Introduction

The UK government introduced R&D tax credits in 2000 to position Britain as a global innovation leader. Since then, the scheme has undergone its most significant overhaul in two decades. From April 2024, most companies now claim under a new merged scheme — and R&D-intensive loss-making SMEs face a dramatically different landscape than they did just three years ago. For businesses that haven't revisited their claims process recently, the gap between what they expect to recover and what HMRC now accepts can be substantial.

This guide covers what UK SMEs, growing companies, and multinationals operating in the UK need to know about the current R&D tax credit landscape. We'll walk through who qualifies, current rates under each scheme, the economic impact debate, and how to make a successful claim in today's compliance-heavy environment.

TLDR: Key Takeaways

- UK R&D tax credits reduce Corporation Tax or provide cash payments for companies investing in qualifying innovation

- Most companies now claim under the merged RDEC-style scheme introduced in April 2024

- R&D-intensive loss-making SMEs may qualify for Enhanced R&D Intensive Support (ERIS), worth up to 27%

- Qualifying expenditure includes staff costs, subcontractors, materials, software, and cloud computing costs

- HMRC now reviews roughly 17% of all claims — enforcement staff have grown fivefold since 2021

- Poorly evidenced claims post-reform face rejection or claw-back; specialist support reduces that risk substantially

What Are UK R&D Tax Credits and Why Do They Exist?

UK R&D tax credits are a Corporation Tax incentive designed to reward businesses that invest in advancing science or technology. Introduced in 2000 for SMEs and extended to large companies in 2002, the scheme reduces tax bills or provides cash repayments to companies undertaking qualifying R&D activities.

R&D drives productivity and economic growth, but innovation is inherently risky and costly. The credits lower the financial barrier to private-sector investment, helping the UK remain competitive globally and work towards the government's target of increasing total R&D spending to 2.4% of GDP by 2027.

The 2023-24 figures show just how far the scheme reaches:

- Average SME claim: ~£85,000

- Average RDEC claim: ~£438,000

- Total relief claimed: £7.6 billion

- Claim volume: Down 26% year-on-year as reforms filtered out non-qualifying applications

All figures sourced from HMRC's R&D Tax Credits Statistics, September 2025.

Who Qualifies for UK R&D Tax Credits — and What Counts as R&D?

Eligibility Requirements

Three core criteria determine eligibility:

- The company must be a UK-incorporated limited company subject to Corporation Tax

- It must have carried out qualifying R&D activities

- It must have incurred expenditure on those activities

Only companies chargeable to UK Corporation Tax can qualify — sole traders and partnerships are explicitly excluded.

The advance being sought must be in science or technology, not arts, humanities, or social sciences. Manufacturing, information and communication, and professional/scientific services represent the top claiming sectors, accounting for 72% of total claims. Care homes, restaurants, personal trainers, and retailers rarely qualify.

What Counts as a Qualifying R&D Activity

HMRC defines qualifying R&D as attempting to resolve a scientific or technological uncertainty — meaning the outcome is not readily deducible by a competent professional in the field. This can involve:

- Creating new products, processes, or services

- Modifying existing ones to achieve an appreciable improvement in overall knowledge

- Overcoming technical challenges where the solution isn't obvious to an expert

The project doesn't need to have succeeded to qualify. What matters is that genuine uncertainty existed and a systematic approach was taken to resolve it.

R&D projects typically sit within larger commercial initiatives. Only the components directed at resolving technological or scientific uncertainty are eligible — routine testing, commercial production work, or administrative tasks within the same project won't qualify.

Qualifying Costs

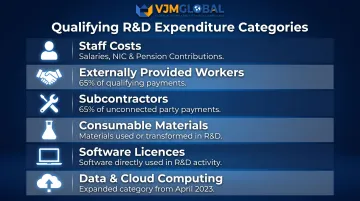

Qualifying expenditure categories include:

- Staff costs: salaries, employer's NIC, pension contributions, reimbursed expenses

- Externally provided workers (EPWs): 65% of payments to unconnected staff providers

- Subcontractors: 65% of payments to unconnected contractors

- Consumable materials: items used up or transformed in the R&D process

- Software licences: directly used in R&D activities

- Data licences and cloud computing costs: expanded category from April 2023

The line between qualifying and non-qualifying costs is rarely obvious. Even within genuine R&D projects, time logs, project records, and cost allocations need to clearly tie each expense to the uncertainty being resolved — not just to the broader commercial project.

Current UK R&D Tax Credit Rates: What Can You Claim?

The Merged Scheme (From April 2024)

For accounting periods beginning on or after 1 April 2024, most companies claim under a new merged RDEC-style scheme. The above-the-line credit rate is 20%, treated as taxable income.

