Introduction

Many Singapore businesses setting up in Dubai free zones share the same misconception: that "free zone" status means complete exemption from all taxes, including VAT. That assumption has real costs — non-compliance penalties under the UAE Federal Tax Authority can reach AED 10,000 for a first registration failure alone, with recurring fines on top.

Free zones do offer real advantages: 100% foreign ownership, customs duty exemptions, and faster company registration. But UAE VAT, introduced in 2018 at 5%, applies to most transactions regardless of where your company is registered. This matters especially for Singapore operators, where GST now sits at 9% and teams often assume Dubai offers blanket tax relief.

This guide walks through how UAE VAT actually applies to free zone companies — what triggers registration, which transactions are taxable, and where Singapore businesses most often get caught out.

Key Takeaways

- UAE VAT applies at 5% to most goods and services, even in Dubai free zones—"free zone" does not mean "VAT-free"

- Only zones classified as "Designated Zones" receive special VAT treatment for goods; services always follow standard rules

- Register for UAE VAT if taxable supplies exceed AED 375,000 annually (voluntary registration from AED 187,500)

- VAT treatment differs based on goods vs. services and whether transactions are within, between, or outside free zones

What Is UAE VAT and How Does It Apply to Free Zone Companies?

The UAE introduced VAT on 1 January 2018 at a standard rate of 5%, covering most commercial transactions including sales, imports, and services rendered within the country. While this is lower than Singapore's current 9% GST, it still means compliance obligations apply to foreign-owned businesses operating in the UAE.

UAE VAT falls into three categories, each with different implications for your free zone company:

- Standard-rated (5%): Most goods and services sold in the UAE

- Zero-rated (0%): Certain exports and designated supplies; businesses can recover input VAT

- Exempt: No VAT charged and no right to recover input VAT (e.g., certain financial services, residential property)

Free zone companies are not automatically outside the UAE VAT system. As legal entities operating within UAE territory, their VAT obligations depend on the nature of their transactions and whether their zone qualifies as a "Designated Zone."

The FTA's Designated Zones VAT Guide states explicitly: "For VAT purposes, both fenced and unfenced Free Zones are considered to be within the territorial scope of the UAE—and therefore subject to the normal UAE VAT rules—unless they fulfil the criteria to be treated as a Designated Zone."

In practice, this means your free zone company's VAT treatment hinges on a specific designation status — not simply on where it's registered.

Designated Zones vs. Regular Free Zones: Why the Distinction Matters

Under UAE VAT Law (Cabinet Decision No. 52 of 2017, Article 51), only specific free zones that meet defined criteria are classified as "Designated Zones" and treated as being outside UAE territory for VAT purposes on goods transactions. All other free zones are treated identically to the UAE mainland for VAT.

To Qualify as a Designated Zone, a Free Zone Must Have:

- A fenced geographic area with clearly defined boundaries

- Security and customs controls that monitor the entry and exit of people and goods

- Internal procedures for handling, storing, and processing goods within the zone

- An operator that complies with FTA-prescribed procedures and reporting requirements

Officially Recognised Dubai Designated Zones (9 zones):

- Jebel Ali Free Zone (JAFZA)

- Dubai Airport Free Zone (DAFZA)

- Dubai Cars and Automotive Zone (DUCAMZ)

- Dubai Textile City

- Free Zone Area in Al Quoz

- DAFZA Industrial Park Free Zone – Al Qusais

- Dubai Aviation City

- International Humanitarian City – Jebel Ali

- Dubai CommerCity

Major Dubai free zones outside the Designated Zone list:

- Dubai International Financial Centre (DIFC)

- Dubai Internet City (DIC)

- Dubai Silicon Oasis (DSO)

- Dubai Media City

- Dubai Multi Commodities Centre (DMCC)

Practical consequence for Singapore businesses: If your company operates in a non-designated free zone, you are treated identically to a UAE mainland company for all VAT purposes—there is no special VAT relief of any kind.

One more point worth flagging: even within a Designated Zone, the special VAT treatment covers goods transactions only. Services remain subject to standard UAE VAT rules regardless of which zone your business is in.

VAT Treatment by Transaction Type: What Singapore Businesses Need to Know

VAT treatment depends on three variables: whether your transaction involves goods or services, the location of your buyer/seller (within zone, another Designated Zone, UAE mainland, or outside UAE), and the intended end use of the goods.

Goods Transactions in Designated Zones

Between two Designated Zones (for further supply):

- VAT treatment: Outside the scope of VAT

- Example: A Singapore-owned trading company in Jebel Ali Free Zone supplies goods to another company in Dubai Airport Free Zone for re-export

- Conditions: Goods must not be released into circulation, used, or altered during transfer; must follow GCC Common Customs Law suspension rules

From Designated Zone to UAE mainland:

- VAT treatment: Treated as an import; standard 5% VAT applies

- Responsibility: The mainland buyer (importer of record) accounts for this VAT

From Designated Zone to outside UAE (exports):

- VAT treatment: Outside the scope of UAE VAT

- Relevance: Particularly important for Singapore businesses using Dubai as a re-export or distribution hub

Services Transactions in Free Zones

Unlike goods, services follow standard UAE VAT rules regardless of whether the provider sits inside a Designated Zone. Two scenarios determine your VAT position:

- Services within the UAE (including between free zone companies): 5% VAT applies. The FTA VAT Guide confirms that the place of supply is treated as within the UAE when standard rules point to a Designated Zone.

