Introduction

If your business imports goods into the UK, cash flow is likely your biggest VAT headache. Before Brexit, importers paid VAT upfront at the border, then waited weeks or months to reclaim it on their next return. Since 1 January 2021, that burden has intensified — and for businesses with tight working capital, the gap between payment and recovery can be genuinely damaging.

Postponed VAT Accounting (PVA) is HMRC's solution: declare and reclaim import VAT on the same return, with no upfront payment required. This guide covers how PVA works, who can use it, and how to avoid the errors that catch businesses out.

What Is Postponed VAT Accounting and Why Does It Matter?

Postponed VAT Accounting (PVA) lets UK VAT-registered businesses declare and reclaim import VAT on the same VAT return, rather than paying it at the border.

Instead of transferring funds at the port of entry or customs warehouse, businesses report the VAT due and recover it in the same accounting period — a net-zero cash transaction for most importers.

The Pre-PVA Problem

Before PVA, businesses paid import VAT upfront at customs and waited until their next VAT return to reclaim it. This tied up working capital — a real problem for high-volume importers and businesses operating on tight cash flow margins.

For example, an importer bringing in £100,000 worth of goods monthly had to front £20,000 in VAT at the border and wait weeks to recover it.

The £135 Threshold

VAT applies to all goods imported into the UK (including from the EU post-Brexit) when the consignment value exceeds £135. Below that threshold, the rules differ by transaction type:

- B2B imports (£135 or less): The UK business recipient accounts for VAT via reverse charge, not the overseas seller.

- B2C sales at this threshold: The overseas seller charges VAT at the point of sale.

How PVA Works on Your VAT Return

PVA works similarly to the EU reverse charge mechanism. Import VAT is entered as output VAT in Box 1 and input VAT in Box 4 on the same return — resulting in no net payment for businesses with full VAT recovery.

Businesses with partial recovery (those engaged in exempt activities) must apply the correct recovery percentage rather than claiming 100% back.

The Scale of UK Imports

UK goods imports totalled approximately £603.1 billion in 2025 — a £15.3 billion increase on 2024. In Q4 2025 alone, EU imports reached roughly £79.8 billion, with non-EU imports at £69.7 billion.

HMRC doesn't publish standalone PVA usage figures, but that import volume makes clear why cash flow relief through this scheme matters for thousands of UK businesses.

Who Can Use Postponed VAT Accounting in the UK?

Automatic Eligibility

PVA is available to any business registered for UK VAT — no application required. Eligibility is automatic provided goods are imported for business purposes.

Non-Established Taxable Persons (NETPs)

Businesses not established in the UK can also use PVA, but must appoint a customs agent or freight forwarder to handle customs declarations on their behalf. The agent must select PVA on the customs declaration and list the business as the consignee with its own UK VAT number.

Optional vs. Mandatory Use

PVA is optional for most imports. Businesses can pay import VAT upfront at the border and reclaim it via C79 certificates if they prefer. One notable update: as of June 2025, HMRC removed the mandatory PVA requirement that previously applied when customs declarations were deferred.

Two specific scenarios, however, sit outside standard rules and are worth understanding separately.

Northern Ireland Exception

For businesses importing into Northern Ireland from outside the EU, PVA remains mandatory for B2B imports valued under £135.

Flat Rate Scheme Consideration

Businesses on the VAT Flat Rate Scheme can use PVA, but must account for these imports outside their FRS turnover calculation. Per HMRC's Revenue and Customs Brief 3 (2022):

- Exclude import VAT accounted for using PVA from your flat rate turnover

- Add the VAT due on imports to Box 1 after completing your FRS calculation

- Report the corresponding input VAT in Box 4

How Postponed VAT Accounting Works: The Step-by-Step Process

Register with the Customs Declaration Service (CDS)

To use PVA, you must first be registered with the Customs Declaration Service. The older CHIEF system was fully decommissioned on 4 June 2024 and is no longer available.

CDS Registration Requirements:

- A Government Gateway user ID and password

- An Economic Operators Registration and Identification (EORI) number beginning with "GB"

- Subscription to the Customs Declaration Service

Complete the Customs Declaration Correctly

Three critical fields must be correctly completed on your customs declaration to activate PVA:

- EORI Number: Your GB EORI number must be entered

- VAT Registration Number: Enter your UK VAT registration number in Data Element 3/40 at header level

- Method of Payment: Under CDS, do NOT use method of payment 'G' in Data Element 4/8. MOP code G was the legacy CHIEF-era method and was deleted from CDS as of 25 May 2023.