The effective net benefit depends on your Corporation Tax rate:

- 15% for companies paying the 25% main CT rate

- 16.2% for companies paying the 19% small profits rate (taxable profits up to £50,000)

This applies regardless of company size, consolidating what were previously separate SME and RDEC schemes.

Enhanced R&D Intensive Support (ERIS) — The Exception

Loss-making SMEs that are R&D intensive can claim under ERIS rather than the merged scheme. ERIS eligibility requires qualifying R&D expenditure to represent at least 30% of total expenditure (reduced from 40% for periods beginning on or after 1 April 2024).

Under ERIS:

- Additional deduction rate: 86% (on top of the normal 100% deduction)

- Payable credit rate: 14.5%

- Effective benefit: up to 27% of qualifying R&D spend

This is the highest available rate, making ERIS particularly valuable for early-stage, pre-revenue companies in sectors like tech and life sciences.

A one-year grace period also applies for companies that previously met the intensity threshold but narrowly miss it in a subsequent period.

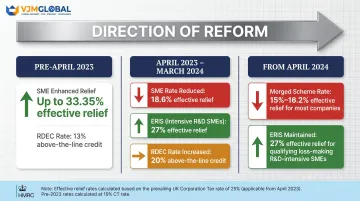

Pre-April 2024 Claims: Legacy Rates

If you're filing for an accounting period that started before April 2024, the old SME and standalone RDEC rates still apply. The table below summarises the key figures:

| Period | Company Type | Enhancement | Credit Rate | Effective Benefit |

|---|---|---|---|---|

| Pre-1 April 2023 | Loss-making SME | 130% additional | 14.5% payable | Up to 33.35% |

| Pre-1 April 2023 | Profit-making SME | 130% additional | N/A | Up to 24.7% |

| 1 Apr 2023 – 31 Mar 2024 | Loss-making non-intensive SME | 86% additional | 10% payable | Up to 18.6% |

| 1 Apr 2023 – 31 Mar 2024 | ERIS-qualifying SME | 86% additional | 14.5% payable | Up to 27% |

| From 1 April 2024 | All (merged scheme) | N/A | 20% above-the-line | 15%–16.2% |

Selecting the correct scheme depends on your accounting period start date, company size, profitability, and R&D intensity — and misapplying these criteria is one of the most frequent reasons HMRC opens an enquiry.

The Economic Impact of UK R&D Tax Credits

The Intended Economic Value

The concept of "additionality" measures the extent to which R&D tax credits generate additional R&D investment that wouldn't have occurred without the incentive. HMRC's 2015 evaluation estimated £1.53–£2.35 of R&D spend was stimulated per £1 of tax forgone, with the large company scheme showing higher ratios (£2.35) than SME payable credits (£1.53).

This positive multiplier effect supported the scheme's expansion and the government's goal to raise total UK R&D investment to 2.4% of GDP by 2027.

The Additionality Concern and Compliance Problem

Later evaluations told a more divided story. A 2020 HMRC study found RDEC additionality remained strong at £2.4–£2.7 per £1, but a separate SME scheme evaluation revealed sharply lower ratios — just £0.60–£1.00 per £1 for SME payable credits. The two schemes were no longer performing equally.

That drop in additionality coincided with a surge in ineligible and fraudulent claims. HMRC estimated overall error and fraud at 16.7% (£1.13 billion) for 2020–21, with the SME scheme posting a 24.4% non-compliance rate. Non-R&D sectors were particularly exposed — accommodation and catering saw compliance rates as low as 16%.

Inflated and bogus claims wasted public funds, damaged the reputation of legitimate claimants, and triggered a crackdown that now subjects genuine applications to far heavier scrutiny.

Broader Innovation and Productivity Effects

The sectors filing the most R&D tax credit claims are, broadly, the ones driving UK productivity growth:

- Manufacturing, tech, and professional services account for 71% of total relief claimed

- These industries invest in qualifying R&D at higher rates than most other sectors

- Their claim volumes suggest the scheme does reach genuinely innovation-intensive activity

Whether the scheme delivers net economic value depends heavily on which part of it you examine. RDEC (the large company route) has consistently shown strong additionality. The SME scheme, by contrast, has struggled — its ratio dipped below £1 per £1 forgone, meaning the incentive was, at points, generating less R&D spend than it cost the Treasury. The 2023–2024 reforms — merging the two schemes and tightening eligibility — were a direct response to that imbalance.

