This article explains what UK DTAs are, how they allocate taxing rights across income types like employment income, dividends, and pensions, which countries have signed treaties with the UK, how to determine your tax residency, and how to claim relief step-by-step. You'll get practical guidance, not just theory.

Key Takeaways

- UK DTAs prevent double taxation by allocating taxing rights and providing credit or exemption methods

- Three relief methods: exemption, foreign tax credit, and reduced withholding rates at source

- UK-India DTA caps withholding rates at 10%–15% across dividends, interest, and royalties

- Relief eligibility hinges on residency status — confirmed via the Statutory Residence Test and DTA tie-breaker rules

- Claim relief using HMRC's country-specific forms or SA106 foreign pages on your tax return

What Are UK Double Taxation Agreements and Why Do They Matter?

A UK Double Taxation Agreement (DTA) is a bilateral treaty between the UK and another country that determines which nation has the right to tax specific types of income, and to what extent. Under the Taxation (International and Other Provisions) Act 2010 (TIOPA 2010), DTAs take precedence over UK domestic tax rules in most cases—an important override that protects taxpayers from conflicting claims.

Without a treaty, a UK resident earning rental income in India could face tax in both jurisdictions with no mechanism for relief—paying tax twice on the same income. DTAs exist to prevent exactly that. One important point to understand, though: DTAs do not automatically eliminate tax in one country. They offset the tax paid in one country against the liability in another, so you pay the higher of the two rates, not zero tax. DTAs coordinate taxing rights; they don't create tax holidays.

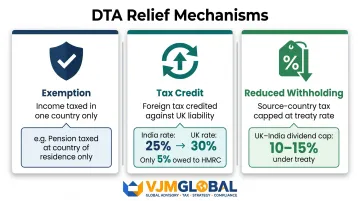

Three Relief Mechanisms

UK DTAs use three distinct mechanisms:

- Exemption – Income is only taxable in one country (usually the residence country). Example: Pension income taxed only where you live.

- Tax credit – Tax paid abroad is credited against your UK liability. For instance, if you pay 25% tax in India on consultancy income and the UK rate is 30%, you owe only an additional 5% to HMRC.

- Reduced withholding rates – Source-country tax is capped at a treaty rate for dividends, interest, and royalties. The UK-India DTA, for example, caps dividend withholding at 10–15% rather than India's standard domestic rate.

How UK DTAs Allocate Taxing Rights Across Key Income Types

Employment Income: The 183-Day Rule

Employment income is generally taxed where the work is physically performed. If you're a UK employee seconded to India for 10 months, your salary would typically be taxable in India.

However, the 183-day exception changes this. Under Article 15(2) of most UK DTAs, employment income remains taxable only in your home country if all three conditions are met:

- You're present in the other country for fewer than 183 days in the relevant period (either the tax year or a rolling 12 months, depending on the specific treaty)

- Your employer is not resident in the other country

- The salary costs are not borne by a permanent establishment in that country

Example: A UK employee on short-term secondment to India for 120 days, paid by a UK-based employer with no Indian permanent establishment, would owe tax only to the UK—not India.

Note that measurement periods differ by treaty: the UK-India DTA counts 183 days within the tax year, while treaties like the UK-Norway agreement use a rolling 12-month period — a meaningfully stricter test.

Dividends, Interest, and Royalties

DTAs typically cap source-country withholding tax on passive income. The UK-India DTA sets the following rates:

| Income Type | Rate | Conditions |

|---|---|---|

| Dividends | 10% | Standard dividends |

| Dividends | 15% | Paid from immovable property income via qualifying investment vehicle |

| Interest | 0% | Paid to government or approved financial institutions |

| Interest | 10% | Paid to a bank |

| Interest | 15% | All other cases |

| Royalties/FTS | 10%/15% | Depends on category and nature of services |

Note: Unlike many treaties, the UK-India DTA dividend rates are not tiered by ownership percentage. The 15% tier applies specifically to dividends from immovable property investment vehicles, not to substantial shareholdings.

Pensions

Under most UK DTAs, regular pension income is taxable only in the country of residence. If you retire to Spain after working 30 years in the UK, Spain taxes your UK pension — not the UK.

