Introduction

The UK starts taxing you the moment you earn UK-source income — even if you never set foot in the country. Non-resident investors who buy UK property, receive dividends from British companies, or operate through a UK branch quickly discover that HMRC's reach extends well beyond the UK's borders.

Your UK tax obligations depend on your residency status, the type of income earned, and how your business is structured. The Statutory Residence Test determines your tax scope. Choosing between a branch and a subsidiary carries distinct compliance requirements — and the wrong choice can be expensive to unwind.

This guide covers:

- How UK tax residency is determined under the Statutory Residence Test

- Key taxes for foreign investors: income tax, corporation tax, capital gains tax, and VAT

- Structural decisions between UK branches and subsidiaries

- Corporate compliance obligations, including CT600 filings and transfer pricing rules

- How double taxation agreements can reduce your overall liability

Key Takeaways

- UK taxes foreign investors on UK-source income regardless of home country residence

- The Statutory Residence Test — including the 183-day automatic residence rule — determines your tax scope

- Branch vs. subsidiary structures each carry distinct tax implications for foreign businesses

- CT600 and VAT filing deadlines are strict, with automatic penalties for late submission

- Double taxation agreements with 157+ countries can reduce your overall UK tax liability

Who Qualifies as a Foreign Investor Under UK Tax Law

In UK tax terms, "foreign investor" covers several distinct categories, each triggering different compliance obligations:

- Non-resident individuals investing in UK assets (property, shares, funds)

- Foreign companies trading in the UK without formal incorporation

- Overseas entities with a UK permanent establishment

The category you fall into determines which taxes apply, what returns you must file, and which reliefs you can claim. A US citizen purchasing London rental property faces different obligations than a German company opening a UK sales office. The category you fall into determines which taxes apply, what returns you must file, and which reliefs you can claim. A US citizen purchasing London rental property faces different obligations than a German company opening a UK sales office. The first question to resolve for individuals is UK tax residence — and for companies, whether a permanent establishment exists.

Determining UK Tax Residence: The Statutory Residence Test (SRT)

HMRC uses the Statutory Residence Test to determine an individual's UK tax residence status. The framework operates through three tiers:

Automatic UK residence applies if you:

- Spend 183 days or more in the UK during a tax year (6 April to 5 April)

- Have your only home in the UK for 91+ days

- Work full-time in the UK for any period of 365 days

Automatic non-residence applies if you:

- Spend fewer than 16 days in the UK (if UK resident in one or more of the previous three tax years)

- Spend fewer than 46 days in the UK (if not UK resident in any of the previous three tax years)

- Work full-time overseas with fewer than 91 UK days and fewer than 31 UK work days

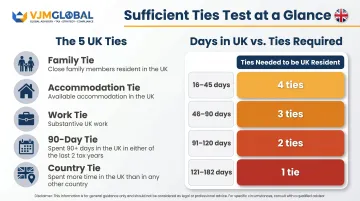

The "sufficient ties" test applies to individuals who fall between these automatic tests. Five potential UK ties exist:

- Family tie – spouse, civil partner, or minor children resident in the UK

- Accommodation tie – available UK accommodation used for 1+ night

- Work tie – 40+ UK work days (3+ hours per day)

- 90-day tie – 90+ UK days in either of the two prior tax years

- Country tie – more UK days than any other single country (applies only if previously UK resident)

Days in the UK and number of ties work together to determine residence status. For someone previously UK resident, even a single tie combined with over 120 UK days is enough to trigger UK residence — a threshold that catches many investors who consider themselves non-resident.

Permanent Establishment for Foreign Companies

"Permanent establishment" (PE) is defined in sections 1141 and 1142 of the Corporation Tax Act 2010 as a fixed UK place of business through which a foreign company carries on business.

What creates a PE:

- Branch office or factory

- Sales office with decision-making authority

- Dependent agent habitually exercising authority to conclude contracts in the UK

What does not create a PE:

- Selling to UK customers from overseas without a UK presence

- An independent agent acting in the ordinary course of business

Storage, display, or purchasing facilities are also excluded under section 1143 CTA 2010 as preparatory or auxiliary activities.

Trading in the UK via a PE triggers corporation tax liability on UK-activity profits. Trading with UK customers from overseas typically does not.

