Introduction

Singapore businesses researching "VAT in India" often encounter outdated and current information mixed together, which makes understanding your actual tax obligations harder than it needs to be. The key fact: India replaced its state-level VAT system with GST (Goods and Services Tax) in July 2017.

For most businesses, VAT is now a historical reference point. That said, the old VAT framework still matters when reviewing pre-2017 contracts, conducting financial due diligence, or operating in sectors like petroleum and alcohol where state-level VAT continues to apply.

This guide clarifies what VAT was, how it operated, where it still applies, and what Singapore businesses specifically need to know about GST compliance when entering or operating in the Indian market.

TLDR:

- India's state-level VAT was replaced by GST on 1 July 2017 for most goods and services

- VAT still applies to petroleum products and alcoholic beverages under state jurisdiction

- GST registration is required for Singapore businesses supplying goods above ₹40 lakh or services above ₹20 lakh annual turnover in India

- GST registration is mandatory for foreign businesses providing OIDAR services or selling through e-commerce platforms in India

- Historical VAT knowledge remains essential for due diligence, audits, and legacy contract reviews from pre-2017 operations

What is VAT in India?

Value Added Tax (VAT) was an indirect tax levied on goods at each stage of the supply chain, from raw material to final consumer. Unlike a simple sales tax applied only at the point of final sale, VAT applied only to the "value added" at each stage — not the total transaction value.

For Singapore businesses reviewing historical India contracts or considering entry into the Indian market, understanding VAT remains relevant: a handful of goods categories still fall outside GST, and pre-2017 financial records frequently reference VAT obligations.

How VAT Worked in India

The Value Added Tax Act came into force on 1 April 2005, replacing the earlier General Sales Tax system. The Empowered Committee of State Finance Ministers, constituted in November 1999, coordinated this nationwide rollout. A few states initially opted out before eventually adopting VAT.

VAT was administered at the state level under Entry 54 of the State List of the Constitution. Each state enacted its own VAT legislation with separate rate schedules and administrative processes. For businesses operating across multiple states, this created a fragmented compliance environment — one of the key inefficiencies that later drove the move to GST.

Scope and Key Rules

- All business transactions involving the sale of goods within a state by individuals, partnerships, or companies were covered

- Businesses below a state-prescribed annual turnover threshold were exempt from VAT registration (thresholds varied by state)

- VAT applied only to goods; services were taxed separately under a central "Service Tax" regime

- Only registered dealers above the turnover threshold were required to collect and remit VAT

Why This Still Matters for Singapore Businesses

- Pre-2017 Indian contracts, financial statements, and due diligence documents frequently reference VAT obligations

- Petroleum products and alcohol remain under VAT jurisdiction today, outside the GST framework

- Understanding the VAT-to-GST transition provides essential context for current compliance requirements

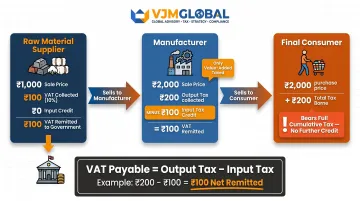

How VAT Works: Input Tax, Output Tax, and Computation

VAT operated on a credit mechanism with two core components:

Output tax: VAT charged by a dealer on sales made to customers

Input tax: VAT paid by a dealer on purchases made from suppliers

VAT computation formula:

VAT Payable = Output Tax − Input Tax

This means a dealer does not pay tax on the full sale value, but only on the value they added. This mechanism eliminated the "cascading" or tax-on-tax problem that plagued the earlier General Sales Tax regime, where tax paid on purchases was embedded in costs without any credit, causing compounding throughout the supply chain — and making Indian goods less competitive in the process.

Worked example:

A manufacturer purchases raw materials worth ₹1,00,000 at 10% VAT:

- Input tax paid: ₹10,000

- Total cost: ₹1,10,000

The manufacturer adds value through processing and sells finished goods for ₹1,50,000 at 10% VAT:

- Output tax collected: ₹15,000

- VAT payable to government: ₹15,000 - ₹10,000 = ₹5,000

The manufacturer remits only ₹5,000 — the tax on the ₹50,000 of value added — not the full ₹15,000. The final consumer bears the full tax burden; each dealer in the chain pays only their share.

Administration Requirements

Dealers were required to:

- Self-assess their VAT liability

- File periodic returns (typically monthly)

- Maintain detailed invoices documenting VAT charged and paid at each stage

- Preserve this paper trail for compliance verification

For Singapore businesses with operations across multiple Indian states, this meant navigating different VAT rates and return schedules in each state — a complexity that GST later resolved with a single unified framework.

