Introduction

Expanding into India represents significant opportunity for Singapore businesses, but GST registration is a critical compliance checkpoint from day one. In practice, a significant share of foreign companies entering India face operational delays tied directly to indirect tax registration errors — missed thresholds, incorrect entity classifications, or incomplete documentation.

This guide addresses Singapore-based businesses entering India through subsidiaries, branch offices, or cross-border digital services. Getting GST registration right prevents penalties starting at INR 10,000, operational bottlenecks, and the inability to issue compliant invoices to Indian B2B clients.

Here's what this guide covers:

- What Indian GST registration involves and how it differs from Singapore's GST framework

- Which Singapore companies must register — and at what threshold or trigger point

- The step-by-step registration process, including documents and timelines

- Post-registration obligations: return filing, invoicing rules, and Input Tax Credit management

Key Takeaways

- GST is India's unified indirect tax requiring most businesses to obtain a 15-digit GSTIN to collect tax, issue invoices, and claim input credits

- Singapore companies must register once turnover exceeds INR 20 lakh (services) or INR 40 lakh (goods), or immediately for inter-state supply or e-commerce

- Digital service providers supplying Indian consumers may need NRTP or OIDAR registration regardless of physical presence

- The registration process takes 3–7 working days on gst.gov.in and requires PAN, Aadhaar authentication, and key business documents

- Ongoing compliance covers monthly/quarterly GSTR-1 and GSTR-3B filings, e-invoicing (above INR 5 crore turnover), and ITC management

What Is GST Registration in India?

GST registration is the process of obtaining a GSTIN — a 15-digit Goods and Services Tax Identification Number — that legally authorises businesses to collect GST, issue tax invoices, and claim input tax credits in India.

The GSTIN structure encodes critical information:

- Digits 1-2: State code

- Digits 3-12: PAN of the business entity

- Digit 13: Registration sequence number for the same PAN within that state

- Digit 14: Default value "Z"

- Digit 15: Checksum verification digit

India's Three-Tier GST Structure vs Singapore's Single Rate

Unlike Singapore's flat 9% GST, India's system splits the tax across central and state governments — which directly affects how a Singapore company accounts for transactions depending on where they occur in India.

Indian GST comprises:

For intra-state transactions:

- CGST (Central GST) — collected by the Central Government

- SGST (State GST) — collected by the State Government, levied alongside CGST at the same rate

For inter-state transactions and imports:

- IGST (Integrated GST) — collected by the Central Government, then apportioned between Centre and states

When GST launched on 1 July 2017, it replaced 17 separate indirect taxes — VAT, service tax, excise duty, octroi, and multiple central and state levies — consolidating them into a single framework.

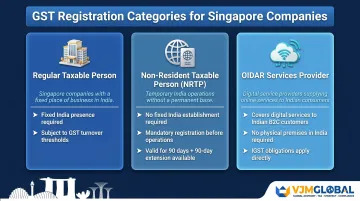

Registration Categories Relevant to Singapore Companies

Three registration categories apply most directly to Singapore companies entering India:

- Regular Taxable Person — For businesses with a fixed place of business in India making taxable supplies. Registration is subject to annual turnover thresholds.

- Non-Resident Taxable Person (NRTP) — For companies that occasionally supply goods or services in India without a fixed place of business or residence. Registration is mandatory regardless of turnover, valid for 90 days with one 90-day extension.

- OIDAR Services Provider — For foreign suppliers of digital services (cloud platforms, software downloads, streaming, online advertising, digital storage) to Indian consumers. Registration is required even without Indian premises.

Do Singapore Companies Need to Register for GST in India?

Mandatory Registration Based on Turnover

Singapore companies with incorporated Indian entities (subsidiary or branch) must register once aggregate annual turnover crosses:

| Business Type | Normal States | Special Category States* |

|---|---|---|

| Goods suppliers | ₹40 lakh | ₹20 lakh |

| Service providers | ₹20 lakh | ₹10 lakh |

*Special Category States include Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Uttarakhand, and Puducherry. Note that Jammu & Kashmir, Ladakh, and Assam opted for the higher ₹40 lakh goods threshold despite special category status.

