Introduction

Picture this: a UK company charges its Indian subsidiary a £500,000 annual management fee for shared services. HMRC opens an enquiry. The company has no intercompany agreement, no functional analysis, and no benchmarking study. The result? A potential upward adjustment, tax-geared penalties, and years of costly dispute resolution.

This isn't a rare edge case. Mid-market groups with cross-border structures face exactly this exposure — often without realising it.

Understanding the rules is the first line of defence. UK transfer pricing sits in Part 4 of the Taxation (International and Other Provisions) Act 2010 (TIOPA 2010), grounded in the OECD arm's length principle. The regime is self-assessed: taxpayers confirm their intragroup pricing meets the arm's length standard in their corporation tax return, or make an upward adjustment. The compliance burden falls entirely on the taxpayer — not HMRC.

This guide covers:

- Who the rules apply to and common exemptions

- How to select the right transfer pricing methodology

- What documentation HMRC actually expects

- The rule changes taking effect in 2026 and 2027

Key Takeaways

- UK transfer pricing applies to all connected-party transactions where a participation condition is met, including smaller groups

- The arm's length principle is the central test: prices between related parties must match what independent parties would agree

- Groups with consolidated revenues above €750 million must maintain a formal Master File and Local File under SI 2023/818

- SMEs currently retain their exemption, confirmed in the November 2025 consultation response (threshold: under 250 employees and under €50m turnover or €43m assets)

- Penalties range from a £3,000 fixed fine to 100% of potential lost revenue for deliberate, concealed errors

What Are UK Transfer Pricing Rules and Who Do They Apply To?

The Participation Condition

UK transfer pricing rules apply where two conditions are met: the actual provision between parties differs from the arm's length provision, and the participation condition is satisfied. Under TIOPA 2010 Part 4, the participation condition is met where one person directly or indirectly participates in the management, control, or capital of the other — or the same third party participates in both.

This is broader than most businesses assume. It covers:

- Consolidated corporate groups (parent-subsidiary)

- Joint ventures where common control exists

- Intercompany financing arrangements

- Certain aggregated rights and familial ownership scenarios

Entities within scope include UK-resident companies, UK permanent establishments of overseas companies, and UK-filing partnerships or trusts where the relevant UK tax computation is affected.

Asymmetric Adjustments: Upward Only

The UK regime operates asymmetrically. Under TIOPA s147, adjustments are made only where the actual provision creates a UK tax advantage. Upward adjustments (increasing UK taxable profits) are required in the self-assessment return.

Downward adjustments are not unilaterally available — the disadvantaged party must claim relief separately under the compensating adjustment rules. In practice, a UK company that has undercharged a foreign affiliate cannot simply reduce its taxable profits without HMRC agreement.

Changes From 1 January 2026

Two significant scope changes take effect for chargeable periods beginning on or after 1 January 2026:

- Broadened participation condition — new provisions extend the condition to include additional connected-party scenarios, including a transfer pricing notice mechanism where HMRC directs that a participatory relationship exists

- UK-to-UK exemption — transactions between UK tax-resident companies within the scope of UK corporation tax will broadly be exempt from transfer pricing, which reduces compliance complexity for purely domestic intragroup transactions

The UK-to-UK exemption is not absolute. Exclusions apply to ring-fenced trades, patent box elections, qualifying asset holding companies (QAHCs), and banks. Groups should retest their connected-party maps (their internal record of related-party relationships) before the first 2026 period.

The Arm's Length Principle and Transfer Pricing Methods

What the Arm's Length Standard Requires

The arm's length price is what two independent, unrelated parties would agree to under comparable conditions in the open market. TIOPA s164, as clarified by HMRC INTM414120, requires UK interpretation of this principle to be consistent with Article 9 of the OECD Model Tax Convention and the OECD Transfer Pricing Guidelines (2022 edition). The OECD Guidelines are directly referenced in UK legislation — they are not merely persuasive.

