Introduction

Many Singapore businesses entering the UAE face an AED 10,000 penalty before they've fully settled in — not from complex transactions, but from a straightforward registration requirement they assumed didn't apply to them. UAE VAT registration with the Federal Tax Authority (FTA) is often mandatory from the very first invoice for non-resident businesses.

Unlike Singapore's GST framework administered by IRAS, the UAE VAT system treats non-resident foreign businesses differently from UAE-domiciled entities. This distinction carries real compliance consequences that many first-time entrants miss.

The central misconception Singapore business owners bring to the UAE is assuming that registration thresholds work the same way they do under Singapore's GST regime. They don't. For non-residents, the AED 375,000 threshold simply doesn't apply — registration may be mandatory before a single dirham of recurring revenue is earned.

This article explains what UAE VAT is, when Singapore businesses are legally required to register, how the registration process works, what documents the FTA expects, and the common mistakes that lead to AED 10,000 penalties and retroactive tax liabilities.

Key Takeaways

- UAE VAT is a 5% consumption tax effective since January 2018, overseen by the Federal Tax Authority

- Non-resident businesses face no minimum turnover threshold—registration is required from the first taxable supply if no UAE-registered party accounts for the VAT

- Voluntary registration is available when taxable expenses exceed AED 187,500

- Registration is completed online via the EmaraTax portal; TRN approval typically takes 20 business days

- Late registration triggers an AED 10,000 penalty plus back-tax liability on all prior supplies

What Is UAE VAT?

UAE VAT is a 5% indirect consumption tax levied at each stage of the supply chain, introduced on 1 January 2018 under Federal Decree-Law No. 8 of 2017. Businesses collect VAT from customers and remit it to the FTA, while reclaiming VAT paid on business purchases as input tax credits.

Key supply categories:

| Category | Rate | Examples |

|---|---|---|

| Standard-rated | 5% | Most goods and services supplied in the UAE |

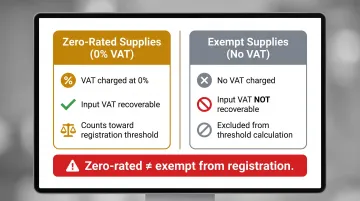

| Zero-rated | 0% | Exports outside the GCC, international transport, first supply of residential property, qualifying healthcare and education |

| Exempt | N/A | Certain financial services, subsequent residential property sales, bare land, domestic passenger transport |

Zero-rated supplies are not exempt from registration obligations. Businesses making only zero-rated supplies still count those revenues when assessing registration thresholds and may still need to register — though they can apply for an FTA exception if 100% of supplies are zero-rated.

How UAE VAT Differs from Singapore GST

The supply categories above follow the same broad logic as Singapore GST, but the administrative rules differ in ways that catch Singapore businesses off guard:

- Regulatory authority: FTA (UAE) vs. IRAS (Singapore)

- Non-resident treatment: No registration threshold in UAE for non-residents; Singapore applies the S$1 million threshold to most overseas businesses

- Filing cycles: Quarterly or monthly in UAE vs. quarterly in Singapore

- Reverse charge rules: More expansive application in UAE for B2B services

Why and When Singapore Businesses Must Register for UAE VAT

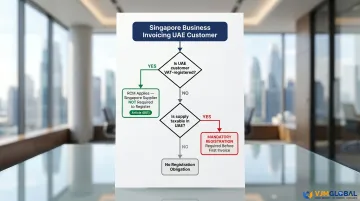

The Zero-Threshold Rule for Non-Residents

Here is the rule that catches most Singapore businesses by surprise: UAE-resident businesses must register when taxable supplies exceed AED 375,000 over 12 months. Non-resident businesses—including Singapore companies—face no such threshold.

Article 13(2) of Federal Decree-Law No. 8 of 2017 states that any person without a place of residence in the UAE or another GCC Implementing State must register if they make taxable supplies and no other person is obligated to pay the VAT on those supplies. The FTA website explicitly confirms: "This threshold is not applicable to foreign businesses."

In practice, if a Singapore company invoices even one unregistered UAE customer for AED 5,000 worth of consulting services, it is legally required to register before issuing that invoice. There is no grace period and no minimum revenue buffer.

The Reverse Charge Mechanism (RCM) Exception

The key relief mechanism for most B2B Singapore suppliers is the Reverse Charge Mechanism (RCM) under Article 48(1). When a UAE VAT-registered customer imports services from abroad, they self-account for the VAT as if they made the supply themselves.

In this scenario, the Singapore supplier is relieved of the registration obligation because "another person is obligated to pay the Due Tax."

Before invoicing any UAE customer, verify their VAT registration status. If they are registered and will apply RCM, you do not need to register. If they are not registered (or are a consumer), you do.