Registration Required Regardless of Turnover

Certain Singapore companies must register immediately, irrespective of revenue:

- Inter-state suppliers — registration is mandatory the moment any sale crosses a state boundary, regardless of turnover

- E-commerce sellers — platforms like Amazon India and Flipkart require registered vendors before onboarding

- Reverse charge mechanism suppliers — where the Indian recipient is liable to pay GST on specified services received

- Input Service Distributors — required from April 2025 for entities distributing input tax credit across multiple GSTINs

Digital Service Providers Without Physical Presence

Singapore companies supplying OIDAR services to Indian consumers face registration obligations even without an Indian office. This includes SaaS providers, streaming platforms, online advertising, and database access services when supplied to non-registered Indian recipients.

The obligation shifts depending on the buyer: registered Indian businesses pay IGST themselves under the reverse charge mechanism, while individual consumers trigger a direct registration and remittance requirement for the Singapore supplier.

Strategic Voluntary Registration

Not all registration decisions are forced by thresholds. Singapore companies below mandatory limits often register voluntarily to:

- Claim Input Tax Credit on Indian procurement, rent, and professional fees

- Issue GST-compliant invoices required by Indian B2B customers

- Conduct inter-state commerce without restrictions

- Build credibility with Indian enterprise clients who require registered vendors

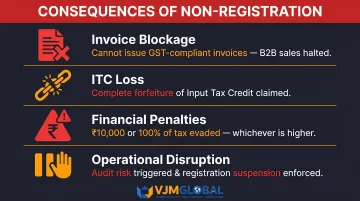

Consequences of Non-Registration

Operating without required GST registration creates serious problems:

- Inability to issue GST-compliant invoices, blocking B2B sales to registered Indian businesses

- Complete loss of Input Tax Credit entitlement

- Penalties of ₹10,000 or 100% of tax evaded (whichever is higher) under Section 122(1)(xi)

- Operational disruption during tax audits and potential registration suspension

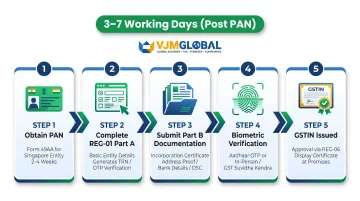

How the GST Registration Process Works for Foreign Companies

GST registration happens entirely online through the official GST portal in two stages — Part A generates a Temporary Reference Number (TRN), Part B involves full documentation submission. Approval typically takes 3–7 working days for compliant applications, though foreign-owned entities often face additional verification.

Step 1: Obtain PAN and Pre-Registration Requirements

PAN (Permanent Account Number) is mandatory before GST registration can begin. For Singapore companies:

- Indian subsidiary or branch: PAN is issued to the Indian legal entity through standard company incorporation processes.

- NRTP registration: Foreign companies must obtain PAN for the Singapore entity itself using Form 49AA — allow 2–4 weeks and start this before other incorporation steps.

VJM Global assists Singapore companies in obtaining PAN for both Indian entities and NRTP registrations, including Form 49AA preparation and liaison with the Income Tax Department.

Step 2: Complete Part A of REG-01 on the GST Portal

Part A captures basic business details — legal name, PAN, email address, and mobile number — and generates your TRN.

Critical requirements for Singapore companies:

- Authorised signatory must have a valid Indian mobile number for OTP verification

- Indian email address recommended (though not mandatory)

- Aadhaar-based authentication now required for smooth Application Reference Number (ARN) generation

Step 3: Submit Part B with Full Documentation

Part B requires comprehensive business information. Here's what Singapore companies need to prepare:

Business details to enter in the form:

- Principal place of business address in India

- Business constitution type (private limited, branch, etc.)

- Bank account information for the Indian entity

- Authorised signatory details with identification

Supporting documents required:

- Certificate of Incorporation of the Indian entity (or Singapore company for NRTP)

- Proof of principal place of business — rental agreement, lease deed, or ownership documents

- Identity and address proof of directors/promoters — passport, address proof, photographs

- Board resolution or Letter of Authorisation designating the authorised signatory

- Cancelled cheque or bank statement for the Indian bank account

- Digital Signature Certificate (DSC) or Aadhaar-based e-signature for application submission

VJM Global assists Singapore companies in preparing compliant documentation packages, including navigating Aadhaar authentication requirements for foreign directors without Indian identification.

