Introduction

Many UK businesses struggle with knowing exactly when and how to register for VAT as they approach the £90,000 taxable turnover threshold. Miss the deadline, and HMRC can charge up to 15% of unpaid VAT for late registration errors, plus late payment interest currently running at 8.5%.

A VAT Registration Number (VRN) is a legal requirement for UK businesses meeting specific criteria, and obtaining one follows a defined process governed by HMRC.

This guide is for UK-based businesses approaching the registration threshold, newly incorporated companies, and overseas businesses planning to trade in the UK. Here's what you'll find inside: what a VAT registration number is, who needs one, the exact steps to apply in 2026, and your post-registration obligations — including the mandatory Making Tax Digital (MTD) requirements that kick in immediately.

Key Takeaways

- A UK VAT Registration Number is a unique 9-digit identifier required for businesses with taxable turnover above £90,000

- Online registration through HMRC's Government Gateway delivers your number within 14–30 working days for UK businesses

- Overseas businesses face longer processing times (10–12 weeks) and require additional documentation

- Once registered, you must charge VAT, file quarterly returns, and display your VRN on all invoices

- Voluntary registration lets businesses below the threshold reclaim VAT on purchases

What Is a UK VAT Registration Number?

A VAT Registration Number (VRN) is the unique 9-digit identifier HMRC issues to businesses registered for Value Added Tax in the UK. It serves four core purposes:

- Tracks your VAT obligations with HMRC

- Allows you to charge VAT on taxable sales

- Enables you to reclaim VAT on business purchases

- Identifies you when filing VAT returns

Only HMRC issues VRNs in the UK. You'll also hear this called a VAT number or VRN—these terms are interchangeable. The number appears on your VAT registration certificate, which HMRC sends by post after processing your application.

How a UK VAT Number Is Structured

UK VAT numbers follow a specific 9-digit format, typically displayed in blocks: 123 4567 89. In international trade contexts, the number carries the "GB" prefix (e.g., GB 123 4567 89). The GB designation is not part of the domestic number itself. It's the ISO country code used for cross-border transactions.

Post-Brexit, this distinction matters more than ever. UK VAT numbers are no longer validated through the EU's VIES system, which ceased recognising GB numbers on 1 January 2021. HMRC now operates its own verification system at gov.uk/check-uk-vat-number, which replaced the EU tool for checking UK VAT registration validity.

VAT Number vs. Other UK Business Identifiers

Three separate numbers serve three distinct purposes for UK businesses:

- VAT Registration Number (VRN): 9-digit tax identifier issued by HMRC for VAT purposes only

- Company Registration Number (CRN): Issued by Companies House when you incorporate a limited company; this identifies your legal entity but has nothing to do with tax

- Unique Taxpayer Reference (UTR): 10-digit number issued by HMRC for income tax or corporation tax purposes, appearing on Self Assessment (SA100) or corporation tax (CT600) returns

These numbers cannot be substituted for one another. When dealing with HMRC on VAT matters, always quote your VRN — using your UTR or CRN in its place will cause processing delays.

Who Needs to Register for VAT in the UK in 2026?

Mandatory registration applies when your VAT-taxable turnover exceeds £90,000 in any rolling 12-month period, or when you expect to exceed this threshold in the next 30 days alone. This £90,000 threshold was raised from £85,000 on 1 April 2024 and remains unchanged for 2025-2026.

Two registration triggers exist:

- Backward-looking test: If your total taxable turnover for the last 12 months exceeds £90,000, register within 30 days of the month-end when you crossed the threshold. Your effective date is the first day of the second month after the breach.

- Forward-looking test: If you expect turnover to exceed £90,000 in the next 30 days alone, register before that 30-day period ends. Your effective date is the day you first anticipated exceeding the threshold.

Not yet at £90,000? Voluntary registration is still an option. It makes sense when you want to reclaim input VAT on business purchases or signal credibility to B2B customers. That said, it adds compliance obligations from day one — including quarterly VAT returns and Making Tax Digital (MTD) software requirements.

