Introduction

Singapore businesses expanding into India often encounter the term "VAT" (Value Added Tax) in contracts, financial records, or discussions about India's indirect tax system — and it can cause confusion. While Singapore operates under a familiar GST framework (currently at 9%), India's VAT system has a distinct history and, for certain goods like petroleum products and alcohol, still applies today.

That history has real practical weight. Legacy financial statements, due diligence on Indian partners, and certain regulated industries all surface VAT references that require context to interpret correctly. This guide covers:

- What VAT in India was and how it functioned

- Why GST replaced it in 2017

- Which goods still fall under state VAT

- What this means for Singapore businesses operating or investing in India

Key Takeaways

- India introduced VAT in 2005 as a state-level consumption tax, designed to stop the problem of taxes being charged on top of other taxes

- It was replaced by GST on 1 July 2017, unifying India's fragmented indirect tax structure

- Petroleum products and alcohol remain governed under state VAT laws today

- Singapore businesses entering India will primarily deal with GST, not VAT

- That said, VAT knowledge still matters — particularly for sector-specific compliance, audits, and reviewing pre-2017 financial records

What Was VAT in India?

The 2005 Reform That Changed Indian Taxation

India introduced VAT on 1 April 2005 under state-specific Value Added Tax Acts, replacing the older general Sales Tax system. The earlier system suffered from a critical flaw: cascading taxes, or "tax on tax." Businesses paid tax on inputs, then paid tax again on outputs that already included the input tax, creating an unfair burden that inflated prices artificially.

The White Paper on State-Level Value Added Tax (17 January 2005) explained the problem: "In the existing sales tax structure, there are problems of double taxation of commodities and multiplicity of taxes, resulting in a cascading tax burden."

How VAT Actually Worked

VAT was a multi-stage, consumption-based tax levied at every stage of the supply chain:

- Manufacturer sold to wholesaler (VAT charged)

- Wholesaler sold to retailer (VAT charged)

- Retailer sold to consumer (VAT charged)

The key difference from the old system: businesses could claim credit for tax already paid on inputs, so only the value added at each stage was taxed. The final burden fell on the end consumer, not business intermediaries.

Critical distinction: VAT was a state-level tax. Each Indian state enacted its own VAT legislation, set its own rates, and maintained its own compliance requirements. This meant a company operating across multiple states faced 28+ different VAT regimes.

Who Had to Register

Any individual, partnership, or company selling goods within a state had to register for VAT if annual turnover exceeded INR 5 lakhs. Registration was compulsory only for intra-state transactions (sales where buyer and seller operated in the same state).

VAT Rate Structure

The nationally agreed framework set four rate categories:

| Category | Rate | Goods Covered | Items Count |

|---|---|---|---|

| Exempt | 0% | Natural, unprocessed products | ~46 items |

| Precious metals | 1% | Gold, silver, precious stones | Limited |

| Essential goods | 4% | Industrial inputs, capital goods, medicines, cooking oil | ~270 items |

| General rate | 12.5% | All other goods | Residual |

Individual states could (and did) apply slight variations, but this framework created the baseline.

Why VAT Was Better Than Sales Tax

These rate categories only tell part of the story. The real advantage of VAT lay in the input tax credit mechanism, which eliminated cascading at every stage of the supply chain.

Here's a simple example: A manufacturer buys raw materials for INR 1,00,000 and pays 12.5% VAT = INR 12,500. They sell the finished product for INR 1,50,000 and collect 12.5% VAT = INR 18,750.

Instead of remitting the full INR 18,750, they claim credit for the INR 12,500 already paid. They remit only INR 6,250: the tax on the value they actually added.

This created:

- Lower final prices for consumers

- Transparent invoicing and audit trails

- Reduced tax evasion (buyers needed seller invoices to claim credits)

- Fairer distribution of tax burden across the supply chain

For Singapore businesses evaluating India's tax history, understanding VAT's input credit logic matters — it's the same principle that underpins GST, the system that replaced it in 2017.