- Services exported outside the UAE: Zero-rated or out of scope, provided the recipient is outside the UAE and uses the service outside the UAE. Place of supply rules must still be applied carefully — see the FTA's guidance on zero-rating of export services for exact conditions.

VAT Registration Requirements for Singapore-Owned Free Zone Companies

Mandatory registration threshold: UAE VAT registration is required when taxable supplies and imports exceed AED 375,000 in the preceding 12 months or are expected to exceed this in the next 30 days.

Voluntary registration: Available from AED 187,500. Opting in allows input VAT recovery, which can benefit businesses purchasing goods and services locally.

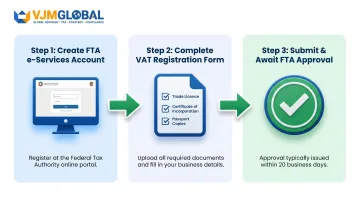

Registration Process

Step 1: Create an e-Services account on the FTA portal

Step 2: Complete the VAT registration form with:

- Business activity details

- Projected turnover

- Supporting documents:

- Trade licence

- Incorporation certificate

- Passport copies of shareholders

- Details of authorised signatories

Step 3: Submit and await FTA approval (typically 20 business days)

Post-Registration Obligations

Once registered, you must meet ongoing compliance obligations. These include:

Tax invoices: Issue VAT-compliant invoices including:

- VAT registration number

- Taxable amount

- VAT rate (5%)

- Total amount payable in AED

VAT returns: File quarterly (due by the 28th day following the end of each quarter)

Record retention: Maintain transaction records for minimum 5 years

Accounting: Track output VAT collected minus input VAT paid

Singapore businesses managing VAT remotely often work with cross-border tax advisors. VJM Global's international tax team handles UAE VAT registration and quarterly filing for foreign-owned entities, so compliance doesn't depend on local headcount.

Common Misconceptions Singapore Businesses Have About UAE Free Zone VAT

Misconception 1: "Free Zone" Means Tax-Free

Reality: "Free" in UAE free zones refers to customs duty exemptions and ownership freedoms, not blanket VAT exemption. Most transactions are subject to 5% VAT.

Misconception 2: Corporate Tax Status Equals VAT Exemption

Singapore businesses sometimes assume that because free zone companies can qualify for 0% corporate tax under the Qualifying Free Zone Person (QFZP) regime, they are also VAT-exempt.

Reality: Corporate tax and VAT are entirely separate frameworks. The UAE Corporate Tax Law (effective 2023) governs profit-based taxation, while VAT regulations govern transactional taxes — qualifying for one provides no relief under the other.

Misconception 3: Services Benefit from Designated Zone Relief

This confusion extends further for service-based businesses. Many Singapore-founded free zone companies — in consulting, technology, and professional services — incorrectly assume they benefit from Designated Zone VAT relief.

Reality: Designated Zone treatment is exclusively for goods. Services remain fully subject to UAE VAT rules, with 5% applying to services consumed within the UAE.

To be clear, Designated Zone relief applies only when:

- Goods are physically stored within the Designated Zone

- Transactions occur between businesses within the same zone

- Goods have not entered the UAE mainland for consumption

None of these conditions apply to service businesses, regardless of where they are registered.

Frequently Asked Questions

Is VAT applicable in UAE free zones?

Yes, VAT applies to free zone companies in the UAE. Only Designated Zones receive special treatment for goods transactions—not services. Businesses in all free zones must register if taxable supplies exceed AED 375,000 annually.

What is the difference between 0% VAT and exempt VAT?

Zero-rated (0%) supplies still allow businesses to claim input tax credits on expenses, improving cash flow. Exempt supplies have no VAT charged but provide no right to recover input VAT, significantly impacting cost recovery and profitability.

Is VAT applicable to services supplied outside the UAE?

Services supplied to recipients outside the UAE who consume them outside the UAE are generally zero-rated or out of scope. Place of supply rules are complex, so professional advice is recommended to ensure correct treatment.

What is the new VAT rule in the UAE in 2027?

UAE introduced mandatory e-invoicing effective 1 January 2027 for businesses with revenue above AED 50M, with phased rollout through July 2027 for smaller businesses. All businesses must appoint an Accredited Service Provider and comply with standardized electronic invoicing formats.

Do free zone companies in the UAE pay corporate tax?

Free zone companies may qualify for 0% corporate tax if they meet QFZP conditions under the UAE Corporate Tax Law (effective 2023). However, this is separate from VAT — all eligible companies must still assess their VAT obligations independently.

Is Dubai really 0% tax?

Dubai/UAE has no personal income tax and offers corporate tax advantages for qualifying free zone companies. However, 5% VAT applies to most business transactions. Singapore business owners should not treat "0% tax" claims as applying to all tax types—VAT compliance is mandatory and enforceable.

Need expert guidance on UAE VAT compliance for your Dubai free zone company? VJM Global's international tax team has helped businesses across Singapore, the UAE, USA, UK, and Australia manage their cross-border tax and VAT compliance obligations. Contact us at info@vjmglobal.com or call +91 9891576441 for a confidential consultation.