Lump sum risk: The UK's 25% tax-free pension commencement lump sum (PCLS) is a feature of UK domestic law. HMRC confirms the 25% PCLS is not automatically protected under most DTAs. If you're tax resident in France when you withdraw the lump sum, France may tax the full 100% even though the UK would have exempted 25%.

Key exception: The US-UK DTA explicitly protects the 25% PCLS. If you're a US resident receiving a UK pension, the exemption applies in both countries.

Capital Gains

Unlike employment income or pensions, capital gains rules turn primarily on asset type rather than residence alone. Gains on most assets are taxable only in the country of residence — but immovable property (real estate) is taxable where the property sits.

Two contrasting scenarios under the UK-India DTA illustrate this:

- A UK resident selling shares in an Indian company: the UK holds primary taxing rights

- A UK resident selling an apartment in Mumbai: India can tax the gain

One point that catches many people off-guard: DTAs determine which country has primary taxing rights, but they do not remove your reporting obligations. You still report gains to both tax authorities.

Countries With a Double Taxation Agreement With the UK

The UK maintains DTAs with around 120 countries, making it one of the world's most extensive treaty networks. Major partners include:

USA, India, Australia, Canada, Germany, France, UAE, Singapore, Japan, South Africa, and all EU member states.

For the authoritative and complete list, consult HMRC's tax treaties collection.

UK-India DTA

The UK-India DTA (1993 Convention, amended by the 2013 Protocol) is especially relevant for NRIs, UK-based companies with India operations, and Indian professionals working in the UK. It covers:

- Employment income (183-day rule)

- Dividends, interest, royalties (reduced rates)

- Pensions

- Capital gains

VJM Global works with UK businesses establishing operations in India and NRIs managing cross-border income to navigate the UK-India DTA. Our team handles India-side tax compliance, residency rules, and treaty relief claims so you're not over-taxed in either jurisdiction.

Brexit and EU Treaties

Post-Brexit, all bilateral UK DTAs with EU countries remain fully in force. These agreements were not affected by the UK's departure from the EU—no renegotiation was required. UK businesses trading with EU-based entities can still rely on the same treaty protections for withholding tax rates, permanent establishment rules, and relief claims that applied before Brexit.

Determining Tax Residency Under UK DTAs

Tax residency is the foundational step before any DTA can be applied. Residency determines which country has the right to tax your worldwide income.

UK Statutory Residence Test (SRT)

In the UK, HMRC uses the Statutory Residence Test (SRT), introduced by Finance Act 2013. The test has three stages:

Stage 1 – Automatic Overseas Tests

You're automatically non-resident if you meet any of these:

- Previously UK-resident and spend fewer than 16 days in the UK

- Not previously UK-resident and spend fewer than 46 days

- Work full-time abroad (35+ hours/week) with fewer than 91 UK days

Stage 2 – Automatic UK Tests

You're automatically UK-resident if you meet any of these:

- Spend 183 days or more in the UK

- Have a UK home for 91+ consecutive days (with 30+ days spent there) and no overseas home

- Work full-time in the UK

Stage 3 – Sufficient Ties Test

If neither automatic test applies, residency depends on how many of these five ties you have:

- Family – Spouse or minor children in the UK

- Accommodation – UK property available 91+ days

- Work – 40+ UK work days

- 90-day – 90+ days in the UK in either of two prior tax years

- Country – More days in the UK than any other single country

The number of ties needed varies by days spent in the UK and prior residence status.

Passing all three SRT stages resolves most residency questions—but some individuals still end up resident in two countries at once.

Dual Residency and DTA Tie-Breaker Rules

Under each country's domestic rules, dual residency is possible. When it occurs, the DTA's tie-breaker rules apply in this order:

- Permanent home – Resident where permanent home is available

- Centre of vital interests – Closer personal and economic relations

- Habitual abode – Where you habitually live

- Nationality – State of which you're a national

- Mutual agreement – Tax authorities settle by agreement

Residency vs. Domicile

These two concepts are often confused but govern entirely separate tax obligations:

- Tax residency (determined by SRT) governs liability to UK income tax and capital gains tax on worldwide income for that tax year.

- Domicile refers to the country you consider your permanent home. From 6 April 2025, the UK replaced its domicile-based inheritance tax rules with a residence-based system — the "10 out of 20 year" rule. Anyone UK-resident for 10 of the preceding 20 tax years becomes liable to UK inheritance tax on worldwide assets.