Key UK Taxes That Apply to Foreign Investors

UK Income Tax for Non-Residents

Non-resident individuals are taxed only on UK-source income, which includes:

- Rental income from UK property

- Dividends from UK companies

- UK employment income

- Interest from UK banks (though often exempt or subject to reduced withholding)

Tax rates for 2025/26:

| Income Type | Basic Rate (£12,571–£50,270) | Higher Rate (£50,271–£125,140) | Additional Rate (£125,140+) |

|---|---|---|---|

| Rental income | 20% | 40% | 45% |

| Dividend income | 8.75% | 33.75% | 39.35% |

| Savings income | 20% | 40% | 45% |

The standard Personal Allowance of £12,570 is available to eligible non-residents, including British citizens, EEA citizens, or where a double taxation agreement includes the allowance.

Important change from April 2027: Separate property income tax rates will apply: 22% (basic), 42% (higher), 47% (additional). Dividend and savings rates will also increase by 2 percentage points.

Beyond income tax, foreign investors disposing of UK property face a separate — and time-sensitive — compliance obligation under CGT rules.

Capital Gains Tax (CGT) for Foreign Investors

Since April 2019, non-residents are liable for CGT on:

- All UK residential property

- UK commercial property

- Indirect disposals of UK property-rich companies (where 75%+ of gross asset value comes from UK land)

CGT rates for 2025/26:

| Asset Type | Basic Rate | Higher Rate |

|---|---|---|

| Residential property | 18% | 24% |

| Commercial property | 18% | 24% |

The annual exempt amount is £3,000 for 2025/26.

Critical compliance requirement: Non-residents must report and pay CGT within 60 days of completion (for disposals on or after 27 October 2021), even with no tax due or a realised loss. This reporting window is shorter than the standard Self Assessment deadline.

Corporation Tax for Foreign Entities

Overseas companies with a UK permanent establishment are liable for UK corporation tax on profits attributable to their UK activities.

Corporation tax rates (2025/26 and 2026/27):

| Profit Band | Rate |

|---|---|

| Up to £50,000 | 19% (small profits rate) |

| £50,001–£250,000 | 19%–25% (marginal relief applies) |

| Over £250,000 | 25% (main rate) |

These thresholds are reduced proportionally where a company has associated companies. The marginal relief fraction is 3/200.

Stamp Duty Land Tax (SDLT) for Property Purchases

SDLT applies to all UK land and property purchases. Since 1 April 2021, a 2% non-resident surcharge applies on top of standard residential rates for non-UK resident buyers.

Standard residential SDLT rates (from 1 April 2025):

| Property Value Band | Standard Rate | Additional Dwelling Rate | Non-Resident Surcharge | Total for Non-Resident Second Home |

|---|---|---|---|---|

| Up to £125,000 | 0% | +5% | +2% | 7% |

| £125,001–£250,000 | 2% | +5% | +2% | 9% |

| £250,001–£925,000 | 5% | +5% | +2% | 12% |

| £925,001–£1,500,000 | 10% | +5% | +2% | 17% |

| Above £1,500,000 | 12% | +5% | +2% | 19% |

The non-resident surcharge does not apply to non-residential/commercial property purchases.

Inheritance Tax (IHT) Exposure

From 6 April 2025, IHT liability is determined by the "long-term UK resident" test, replacing the previous domicile-based rules.

Key provisions:

- An individual is in scope for worldwide IHT once UK-resident for 10 out of the last 20 tax years

- After departure, individuals remain in scope for 3 to 10 years (the "tail" increases by one year for each additional year of UK residence, up to a maximum 10-year tail)

- The standard nil-rate band is £325,000; the residence nil-rate band is £175,000 (for qualifying homes passed to direct descendants)

Foreign Income and Gains (FIG) Regime

Newly UK-resident individuals — those not UK-resident in any of the prior 10 consecutive tax years — pay no UK tax on foreign income and gains for their first 4 years of tax residence. This makes the FIG regime a practical consideration for investors planning a UK move.

Branch vs. Subsidiary: Choosing Your UK Business Structure

Foreign companies operating in the UK must choose between establishing a branch (UK branch of an overseas company) or a subsidiary (UK-incorporated private limited company). The decision directly affects your tax exposure, liability protection, and the cost of eventually exiting the UK market.