How VAT Was Calculated: Input Tax, Output Tax, and Credits

The Core Formula

VAT Payable = Output Tax – Input Tax

- Output tax: VAT charged to customers on sales

- Input tax: VAT paid to suppliers on purchases — covering raw materials, goods for resale, and eligible capital goods

Singapore businesses will recognize this logic immediately: it mirrors the GST input/output tax credit system Singapore businesses will recognize this immediately — the mechanics mirror how GST input/output credits work under Singapore's own system.

Practical Example

A dealer purchases goods worth INR 1,00,000 at 12.5% VAT:

- Purchase price: INR 1,00,000

- Input tax paid: INR 12,500

- Total payment: INR 1,12,500

They sell these goods for INR 1,50,000 at 12.5% VAT:

- Sale price: INR 1,50,000

- Output tax collected: INR 18,750

- Total receipt: INR 1,68,750

VAT payable to government: INR 18,750 (output) – INR 12,500 (input) = INR 6,250

The dealer remits only the net difference, having already credited upstream taxes. That net-only remittance worked because the system was built around documented invoices at every stage.

Invoice-Based Collection

VAT operated through an invoice-based credit mechanism. Dealers issued tax invoices for every sale, which served dual purposes:

- Proof of tax paid by the seller

- Documentation enabling the buyer to claim input tax credit

This created an audit trail that made evasion more difficult, a structural improvement over the old sales tax system.

Registration and Compliance Process

Businesses exceeding the INR 5 lakh threshold had to:

- Register with their state's VAT office

- Obtain an 11-digit Tax Identification Number (TIN)

- File periodic VAT returns (monthly or quarterly, depending on state rules and turnover)

- Maintain detailed records of all taxable transactions

This process is now replaced by GST registration for most goods, but remains relevant for petroleum and alcohol.

VAT vs. GST: How India's Tax System Evolved

The 2017 Transformation

On 1 July 2017, India replaced VAT and more than 17 other indirect taxes with a unified Goods and Services Tax (GST). The midnight ceremony in Parliament's Central Hall marked a historic shift: India moved from a fragmented, state-by-state regime to a single national framework.

GST subsumed:

- Central Excise duty and additional duties of excise

- Service Tax

- State VAT and Central Sales Tax

- Purchase Tax, Entry Tax, Luxury Tax

- Entertainment Tax and taxes on lottery/betting

- Multiple surcharges and cesses

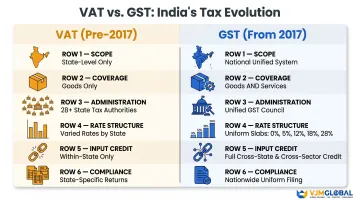

Structural Differences: VAT vs. GST

| Feature | VAT (pre-2017) | GST (from 1 July 2017) |

|---|---|---|

| Scope | State-level only | National (Centre + States jointly) |

| Coverage | Goods only | Goods and services |

| Administration | 28+ state VAT authorities | GST Council + CBIC + State GST depts |

| Rate structure | Varied by state (0%, 1%, 4%, 12.5%) | Uniform nationwide (0%, 5%, 12%, 18%, 28%) |

| Input credit | Within-state purchases only | Across goods, services, inter-state |

| Compliance | Different rules per state | Uniform nationwide framework |

Why VAT Had to Go

The fragmented state VAT system created serious problems for businesses operating across India:

- A business in five states navigated five VAT Acts, five rate schedules, five registration processes, and five separate filing systems

- Varying definitions across states let companies exploit classification gaps or misclassify goods to reduce liability

- Central Sales Tax on interstate transactions created artificial economic borders, slowing trade within India

- Lack of Centre-State coordination made comprehensive enforcement — and revenue protection — nearly impossible

For Singapore businesses evaluating Indian partners or reviewing historical accounts, understanding this fragmentation explains why pre-2017 compliance records look so inconsistent.