Important: Many older guides still reference entering code "G" in Box 47e. This no longer applies under CDS. Simply entering your VAT number in Data Element 3/40 activates PVA.

Failure to enter these fields correctly means import VAT will be collected at the border instead of being postponed. Once the declaration is submitted with the correct details, HMRC automatically picks up the data and records the postponed VAT against your account.

HMRC Records the Postponed VAT and Issues Your Statement

HMRC records the postponed VAT against your business's account using the VAT number entered on the customs declaration. This data feeds into your Monthly Postponed Import VAT Statement (MPIVS), which is accessible via the CDS portal.

Your MPIVS is typically available from the 6th working day of the month following the import. It shows the total postponed VAT for each period, broken down by individual import entries. You use this figure — not an estimate — when completing Box 1 (VAT due on sales) and Box 4 (VAT reclaimed) of your VAT return.

Importer of Record Requirements

The business using PVA must be declared as the consignee on customs documents. If using a freight forwarder or customs agent, you must instruct them to:

- Select PVA on the declaration

- Enter your business's VAT number in Data Element 3/40 (not the agent's own details)

- Confirm the declaration references your GB EORI number as consignee

This distinction matters. If your agent inadvertently enters their own VAT details, the postponed VAT will be recorded against their account — not yours — and you'll have no valid basis to reclaim it on your VAT return.

Understanding Import VAT Calculation

Import VAT is calculated on the customs value of goods, which includes:

- Cost of goods

- Insurance and freight to first UK destination

- Any applicable customs duty

- Any excise duty or other import charges (excluding VAT itself)

Per HMRC guidance, businesses should not attempt to estimate import VAT based solely on the supplier invoice, as this will likely be inaccurate. The customs value typically exceeds the invoice value.

Completing Your VAT Return Under Postponed VAT Accounting

Three specific VAT return boxes must be completed when using PVA. Record these entries in your bookkeeping or accounting software — they cannot be manually overridden in Making Tax Digital (MTD) compliant submissions.

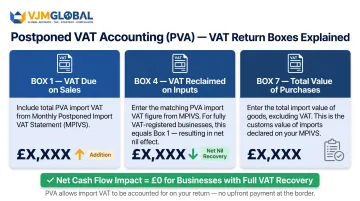

Box 1 – VAT Due on Sales and Other Outputs

Box 1 should include the total VAT due on imports accounted for through PVA during the return period. This figure is taken directly from your MPIVS, or estimated if the statement is not yet available due to a deferred declaration.

For FRS businesses, this import VAT is added to Box 1 after completing the standard FRS calculation.

Box 4 – VAT Reclaimed on Purchases and Other Inputs

Box 4 should include the corresponding VAT reclaimed on those same PVA imports. The figure matches Box 1 for businesses with full VAT recovery, resulting in a net nil cash impact.

Businesses with partial recovery (those with exempt activities) must apply the correct recovery percentage to determine the reclaimable amount.

Box 7 – Total Value of Purchases and Inputs

Box 7 requires the total value of all imported goods (excluding VAT) as shown on the MPIVS. This ensures HMRC has an accurate picture of total import activity even when no net VAT is due.

When Statements Are Not Available

If you've deferred your customs declaration, you may not have an MPIVS available when completing your VAT return. In this case:

- Estimate the import VAT as precisely as available data allows using the customs value (not just the supplier invoice)

- Include the estimate in Boxes 1, 4, and 7

- Correct the figure on the subsequent VAT return once the actual MPIVS is available

HMRC states: "As long as you take reasonable care to follow this guidance, there will be no penalty for errors."

Getting these entries right matters — especially for businesses with partial VAT recovery or deferred declarations. VJM Global's UK tax advisory team helps businesses configure their accounting systems for PVA compliance and complete VAT returns accurately under MTD requirements.

Accessing and Managing Your Monthly Postponed Import VAT Statements

How to Access MPIVS

Monthly postponed import VAT statements are generated by HMRC and made available through the CDS portal. Statements are typically available by the 10th working day of each month, covering all PVA imports from the previous month.