Branches: How They Are Taxed and Regulated

A UK branch has no separate legal personality from its overseas parent. Key characteristics:

Tax treatment:

- Subject to UK corporation tax only on UK branch profits (not worldwide profits)

- Losses may potentially be offset against the overseas parent's profits (subject to the parent's home country tax law)

- Interest and royalty payments from the branch to the parent are generally not deductible against UK taxable profits (treated as intra-company transfers)

Compliance obligations:

- Must register with Companies House under the Overseas Companies Regulations 2009

- Must file the parent company's audited accounts (if required to prepare accounts under parent-country law) with Companies House for public inspection

- No UK statutory audit requirement for the branch itself

- CT600 filing deadline is 13 months after the end of the accounting period (one month longer than for UK companies)

Subsidiaries: How They Are Taxed and Regulated

A UK subsidiary is a separate legal entity incorporated in the UK. Key characteristics:

Tax treatment:

- Subject to UK corporation tax on worldwide profits (not just UK-sourced profits)

- Profits are not taxed in the parent's hands until dividends are distributed

- Arm's-length interest and royalty payments to the overseas parent are generally deductible (subject to transfer pricing rules)

- Potential for group relief and other intra-group tax planning

Compliance obligations:

- Must file annual financial statements with Companies House (publicly available)

- May require a UK statutory audit if two of three thresholds are met (for financial years beginning on or after 6 April 2025): (1) turnover over £15 million, (2) balance sheet over £7.5 million, or (3) more than 50 employees

- CT600 filing deadline is 12 months after the end of the accounting period

The table below summarises how the two structures compare across the factors that matter most to foreign investors.

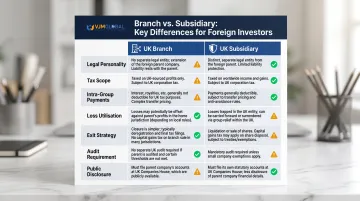

Branch vs. Subsidiary: Side-by-Side Comparison

| Factor | Branch | Subsidiary |

|---|---|---|

| Legal personality | Part of overseas company | Separate UK legal entity |

| Tax scope | UK-activity profits only | Worldwide profits |

| Intra-group payments | Generally not deductible | Deductible if arm's-length |

| Loss utilisation | May offset against parent (subject to parent's tax law) | UK losses only, unless group relief applies |

| Exit strategy | Asset disposal (may trigger UK CGT on individual assets) | Share disposal (generally no UK CGT unless property-rich) |

| Audit requirement | No UK statutory audit | Audit required if above thresholds |

| Public disclosure | Parent company's accounts filed | Subsidiary's accounts filed |

Exit consideration: A branch exit triggers UK CGT on individual asset disposals — each asset is assessed separately. Selling a subsidiary's shares is different: an overseas company typically owes no UK CGT on that disposal, unless the subsidiary is UK property-rich (meaning 75%+ of its gross asset value derives from UK land).

UK Corporate Tax Compliance: Returns, Payments, and Transfer Pricing

CT600 Corporation Tax Returns

All UK-resident companies and UK branches of foreign companies must file a CT600 corporation tax return annually:

- UK companies: 12 months after the end of the accounting period

- UK branches: 13 months after the end of the accounting period

Automatic late filing penalties:

| Timing | Penalty |

|---|---|

| 1 day late | £200 |

| 3 months late | Additional £200 |

| 6 months late | 10% of unpaid tax (HMRC issues tax determination) |

| 12 months late | Additional 10% of unpaid tax |

| Late 3 times in a row | £200 penalties increase to £1,000 each |

Payment deadlines:

- Small companies (taxable profits under £1.5 million): 9 months and 1 day after the end of the accounting period

- Large companies (annual taxable profits over £1.5 million, divided by number of associated companies + 1): quarterly instalment payments, which can accelerate tax payment by approximately 10 months

For a 12-month accounting period, quarterly instalments are due:

- 6 months and 13 days after the first day of the period

- 3 months later

- 3 months later

- 3 months and 14 days after the last day of the period

Capital Allowances and R&D Relief

Depreciation is not deductible for UK tax purposes. Instead, capital allowances apply:

Annual Investment Allowance (AIA): £1 million per 12-month accounting period (permanently set at this level since 1 January 2019)

Writing Down Allowance rates (changed 1 April 2026 for Corporation Tax):

- Main pool: 14% (reduced from 18%)

- Special rate pool: 6%

- Structures and buildings: 3%

R&D relief: For accounting periods beginning on or after 1 April 2024, the old RDEC and SME schemes are merged. The merged scheme provides an above-the-line expenditure credit at 20% of qualifying R&D costs.