The 2023–2024 Reform Wave: What Changed and Why

From April 2023, significant rate changes took effect:

- SME additional deduction reduced from 130% to 86%

- SME payable credit rate fell from 14.5% to 10% (except ERIS-qualifying companies)

- RDEC increased from 13% to 20%

- Corporation Tax main rate increased from 19% to 25%

Driven by fraud concerns, poor additionality outcomes in the SME scheme, and fiscal pressure, these cuts set the stage for deeper structural change.

The April 2024 merged scheme was the result. Rather than running two parallel systems, HMRC consolidated most claims into a single merged RDEC-style framework — reducing compliance complexity, closing fraud vectors, and bringing the UK closer to how other major economies structure R&D incentives. ERIS remained as a targeted carve-out for genuinely innovation-intensive SMEs.

Compliance requirements intensified :

- Claim notification forms must be submitted within six months of the accounting period end

- Additional Information Forms (AIF) became mandatory for all claims from August 2023

- HMRC enquiry coverage reached approximately 17% of claims in 2023-24 (roughly 9,700 compliance checks)

- R&D compliance staff grew from 100 to over 500

Companies must now treat documentation as a core requirement, not an afterthought. Claims submitted without robust supporting evidence face a significantly higher chance of HMRC scrutiny — and rejection.

How to Claim UK R&D Tax Credits: A Practical Guide

R&D tax credit claims are made as part of the CT600 Corporation Tax return. The process involves:

1. Submit a claim notification form Required within six months of the accounting period end for first-time claimants or those whose last claim was made more than three years before. The form must include company UTR, senior internal R&D contact details, all agent details, accounting period dates, and a high-level project summary.

2. Prepare the Additional Information Form (AIF) Mandatory for all claims from August 2023 onwards. The AIF captures project-level detail and qualifying expenditure — it must be submitted before or alongside the CT600 return.

3. Complete the CT600 with detailed technical narrative The claim must include a comprehensive explanation of qualifying projects and a breakdown of qualifying expenditure. The technical narrative should demonstrate:

- The scientific or technological uncertainty faced

- Why the solution wasn't readily deducible by a competent professional

- The systematic approach taken to resolve the uncertainty

- Project boundaries separating qualifying from non-qualifying activity

Common Mistakes That Trigger HMRC Enquiries

- Claiming for activities that don't meet the scientific or technological uncertainty test

- Poor documentation of project boundaries

- Over-claiming staff time without adequate timesheets or project records

- Failing to apply the correct scheme based on company size and accounting period

- Missing notification deadlines or submitting incomplete AIFs

- Inconsistencies between R&D claims and other HMRC-held data

For UK companies with operations in India — or Indian entities receiving R&D funding from a UK parent — cross-border cost allocation and transfer pricing obligations can affect what qualifies for relief. VJM Global advises on the international tax compliance side of these arrangements, including how intercompany agreements are structured for UK-India operations.

Frequently Asked Questions

How much do you get for R&D tax credits?

The benefit depends on your company's size, profitability, and which scheme applies. Under the merged scheme from April 2024, most companies receive an effective net benefit of 15%–16.2% of qualifying expenditure. R&D-intensive loss-making SMEs under ERIS can receive up to 27%. The average SME claim was approximately £85,000 in 2023–24.

What can R&D tax credits be used for?

R&D tax credits reduce a company's Corporation Tax liability or, for loss-making companies, provide a cash repayment from HMRC. The funds can be deployed freely for any business purpose, including hiring staff, funding further R&D, or improving cash flow.

What is the 80% rule for R&D credit?

The "80% rule" applies to the US R&D tax credit system, not UK R&D tax credits. Under the UK merged scheme, the relevant rule limits qualifying contracted-out R&D expenditure to 65% of payments made to unconnected subcontractors and externally provided workers.

Who is eligible for UK R&D tax credits?

UK-incorporated limited companies subject to Corporation Tax that have carried out and spent money on qualifying R&D activities in science or technology are eligible. Sole traders, partnerships, and activities in arts or social sciences do not qualify.

What is the difference between the SME scheme and RDEC?

The SME scheme offered higher relief through an enhanced deduction, whilst RDEC was an above-the-line credit for large companies and grant-funded SMEs. Since April 2024, both tracks have merged into a single RDEC-style scheme — only ERIS-eligible R&D-intensive SMEs now claim under a separate enhanced rate.

What changed with the UK R&D tax credit scheme from April 2024?

HMRC merged the previous SME and RDEC schemes into a single track for most companies, offering a 20% above-the-line credit (net benefit 15%–16.2%). ERIS was retained separately for qualifying loss-making SMEs spending 30%+ of total costs on R&D, providing up to 27% benefit.