When assessing DTA applicability, confirm both statuses. Getting one right while overlooking the other can lead to unexpected tax exposure.

How to Claim DTA Tax Relief in the UK: Step-by-Step

Step 1 – Establish Residency

Confirm tax residency in both countries using each country's domestic rules (e.g., SRT for the UK) before claiming any treaty benefit. If you're dual-resident, apply the DTA tie-breaker rules.

Step 2 – Identify the Applicable DTA and Income Type

Locate the correct DTA on HMRC's government website and identify which article covers your income:

- Article 15 – Employment income

- Article 10 – Dividends

- Article 11 – Interest

- Article 12 – Royalties

- Article 18 – Pensions

The relevant article specifies which country has taxing rights and any applicable rate caps or exemptions.

Step 3 – File the Correct Claim Form

For relief at source (before tax is deducted), use:

- Country-specific forms: HMRC has dedicated DTA claim forms for Australia, Canada, France, Germany, Ireland, USA, and others

- Standard form: Form DT-Individual for treaty partners without a dedicated form

Process:

- Complete the form with personal details and UK income details

- Send to your country of residence's tax authority for certification

- Submit certified form to HMRC Personal Tax International

- If approved, HMRC may issue an NT (No Tax) code to the UK payer

Step 4 – Claim Relief on Your Tax Return

For UK residents paying foreign tax on income also taxable in the UK, relief is claimed on the self-assessment return using:

- Form SA106 (Foreign supplementary pages)

- Foreign Tax Credit Relief, capped at the lower of the foreign tax paid or the UK tax attributable to that income

Example: Income taxed at 25% in India, UK rate 30%: you claim a £250 credit for every £1,000 earned, paying only an additional £50 to HMRC.

Alternatively, you can claim deduction relief, treating foreign tax as an expense (useful if your income is below the UK tax threshold).

What If No DTA Exists Between the UK and Another Country?

If no DTA exists, the UK's domestic unilateral relief provisions may still apply. Under TIOPA 2010 s.18, a UK resident who has paid tax on foreign income can claim a credit for the foreign tax paid against their UK liability—even without a formal treaty.

Key limitation: Unilateral relief is less generous than treaty relief:

- Covers credit only — exemptions and reduced withholding rates at source are not available

- Applies only where the foreign tax corresponds to UK income tax, corporation tax, or capital gains tax

- Available to UK residents only; non-residents cannot claim it

For businesses with cross-border operations in non-treaty countries, the cost gap is real. A UK company receiving dividends from a country with no DTA faces the full domestic withholding rate, with no reduced treaty alternative available — just a credit applied against the UK liability.

Frequently Asked Questions

Which countries have a double tax agreement with the UK?

The UK has DTAs with around 120 countries, including the USA, India, Australia, Canada, Germany, France, UAE, and Singapore. For the complete and up-to-date list, visit HMRC's official tax treaties page.

Is there a double tax treaty between the UK and the USA?

Yes. The US-UK DTA (signed in 2001) covers employment income, dividends, interest, royalties, pensions, and capital gains. US citizens should note that the saving clause preserves the US right to tax worldwide income regardless of the treaty, though foreign tax credits can offset double taxation.

How can I avoid double taxation in the UK?

Three main routes:

- Claim a foreign tax credit on your UK self-assessment return for tax already paid abroad

- Apply for an exemption under the relevant DTA article where income is only taxable in the other country

- Claim reduced withholding tax rates at source under treaty provisions

Do I have to pay UK tax on US income?

If you're a UK tax resident, you're generally taxable in the UK on worldwide income—including US income. However, the US-UK DTA typically allows you to offset US tax already paid against your UK liability, so you pay the higher of the two rates rather than both in full.

How can a US citizen avoid double taxation between the US and the UK?

US citizens primarily use the Foreign Tax Credit (Form 1116) to offset UK taxes paid against their US liability. The Foreign Earned Income Exclusion (Form 2555) may also apply for employment income. The US-UK DTA provides additional relief provisions for pensions, dividends, and interest income specifically.

Need help navigating the UK-India DTA? VJM Global's international tax team assists UK businesses and NRIs with India-side compliance, residency determination, and treaty relief claims. Contact us at info@vjmglobal.com or call +91 9213397070.