Introduction

For many UK limited company directors, dividends are an attractive way to reduce overall tax liability — but getting from declaration to payment involves legal, accounting, and compliance steps that catch out even experienced business owners. The consequences of missteps are real: unlawful dividends can trigger personal liability for directors, forced repayment by shareholders, and tax penalties exceeding 33% of the amount paid.

The real challenge is compliance. Unlike salary payments, which flow through PAYE with built-in safeguards, dividend payments require directors to verify distributable profits, hold formal board meetings, and produce proper documentation — all while navigating the intersection of company law, tax law, and accounting standards.

This guide covers each dimension: the accounting treatment under FRS 102, current tax rates and allowances, the legal process mandated by the Companies Act 2006, and how to structure a compliant salary-and-dividend remuneration strategy.

TLDR: Key Takeaways

- Dividends must be paid from realised post-tax profits — unrealised gains don't count, and insufficient reserves make any payment unlawful

- Individual shareholders pay dividend tax (8.75%, 33.75%, or 39.35%) on amounts above £500, but the company pays no Corporation Tax on distributed dividends

- Board meeting minutes and dividend vouchers are legally required for every dividend payment

- Dividends reduce retained earnings directly — not the P&L — and only become liabilities once formally declared

- Salary-plus-dividend structures minimise Income Tax and eliminate National Insurance — a core tool for owner-manager tax planning

What Are Dividends in a UK Limited Company?

Dividends are distributions of a company's post-tax profits to shareholders, governed by Part 23 of the Companies Act 2006. Unlike salary or bonuses, dividends are not a business expense — HMRC Company Taxation Manual CTM02050 explicitly confirms that "dividends and other distributions are not deductible in computing income" because they represent distributions of profit rather than costs incurred to earn it.

How Dividends Differ from Salary

The fundamental distinction lies in tax treatment and legal basis:

- Salary is remuneration for employment services, subject to Income Tax via PAYE and both employee and employer National Insurance contributions (NICs)

- Dividends derive from share ownership, not employment, and cannot be classed as earnings for NICs purposes under HMRC guidance NIM02115

That distinction creates the core tax advantage: dividends attract only dividend tax (at lower rates than Income Tax on equivalent amounts), with no NICs applying on either side — employee or employer.

Proportionality Requirements

Dividends must be paid proportionally within the same class of shares, according to the rights specified in your Articles of Association.

How this plays out in practice depends on your ownership structure:

- Sole director/100% shareholder: Proportionality is automatically satisfied — no additional steps required

- Multiple shareholders: Each payment must reflect the proportional entitlement of every holder within that share class

- Multiple share classes: Rights attached to each class (as defined in your Articles) govern what each shareholder receives

When Can a UK Limited Company Legally Pay Dividends?

The legality of any dividend payment hinges on two core tests mandated by the Companies Act 2006: distributable profits and solvency.

Distributable Profits Test

Section 830(2) of the Companies Act 2006 defines distributable profits as "accumulated, realised profits, so far as not previously utilised by distribution or capitalisation, less accumulated, realised losses, so far as not previously written off." This definition has three critical implications:

- Only realised profits count — unrealised gains such as property revaluations shown on the balance sheet are excluded

- You must consider cumulative results — a profitable year doesn't automatically permit dividends if previous years' losses exceed current profits

- The test is backwards-looking — you measure distributable reserves based on the most recent annual accounts or interim accounts prepared specifically for dividend purposes

Practical example: If your company made £40,000 profit this year but has £50,000 accumulated losses from prior years, your distributable reserves are negative £10,000, and you cannot legally pay any dividend until the cumulative position becomes positive.

When to Prepare Interim Accounts

If your financial position has improved since the last annual accounts (such as strong trading in the current year), you cannot declare dividends based on anticipated profits. Section 836 CA 2006 requires that distributable profits be evidenced by "relevant accounts" — either the last audited annual accounts circulated to shareholders, or interim accounts prepared specifically to justify the distribution.

The reverse is also true — if losses since the last accounts have eroded reserves, you must reduce planned dividends accordingly, even if the statutory accounts show sufficient reserves.

Director Liability and Solvency

Directors owe fiduciary duties under Sections 171-174 of the Companies Act 2006, including the duty to exercise reasonable care, skill, and diligence. Declaring dividends without verifying distributable profits breaches these duties. In the case of Re BM Electrical Solutions Ltd, a sole director who paid himself over £220,000 labelled as "dividends" without proper reserves or documentation was held personally liable by the court.

The accounting test alone isn't sufficient. Directors must also apply a solvency test: even where distributable profits exist on paper, paying a dividend that leaves the company unable to meet its debts as they fall due is unlawful.

