)

- Box 4: Zero-rated supplies (exports, international transport)

- Box 5: Exempt supplies (financial services, residential property)

- Box 6: Imports—auto-populated from UAE Customs data; review for accuracy

- Box 7: Import adjustments if Box 6 data is incomplete

Step 3: Enter VAT on Expenses and All Other Inputs (Boxes 9–11)

Box 9: Standard-rated expenses and recoverable input VAT

- Only input VAT directly related to taxable business activities may be claimed

- Blocked deductions under Article 53, VAT Executive Regulations — input VAT cannot be claimed on:

- Entertainment expenses (meals, hospitality, event tickets for non-employees)

- Motor vehicles for personal use

- Employee personal benefits

Box 10: Reverse charge purchases (services acquired from non-UAE suppliers)

Box 11: Auto-calculated total input VAT — no manual entry required

Step 4: Review Net VAT Due (Boxes 12–14) and Submit

Box 14 calculates your net VAT position:

- If output VAT (Box 12) exceeds input VAT (Box 13), you owe the FTA the difference

- If input exceeds output, the excess can be carried forward or claimed as a refund

Review all entries carefully. You can edit filings until the due date. Complete the declaration and submit.

Step 5: Make Payment by the Deadline

VAT payment must be completed within the same 28-day deadline via the FTA portal. Submitting the return without payment results in penalties. Accepted payment methods are processed directly through EmaraTax.

Filing Deadlines, Frequency, and Required Documents

Filing Frequency

Quarterly filing (businesses with annual turnover below AED 150 million):

- Q1 (Jan-Mar): Due 28 April

- Q2 (Apr-Jun): Due 28 July

- Q3 (Jul-Sep): Due 28 October

- Q4 (Oct-Dec): Due 28 January

Monthly filing (businesses above AED 150 million annual turnover) — returns are due by the 28th of the month following each reporting period.

The FTA may assign a different period in specific circumstances. Confirm your assigned period in your EmaraTax account.

Required Documents

Prepare these before each filing period:

- VAT Registration Certificate (with TRN)

- Sales invoices showing VAT at the Emirate level

- Purchase and expense invoices for input VAT recovery

- Customs declarations for imported goods

- Bank statements for reconciliation

- Credit/debit notes for adjustments

Currency Conversion Note for Singapore Businesses

Since most Singapore businesses maintain accounts in SGD, note that all UAE VAT returns must be reported in AED. All foreign currency transactions must be converted using the exchange rate on the date of supply or the FTA-approved UAE Central Bank rate.

This catches many Singapore finance teams off guard when managing UAE accounts.

Common Mistakes and Penalties Singapore Businesses Should Avoid

Incorrect Supply Classification

The most frequent error: treating UAE standard-rated supplies (5%) as zero-rated or exempt. This is particularly relevant for Singapore businesses in education, healthcare, or financial services where Singapore GST exemptions do not automatically apply to UAE operations. This is one of the most common FTA audit triggers.

Ineligible Input VAT Claims

Singapore businesses accustomed to GST input tax rules may assume similar recoverability in the UAE. Common blocked expenses include:

- Entertainment expenses (hospitality, meals, event tickets for non-employees)

- Motor vehicles for personal use

- Employee personal benefits provided at no charge

- Expenses related to exempt supplies

Late Filing and Payment Penalties

Late filing penalties:

- First offence: AED 1,000

- Repeat within 24 months: AED 2,000

Late payment penalties (new regime effective 14 April 2026): The UAE replaced the old tiered penalty structure with a flat 14% per annum applied monthly. This new rate aligns VAT penalties with Corporate Tax penalties and creates more predictable (but still material) cost exposure for late-paying businesses.

Revenue context: UAE VAT generated AED 10.1 billion in 2024 and an estimated AED 11.3 billion in 2025, signaling that the FTA is actively expanding enforcement.

Free Zone Misconception

Many Singapore businesses set up in UAE Free Zones assuming tax-free status covers VAT. That assumption is wrong — Free Zone businesses are still required to register and file if they meet the AED 375,000 threshold. VAT treatment only differs for certain designated zone transactions involving goods—services supplied in or from a Designated Zone remain subject to normal UAE VAT rules.

Remote Compliance Support

These mistakes compound quickly when managed from a distance. Singapore businesses handling Dubai VAT remotely should consider appointing a UAE-registered Tax Agent or working with a cross-border advisory firm — this reduces error risk, keeps you current on FTA regulatory changes, and ensures you have representation during audits.

VJM Global supports businesses with multi-jurisdiction tax compliance, including UAE VAT obligations for Singapore and other international operators.

Frequently Asked Questions

What is the step-by-step process to file VAT returns in Dubai?

Log in to the FTA's EmaraTax portal, select your tax period, complete Form VAT 201 by entering sales (broken down by Emirate), expenses, and net VAT, submit the return, and make payment—all within 28 days of the tax period end.

What is the deadline for VAT return filing in Dubai?

VAT returns must be submitted within 28 days from the end of the tax period. For example, a return covering January to March is due by 28 April. The same deadline applies to VAT payment.

Is VAT filing in Dubai monthly or quarterly?

Most businesses file quarterly, which applies when annual taxable turnover is below AED 150 million. Those exceeding AED 150 million file monthly. The FTA may also assign a different period in specific cases, so verify your assigned cycle in EmaraTax.

Who must file VAT returns in Dubai — is VAT filing mandatory?

All VAT-registered businesses—including Singapore companies with UAE operations—must file a return for every tax period, even if no transactions occurred (a nil return), or risk FTA penalties.

How do I claim a VAT refund in Dubai and how much can I get?

If input VAT exceeds output VAT in a period, you can either carry the excess forward or submit a formal refund application through EmaraTax. The refund amount is determined by the FTA after reviewing your claim.