The Parallel for Singapore Businesses

Singapore's GST (9% since 1 January 2024) and India's GST operate on identical principles: tax on output minus credit for tax on input. You're not encountering an unfamiliar concept — you already understand the mechanism.

The differences lie in:

- Multiple rate slabs: India uses 0%, 5%, 12%, 18%, and 28% — not a single flat rate like Singapore's 9%

- Dual administration: Both Centre and States levy GST (CGST + SGST for intra-state; IGST for inter-state transactions)

- E-invoicing mandates: Required for businesses above INR 5 crore turnover, with strict technical specifications

- Frequent updates: India's GST framework evolves regularly — rate changes, rule clarifications, and new compliance requirements appear throughout the year

The VAT Term Still Appears

Knowing the GST framework is essential — but the term "VAT" hasn't disappeared entirely. It still surfaces in:

- Contracts signed before 2017

- Financial statements and historical records

- Specific goods categories (petroleum and alcohol)

- Legacy compliance matters

Singapore businesses conducting due diligence on Indian partners or reviewing historical accounts should understand this overlap to avoid confusion.

What Remains Under VAT in India Today

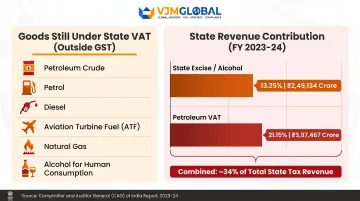

Goods Still Outside GST

A limited set of goods was deliberately excluded from GST and continues under state VAT laws:

Petroleum products:

- Petroleum crude

- Petrol (motor spirit)

- High-speed diesel (HSD)

- Aviation turbine fuel (ATF)

- Natural gas

Alcohol:

- Alcohol for human consumption

Legal basis: Section 9(2) of the CGST Act 2017 states GST shall be levied on petroleum products "from such date as may be notified by the Government on the recommendation of the GST Council." For alcohol, Article 366(12A) of the Constitution excludes it from the GST definition entirely.

Why These Exclusions Exist

These goods represent a major share of state tax revenue. According to the CAG State Finances 2023-24 report:

- State Excise (primarily alcohol): INR 2,49,134 crore = 13.25% of State Own Tax Revenue

- Taxes on Sales/Trade (primarily petroleum VAT): INR 3,97,467 crore = 21.15% of State Own Tax Revenue

- Combined: approximately 34% of all state tax revenue

States refused to surrender this revenue to a unified GST framework without clear compensation guarantees.

No Timeline for Integration

Despite periodic discussions, no fixed timeline exists for bringing petroleum products under GST. Article 279A(5) of the Constitution requires the GST Council to recommend a date, but as of 2026, the Council has maintained status quo.

For alcohol, a Constitutional Amendment would be required — a far higher bar.

Compliance Implications

Businesses in specific industries still face state VAT obligations alongside GST. This applies to:

- Oil and gas companies, manufacturers using industrial petroleum inputs, and logistics firms with significant fuel costs

- Alcohol producers, distributors, hotels, restaurants, and retail outlets

If your business deals with these goods, you must:

- Register under the relevant state's VAT law (in addition to GST)

- Comply with that state's specific rates and return-filing rules

- File separate VAT returns

- Maintain VAT-specific records

For most Singapore businesses entering India in manufacturing, services, retail, technology, or trading, VAT is unlikely to be a primary compliance obligation. That said, if your operations touch energy, hospitality (alcohol sales), or fuel-heavy logistics, verify state VAT requirements with a local tax advisor before setting up.