Shareholder Repayment Obligation

Section 847 CA 2006 provides that shareholders who "know or have reasonable grounds for believing" a distribution was unlawful must repay it to the company. In owner-managed businesses, courts presume shareholder-directors have this knowledge because they have access to financial information and control the decision-making process.

How to Account for Dividends in a UK Limited Company

Dividends are treated as equity reductions — not expenses — and the timing of when you recognise them depends on whether they are final or interim.

Double-Entry Accounting Treatment

When a dividend is declared (final dividend) or paid (interim dividend):

- Debit: Retained Earnings (Profit and Loss Reserve) — reduces equity

- Credit: Dividends Payable (current liability) — recognises obligation

When the cash payment is made:

- Debit: Dividends Payable — clears the liability

- Credit: Bank — reduces cash

Example: ABC Ltd declares a final dividend of £10,000 on 30 June 2025, payable in July.

| Date | Account | Debit (£) | Credit (£) |

|---|---|---|---|

| 30 June 2025 | Retained Earnings | 10,000 | |

| 30 June 2025 | Dividends Payable | 10,000 | |

| 15 July 2025 | Dividends Payable | 10,000 | |

| 15 July 2025 | Bank | 10,000 |

Final vs Interim Dividends: Timing of Recognition

FRS 102 — the UK accounting standard for most limited companies — sets different recognition rules for each dividend type.

Final dividends proposed or declared after the reporting date are classified as non-adjusting events. FRS 102 Paragraph 32.8 prohibits recognising these as a liability at the period end. The liability only arises once shareholders approve the dividend by ordinary resolution — typically at the AGM.

Interim dividends are recognised when paid. Under the legal precedent in Potel v CIR, directors can rescind interim dividends before payment, so the liability crystallises only upon actual payment.

Impact on Financial Statements

Dividends reduce equity directly and never appear as an expense in the Profit and Loss account. FRS 102 Paragraph 22.17 requires entities to "reduce equity for the amount of distributions to its owners," presented either in the Statement of Changes in Equity or the Statement of Income and Retained Earnings.

This treatment matters because:

- Dividends don't reduce reported profit figures (unlike salary, which is a P&L expense)

- They directly reduce the retained earnings balance available for future dividends

- The company's profit margin and EBITDA are unaffected by dividend payments

Documentation Requirements

Every dividend payment must be supported by three documents.

Dividend voucher: GOV.UK requires each voucher to show the payment date, company name, names of shareholders receiving the dividend, and the amount paid. Copies must be given to all recipients and retained by the company.

Board meeting minutes: Even if you are the sole director, formal minutes must record the date of the meeting, the resolution to declare or recommend the dividend, the amount per share, and the payment date.

Record retention: HMRC requires company records to be kept for six years from the end of the accounting period — longer than the Companies Act's three-year requirement for private companies.

Creating documentation after the fact with false dates can constitute fraud and provides no legal protection if HMRC or liquidators challenge the payment.

VJM Global, which supports over 250 UK limited companies with accounting outsourcing services, ensures dividend transactions are recorded accurately, distributable reserves are verified before each payment, and all required documentation is produced and retained to reduce compliance risk and protect directors from personal liability.

UK Dividend Tax Rates and Allowances (2024/25)

Current Tax Rates and Bands

For the 2024/25 tax year, dividend tax applies at three rates:

| Tax Band | Income Range (2024/25) | Dividend Tax Rate |

|---|---|---|

| Dividend Allowance | First £500 | 0% |

| Basic Rate | £12,571 to £50,270 (total income) | 8.75% |

| Higher Rate | £50,271 to £125,140 | 33.75% |

| Additional Rate | Above £125,140 | 39.35% |

Note: The dividend allowance was reduced from £1,000 in 2023/24 and £2,000 in prior years. Always verify current rates with HMRC or your adviser before planning distributions, as allowances and bands are subject to change.

How the Personal Allowance Interacts with Dividends

The Personal Allowance for 2024/25 is £12,570. If dividends are your only income source, the first £12,570 is sheltered by the Personal Allowance and the next £500 by the dividend allowance — meaning you can receive approximately £13,070 tax-free.

Salary and employment income use up the Personal Allowance first. Pay yourself a £12,570 salary and your entire Personal Allowance is consumed — dividend tax then applies from the first pound above the £500 dividend allowance.

No Company Tax on Dividends

The company pays no Corporation Tax on dividends distributed to shareholders. There is no withholding tax on dividends paid by UK companies to UK-resident individuals — the tax liability falls entirely on the shareholder, not the company.