VAT Rates in India by Product Category

Because each state set its own VAT rates, there was no single national rate structure. However, most states followed the four-tier framework recommended by the Empowered Committee of State Finance Ministers in January 2005:

| Rate Tier | Product Categories | Notes |

|---|---|---|

| 0% (Exempt) | Approximately 46 natural and unprocessed products of social importance, plus up to 10 items of local importance chosen by individual states | Fresh produce, grains, essential commodities |

| 1% | Gold, silver, and precious stone ornaments | Low rate aimed at reducing tax evasion in the jewellery trade |

| 4% | Approximately 270 goods: items of basic necessity, medicines, agricultural and industrial inputs, capital goods, and declared goods | Includes medicines, fertilizers, and capital equipment |

| 12.5% (General rate) | All remaining commodities not covered in the above categories | Standard revenue rate for most manufactured goods |

| 20%+ | Liquor, lottery tickets, petrol, diesel, aviation turbine fuel (ATF), and other motor spirits | Excluded from the VAT chain; states set their own high rates |

Despite the recommended framework, VAT carried structural gaps that Singapore businesses should understand when reviewing historical India exposure:

- Covered goods only — services fell under the separate central Service Tax regime

- Rate variation was common across states despite the four-tier guidance

- States could apply surcharges or adjust the 4% rate for specific goods

- Petroleum and alcohol sat outside the standard VAT structure entirely

For Singapore businesses, these rates are most relevant when reviewing legacy transactions, pre-July 2017 contracts, or outstanding liabilities from India operations that predate GST.

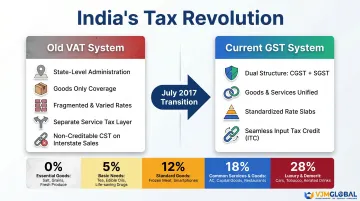

VAT vs. GST: The 2017 Transition That Changed Everything

VAT vs. GST: How India Replaced 29 State VAT Systems with One Unified Framework

On 1 July 2017, India introduced the Goods and Services Tax (GST), enabled by the 101st Constitutional Amendment Act of 2016. For the first time, India replaced a fragmented patchwork of 29+ state-level VAT systems with a single nationwide indirect tax structure. For Singapore businesses operating across multiple Indian states, this shift fundamentally changed how tax obligations work.

Structural differences:

Old VAT system:

- State-level tax applying only to goods

- Fragmented rates across states

- Separate Service Tax at the central level

- Central Sales Tax (CST) on inter-state transactions (non-creditable)

- No unified input tax credit across goods and services

Current GST system:

- Dual structure: CGST (Central GST) + SGST (State GST) on intra-state transactions

- IGST (Integrated GST) on inter-state transactions

- Unified taxation of both goods and services

- Standardized rate structure across India

- Seamless input tax credit across goods, services, and states

GST rate slabs:

| Rate | Category | Common Examples |

|---|---|---|

| 0% | Essential items | Fresh fruits, vegetables, milk, eggs, unbranded flour |

| 5% | Mass consumption items | Spices, tea, coffee, edible oil, life-saving drugs, EVs |

| 12% | Standard goods | Butter, ghee, cheese, processed foods, mobile phones |

| 18% | Most common rate | Electronics (laptops, ACs, TVs, refrigerators), professional and financial services |

| 28% | Luxury/sin goods | High-end cars, specific luxury items |

Special rates: 3% for gold; 0.25% for rough precious stones; Compensation Cess (1-22%) on luxury cars, tobacco, and aerated drinks

Most Singapore businesses operating in India fall into the 18% bracket — here's how the standard slabs apply by sector:

| Business Sector | GST Rate | Notes |

|---|---|---|

| Professional services (IT, consulting, finance) | 18% | Standard rate for most services |

| Electronics (laptops, TVs, ACs, cameras) | 18% | Standardized rate (many moved down from 28%) |

| Manufactured goods (general) | 12-18% | Depends on product classification |

| F&B products (processed foods) | 5-18% | 5% for essential packaged foods; 12% for items like butter; 18% for restaurant services |

Input Tax Credit (ITC) under GST:

The ITC mechanism mirrors and expands the old VAT input credit system. Key improvements:

- Goods + services credit: ITC now covers both goods and services — VAT only covered goods

- Flexible offset: IGST credit can offset CGST, SGST, or IGST liability; similar flexibility exists for CGST and SGST

- Inter-state trade: Full ITC available on IGST paid on inter-state transactions (old CST was non-refundable)

- No cascading tax: Tax applies only to value added at each stage — not stacked on prior tax paid

- Capital goods: Full ITC claimable upfront, rather than spread over multiple years as under VAT

Practical note for Singapore businesses:

If you are selling goods or services in India above the GST registration threshold (₹40 lakh for goods suppliers; ₹20 lakh for service providers in normal states), you must register for GST. The old VAT registration is no longer valid — a GSTIN (GST Identification Number) has replaced the old VAT TIN.

