Introduction

UK businesses claimed £7.6 billion in R&D tax relief for the 2023–2024 tax year across 46,950 claims filed with HMRC — yet many eligible companies still leave money on the table, either unaware they qualify or uncertain how to navigate the system.

The confusion is understandable. Between April 2023 and April 2024, HMRC reformed virtually every aspect of R&D relief: rates changed, new cost categories were introduced, a mandatory pre-notification requirement arrived, and a new merged scheme replaced the previous dual-track system. For businesses trying to claim correctly, the landscape shifted considerably.

This guide explains the current UK R&D tax credit system in plain English — for UK limited companies of all sizes and sectors that invest in resolving scientific or technological problems as part of their work. It covers:

- Who can claim and which activities qualify

- Which costs count toward a claim

- How the two active schemes work

- What the claims process now involves

Key Takeaways

- R&D tax credits are a Corporation Tax relief for companies resolving scientific or technological uncertainties — covering far more than traditional lab-based research

- From April 2024, most companies use the merged scheme (20% gross credit); R&D-intensive loss-making SMEs may qualify for ERIS instead

- Qualifying costs include staff wages, subcontractor fees, software licences, consumables, and cloud/data costs — all must be directly tied to eligible R&D activity

- Loss-making companies can receive a payable cash credit, making the relief accessible to pre-revenue businesses too

- Claims now require pre-notification to HMRC and a detailed additional information form — robust records are essential to a successful claim

Who Can Claim UK R&D Tax Credits?

Only UK limited companies chargeable to Corporation Tax can claim R&D tax relief. Sole traders, ordinary partnerships, and entities outside the UK Corporation Tax net are excluded from claiming directly.

Eligibility by Company Size

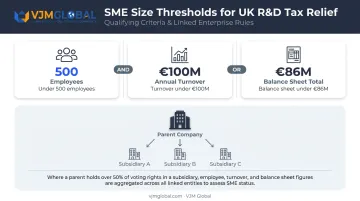

SME status matters because the Enhanced R&D Intensive Support scheme (ERIS) is only available to SMEs. HMRC defines an SME as a company with:

- Fewer than 500 employees, AND

- Either annual turnover under €100 million or a balance sheet total under €86 million

One area that catches businesses off guard: linked and partner enterprises must be included when calculating these thresholds.

If another entity holds over 50% of your company's voting rights or exercises control, you are "linked" — their financial figures are aggregated with yours. A subsidiary of a large group may fail the SME test even if it looks small in isolation.

Once you've confirmed SME status, the applicable scheme follows. For accounting periods beginning on or after 1 April 2024, both SMEs and large companies generally claim under the merged scheme — so the previous need to identify which separate scheme applies is largely gone. The main exception is ERIS, which remains SME-specific.

Eligible Industries and Sectors

R&D activity takes place across a wide range of sectors. HMRC's own statistics show that Information and Communication, Manufacturing, and Professional, Scientific and Technical sectors together account for 72% of all claims — but qualifying work also happens in construction, engineering, software development, food and drink, agriculture, financial technology, and many others.

That said, some activities and sectors are excluded:

- Advances in the arts, humanities, or social sciences (including economics) do not qualify under any circumstances

- HMRC has identified sectors it flags as rarely eligible, including care homes, childcare providers, personal trainers, wholesalers, retailers, pubs, and restaurants

What matters is whether the specific project meets the R&D definition. The sector is secondary.

What Qualifies as R&D for Tax Purposes?

HMRC's definition is precise: a project qualifies as R&D when it seeks to achieve an advance in science or technology by overcoming scientific or technological uncertainty. Both elements must be present.

Advance in Science or Technology

The advance must benefit the overall field — not just your own company's knowledge. Creating a genuinely new process, product, or service increases overall capability. So does appreciably improving an existing one. Routine upgrades and cosmetic changes do not qualify.

If a competent professional in the field would consider the outcome obvious or straightforward, it is unlikely to represent a qualifying advance.

From 1 April 2023, pure mathematics is treated as science for R&D purposes. This directly benefits businesses working in data science, AI, and machine learning where the underlying work involves mathematical innovation.