The Five Accepted Methods

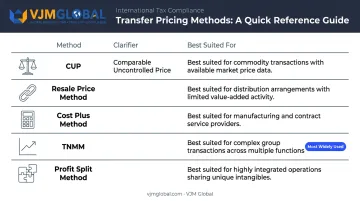

UK practice follows the OECD "most appropriate method" approach. There is no rigid statutory hierarchy. The five recognised methods are:

| Method | Best suited for |

|---|---|

| Comparable Uncontrolled Price (CUP) | Commodity trades, financial transactions, royalties where reliable market data exists |

| Resale Price Method | Distribution entities with limited value-added functions |

| Cost Plus Method | Manufacturing or contract service arrangements |

| Transactional Net Margin Method (TNMM) | Routine functions — the most widely used method in practice |

| Profit Split Method | Highly integrated operations or transactions involving unique, hard-to-value intangibles |

CUP takes natural preference where reliable comparable transactions exist. For intra-group services, HMRC guidance notes that CUP and cost plus are often the most appropriate starting points, depending on the facts.

Low Value-Adding Intragroup Services

Where services are routine in nature and do not create significant value for the group — administrative, IT support, HR, basic accounting — a simplified approach is available. HMRC's guidance confirms a 5% mark-up on relevant costs may be applied, but only consistently across the group. The documentation must cover:

- Nature and description of each service

- Benefit analysis confirming the recipient receives genuine value

- Allocation keys used to distribute costs across recipients

- Confirmation that the simplified approach is applied consistently

Economic Analysis and Comparables

Once the method is selected, the quality of supporting evidence determines how defensible the position is. HMRC expects taxpayers to search for internal comparables first — transactions the UK entity has with unrelated third parties on similar terms. Where no internal comparables exist, external databases are used. Local UK comparables are preferred, though EMEA-regional comparables are accepted where UK-only searches produce insufficient results.

HMRC's GfC7 Guidelines for Compliance, first published on 10 September 2024, identifies specific risk indicators that attract scrutiny — including cherry-picked comparables, unsupported cost allocation keys, and inconsistent application of methods across group entities. Any documentation exercise should be tested against these markers before submission.

UK Transfer Pricing Documentation Requirements

Who Must Prepare What

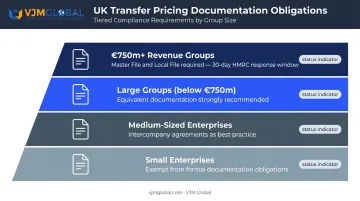

Documentation obligations under the Transfer Pricing Records Regulations 2023 (SI 2023/818) are tiered by group size:

| Group Size | Documentation Obligation |

|---|---|

| €750m+ consolidated revenue | Mandatory Master File and Local File; must be available to HMRC within 30 days of request |

| Large groups below €750m | Not formally required to prepare Master/Local Files, but HMRC strongly recommends equivalent documentation |

| Medium-sized enterprises | Exempt, but intercompany agreements and pricing policies are best practice |

| Small enterprises | Exempt |

Master File and Local File

The Master File provides a group-level overview: global operations, organisational structure, transfer pricing policies, and income allocation across jurisdictions.

The Local File operates at entity level. For each material intercompany transaction, it must include:

- Functional analysis (functions performed, assets employed, risks assumed)

- Industry and comparability analysis

- Selected transfer pricing method with justification

- Benchmarking study with updated financial data

Both documents must be prepared before the UK corporation tax return is filed — not retrospectively. HMRC treats post-enquiry documentation as a significantly weaker basis for penalty mitigation.

Materiality: What Goes in the Local File

The de minimis threshold is £1 million per category of controlled transactions. Below this, documentation is not formally required for that category. However, certain transaction types are always treated as material regardless of value:

- Transfers of intangibles and hard-to-value intangibles

- Transactions priced using a profit split methodology

- Business reorganisations

- Commencement or cessation of transactions in the period

Country-by-Country Reporting

UK-parented groups with consolidated turnover exceeding €750 million in the preceding period must prepare and file a CbCR report in XML format. The report captures income, taxes paid, and measures of economic activity across jurisdictions, and is shared with overseas tax authorities through multilateral exchange arrangements.