Voluntary Registration Pathway

Singapore businesses not yet making taxable UAE supplies can still register voluntarily if:

- Their taxable expenses in the UAE exceeded AED 187,500 in the previous 12 months, or

- They reasonably expect to exceed this threshold within the next 30 days

Registering early offers several practical advantages:

- Recover input VAT on UAE setup costs (office deposits, legal fees, marketing)

- Establish credibility with UAE B2B partners and government tender processes

- Avoid last-minute registration delays when the first customer contract materializes

Free Zone Setup Scenario

Many Singapore businesses enter the UAE through a Designated Zone (DZ) entity, a type of UAE free zone. Goods supplied within DZs may be treated as outside the UAE for VAT purposes.

Services are different. Under Executive Regulation Article 51(6), services supplied within DZs are treated as inside the UAE.

A Singapore software consultancy operating from Dubai Internet City and selling services to UAE mainland customers is making standard-rated supplies at 5%, with the same registration obligations as any other supplier. VAT registration requirements are separate from the free zone license.

What Counts as "Taxable Supplies"

For threshold calculations, include:

- Standard-rated (5%) supplies

- Zero-rated (0%) supplies

- Reverse charge imports (B2B services where the UAE customer accounts for VAT)

Exempt supplies are excluded from the calculation. These include certain financial services, bare land, and subsequent residential property sales.

This distinction matters for Singapore businesses with mixed revenue streams. A logistics provider exporting goods to UAE customers (zero-rated) while also providing local warehousing services (standard-rated) must count both revenue streams when assessing registration obligations.

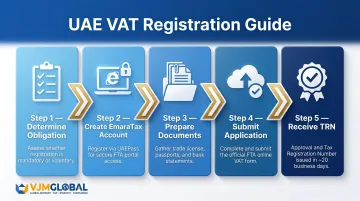

Step-by-Step UAE VAT Registration Process for Singapore Businesses

VAT registration is completed entirely online through the FTA's EmaraTax portal. Singapore businesses must create an account, submit supporting documents, and wait for FTA review before receiving a Tax Registration Number (TRN)—which must appear on all UAE tax invoices. Processing typically takes 20 business days.

Step 1: Determine Registration Obligation

Before starting the application, assess whether you face mandatory or voluntary registration:

Mandatory: Non-resident making taxable supplies with no UAE-registered party accounting for VAT → register before the first supply

Voluntary: Taxable expenses or anticipated supplies exceed AED 187,500 → register to recover input tax

For mandatory cases, timing is critical: complete registration before issuing the first invoice. For voluntary cases, confirm your expense documentation supports the AED 187,500 threshold claim.

Step 2: Create an EmaraTax Account and Prepare Documentation

Log into the EmaraTax portal and create a user account. Authentication requires UAEPass, the UAE government's digital identity platform.

Before submitting, complete these three preparatory steps:

- Appoint a Tax Agent (if you have no UAE resident representative) — not legally required, but reduces FTA queries and processing delays

- Gather incorporation documents from Singapore's ACRA: BizFile extract or certificate of incorporation

- Collect financial records supporting your turnover declaration or expense threshold claim

Step 3: Complete and Submit the VAT Registration Application

Navigate to the VAT Registration service within EmaraTax and complete the online form. Key sections include:

- Legal entity proof: Company name, ACRA incorporation documents, and nature of activities

- Revenue declaration: Historical revenue figures or forward projections

- Banking information: Account number, IBAN, bank name, and branch

- Signatory details: Authorised representative's passport and contact information

Singapore-specific note: Instead of a UAE trade license, submit incorporation documents from Singapore's ACRA (Accounting and Corporate Regulatory Authority) as your legal entity proof. Acceptable documents include the BizFile extract or certificate of incorporation.

Step 4: Await FTA Review and TRN Issuance

The FTA reviews applications within approximately 20 business days. During this period, the FTA may request additional clarifications or supporting documents.

Critical rule: Do not issue VAT invoices or make taxable UAE supplies (in mandatory registration cases) before receiving your TRN.

VJM Global works with Singapore companies to prepare complete VAT registration applications for UAE submission — covering document preparation, FTA correspondence, and cross-border compliance across 15+ industries. A well-prepared application typically clears FTA review without additional queries.

Step 5: Post-Registration Compliance Obligations

Once registered, your obligations include:

- Tax invoices: Issue UAE-compliant invoices with your TRN

- VAT returns: File quarterly or monthly (as allocated by the FTA)

- Record retention: Maintain accounting records for at least 5 years

- Remittance: Pay net VAT due by the return deadline

2026 update: A 5-year limitation now applies to excess input VAT refund claims under amended Article 74(3). Businesses with parked VAT credits from tax years 2018–2020 must submit refund requests by 31 December 2026 under the transition rule — after this date, unclaimed balances expire permanently.

Documents Required for UAE VAT Registration

Non-resident Singapore businesses must provide the following core documents:

Essential documents:

- Singapore certificate of incorporation (ACRA BizFile extract or incorporation certificate)

- Company constitution or memorandum and articles of association

- Passport copies of all directors, shareholders, and authorized signatories

- Proof of business address — UAE or Singapore office lease, utility bill, or company letterhead

- Bank account details: IBAN, account number, bank name, and branch

- Turnover declaration or financial projections, signed and stamped on company letterhead

Singapore-specific considerations:

Singapore businesses without a UAE subsidiary or branch won't hold a UAE trade license. The FTA accepts home-country incorporation documents in its place.