Step 4: Biometric Verification and Application Submission

Once your documentation is submitted, the next stage is identity verification — and this is where recent regulatory changes add complexity. A GSTN advisory (March 2025) rolled out biometric-based Aadhaar authentication in Uttar Pradesh, with progressive state-by-state expansion underway.

After form submission, applicants receive either:

- OTP-based Aadhaar authentication link, or

- Appointment booking for in-person biometric verification at a GST Suvidha Kendra

For foreign nationals serving as directors of Indian entities, alternative verification exists through physical verification of the place of business. Non-compliance with biometric verification requirements delays ARN generation.

Step 5: Approval and GSTIN Issuance

Once submitted, the GST officer reviews your application and either approves it or raises queries via Form GST REG-03. You have 7 working days to respond with clarifications in Form GST REG-04.

Upon approval, your GSTIN is issued via Form GST REG-06. The GST Registration Certificate must be displayed prominently at your principal place of business.

Critical post-approval requirement: Rule 10A mandates furnishing valid bank account details within 30 days of registration or before filing GSTR-1/IFF (whichever is earlier). Failure triggers automatic account suspension. NRTP and OIDAR registrations are exempt from this requirement.

GST Rates and Post-Registration Compliance Obligations

Singapore's GST vs India's GST: Key Rate Differences

Singapore operates a single 9% GST rate effective from 1 January 2024. India uses a tiered system that was significantly reformed in September 2025.

Current GST rate structure (effective 22 September 2025 under GST 2.0 reforms):

| Rate | Category | Examples |

|---|---|---|

| 0% | Essential items, exempt categories | Healthcare, education materials, 33 lifesaving drugs |

| 5% | Essential goods/services | Dairy products (butter, ghee), hair oil, shampoo, toothpaste, soaps, tractors |

| 18% | Standard rate for most supplies | Air conditioners, TVs, small cars, paper products, most services |

| 40% | Luxury and sin goods | Tobacco, pan masala, aerated beverages, luxury vehicles, motorcycles >350cc, betting/gaming |

The previous 12% and 28% slabs were eliminated under GST 2.0. Specific niche rates of 0.25% (rough diamonds) and 3% (gold, precious metals) remain.

The applicable rate depends on HSN (Harmonized System of Nomenclature) codes for goods and SAC (Services Accounting Code) for services. Singapore companies should verify specific product/service classifications through the GST Council's official rate schedules.

Once your rate classification is confirmed, the next step is understanding the recurring filing obligations that come with registration.

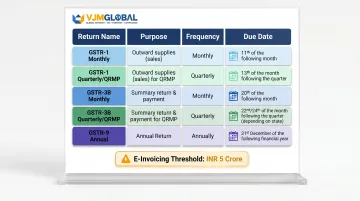

Ongoing Filing and Compliance Requirements

Primary monthly/quarterly returns:

| Return | Purpose | Frequency | Due Date |

|---|---|---|---|

| GSTR-1 | Outward supply details | Monthly (turnover >INR 5 crore) | 11th of following month |

| GSTR-1 | Outward supply details | Quarterly (QRMP scheme) | 13th of month following quarter |

| GSTR-3B | Summary return with tax payment | Monthly (turnover >INR 5 crore) | 20th of following month |

| GSTR-3B | Summary return with tax payment | Quarterly (QRMP scheme) | 22nd/24th of month following quarter |

| GSTR-9 | Annual return | Annually | 31st December of following financial year |

Additional compliance requirements:

E-invoicing: Mandatory for businesses with aggregate turnover exceeding INR 5 crore for B2B supplies and exports. OIDAR (Online Information and Database Access or Retrieval) services are excluded from e-invoicing requirements.

Input Service Distributor (ISD) registration: From April 2025, businesses operating multiple GST registrations under one PAN must register as ISD if any branch receives common input services (legal, audit, consulting, software) used by other units. The previous cross-charge method is no longer permitted. ISD must file GSTR-6 monthly.

Singapore companies navigating these obligations for the first time often work with a local compliance partner — VJM Global supports Singapore-owned Indian entities with GST return filing, ISD registration, and annual compliance management.

Input Tax Credit (ITC) Benefits for Singapore Companies

Beyond filing obligations, GST registration unlocks a direct cost benefit: Input Tax Credit. Tax paid on purchases, rent, professional fees, and other business inputs can be offset against GST collected on sales, reducing net tax liability.