Overseas businesses face entirely different rules. Non-Established Taxable Persons (NETPs) must register for UK VAT regardless of turnover if they supply goods or services to UK customers or hold stock in the UK.

The £90,000 threshold simply does not apply to NETPs. Even a single taxable supply to a UK customer triggers mandatory registration. Post-Brexit, EU sellers are treated as overseas businesses and must follow the same NETP rules.

How to Get a VAT Registration Number in the UK

Most businesses register online through HMRC's Government Gateway. The sections below cover what documents you need, how to complete the application, and what to do while you wait for your certificate.

Documents and Information You Need

For limited companies:

- Company Registration Number (CRN) from Companies House

- Unique Taxpayer Reference (UTR)

- Business bank account details

- Annual turnover details and estimated taxable turnover for the next 12 months

- Corporation Tax, Self Assessment, and PAYE information

For sole traders and partnerships:

- National Insurance number

- Valid identity document (passport or driving licence)

- Bank account details

- UTR (if available)

- Annual turnover details and estimated taxable turnover for the next 12 months

- Supporting documents such as P60 or payslips

For overseas and non-UK businesses:

Overseas applicants face significantly higher documentation requirements. You'll typically need passport copies, proof of UK business activity, and evidence of VAT compliance in your home country. Incomplete applications are the leading cause of delays or rejections for non-UK businesses.

Foreign businesses from the USA, Australia, or India often find this process more involved than expected. VJM Global has helped 250+ UK businesses—including many international entrants—ensure their applications are correctly prepared and submitted from the start.

Registering Online: Step-by-Step

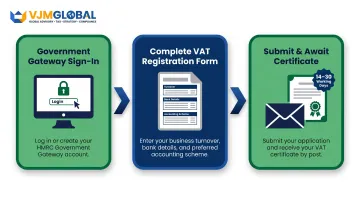

Sign in to or create a Government Gateway account at the HMRC VAT registration portal. First-time users will need to set up sign-in credentials first.

Complete the VAT registration form by entering business details, turnover figures, bank account information, and your chosen VAT accounting scheme (if applicable). The form can be saved and completed in stages at any point.

Submit the application and await HMRC's review. UK businesses typically receive their VAT registration certificate within 14-30 working days, though processing times can be unpredictable. The certificate contains your 9-digit VAT number and the effective date of registration.

When You Cannot Register Online

HMRC requires paper registration using form VAT1 in specific scenarios only:

- Limited liability partnerships registering as representative members of a VAT group

- Registering separate divisions of a corporate body under different VAT numbers

- Overseas partnerships

- Local authorities, parish, or district councils

- Applying for a registration exception

- Insolvency practitioners registering a business

- Digital exclusion due to age, disability, location, religious grounds, or lack of internet access

You cannot simply download VAT1—you must first call HMRC's VAT general enquiries helpline and confirm you qualify for paper registration.

What to Do While Waiting for Your VAT Number

There are a few practical steps to take during the waiting period:

- Hold off on showing a VAT number on invoices until your certificate arrives — you cannot display one before then

- Adjust your prices to account for the VAT you'll owe once registration is confirmed

- Reissue invoices once your number arrives, showing the VAT amount separately so customers can reclaim it on their own returns

Your Obligations After Getting a VAT Number

Charging and Displaying VAT

Your VRN must appear on all invoices, receipts, and public-facing business communications including websites and marketing materials. HMRC mandates that every VAT invoice includes:

- Your VAT registration number and a unique sequential invoice number

- The customer's name and address

- A description of the goods or services supplied

- The total VAT chargeable

UK VAT rates in 2026:

- Standard rate (20%): Most goods and services

- Reduced rate (5%): Some goods and services, such as children's car seats and home energy

- Zero rate (0%): Zero-rated items like most food and children's clothes

Applying the correct rate is critical: mistakes trigger penalties and compliance reviews.