Since Pillar 2 took effect, CbCR data is also used to test transitional safe harbour thresholds — making accuracy in CbCR filing more consequential than before.

Record retention: Documentation must be kept for the longest of:

- Six years from the end of the accounting period

- The date an HMRC enquiry closes

- The date HMRC's assessment window expires

Comparables data must be refreshed annually, even where the business description has not materially changed.

UK businesses with Indian operations face a dual compliance burden: HMRC's documentation requirements and India's Section 92 obligations run in parallel. VJM Global supports both, covering Master Files, Local Files, CbCR preparation, and benchmarking studies aligned with OECD standards.

Exemptions from UK Transfer Pricing Rules

The SME Exemption

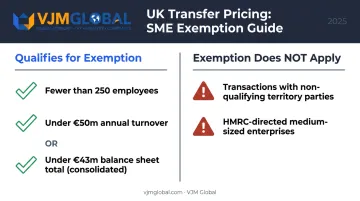

Groups meeting both a headcount threshold (fewer than 250 employees) and either a turnover threshold (under €50 million) or a balance sheet threshold (under €43 million) are currently exempt from UK transfer pricing rules. Thresholds are tested against consolidated group figures, not the individual entity.

Following the 2025 HMRC consultation — response published 26 November 2025 — the government confirmed it will not proceed with restricting the SME exemption. SMEs retain their general exemption for now.

Key Limitations on the Exemption

The SME exemption is not a complete safe harbour. It does not apply to:

- Transactions with parties in non-qualifying territories — broadly, jurisdictions without an appropriate double tax treaty with the UK. HMRC publishes the qualifying territories list, and tax havens are notably excluded

- Medium-sized enterprises directed by HMRC — HMRC has the power to direct a medium-sized enterprise to apply the full transfer pricing rules regardless of the exemption

Taxpayers may also voluntarily elect out of the SME exemption. This is relevant where a group wants to establish pricing certainty for future years, or where a connected foreign party already faces a transfer pricing adjustment.

Even where the exemption applies, all transactions must still be priced at arm's length and supported by analysis. The exemption removes formal documentation obligations — it does not remove the substantive pricing requirement.

Penalties for Non-Compliance with UK Transfer Pricing Rules

Fixed Penalties for Record Failures

HMRC INTM450070 confirms that failure to keep or preserve adequate transfer pricing records attracts a penalty of up to £3,000 per accounting period. For groups above the €750 million threshold, failure to maintain a Master File and Local File creates a presumption of carelessness on any HMRC adjustment — which directly elevates the penalty exposure on any tax underpayment.

Tax-Geared Penalties

Under Finance Act 2007, Schedule 24, inaccuracies in returns attract penalties based on behaviour:

| Behaviour | Maximum Penalty |

|---|---|

| Careless error | 30% of potential lost revenue (PLR) |

| Deliberate but not concealed | 70% of PLR |

| Deliberate and concealed | 100% of PLR |

Penalties can be reduced through:

- Disclosure — unprompted disclosure attracts lower reductions than prompted

- Cooperation with HMRC — the quality and completeness of your engagement matters

- Contemporaneous documentation — a documented, reasoned attempt to establish an arm's length price can prevent a careless error finding and significantly reduce penalty exposure

HMRC Enquiry Windows

HMRC can open a formal enquiry up to 12 months after the return filing date. Beyond that, discovery assessments apply:

- 4 years — errors not caused by careless or deliberate behaviour

- 6 years — careless errors

- 20 years — deliberate errors

For CbCR non-compliance, separate penalties range from £300 to £3,000, with daily penalties for persistent failure to provide required information.

