Introduction

The UK SME R&D tax credit scheme launched in April 2000 with straightforward rules: a 150% enhanced deduction and a 16% payable credit for qualifying innovation spend. For the first eight years, the framework remained relatively stable. But the period since 2008 tells a very different story.

Since then, the scheme has undergone twelve rate changes, the introduction of a parallel RDEC regime, and a dramatic reduction in cash benefits for loss-making SMEs. April 2024 brought a fundamental restructure into a merged scheme. What was once a straightforward uplift has become a layered, compliance-heavy framework — and knowing exactly when each change took effect directly affects how much you can claim.

For companies with accounting periods spanning transition dates — particularly April 2023 and April 2024 — you'll need specialist knowledge to navigate the rules correctly. The timeline below traces each change, showing how the government has repeatedly recalibrated the balance between incentivising innovation, controlling Exchequer costs, and tightening fraud controls.

Key Takeaways

- The SME enhancement rate peaked at 230% in April 2015 before being cut to 186% in April 2023

- RDEC launched in April 2013 at 10% and now operates at 20%, forming the structural basis for the merged scheme

- From April 2024, most companies claim under a single merged RDEC-style scheme (R&D-intensive loss-making SMEs use ERIS at 14.5%)

- Mandatory Additional Information Forms and advance claim notifications took effect from August 2023

- The claim window shortened permanently to two years in March 2008, down from the original six-year limit

The SME R&D Tax Credit Before 2008: Setting the Baseline

When the Labour government and Chancellor Gordon Brown introduced R&D tax credits on 1 April 2000, the framework was deliberately simple. An SME spending £100 on qualifying R&D could deduct £150 from taxable profits — a 150% enhanced deduction representing a 50% uplift on actual spend.

Loss-making companies could surrender the enhanced loss for a payable cash credit of 16%.

Eligibility criteria at launch:

- Fewer than 250 employees

- Annual turnover below €50 million

- Balance sheet total under €43 million

- Minimum R&D spend of £25,000 per accounting period (reduced to £10,000 in September 2003)

The scheme was designed to encourage innovation in smaller companies where capital constraints limited R&D investment. The 2004 DTI Guidelines on the Meaning of Research and Development for Tax Purposes formalised the R&D definition that HMRC still references today, requiring projects to resolve genuine scientific or technological uncertainty.

The scheme continued to develop in the years that followed, with several incremental changes before 2008:

Pre-2008 additions:

- Large company scheme at 125% enhancement, introduced April 2002 (no payable credit)

- Consumables and software costs added to qualifying expenditure from April 2004

- Minimum spend threshold cut from £25,000 to £10,000 in 2003, opening access to micro-businesses

By early 2008, HMRC was processing around 5,000 SME R&D claims annually — a fraction of the eligible population, and well below the volumes the scheme would reach after the rate enhancements that followed.

2008: Wider Access, Enhanced Rates, and a Shorter Claim Window

August 2008 brought the first significant expansion of the SME definition. The thresholds doubled across all three metrics:

| Threshold | Pre-August 2008 | Post-August 2008 |

|---|---|---|

| Headcount | Fewer than 250 | Fewer than 500 |

| Turnover | €50 million | €100 million |

| Balance Sheet | €43 million | €86 million |

This change had real impact. Companies previously too large for the SME scheme (previously limited to the less favourable large company route at 125%) could now access the higher relief. A mid-sized manufacturer with 350 employees and €70 million turnover suddenly qualified as an SME for tax purposes.

Rate changes effective 1 August 2008:

- Enhanced deduction increased from 150% to 175% (a 75% uplift rather than 50%)

- Payable credit rate reduced from 16% to 14%

- Large company rate also increased from 125% to 130%

For a loss-making SME, the effective cash benefit remained around 24.5p per £1 of qualifying spend — broadly similar to the pre-2008 position — but profitable SMEs gained more generous tax relief.

One change from 2008 still catches businesses out today. Far less publicised was the Finance Act 2008 provision reducing the claim window from six years to two years from the end of the accounting period, effective 31 March 2008. This rule remains in force. Businesses that discover R&D eligibility late — typically after a new accountant reviews their activity — often find that qualifying spend from earlier years is already out of time and cannot be recovered.