Filing VAT Returns and Making Tax Digital

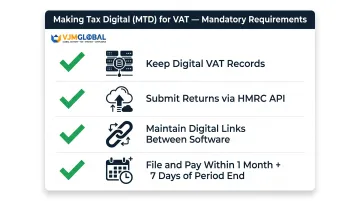

VAT-registered businesses must submit VAT returns, typically quarterly. From the date of registration, Making Tax Digital for VAT is mandatory—you must use HMRC-compatible software to keep digital records and file returns.

MTD requirements include:

- Keeping digital VAT records using functional compatible software

- Submitting VAT returns via HMRC's API platform

- Ensuring digital links between software programs (manual transfers are not permitted)

- Filing returns and making payments within one calendar month and 7 days of each accounting period end

Record-Keeping and Penalties

HMRC enforces penalties through three separate mechanisms since January 2023:

Late Filing Penalties (Points-Based System)

| Filing frequency | Penalty threshold |

|---|---|

| Quarterly filers | 4 points |

| Monthly filers | 5 points |

| Annual filers | 2 points |

Each late submission earns one point. Reaching the threshold triggers a £200 penalty, with further £200 penalties for each subsequent late return.

Late Payment Penalties

- Days 1-15: No penalty, but interest accrues at 8.5% (Bank of England base rate + 4%)

- Day 16-30: 2% penalty on outstanding VAT at day 15

- Day 31+: Additional 4% annual penalty on outstanding amount

Late Registration Penalties

HMRC calculates failure-to-notify penalties as a percentage of "potential lost revenue," meaning the VAT you should have paid had you registered on time. Penalties range from 0% to 100% depending on whether the failure was careless, deliberate, or disclosed unprompted.

Common Mistakes and Misconceptions When Registering for VAT

These are the errors that most commonly delay registrations or trigger penalties:

- Registration date vs. application date: Your VAT obligations begin on the "effective date of registration," not when you receive your certificate. For businesses that crossed the threshold in the past 12 months, that date is typically the first day of the second month after the breach — VAT is owed from that point forward.

- Incomplete documentation for overseas businesses: Non-UK businesses frequently submit applications missing required evidence, since the documentation standards differ considerably from UK company requirements. This is the leading cause of delays and outright rejections for overseas applicants.

- Assuming HMRC registers you automatically: HMRC does not trigger registration when you cross the £90,000 threshold. You must register proactively within 30 days. Late registration penalties are calculated from when you should have registered, not from your actual application date.

Frequently Asked Questions

What is a GST registration number in the UK?

The UK does not use GST (Goods and Services Tax). The equivalent consumption tax is Value Added Tax (VAT), and the identifier issued by HMRC is called a VAT Registration Number. GST is used in countries like Australia, Canada, and India.

Is a VAT number the same as a GST registration number?

VAT and GST are functionally similar consumption taxes, but they apply in different countries and are issued by separate national tax authorities. A UK VAT number is not interchangeable with a GST registration number from Australia, India, or Canada.

Is a VAT registration number the same as an EIN?

No. An EIN (Employer Identification Number) is a US tax identifier issued by the IRS for federal tax purposes. The UK has no direct equivalent to the EIN, though the UTR (Unique Taxpayer Reference) serves a comparable role for income and corporation tax identification.

How long does it take to get a VAT registration number in the UK?

UK businesses typically receive their VAT registration certificate within 14-30 working days of a complete online application. Overseas businesses should allow 10-12 weeks. HMRC may take longer during busy periods, and incomplete applications cause further delays.

Can I trade without a VAT registration number?

Businesses with taxable turnover below £90,000 can trade without registering. However, businesses above this threshold must register and face penalties for failing to do so. Unregistered businesses cannot charge VAT to customers or reclaim VAT on business purchases.

How do I check or verify a UK VAT number?

UK VAT numbers can be verified using HMRC's official checker at gov.uk/check-uk-vat-number. Businesses should verify supplier VAT numbers before reclaiming input VAT, as invalid numbers can invalidate VAT claims and trigger compliance reviews.