ITC eligibility conditions under Section 16 CGST Act:

- Possession of valid tax invoice from registered supplier

- Receipt of goods or services

- Supplier has paid the tax to the government

- Recipient has filed GSTR-3B return

- Credit claimed within 30th November of the financial year following the one in which the invoice was received, or the annual return filing date (whichever is earlier)

Blocked credits under Section 17(5) — ITC not available on:

- Motor vehicles (unless used for further supply or passenger transport)

- Food and beverages, outdoor catering (unless employer-obligatory)

- Works contract for construction of immovable property (except plant and machinery)

- Goods lost, stolen, destroyed, or given as gifts

- Non-Resident Taxable Persons (NRTP): ITC blocked on all goods/services received, except tax paid on goods directly imported by the NRTP

For Singapore companies in IT services or professional services, ITC recovery on rent, software subscriptions, and consulting fees can meaningfully reduce effective tax costs — making accurate ITC reconciliation under Rule 42/43 worth close attention.

Common Misconceptions Singapore Companies Have About Indian GST

"No Physical Office Means No GST Obligation"

This is the most frequent misconception VJM Global encounters. Singapore companies providing digital services — SaaS platforms, streaming content, online advertising, database access, or cloud services — to Indian consumers must register under the OIDAR category regardless of whether they have Indian premises. This obligation stems directly from Section 14 of the IGST Act, which requires foreign OIDAR suppliers to register and pay IGST when supplying non-registered Indian recipients, even without physical presence.

"One GST Registration Covers All of India"

Many Singapore companies assume a single GSTIN covers nationwide operations — it does not. The GSTIN itself encodes the state code in its first two digits, and each state where you conduct business requires its own separate registration.

Companies establishing regional offices in Mumbai, Bangalore, and Delhi, for instance, need three distinct GSTINs — one per state of operation.

"GST Registration Covers Income Tax Compliance"

GST and corporate income tax are entirely separate compliance obligations under different statutes:

- GST is governed by the CGST Act, SGST Acts, and IGST Act (administered by CBIC)

- Corporate income tax is governed by the Income Tax Act, 1961 (administered by CBDT)

Singapore companies must comply with both independently. GST registration does not exempt you from income tax obligations. Equally, income tax registration carries no bearing on your GST obligations.

Frequently Asked Questions

How much does it cost to get a GST number in India?

There is no government fee for obtaining a GSTIN through the official GST portal. However, businesses typically engage tax consultants or advisory firms like VJM Global to handle the process, with professional fees varying based on business structure complexity and documentation requirements.

What is the GST rate for businesses in India?

India's current primary GST rate slabs are 0% (exempt items), 5% (essential goods/services), 18% (standard rate), and 28% (luxury/sin goods) as of September 2025. The applicable rate depends on HSN classification for goods and SAC codes for services. Verify specific rates via the GST Council's official classification system.

How can I get a GST number for my business in India?

Apply online via gst.gov.in requiring PAN, business registration documents, proof of principal place of business, and Aadhaar authentication. Typical approval takes 3–7 working days for compliant applications with all documentation in order.

How does GST work for a business in India?

GST is charged on sales of goods and services, collected from customers, and remitted to the government after deducting input tax credits on eligible business purchases. This creates a value-added taxation chain, with periodic return filings required monthly or quarterly depending on turnover.

Is GST required for small businesses in India?

GST registration is mandatory once aggregate turnover exceeds INR 40 lakh (goods) or INR 20 lakh (services) in normal states. Inter-state suppliers, e-commerce sellers, and digital service providers must register regardless of turnover. For Singapore companies making cross-border or inter-state supplies into India, these thresholds do not apply — registration is required from the outset.

Can a Singapore company register for GST in India without setting up a local entity?

Yes. Singapore companies can register as a Non-Resident Taxable Person (NRTP) for up to 90 days (extendable once) or under the OIDAR category for digital services. For ongoing operations, establishing an Indian subsidiary or branch with standard GST registration provides greater stability and compliance coverage.

Ready to navigate GST registration for your India expansion? VJM Global's experienced team has assisted businesses from Singapore, USA, UK, and Australia with Indian GST registration, ongoing compliance, and strategic tax planning. Contact us at info@vjmglobal.com or call +91 9213397070 for expert consultation tailored to Singapore companies entering the Indian market.