Reporting and Payment: Self Assessment

While the company owes nothing, shareholders receiving dividends above the £500 allowance must declare this income via Self Assessment. Key deadlines:

- Registration: By 5 October following the end of the tax year (e.g., 5 October 2025 for 2024/25 income)

- Filing: Online tax return due by 31 January following the end of the tax year (e.g., 31 January 2026 for 2024/25)

- Payment: Tax due by 31 January

PAYE employees who receive dividends exceeding £10,000 must file a Self Assessment return. Those receiving between £500 and £10,000 should contact HMRC to update their tax code if not already registered for Self Assessment.

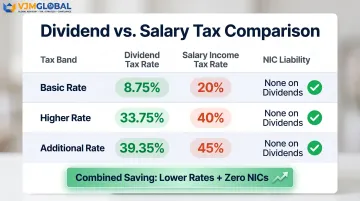

Tax Efficiency vs Income Tax

Dividend tax rates are substantially lower than Income Tax rates on equivalent amounts:

| Tax Band | Dividend Rate | Salary (Income Tax) Rate | NIC Liability |

|---|---|---|---|

| Basic | 8.75% | 20% | None on dividends |

| Higher | 33.75% | 40% | None on dividends |

| Additional | 39.35% | 45% | None on dividends |

This combined saving — lower tax rates plus zero NICs on dividends — is why salary-plus-dividend structures are the default approach for most owner-managed businesses.

How to Pay Dividends: The Legal Process Step by Step

Pre-Payment Verification

Before declaring any dividend, directors must complete three checks:

- Verify distributable profits: Review the latest annual accounts or prepare interim accounts to confirm sufficient realised reserves exist

- Confirm solvency: Ensure the company will remain able to meet its debts as they fall due after the payment

- Check Articles of Association: Confirm any specific dividend provisions or restrictions

Formal Declaration Process

For interim dividends (paid during the financial year):

- Hold a directors' meeting (even if you are the sole director)

- Pass a resolution declaring the dividend, specifying the amount per share and payment date

- Record minutes of the meeting

- Directors can act alone under authority typically granted by the Articles

For final dividends (paid after year-end):

- Directors propose the dividend

- Shareholders approve by ordinary resolution at a general meeting (typically the AGM)

- The dividend becomes a legally binding obligation only once approved

- Record minutes of both the board meeting (proposing) and shareholder meeting (approving)

Dividend Voucher Preparation

Produce a voucher for each payment showing:

- Date

- Company name

- Shareholder names

- Number of shares held

- Dividend amount per share

- Total amount paid

- Relevant tax year

Provide copies to all recipients and retain originals in company records for six years minimum.

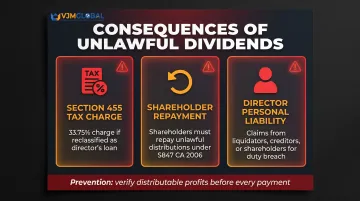

Consequences of Unlawful Dividends

If a dividend is paid without sufficient distributable profits, it is unlawful and triggers:

- A Section 455 CTA 2010 tax charge of 33.75% if HMRC reclassifies the payment as a director's loan — due nine months and one day after the accounting period ends

- A repayment obligation under Section 847 CA 2006, requiring shareholders who knew (or should have known) the dividend was unlawful to return it to the company

- Personal liability for directors, who can face claims from liquidators, creditors, or fellow shareholders for breaching their duties

Verifying distributable profits before every payment is the step that prevents all three. A dividend paid against outdated accounts can cost directors significantly more than the tax saving they were aiming for.

Salary and Dividends: Building a Tax-Efficient Remuneration Strategy

The Core Principle

Most UK owner-directors pay themselves a modest salary — typically around £12,570 (the Personal Allowance level) — and extract additional income as dividends to minimise Income Tax and eliminate NICs on the majority of their earnings.

National Insurance Thresholds for 2024/25

Current thresholds:

| Threshold | Annual Amount |

|---|---|

| Secondary Threshold (employer NI starts) | £9,100 |

| Primary Threshold (employee NI starts) | £12,570 |

| Upper Earnings Limit | £50,270 |

Employee NI: 8% between Primary Threshold and Upper Earnings Limit; 2% above. Employer NI: 13.8% above Secondary Threshold.

Optimal Salary Level for 2024/25

Two common strategies exist:

Strategy 1 — £9,100 (Secondary Threshold):

- No employee NI, no employer NI

- Salary falls within Personal Allowance, so no Income Tax

- Leaves £3,470 of Personal Allowance unused

Strategy 2 — £12,570 (Personal Allowance level):

- No employee NI (below Primary Threshold), no Income Tax

- Triggers employer NI of 13.8% on the £3,470 gap (approximately £479)

- However, the additional salary plus employer NI is deductible for Corporation Tax, generating a CT saving of approximately £750 (at 19% rate)

- Net benefit: approximately £270 (£750 CT saving minus £479 NI cost)

ICAEW guidance confirms that "the optimum salary for a director in this case will be £12,570" where the individual has the full Personal Allowance available.