Where VAT Still Applies in India Today

While GST replaced VAT for most goods and services, two major categories remain outside GST and continue under state-level VAT jurisdiction:

1. Petroleum products:

- Petroleum crude

- Petrol (motor spirit)

- High-speed diesel

- Aviation turbine fuel (ATF)

- Natural gas

2. Alcoholic beverages: Alcoholic liquor for human consumption falls entirely outside GST, with states setting their own excise duty and VAT rates.

Both categories contribute significantly to state government revenues. Under Section 9(2) of the CGST Act, bringing them under GST requires a GST Council recommendation — one that has not been made.

State VAT rates on petroleum

Fuel taxes comprise approximately 55% of petrol's retail price and 50% of diesel's retail price in India. Central excise duty is uniform nationwide (₹19.90/litre on petrol; ₹15.80/litre on diesel as of April 2025), but state VAT varies significantly:

Sample state VAT rates:

- Andhra Pradesh: 31% + ₹4/litre + ₹1/litre cess (petrol)

- Delhi: 19.40% (petrol); 16.75% + ₹250/KL air ambience charges (diesel)

- Goa: 21.5% + 0.5% green cess (petrol); 17.5% + 0.5% green cess (diesel)

- Andaman & Nicobar Islands: ~1% (lowest rate)

The range across states is broadly 1% to 31%+ on petrol. For current state-wise rates, consult PPAC (Petroleum Planning & Analysis Cell) data.

VAT on alcohol

Beyond petroleum, alcohol is the other major holdout. States set their own excise duty and VAT rates with no national standardization — a significant revenue source they have consistently resisted bringing under GST.

Practical implications for Singapore businesses

If your company operates in the energy, oil & gas, aviation, or F&B (alcohol) sectors in India, you must still track and comply with state-specific VAT rates — and those rates differ meaningfully from state to state. For all other sectors, VAT is a historical reference point; your indirect tax obligations fall entirely under GST. Either way, understanding which regime applies to your specific activities is where sector-specific compliance advice from a firm like VJM Global becomes practical rather than optional.

GST Compliance: What Singapore Businesses Entering India Need to Know

Registration Thresholds

Mandatory GST registration thresholds (effective 1 April 2019):

| Category | Normal States | Special Category States* |

|---|---|---|

| Goods suppliers | ₹40 lakh | ₹20 lakh |

| Service providers | ₹20 lakh | ₹10 lakh |

*Special category states: Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh, and Uttarakhand

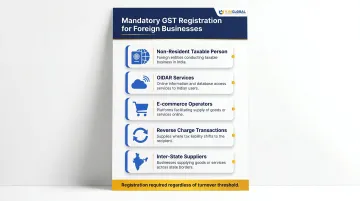

Mandatory registration regardless of turnover:

Foreign businesses must register under Section 24 of the CGST Act in the following scenarios:

- Non-Resident Taxable Persons (NRTP): Foreign businesses making taxable supply in India must apply for registration at least 5 days before commencing business

- OIDAR service providers: Businesses supplying Online Information and Database Access or Retrieval services (cloud computing, digital advertising, streaming, online gaming) from outside India to non-registered persons in India

- E-commerce operators: Selling goods or services through e-commerce platforms in India

- Reverse charge transactions: Liable to pay tax under reverse charge mechanism

- Inter-state suppliers: Making inter-state supplies of goods or services

Ongoing Compliance Obligations

Mandatory GST returns:

| Return Type | Description | Frequency |

|---|---|---|

| GSTR-1 | Details of outward supplies (sales) | Monthly or quarterly |

| GSTR-3B | Summary return with self-assessed tax liability | Monthly |

| GSTR-9 | Annual return | Annually |

E-invoicing requirement:

Mandatory for businesses with annual turnover exceeding ₹5 crore (effective 1 August 2023). OIDAR providers are exempt from e-invoicing.