Enhanced R&D Intensive Support (ERIS): For loss-making SMEs whose qualifying R&D expenditure is 30%+ of total expenditure, an enhanced credit rate of up to 27% applies.

Transfer Pricing Obligations

All related-party cross-border transactions (goods, services, loans, intangibles) must be priced at arm's length under TIOPA 2010 (Taxation (International and Other Provisions) Act 2010).

Key requirements:

- Transactions must reflect terms that independent parties would agree under comparable circumstances

- Contemporaneous documentation must support pricing decisions

- HMRC-recognised methods include: comparable uncontrolled price, cost-plus, resale price, transactional net margin, and profit split

Penalties for non-compliance:

- £3,000 annual penalty for inadequate transfer pricing records

- Up to 100% of additional tax due for inaccuracies

SME exemption: Small enterprises are exempt from UK transfer pricing rules for transactions with entities in DTA countries, provided they meet all three criteria:

- Fewer than 250 employees

- Annual turnover not exceeding €50 million, or

- Balance sheet total not exceeding €43 million

Foreign investors managing CT600 filings, instalment schedules, and transfer pricing documentation across jurisdictions often work with a specialist cross-border compliance firm. VJM Global's Chartered Accountants have supported 250+ UK businesses with these obligations over 30+ years of practice.

Company Residence and Dual Residency Risks

A company is UK-resident if:

- Incorporated in the UK, or

- Its central management and control (the highest strategic decision-making) is exercised in the UK

Dual-residence risk: A company may be regarded as resident in both its country of incorporation and the UK. Double Taxation Agreements typically include a "tie-breaker" clause (usually effective management and control) to determine single residence for treaty purposes. Dual residence can create unexpected tax liabilities and compliance burdens.

VAT and Employment Tax Obligations for Foreign Investors

UK VAT Registration

A foreign business with a taxable presence in the UK must register for VAT once its UK taxable turnover exceeds £90,000 over a rolling 12-month period (effective from 1 April 2024).

Key points:

- Voluntary registration is possible below the threshold and allows recovery of input tax on costs

- Registered businesses must file VAT returns (quarterly or monthly) via HMRC's Making Tax Digital (MTD) platform using compatible software

- HMRC generally disregards supplies between a UK branch and its overseas parent — both are the same legal entity

- Supplies between a UK subsidiary and its parent are subject to normal VAT rules (separate legal entities)

- Deregistration threshold is £88,000 (once turnover drops and remains below this level)

PAYE and National Insurance for Overseas Employers

Individuals working in the UK for more than 30 days are generally subject to UK PAYE withholding on their UK earnings. Overseas employers with a UK presence bear this withholding responsibility.

Under the STBV Agreement, employers from DTA countries can apply a lighter-touch PAYE approach for qualifying employees:

- Applies to employees expected to stay 183 days or fewer in a 12-month period

- PAYE withholding can be disregarded if the UK entity will not ultimately bear the remuneration cost

- Removes PAYE obligation for qualifying short-term visitors

The Appendix 8 Special Arrangement applies to shorter visits:

- Covers employees working in the UK for 60 days or fewer

- Employers report and pay PAYE by 31 May following the tax year end

Employer Pension Auto-Enrolment Obligations

Beyond payroll withholding, UK employers also carry pension obligations for their workforce. Foreign businesses with UK employees must auto-enrol eligible staff into a qualifying pension scheme and meet minimum contribution requirements.