Scientific or Technological Uncertainty

Uncertainty exists when a competent professional in the field cannot determine — even after reviewing all available evidence — whether something is technically feasible or how to achieve it in practice.

A practical example: developing a software algorithm to process a specific type of unstructured data where no established method exists. The uncertainty is not whether you want to do it, but whether it can be done and how.

Two important points:

- Failed projects still qualify — systematic attempts to resolve an uncertainty count, even if the advance is never achieved.

- Mathematical advances made as part of resolving such uncertainties are now within scope.

Defining the Project Boundaries

A qualifying R&D project covers all activities carried out to resolve the specific scientific or technological uncertainty. However, that R&D project may sit within a larger commercial project that also includes non-qualifying work — only the R&D component is eligible.

Getting project boundaries right is one of the most common problem areas. Businesses frequently make two opposite mistakes:

- Undercounting — missing qualifying work that sits within a larger commercial project

- Overclaiming — including routine commercial activity that does not meet the uncertainty threshold

Both errors carry risk with HMRC. Defining boundaries accurately from the outset is essential.

What Costs Can You Include in Your R&D Claim?

Once qualifying R&D activity is established, only specific categories of expenditure associated with that activity count. Not every cost in a project qualifies — only those HMRC recognises under its defined headings.

Staff Costs

Staff costs are typically the largest component of any R&D claim. Qualifying elements include:

- Gross salary and wages

- Employer's Class 1 National Insurance contributions

- Employer pension contributions

- Reimbursed expenses directly related to R&D

Employees must be directly and actively engaged in the R&D. Where staff split their time between qualifying and non-qualifying work, only an appropriate proportion of their costs is claimable. Supervisory and support staff can be included where their time directly relates to the project.

Subcontractors, Consumables, and Software

Under the merged scheme (from April 2024), the company that commissions and controls the R&D can generally claim subcontractor costs. For unconnected providers, 65% of relevant payments are claimable. The subcontractor performing the work cannot also claim the same costs — one project, one claim. Connected-party rules and questions of who "controls" the R&D make this one of the more technically demanding areas of any submission.

Other qualifying cost categories include:

- Consumable materials used up in R&D activity — fuel, power, water, chemicals, ingredients

- Software licence fees used directly in the R&D project

- Cloud computing and data licence costs (qualifying from 1 April 2023) where directly aligned with R&D activity, not merely indirect support functions

Not everything incurred during an R&D project is claimable. Costs that don't directly contribute to resolving the scientific or technological uncertainty — routine payroll administration, general overhead — fall outside the qualifying headings even if they sit within the same project budget.

UK R&D Tax Credit Schemes and Rates

As of April 2024, two schemes are active. The older standalone SME scheme and the pre-2024 RDEC scheme apply only to accounting periods beginning before 1 April 2024.

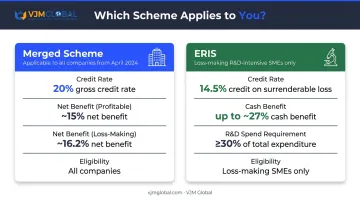

The Merged Scheme

For accounting periods beginning on or after 1 April 2024, most companies claim under the merged R&D expenditure credit scheme. Its core mechanics:

| Metric | Detail |

|---|---|

| Credit rate | 20% of qualifying R&D expenditure |

| Tax treatment | Gross taxable credit, brought into account above the line |

| Net benefit (profitable companies) | Approximately 15% after Corporation Tax at 25% |

| Net benefit (loss-making companies) | Approximately 16.2% as a repayable credit |

The merged scheme simplifies administration by applying uniformly to both SMEs and large companies. For many smaller businesses, though, the trade-off is a lower effective benefit than the old SME-specific scheme provided.

Enhanced R&D Intensive Support (ERIS)

ERIS is available to loss-making SMEs where at least 30% of total expenditure consists of qualifying R&D spend (reduced from 40% for periods from April 2024).