2009–2022: Gradual Expansion, RDEC's Arrival, and Growing Compliance Focus

Enhancement Rate Progression

Between 2009 and 2015, the SME scheme underwent five further rate increases, each announced in successive Budgets and typically effective from April of the announcement year:

| Effective Date | Enhanced Deduction | Additional Uplift | Payable Credit Rate |

|---|---|---|---|

| April 2011 | 200% | 100% | 12.5% |

| April 2012 | 225% | 125% | 11% |

| April 2014 | 225% | 125% | 14.5% |

| April 2015 | 230% | 130% | 14.5% |

The April 2015 rate of 230% enhancement and 14.5% payable credit represented the peak generosity of the SME scheme. For a loss-making company, this delivered approximately 33.35p cash back per £1 of qualifying spend — a powerful subsidy that positioned the UK among the most generous R&D tax regimes globally.

2012 Simplification Measures

On 1 April 2012, two significant administrative barriers were removed:

- The PAYE/NIC cap on payable credits was abolished, allowing companies to receive cash refunds regardless of their employee payroll size

- The £10,000 minimum spend threshold was eliminated entirely, opening access to micro-businesses with minimal R&D budgets

These changes sharply expanded the claimant pool, particularly among startups and early-stage technology companies with small teams and limited revenues.

RDEC: Introduction and Evolution

The Research and Development Expenditure Credit (RDEC) launched on 1 April 2013 as a replacement for the large company super-deduction scheme. Unlike the SME scheme's "below-the-line" additional deduction, RDEC operates as an "above-the-line" taxable expenditure credit — accounted for separately in profit-before-tax calculations.

RDEC rate progression:

| Effective Date | RDEC Rate |

|---|---|

| April 2013 | 10% |

| April 2015 | 11% |

| January 2018 | 12% |

| April 2020 | 13% |

The old large company super-deduction ran in parallel until April 2016, when it was abolished entirely and all large companies migrated to RDEC.

This structural difference mattered beyond administration. RDEC's above-the-line treatment gave companies clearer visibility in financial statements and aligned more closely with accounting standards — a distinction that would shape the government's later push toward a single unified scheme.

2019–2021: Compliance Tightening

By the late 2010s, claim volumes had surged alongside growing HMRC concerns about error and fraud. HMRC's September 2025 statistics show total annual relief rising from approximately £6.6 billion in 2020-21 to £7.6 billion in 2021-22.

Key compliance milestones:

- April 2019: CT600 corporation tax return and supporting computation became mandatory with every claim; HMRC began rejecting incomplete submissions

- 2019–2020: First major government consultations on preventing SME R&D abuse launched

- April 2021: PAYE/NIC cap reintroduced at £20,000 plus 300% of relevant PAYE and NIC liabilities — designed specifically to curb fraudulent contractor-heavy claims where companies claimed substantial credits while employing minimal UK staff

- November 2021: Government announced data and cloud computing costs would qualify from April 2023

The PAYE cap reintroduction directly addressed a documented problem. HMRC found approximately half of all SME claims were at least partly non-compliant, with common errors including ineligible subcontractor costs, misclassified activities, and inflated staff time allocations.

Between 2020 and 2022, multiple consultations explored redefining qualifying R&D, tightening overseas restrictions, and fundamentally restructuring the reliefs. The Autumn Statement 2022 signalled the outcome: a major rebalancing away from high SME cash subsidies toward a UK-employment-linked model and a "step toward a simplified, single RDEC-like scheme for all."

The 2023 Shake-Up: Rate Cuts, New Restrictions, and the R&D-Intensive SME Category

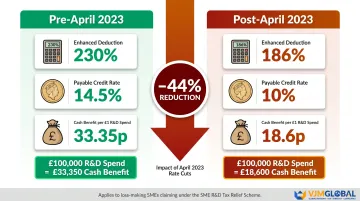

Rate Changes That Halved the Cash Benefit

From 1 April 2023, the SME scheme underwent its most dramatic rate reduction in history:

| Element | Pre-April 2023 | Post-April 2023 | Change |

|---|---|---|---|

| Enhanced deduction | 230% | 186% | -44 percentage points |

| Additional uplift | 130% | 86% | -44 percentage points |

| Payable credit rate | 14.5% | 10% | -4.5 percentage points |

Cash benefit impact for loss-making SMEs:

- Pre-April 2023: 14.5% × £2.30 = approximately 33.35p per £1 of qualifying spend

- Post-April 2023: 10% × £1.86 = approximately 18.6p per £1 of qualifying spend

This represented a 44% reduction in the effective cash subsidy — the single most impactful change in the scheme's 23-year history. For a startup claiming £100,000 in qualifying R&D expenditure, the cash benefit dropped from approximately £33,350 to £18,600.

Simultaneously, the RDEC rate increased from 13% to 20%, narrowing the gap between SME and large company relief. For profitable companies, the difference between routes became far less pronounced.