Minimum contribution rates:

- Employer contribution: 3% of qualifying earnings

- Total contribution: 8% of qualifying earnings (employee contributes remaining 5%)

Earnings thresholds for 2026/27:

- Earnings trigger: £10,000 per year

- Lower limit of qualifying earnings: £6,240 per year

- Upper limit of qualifying earnings: £50,270 per year

Double Taxation Agreements: Reducing Your UK Tax Burden

What DTAs Do (and Don't Do)

The UK has approximately 157 tax treaties in force — one of the world's largest DTA networks. DTAs:

DTAs allocate rights and reduce tax by:

- Assigning taxing rights between countries (for example, employment income taxed where you work vs. where you reside)

- Preventing double taxation through foreign tax credits or income exemptions

- Reducing withholding tax rates on cross-border dividends, interest, and royalties

- Applying "tie-breaker" clauses to resolve dual-residence conflicts

DTAs do not override UK domestic law:

- UK residence rules still apply — you remain UK-resident if you meet the Statutory Residence Test

- Self Assessment filing obligations and reporting requirements remain in force

- Deadlines and penalties apply regardless of treaty status

Foreign Tax Credits in Practice

A UK-resident foreign investor who has already paid tax in their home country on the same income can generally claim a foreign tax credit against their UK tax liability under TIOPA 2010.

How it works:

- The credit is limited to the lower of the UK tax and the foreign tax on that income

- Pay 30% overseas on dividends (UK rate: 33.75%) → credit capped at 30%, leaving 3.75% UK tax due

- Pay 15% overseas (UK rate: 33.75%) → 15% credit applied, 18.75% UK tax remains

Check whether your country has a UK DTA and verify coverage for your specific income type — salary, dividends, property income, and pension articles each operate differently within the same treaty.

Understanding your credit entitlement is the first step; the next is ensuring you meet UK filing requirements to claim it.

Self-Assessment Filing for Individual Foreign Investors

Non-resident individuals with UK-source income generally need to file a UK Self Assessment tax return by 31 January following the tax year (which runs 6 April to 5 April).

Forms:

- P85 – for individuals leaving the UK (to claim tax refunds and notify departure)

- P86 – for individuals arriving in the UK

Automatic late filing and payment penalties:

| Timing | Penalty |

|---|---|

| Immediately after deadline | £100 |

| After 3 months | £10/day for up to 90 days (max £900) |

| After 6 months | 5% of tax due or £300, whichever is greater |

| After 12 months | Further 5% of tax due or £300, whichever is greater |

60-day property reporting: Non-residents must report UK property disposals within 60 days of completion, even if no CGT is due. This deadline is separate from — and independent of — the annual Self Assessment return.

Frequently Asked Questions

Do foreign investors pay tax in the UK?

Yes, foreign investors are subject to UK tax on UK-source income and gains, including rental income from UK property, dividends from UK companies, and capital gains on UK property. Foreign companies trading in the UK through a permanent establishment are subject to UK corporation tax on the profits attributable to their UK activities.

What is the 90% rule for non-residents?

The "90% rule" allows non-UK residents to claim the UK personal income tax allowance if at least 90% of their total worldwide income is UK-sourced — making it difficult for most non-residents with significant overseas earnings to qualify. British and EEA citizens, along with certain DTA provisions, can claim the Personal Allowance regardless of this test.

What is a permanent establishment, and when does a foreign company create one in the UK?

A permanent establishment (PE) is a fixed place of business — such as a branch, office, or factory — or a dependent agent through which a foreign company conducts UK business, triggering corporation tax on UK-attributable profits. Merely selling to UK customers or undertaking preparatory or support activities (storage, display, purchasing) typically does not create a PE.

What is the difference between a branch and a subsidiary for UK tax purposes?

A branch is legally part of the overseas company and is taxed only on UK-activity profits, while a subsidiary is a separate UK-incorporated entity taxed on its worldwide profits. Key differences affect intra-group payment deductibility, exit strategy (asset vs. share disposal), audit obligations, and loss utilisation — all of which should be weighed before choosing a structure.

How does the UK's double taxation agreement network benefit foreign investors?

The UK's extensive DTA network (covering approximately 157 jurisdictions) can reduce or eliminate withholding taxes on cross-border dividends, interest, and royalties, and provides mechanisms for foreign tax credits to avoid being taxed on the same income twice. However, DTAs do not remove UK reporting obligations or override UK domestic residence rules.

What UK taxes apply to a foreign investor who purchases UK property?

A non-UK resident purchasing UK property faces three main tax exposures:

- SDLT: Includes a 2% non-resident surcharge (total 7% on the first £125,000 for additional residential dwellings)

- Income tax: Applies to any rental income earned from the property

- Capital Gains Tax: Charged at 18% or 24% on disposal, depending on income level

Residential property gains must be reported to HMRC within 60 days of completing the sale.