Requirements around notarization or apostille can vary by application. Confirm the current FTA position — or work with a UAE tax agent — before submitting to avoid delays.

Additional documents (if applicable):

- UAE trade license (if you have a UAE subsidiary or branch)

- Customs registration letter (if you import/export goods)

- Sample contracts or invoices (service-based businesses may need to demonstrate the nature and location of supply)

Common Mistakes Singapore Businesses Make with UAE VAT Registration

Mistakenly Assuming the AED 375,000 Threshold Applies

This is the most consequential error Singapore business owners make. The AED 375,000 mandatory registration threshold applies only to UAE-resident businesses. For non-residents, there is no threshold—any single taxable supply in the UAE triggers registration if the UAE customer is not VAT-registered.

Many Singapore companies familiar with the S$1 million GST threshold back home assume the UAE works similarly. It doesn't. A Singapore consulting firm invoicing a UAE startup for AED 10,000 in advisory services must register if that startup is not VAT-registered — even if this is the Singapore firm's first-ever UAE customer.

Delaying Registration Because the Business Is "New" or "Not Yet Profitable"

The registration obligation is tied to the nature and location of supply, not profitability or business maturity. A Singapore company may be VAT-liable in the UAE from its first invoice to a UAE consumer, regardless of whether the Singapore entity is two months old or twenty years old.

Overlooked benefit: New businesses that register voluntarily early can recover input VAT on UAE setup costs—legal fees, office deposits, marketing expenses. This can recover thousands of dirhams in otherwise sunk costs.

Confusing Zero-Rated Supplies with Exemption from Registration

Some Singapore exporters believe that because their goods are zero-rated upon export to the UAE, they are exempt from registration. This is incorrect.

The distinction:

- Zero-rated means VAT is charged at 0%, and the business can still recover input VAT. Zero-rated supplies count as taxable supplies for threshold purposes and may still trigger registration.

- Exempt means no VAT is charged, and the business cannot recover input VAT. Only businesses making exclusively exempt supplies are relieved from registration — and even they may need to apply for formal exemption from the FTA.

A Singapore freight forwarder exporting goods outside the GCC (zero-rated) while also providing local warehousing services in the UAE (standard-rated at 5%) cannot claim exemption based on the zero-rated exports alone.

Frequently Asked Questions

How much does it cost to register for VAT in the UAE?

VAT registration through the FTA is free of charge—the FTA does not charge a fee. However, late registration incurs an AED 10,000 penalty, and many businesses engage a tax agent or advisory firm to manage the process, which carries professional fees.

How to register VAT for a new company in the UAE?

Registration is completed online through the FTA's EmaraTax portal. Create an account using UAEPass authentication, complete the VAT registration application with supporting documents (incorporation certificate, passport copies, bank details), and wait approximately 20 business days for the FTA to review and issue your TRN.

What is the minimum turnover to register for VAT in the UAE?

For UAE-resident businesses, mandatory registration applies when taxable supplies exceed AED 375,000 per year; voluntary registration is available from AED 187,500. Crucially, these thresholds do not apply to non-resident (including Singapore) businesses—they must register before making any taxable supply in the UAE if no UAE-registered party accounts for the VAT via reverse charge.

Who is exempted from VAT in the UAE?

Businesses making only VAT-exempt supplies—such as certain financial services, bare land sales, domestic passenger transport, and residential property resales—are not required to register. Those supplying only zero-rated goods or services may request a registration exemption under Article 15, but if granted, they forfeit the right to recover input tax.

What is the new VAT rule in UAE 2026?

Effective 1 January 2026, a 5-year time limitation was introduced on claims for excess input VAT refunds under amended Article 74(3). Businesses with outstanding refundable VAT balances from tax years 2018-2020 must submit refund requests by 31 December 2026 under the transitional provision—after this date, unclaimed credits expire permanently.

What happens if a Singapore business misses the VAT registration deadline in the UAE?

Failure to register on time results in an AED 10,000 penalty under Cabinet Decision No. 49 of 2021. The business also remains liable to remit VAT on all taxable supplies made during the unregistered period under Executive Regulation Article 7(7)—back-tax exposure that cannot be recovered from customers retroactively.

Final Word

Singapore businesses entering the UAE market face a VAT compliance framework that operates on fundamentally different principles than Singapore's GST regime. The absence of a minimum registration threshold for non-residents means that even small-scale suppliers can face immediate registration obligations—and the AED 10,000 penalty for late registration, combined with retroactive tax liability, makes early assessment critical.

If your Singapore business is expanding into the UAE and you're uncertain whether you need to register, verify your customers' VAT status before invoicing, understand whether the Reverse Charge Mechanism applies, and consider voluntary registration if you're incurring significant UAE expenses. Engaging experienced cross-border tax advisors—such as VJM Global, which supports businesses across USA, UK, Australia, and UAE markets—can help you navigate the FTA's requirements, prepare complete applications, and establish compliant processes from day one.