UK Transfer Pricing Reforms: What's Changing in 2025–2027

What the 2025 Consultation Confirmed

Two consultations closed in mid-2025, with responses published on 26 November 2025. The confirmed outcomes are:

- SME exemption retained — no restriction to the current thresholds

- UK-to-UK exemption introduced — broadly removing domestic transfer pricing from periods starting on or after 1 January 2026, subject to carve-outs (ring-fenced trades, patent box, QAHCs, banks)

- International Controlled Transactions Schedule (ICTS) announced — a new annual reporting requirement for cross-border related-party transactions

The ICTS: What It Will Require

The ICTS policy paper confirms the schedule will apply for accounting periods beginning on or after 1 January 2027, subject to a technical consultation on secondary legislation in Spring 2026.

In-scope businesses will file a standardised summary of cross-border controlled transactions alongside their corporation tax return. Key features:

- £1 million aggregate threshold — groups with total cross-border related-party transactions below this are exempt

- Tabular format — capturing nature, value, and pricing methodology for each transaction category

- Automated risk targeting — the ICTS is designed to improve HMRC's data-led risk identification, enabling more targeted enquiries rather than broad fishing exercises

The practical implication: many mid-market UK businesses with overseas subsidiaries — including those below the €750 million Master File threshold — will need structured transaction data for 2027 filings.

Start building data capture processes now. Waiting until 2027 leaves little room to identify gaps in how related-party transactions are categorised and valued.

Additional Finance Bill Changes From 1 January 2026

Beyond the UK-to-UK exemption and expanded participation condition, the 2026 Finance Bill also:

- Updates the transfer pricing treatment of loan guarantees to align with OECD guidance

- Aligns the valuation standard for transfers and licences of intangible fixed assets to a single arm's length standard

For UK businesses with cross-border India operations, these reforms intersect with Indian transfer pricing requirements — creating a need to review existing intercompany policies from both ends. VJM Global works with UK-India groups on exactly this: assessing how the 2026–2027 changes affect current documentation and building ICTS-ready transaction frameworks ahead of the first filing year.

Frequently Asked Questions

What is transfer pricing in the UK?

UK transfer pricing refers to rules governing how prices are set for transactions between connected or related parties, such as group companies. Under TIOPA 2010, those prices must reflect what independent parties would agree — the arm's length principle — to prevent artificial profit shifting and protect the UK tax base.

Is transfer pricing mandatory under UK law?

Yes. UK transfer pricing rules are mandatory for businesses within scope under TIOPA 2010, with a self-assessment obligation to confirm or adjust intragroup pricing. SMEs benefit from a statutory exemption, though HMRC can override this for medium-sized enterprises in certain circumstances.

Who is exempt from UK transfer pricing rules?

SMEs with fewer than 250 employees and either under €50m turnover or under €43m assets qualify for the general exemption. Dormant companies (dormant since 31 March 2004) are also excluded. The SME exemption does not cover transactions with parties in non-qualifying territories (jurisdictions without an appropriate UK double tax treaty).

What documentation does HMRC require for UK transfer pricing?

Groups with consolidated revenues above €750 million must maintain a formal Master File and Local File under SI 2023/818, available to HMRC within 30 days of request. Other large businesses are strongly advised to prepare equivalent documentation and have it ready before filing their corporation tax return.

What penalties apply for UK transfer pricing non-compliance?

A fixed penalty of up to £3,000 applies for failure to maintain records. Tax-geared penalties reach 30% of potential lost revenue for careless errors, 70% for deliberate errors, and 100% for deliberate and concealed errors. HMRC's discovery window extends to 20 years for deliberate behaviour.

What is the arm's length principle in UK transfer pricing?

The arm's length principle requires that prices in intragroup transactions match what two independent, unrelated parties would agree to under comparable market conditions. UK law, via TIOPA s164, mandates that this principle be interpreted in accordance with the OECD Transfer Pricing Guidelines.