R&D-Intensive SME Category

To soften the blow for companies heavily invested in R&D (particularly life sciences, biotech, and deep-tech), the government introduced an R&D-intensive SME category from April 2023.

Companies where qualifying R&D expenditure represented at least 40% of total expenditure retained the higher 14.5% payable credit rate, delivering approximately 27p per £1 of qualifying spend. This threshold was later reduced to 30% from April 2024, widening access to more companies.

The R&D-intensive route is highly sector-specific. A pharmaceutical startup with minimal revenues but substantial lab costs easily meets the threshold; a profitable software consultancy rarely does.

New Qualifying Expenditure Categories

From April 2023, qualifying expenditure expanded to include:

- Data licences

- Cloud computing costs

- Pure mathematics

These changes reflected the modern reality of R&D delivery — cloud infrastructure and data access had become as fundamental to innovation as traditional lab equipment and consumables.

Overseas R&D Restrictions

Simultaneously, overseas R&D activities were restricted. From April 2024 (the implementation was delayed from the original April 2023 target), subcontractor and externally provided worker costs must relate to UK-based R&D unless narrow qualifying conditions are met:

- The conditions necessary for the R&D are not present in the UK

- The conditions are present at the overseas location

- It would be wholly unreasonable to replicate them in the UK

Cost savings and worker availability are explicitly excluded as justifications. A company cannot claim relief on overseas subcontractor fees simply because skilled developers are cheaper in Eastern Europe — the R&D itself must require the overseas location.

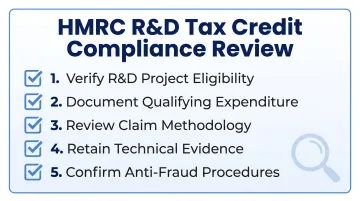

August 2023 Compliance Requirements

Beyond the overseas restrictions, HMRC also tightened the claims process itself. From 8 August 2023, every R&D claim must include:

Additional Information Form (AIF): A mandatory digital submission including:

- Detailed project descriptions broken down by qualifying activity

- Cost breakdowns by expenditure category (staff, subcontractors, consumables, etc.)

- Named senior officer endorsement (typically a director)

- Details of any adviser involved in preparing the claim

Advance Claim Notification: Companies that have not submitted an R&D claim in any of the previous three accounting periods must notify HMRC within six months of the period end. Miss this window and the claim is invalid, with no exceptions.

These requirements added considerable administrative burden but reflected HMRC's move to require documented evidence for every claim. Claims without valid AIFs are rejected outright.

Straddling Periods: A Practical Complexity

Companies with accounting periods crossing 1 April 2023 face a calculation challenge that catches many advisers off guard:

- Split qualifying R&D expenditure by financial year (pre and post 1 April 2023)

- Apply the appropriate enhancement rate to each portion (230% vs 186%)

- Recalculate trading losses for each part separately

- Apply the correct payable credit rate to each slice (14.5% vs 10%)

For a company with a 31 December 2023 year-end, this means apportioning costs across the 1 January to 31 March 2023 period (old rates) and the 1 April to 31 December 2023 period (new rates). The calculation complexity multiplies if the company also qualifies as R&D-intensive for part of the period.

2024 and Beyond: The Merged Scheme, ERIS, and What It Means for SMEs Today

The Merged R&D Scheme

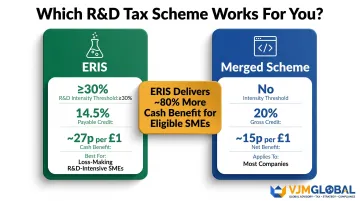

For accounting periods beginning on or after 1 April 2024, most companies claim under a single merged RDEC-style scheme. The structural distinction between SME and large company routes has been abolished for the majority of claimants.

Merged scheme mechanics:

- Taxable expenditure credit applied above the tax line

- Credit rate: 20% (gross)

- Net benefit after 25% corporation tax: 15p per £1 of qualifying spend for profitable companies

- Payable credit available for loss-making companies, subject to PAYE cap

The merged scheme brings the UK in line with international practice. Most OECD countries operate volume-based tax credits rather than enhancement-based deductions, and the new structure simplifies financial reporting by making R&D support visible in profit-before-tax figures.