Key figures:

- Credit rate: 14.5% of surrenderable loss

- Cash benefit: Up to approximately 27% of qualifying R&D spend — the highest rate available under either current scheme

- Claims: HMRC statistics recorded 3,990 R&D intensive claims for 2023–2024, with ERIS-specific data expected in later reporting periods once the scheme has had time to accumulate full-year data

For a loss-making SME investing heavily in innovation, ERIS can be more valuable than the standard merged scheme. If R&D spend is approaching the 30% threshold, it's worth modelling both routes before filing — the difference in cash benefit can be material.

How to Claim UK R&D Tax Credits

The claims process now has more steps than it did before 2023, and missing any of them can invalidate a claim entirely.

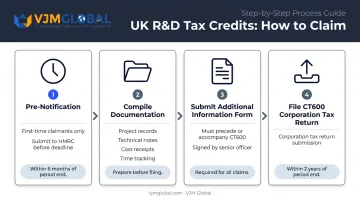

Pre-Notification Requirement

First-time claimants, and companies that have not claimed in the past three years, must notify HMRC of their intention to claim within six months of the end of the accounting period. There is no discretion here — late notifications are not accepted, and a missed deadline means losing that period's claim permanently.

Additional Information Form

Before or on the same day as filing the Corporation Tax return (CT600), companies must also submit a mandatory additional information form. Where both are submitted on the same day, the additional information form must go first.

The form requires:

- Description of the R&D undertaken and the field of science or technology

- The baseline position and the advance sought

- Explanation of how scientific or technological uncertainties were addressed

- Breakdown of qualifying costs and amount claimed

- Details of any agent who advised on the claim

- Include sign-off from a senior company officer

Thorough supporting documentation — project records, technical notes, time-tracking evidence, and cost receipts — is essential both for completing the form accurately and for defending against an HMRC enquiry.

General Claim Deadline

R&D claims must be filed within two years of the end of the relevant accounting period. Note that this is separate from the pre-notification deadline, which falls six months after period end. Both deadlines must be met independently.

Navigating these requirements — particularly for first-time claimants or companies with complex project boundaries — is where specialist support adds the most practical value.

VJM Global's tax advisory team has worked with 250+ UK businesses across industries including technology, manufacturing, financial services, and emerging sectors such as fintech and edtech. Our team can help you assess R&D eligibility, structure qualifying costs correctly, and ensure the claims process is handled with the documentation rigour HMRC now expects.

Frequently Asked Questions

What qualifies for the research and development tax credit?

A project must seek an advance in science or technology by resolving a genuine uncertainty that a competent professional in the field could not readily solve. The work must be systematic, and the advance must benefit the overall field — not just the claimant's own knowledge or processes.

How much do you get back for R&D tax credit?

Under the merged scheme, most companies receive a net benefit of approximately 15–16.2% of qualifying R&D spend. R&D-intensive loss-making SMEs under ERIS can receive up to approximately 27%. HMRC reported £3.15 billion claimed across 36,885 SME scheme claims for 2023–2024.

Is the UK R&D credit refundable?

Yes. Loss-making companies with no Corporation Tax liability can surrender their losses and receive a repayable cash credit directly from HMRC. This makes the relief accessible to pre-revenue and early-stage businesses , though the PAYE cap (£20,000 plus 300% of relevant PAYE and NIC liabilities) limits the maximum payable amount.

What is the difference between the SME scheme and the merged R&D scheme?

The SME scheme (186% enhanced deduction) applied to accounting periods starting before 1 April 2024. The merged scheme, effective from April 2024, applies to all companies except ERIS-qualifying SMEs and delivers a 20% above-the-line credit — a lower net benefit for most SMEs than the old scheme provided.

Can loss-making companies claim R&D tax credits in the UK?

Yes. Loss-making companies can claim a payable cash credit subject to the PAYE cap. This makes the relief particularly valuable for high-growth startups and early-stage companies investing heavily in R&D before reaching profitability — provided their PAYE and NIC liabilities support a meaningful claim.

What is the deadline to submit an R&D tax credit claim in the UK?

R&D claims must generally be filed within two years of the end of the relevant accounting period. However, the pre-notification requirement — which must be submitted within six months of the period end — is a separate and earlier deadline. Missing pre-notification invalidates the claim, regardless of whether the main return is filed on time.