Access Requirements:

- Log in via the CDS portal using your Government Gateway credentials

- Agents cannot access statements on behalf of clients — only the business itself can log in

Critical Six-Month Window

Statements are only available online for six months from their publication date. Download and store copies immediately as part of your VAT records. Once archived, statements can only be retrieved through HMRC's archived statement process — and failure to retain them can result in rejected VAT reclaims or compliance penalties.

VAT Group Member Scenario

If your business is part of a VAT group, the process works as follows:

- Each entity with an EORI number accesses its own MPIVS independently

- Each entity forwards its statement to the representative member

- The representative member consolidates all statements to complete the group VAT return

Special Scenarios and Common PVA Pitfalls to Avoid

Northern Ireland's Unique Position

Northern Ireland businesses are treated as part of the EU VAT area under the Protocol. This means:

Goods from EU Member States:

- Treated as intra-community acquisitions (not imports)

- PVA does not apply

- Report acquisition VAT in Box 2, input VAT in Box 4, and values in Boxes 7 and 9

Goods from Outside the EU:

- PVA is available and follows the same process as GB

- PVA is mandatory for B2B imports valued under £135

Most Common PVA Errors

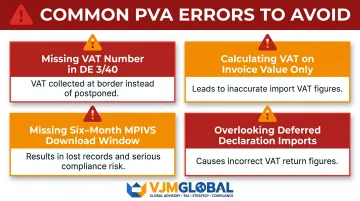

Missing VAT number in Data Element 3/40 — Not completing the customs declaration correctly results in VAT being collected at the border. Under CDS, entering your VAT registration number in Data Element 3/40 activates PVA; do not use method of payment code G.

Calculating VAT on invoice value only — Import VAT must be calculated on the full customs value (goods cost + insurance + freight + duty), not just the supplier's invoice amount. Using invoice value alone will produce inaccurate figures.

Missing the six-month MPIVS download window — Statements are only available for six months. Missing this window means losing access to critical records and potentially facing difficulties during HMRC audits.

Overlooking deferred declaration imports — When customs declarations are deferred, MPIVS data may not be available for the current VAT return. Estimate these imports on the current return and correct the figures once actual statements become available.

Excise Goods and Special Procedures

Beyond the common errors above, two specific scenarios require extra care due to rules that differ from standard PVA treatment.

Excise Goods

For goods subject to excise duty (alcohol, tobacco), you account for VAT when goods are released for home consumption rather than at declaration. This includes releases from excise warehouses after duty suspension.

Customs Special Procedures

Businesses using customs special procedures — such as bonded warehouses, inward processing, temporary admission, or duty suspension arrangements — should seek specialist advice to ensure correct PVA treatment. The timing and method of accounting can differ from standard import procedures.

Frequently Asked Questions

Is postponed VAT accounting mandatory in the UK?

PVA is optional for most imports — businesses can choose to pay VAT upfront at the border instead. However, as of June 2025, the previous mandatory requirement for deferred declarations has been removed. PVA remains mandatory only for B2B imports into Northern Ireland from outside the EU valued under £135.

What is the difference between postponed VAT accounting and deferred VAT?

Deferred VAT was a temporary COVID-era relief measure allowing businesses to delay VAT payments. PVA is a permanent post-Brexit import mechanism where VAT is declared and reclaimed on the same return — resulting in no net cash outflow for businesses that reclaim VAT in full.

How do I access my monthly postponed import VAT statement?

MPIVS statements are accessed via the HMRC Customs Declaration Service (CDS) portal using Government Gateway credentials. Statements are usually available by the 10th working day of each month and must be downloaded within six months of publication.

What happens if I cannot access my postponed import VAT statement?

If a statement is unavailable, estimate import VAT based on the customs value of goods and report it in Boxes 1 and 4 of the VAT return. Correct the figure on the next return once the actual statement is available — HMRC will not penalise reasonable estimates.

Can I use postponed VAT accounting if I am on the VAT Flat Rate Scheme?

Yes, FRS businesses can use PVA. Import VAT under PVA must be accounted for outside the FRS calculation and reported in Boxes 1 and 4 of the standard VAT return — not within the FRS turnover percentage.

Does postponed VAT accounting apply to goods imported into Northern Ireland from the EU?

No — Northern Ireland remains part of the EU VAT area, so goods arriving from EU member states are treated as intra-community acquisitions, not imports. PVA does not apply to these movements. PVA is only available for NI businesses importing from countries outside the EU.