Enhanced R&D Intensive Support (ERIS)

Loss-making SMEs meeting the R&D intensity threshold retain access to ERIS (Enhanced R&D Intensive Support), a separate track offering more generous relief:

| Feature | ERIS | Merged Scheme |

|---|---|---|

| Qualifying threshold | R&D ≥ 30% of total expenditure | None |

| Enhanced deduction | 86% additional (186% total) | None (uses 20% credit instead) |

| Payable credit rate | 14.5% | Effective 15% (net of tax) |

| Effective cash benefit | Approximately 27p per £1 | Approximately 15p per £1 |

ERIS delivers approximately 80% more cash benefit per pound of qualifying spend compared to the merged scheme for loss-making companies. The one-year grace period allows companies that dip below the 30% threshold in a single year to continue claiming ERIS, provided they met the test in the previous year.

PAYE cap applies to both routes: The maximum payable credit remains £20,000 plus 300% of relevant PAYE and NIC liabilities. Exemptions exist for companies whose employees create or manage IP and whose connected-party subcontracting is below 15% of total R&D expenditure.

Autumn Budget 2024: Rate Stability Commitment

Understanding the relief rates matters more now that the government has committed to keeping them unchanged. The Corporate Tax Roadmap published on 30 October 2024 confirmed that merged scheme and ERIS rates will be maintained for the duration of this parliament. The government stated it is "committed to the current structure of the R&D tax relief system" and will maintain the generosity of R&D reliefs.

After years of near-constant reform, this is a meaningful shift. For the first time in over a decade, companies can build multi-year R&D investment plans around relief rates that are unlikely to change mid-cycle.

Current Documentation Expectations

HMRC's updated guidance on "How to identify qualifying R&D activities" (published 23 January 2025) emphasises evidence-led compliance:

- Well-evidenced project narratives demonstrating uncertainty and advance in science/technology

- Contemporaneous cost attribution records linking expenditure to specific projects

- Technical justification showing why the work required resolving scientific or technological uncertainty

- Documentation of the baseline knowledge state and the specific advance achieved

The compliance approach has shifted away from accepting broad-brush claims toward requiring granular, project-level evidence. Companies should maintain R&D logs, technical meeting notes, and cost tracking systems throughout the accounting period — reconstructing evidence after the fact rarely satisfies HMRC scrutiny.

What This Means for UK SMEs Claiming Today

For claims relating to accounting periods beginning on or after 1 April 2024:

- Determine your route: Most companies claim under the merged scheme at 20%; loss-making SMEs where R&D spend ≥ 30% of total expenditure can access ERIS at 14.5%

- Complete the AIF accurately: Every claim requires a valid Additional Information Form with project descriptions and cost breakdowns

- Check the claim notification requirement: First-time claimants or companies returning after a three-year gap must notify HMRC within six months of period end

- Review overseas costs: Subcontractor and EPW costs must relate to UK-based R&D unless narrow qualifying conditions apply

- Build contemporaneous evidence: HMRC expects project-level documentation created during the R&D work, not retrospective narratives

Period-Straddling Calculations

Companies with accounting periods crossing 1 April 2023 or 1 April 2024 face some of the trickiest calculations in the current regime:

- Expenditure must be apportioned by financial year

- Different rates apply to each portion of the period

- Losses must be recalculated separately for each segment

Errors here are common and can be costly.

For companies claiming across multiple transition dates, the interaction of old and new rules adds another layer of complexity. Specialist tax advisory support is not just helpful at this stage — for many SMEs, it is the difference between a successful claim and a compliance failure.

Frequently Asked Questions

What is the SME R&D tax credit?

The SME R&D tax credit is a UK government incentive that lets qualifying small and medium-sized enterprises claim enhanced tax relief or a payable cash credit on eligible R&D expenditure. From April 2024, most companies claim under the merged RDEC-style scheme at 20%, while R&D-intensive loss-making SMEs access ERIS at 14.5%.

How many years back can you claim R&D tax credits in the UK?

Since March 2008, the time limit for making an R&D tax credit claim is two years from the end of the relevant accounting period, reduced from the original six-year window. Any missed or late-identified qualifying activity can only be recovered within that two-year period.

What changed about the R&D tax credit in 2026 in the UK?

By 2026, the merged scheme introduced in April 2024 is fully operational, with greater emphasis on contemporaneous documentation. The Autumn Budget 2024 confirmed existing ERIS and merged scheme rates, with no structural reforms announced for 2025-26.

When was RDEC introduced in the UK?

RDEC (Research and Development Expenditure Credit) was introduced in April 2013 at a starting rate of 10%, replacing the large company super-deduction scheme. It operates as an above-the-line credit and underpins the merged scheme that applies to most companies from April 2024.

When did R&D tax credits start in the UK?

R&D tax credits for SMEs launched on 1 April 2000 under Chancellor Gordon Brown, offering a 150% enhanced deduction on qualifying expenditure. A separate large company scheme followed in April 2002 at 125% enhancement.