What Singapore Businesses Need to Know About India's Indirect Taxes

GST Is Your Primary Concern

When establishing operations in India, you'll primarily need to register for and comply with GST, not VAT. GST registration becomes mandatory when:

- Annual turnover exceeds INR 40 lakhs for goods suppliers (approximately SGD 63,000)

- Annual turnover exceeds INR 20 lakhs for service providers (INR 10 lakhs in special category states)

- You engage in inter-state supply, regardless of turnover

- You operate through e-commerce platforms

- You're a non-resident taxable person or casual taxable person

- You need to pay tax under reverse charge mechanism (common for imported services)

Common Indirect Tax Pitfalls

Singapore businesses frequently encounter challenges in these areas:

- GST rate classification: The correct rate (5%, 12%, 18%, or 28%) depends on HSN code analysis — misclassification triggers reassessments and penalties

- Reverse charge mechanism (RCM): When Singapore parent companies provide services to Indian subsidiaries, the Indian recipient must self-assess and pay GST — many businesses miss this initially

- Input tax credit (ITC) reconciliation: The GST portal auto-populates returns from supplier filings; mismatches block ITC claims and create cash flow gaps

- E-invoicing compliance: Businesses with turnover above INR 5 crore must generate e-invoices through the GST portal for B2B transactions — the threshold has dropped repeatedly and may fall further

- Invoice requirements: GST-compliant invoices require specific mandatory fields; non-compliant invoices prevent customers from claiming ITC, triggering commercial disputes

- Non-compliance penalties: Section 122 of the CGST Act imposes INR 10,000 or the tax amount due (whichever is higher); late payment attracts 18% per annum interest under Section 50

Why These Pitfalls Are Hard to Avoid

The pitfalls above aren't one-time setup mistakes — they reflect ongoing systemic volatility in India's indirect tax environment:

- Frequent rule changes and clarifications

- State-specific variations in administration

- Complex IT system requirements (e-invoicing, e-way bills)

- Stringent audit and verification processes

- Language and procedural differences across states

According to Deloitte India's GST@8 Survey (June 2025, based on 963 senior corporate executives), 67% of businesses cited ongoing ground-level implementation challenges, including expansive legal interpretations by tax officials, ITC mismatches, and denial of export status.

Professional Support Makes the Difference

Navigating this environment — including knowing when residual VAT obligations apply and staying current with frequent GST rule changes — is particularly demanding for foreign businesses without in-country expertise.

VJM Global specialises in helping foreign businesses establish and maintain GST compliance in India. With 30+ years of experience, the firm supports Singapore businesses across the full compliance cycle — from GST registration and return filing to e-invoicing setup, ITC reconciliation, and reverse charge mechanism advisory for imported services.

Working with advisors who understand both Singapore's GST framework and India's indirect tax system reduces compliance risk and avoids the implementation delays that catch most new entrants off guard.

Frequently Asked Questions

Is VAT the same as GST in India?

No, VAT and GST are not the same. VAT was a state-level tax applying only to goods, replaced by the national GST framework on 1 July 2017. GST covers both goods and services, applies uniformly across India with standardised rate slabs, and subsumes most of what VAT previously covered.

Why was VAT removed in India?

India replaced VAT to eliminate a fragmented, state-by-state tax system with inconsistent rates, cascading tax effects, and heavy compliance burdens. GST unified the indirect tax structure into a single national framework, simplifying compliance and improving audit trails to reduce tax evasion.

Is VAT mandatory to pay in India?

For the vast majority of goods and services, VAT no longer applies — GST replaced it in 2017. The exceptions are petroleum products (crude, petrol, diesel, ATF, natural gas) and alcohol for human consumption, which remain under state VAT laws at rates that vary by state.

What goods are still taxed under VAT in India after GST?

Six categories remain outside GST and subject to state VAT: petroleum crude, petrol, diesel, aviation turbine fuel, natural gas, and alcohol for human consumption. States set their own rates for these items, so costs vary depending on where your business operates.

Do Singapore businesses need to register for VAT when entering India?

Most Singapore businesses entering India need to register for GST, not VAT. VAT registration is only relevant if your operations specifically involve petroleum products or alcohol distribution.