To see how these strategies play out in practice, consider a director extracting £50,000 in total income during 2024/25.

Worked Example: Salary-Only vs Salary-Plus-Dividend

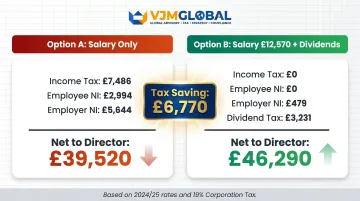

Scenario: Owner-director extracts £50,000 total income in 2024/25.

Option A — Salary only (£50,000):

- Income Tax: (£50,000 - £12,570) × 20% = £7,486

- Employee NI: (£50,000 - £12,570) × 8% = £2,994

- Employer NI: (£50,000 - £9,100) × 13.8% = £5,644

- Corporation Tax saving: (£50,000 + £5,644) × 19% = -£10,572 (deduction)

- Net to director: £39,520

- Net cost to company: £45,072 (before CT relief)

Option B — Salary £12,570 + Dividends £37,430:

- Salary:

- Income Tax: £0 (within Personal Allowance)

- Employee NI: £0

- Employer NI: (£12,570 - £9,100) × 13.8% = £479

- Dividends:

- First £500: £0 (dividend allowance)

- Remaining £36,930: £36,930 × 8.75% = £3,231

- Corporation Tax saving on salary: (£12,570 + £479) × 19% = -£2,479

- Net to director: £50,000 − £479 (employer NI) − £3,231 (dividend tax) = £46,290

- Tax saving vs Option A: £6,770

The worked example assumes a 19% Corporation Tax rate. When profits are higher, the calculus shifts.

When Salary Might Be More Efficient

At the 25% Corporation Tax rate (for profits above £250,000), salary or bonus payments may become more efficient than dividends because the higher CT deduction can outweigh the NIC cost.

ACCA guidance notes that "when a company is a 25% taxpayer, the salary/bonus route can be more efficient than dividends."

Individual Circumstances Matter

The examples above use a single director with no other income and a straightforward tax profile. Real situations are rarely that clean. The optimal strategy depends on:

- Other income sources (rental income, pensions, spouse's income)

- Company profitability and Corporation Tax rate

- IR35 status for contractors

- Pension contribution plans

- Student loan repayments

Given this complexity, most owner-directors benefit from working with an accountant who can model scenarios against their specific numbers rather than applying a one-size-fits-all approach.

Frequently Asked Questions

How do you account for dividends in the UK?

Dividends are recorded by debiting Retained Earnings and crediting Dividends Payable when declared (final) or paid (interim), then debiting Dividends Payable and crediting Bank when cash is transferred. They reduce equity directly and never appear as P&L expenses.

How to report dividend income in the UK?

Shareholders receiving dividends above the £500 annual allowance must report this via Self Assessment by 31 January following the relevant tax year. Those receiving over £10,000 must file a return; those between £500 and £10,000 can contact HMRC to update their tax code instead.

How to avoid paying tax on dividends in the UK?

You cannot legally avoid all dividend tax, but you can minimise it by using your £500 dividend allowance, ensuring dividends fall within your Personal Allowance where salary is low, and keeping total income within the basic rate band to benefit from the 8.75% rate.

What is the 25% dividend rule?

The "25% rule" refers to double tax treaty provisions (OECD Model Tax Convention Article 10), where a parent company holding at least 25% of voting power may qualify for reduced withholding rates on dividends. It does not apply to domestic UK dividends, which carry no withholding tax.

Can you pay dividends if your company has made a loss?

You cannot pay dividends in a loss year unless sufficient retained profits from prior years remain in distributable reserves. Under the Companies Act 2006, cumulative realised profits must exceed cumulative realised losses before any distribution is lawful.

What is the difference between a final dividend and an interim dividend?

A final dividend is declared by shareholders (typically at the AGM) after year-end accounts are approved and becomes a legal liability on declaration. An interim dividend is declared and paid by directors during the financial year and only becomes a liability when actually paid, allowing directors to rescind it before payment.

Dividend accounting in UK limited companies requires compliance with company law, accurate record-keeping, and deliberate tax planning. Whether you're an experienced director or newly incorporated, verifying distributable profits, maintaining proper documentation, and structuring remuneration efficiently are essential to protecting yourself legally and maximising take-home income. UK businesses working with VJM Global benefit from a team of qualified accountants with 30+ years of experience across tax, audit, and cross-border compliance — handling dividend documentation, remuneration planning, and accounting outsourcing so owner-directors can focus on running their business.