Key compliance tasks:

- Maintain proper tax invoices with all required details

- Track and claim Input Tax Credit (ITC) correctly

- Reconcile ITC claimed with GSTR-2B (auto-populated from supplier returns)

- File returns within prescribed deadlines

- Respond to GST authority notices promptly

- Implement e-invoicing if applicable

Penalties for Non-Compliance

Under Section 122 of the CGST Act:

- Offences without fraud: ₹10,000 or the tax amount involved (whichever is higher)

- Offences involving fraud or wilful misstatement: Penalty equal to the tax amount evaded (100% of tax)

Under Section 47 of the CGST Act:

- Late filing of periodic returns: ₹100/day up to maximum ₹5,000

- Late filing of annual return: ₹100/day up to maximum 0.25% of turnover in the state

Common Challenges for Foreign Businesses

Singapore businesses entering India face recurring compliance hurdles across three areas:

ITC claim issues:

- Mismatch between books and GST returns (GSTR-3B)

- Inadvertent claims on ineligible transactions

- Reverse charge mechanism oversights

Return filing challenges:

- Delays leading to interest and penalties

- Errors in reporting sales, purchases, or tax liabilities

- Difficulty managing large transaction volumes

Registration complexities:

- Documentation requirements (business address proof, digital signatures, authorized signatory details)

- Understanding threshold and mandatory registration triggers

- Determining correct HSN/SAC codes for products/services

How VJM Global Supports Foreign Businesses

Each of these challenges has a clear solution — provided you have the right compliance partner from the start.

VJM Global brings 30+ years of Indian tax compliance experience and a dedicated team serving foreign businesses. Support covers GST registration through to audit representation:

GST registration services:

- Critical analysis of business operations, supply types, and registration categories

- Complete documentation preparation and online application filing

- Representation during GST authority clarifications

GST compliance and filing:

- Accurate and timely GST return filing (GSTR-1, GSTR-3B, GSTR-9)

- E-invoicing implementation for businesses above ₹5 crore turnover

- Monthly reconciliation of ITC and transaction data

GST advisory:

- Fiscal impact assessment of GST on business operations

- Tax rate determination and supply rule guidance

- Input tax credit optimization

- Business model evaluation for tax efficiency

- HSN/SAC classification advisory

GST audit and refund assistance:

- Comprehensive GST audits of records, refunds, and ITC claims

- GST refund filing for exports, excess payments, or input tax credits

- Representation in disputes with tax authorities

OIDAR and e-commerce support:

- Specialized registration for OIDAR service providers from Singapore and other jurisdictions

- Compliance support for e-commerce operators and marketplace sellers

VJM Global has supported foreign businesses across 15+ industries — including technology, manufacturing, and professional services — achieving a 95% client retention rate. Singapore businesses entering India benefit from the same cross-border compliance infrastructure built for 500+ American and 500+ UK and Australian clients combined.

Frequently Asked Questions

What is VAT tax in India?

VAT (Value Added Tax) was an indirect consumption tax levied at each stage of the goods supply chain in India, administered by individual states from 2005 to 2017. It has been largely replaced by GST, though VAT still applies to petroleum products and alcoholic beverages.

How does VAT work in India?

A registered dealer collects VAT on sales (output tax), deducts VAT paid on purchases (input tax), and remits only the difference to the government. This ensures tax is levied only on the value added at each stage, not the full transaction value.

What is the VAT rate in India?

Historical VAT rates ranged from 0% (essentials) to 1% (gold), 4% (medicines), 12.5% (standard goods), and 20%+ (luxury items and liquor), varying by state. GST has since replaced most of these with unified rates of 0%, 5%, 12%, 18%, and 28%; petroleum and alcohol still carry state-set VAT rates.

How does VAT differ from GST in India?

VAT was a state-level tax applying only to goods with fragmented rates across states. GST is a unified national tax covering both goods and services under a single framework with standardised rates (CGST + SGST on intra-state; IGST on inter-state transactions), administered jointly by centre and states.

When and why was VAT replaced by GST in India?

VAT was replaced by GST on 1 July 2017 to eliminate cascading taxation, reduce compliance complexity for businesses operating across multiple states, and create a single national indirect tax market.

Who is liable to pay VAT in India?

Under the VAT system, any dealer — individual, partnership, or company — selling taxable goods above the state-prescribed turnover threshold was liable to register and pay VAT. This obligation now falls under GST for most goods, with VAT liability continuing only for petroleum and alcohol.