Introduction: UAE VAT for Singapore Businesses – What You Need to Know

Singapore-UAE trade ties have strengthened considerably, with bilateral merchandise trade reaching S$24 billion in 2024. The UAE ranks as Singapore's largest trading partner in the Middle East, making it a natural expansion destination. Yet many Singapore companies entering this market remain unprepared for its VAT obligations.

While Singapore businesses understand GST, the UAE's VAT framework operates differently in one critical way: non-resident businesses face immediate registration obligations with no minimum turnover threshold. This catches many Singapore companies off guard.

The UAE introduced VAT only in 2018, but enforcement is strict. Non-compliance triggers fines up to AED 10,000 for late registration and compound interest of 4% monthly on unpaid tax.

Those penalties accumulate fast. This guide covers UAE VAT registration requirements, filing obligations, compliance rules, and how to avoid costly missteps.

Key Takeaways

- UAE VAT is 5% (vs. Singapore's 9% GST), but non-resident businesses must register immediately with no turnover threshold

- Singapore businesses must appoint a UAE fiscal representative when registering for VAT, creating joint liability for compliance obligations

- Returns are due by the 28th of the following month — quarterly for most businesses, monthly above AED 150 million annual revenue

- Input VAT on purchases is fully reclaimable, reducing the effective tax burden below the 5% headline rate

UAE VAT Basics: What Singapore Businesses Need to Know

The UAE implemented VAT on 1 January 2018 under Federal Decree-Law No. 8 of 2017, administered by the Federal Tax Authority (FTA). The standard rate is 5%—nearly half of Singapore's current 9% GST rate.

UAE VAT is a consumption tax applied at each stage of the supply chain, not just at final sale. This structure mirrors Singapore's GST, but key differences exist in registration thresholds, non-resident treatment, and filing obligations.

How UAE VAT Works: Output vs. Input Tax

VAT operates through a credit mechanism:

- Output VAT: Tax you charge on sales to customers (5% on standard-rated supplies)

- Input VAT: Tax you pay on business purchases from suppliers

- Net VAT Payable: Output VAT minus Input VAT

Example: A Singapore technology company with a UAE branch sells software licences worth AED 100,000. They charge customers AED 5,000 in output VAT (5%). The company paid AED 2,000 input VAT on office rent, cloud hosting, and other business expenses. Net VAT payable to the FTA: AED 3,000 (AED 5,000 - AED 2,000).

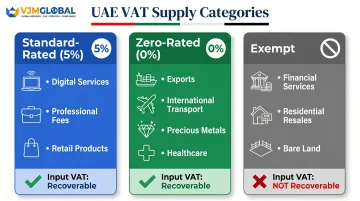

Supply Categories

Every transaction falls into one of three categories:

| Category | VAT Rate | Common Examples | Input VAT Recoverable? |

|---|---|---|---|

| Standard-rated | 5% | Digital services, professional fees, retail products | Yes |

| Zero-rated | 0% | Exports outside UAE/GCC, international transport, investment-grade precious metals, newly constructed residential property (first supply within 3 years), certain healthcare and education | Yes |

| Exempt | N/A | Financial services (interest, insurance premiums), residential property resales, bare land | No — becomes an unrecoverable cost |

Both standard-rated and zero-rated supplies count toward VAT registration thresholds. Exempt supplies do not — a distinction that directly affects whether your Singapore business needs to register.

UAE VAT Registration for Singapore Businesses

The Zero-Threshold Rule for Non-Residents

Here's the critical difference: UAE-resident businesses must register only when taxable supplies exceed AED 375,000 per year. Singapore businesses, classified as non-residents, must register immediately upon making any taxable supply in the UAE, regardless of amount.

According to the FTA's official guidance: "The mandatory registration threshold is AED 375,000. This threshold is not applicable to foreign businesses." Article 18 of the VAT Decree-Law requires non-residents to register if they make any taxable supplies in the UAE, provided no other person is obligated to pay the tax (meaning reverse charge doesn't apply).

This means a Singapore company making even a single taxable supply—whether a consulting engagement, a software subscription, or a product sale—must register before or at the time of that first transaction.

Registration Thresholds (For Context)

While these don't apply to Singapore businesses, understanding them provides useful context:

- Mandatory threshold: AED 375,000 (UAE residents only)

- Voluntary threshold: AED 187,500 (UAE residents only)

Registration applications must be submitted within 30 days of reaching these thresholds for UAE-resident businesses.

Fiscal Representative Requirement

Singapore companies registering for UAE VAT must appoint a UAE-based fiscal representative who becomes jointly and severally liable for VAT compliance. This requirement stems from Article 18 of the VAT Decree-Law and the Executive Regulations.

The fiscal representative is responsible for:

- Filing VAT returns and communicating with the FTA on your behalf

- Accepting joint liability for any VAT due, penalties, or compliance obligations

Choose a UAE-licensed tax agent or international accounting firm with a UAE presence. Engaging a reputable advisor early prevents compliance gaps before your first taxable transaction.

Registration Process

Step 1: Prepare required documents

- Valid trade license or business registration certificate

- Passport copies of authorized signatories

- Detailed description of business activities in the UAE

- UAE bank account details (or proof of application)

- Projected annual revenue from UAE operations

- Confirmation of taxable supplies

Step 2: Set up UAEPass access Registration requires a UAEPass digital identity. Create one at selfcare.uaepass.ae.

Step 3: Submit online application Complete the registration via the FTA EmaraTax portal. The portal guides you through required fields, including emirate breakdown of supplies and fiscal representative details.

Step 4: Await approval The FTA typically processes applications within 20 business days. Upon approval, you receive a unique 15-digit Tax Registration Number (TRN) and digital VAT certificate.

Free Zone Companies

Singapore businesses that establish UAE free zone entities face the same VAT obligations as mainland companies. The location doesn't grant exemption from VAT registration or compliance.

However, 27 Designated Zones defined under Cabinet Decision No. 59 of 2017 receive special treatment for goods:

- Goods movement between Designated Zones: outside VAT scope

- Goods from Designated Zone to mainland: treated as import, triggering 5% VAT

- Exports from Designated Zone outside UAE: zero-rated

- Services within Designated Zones: still taxed at 5%

Singapore businesses setting up in Dubai International Financial Centre, Jebel Ali Free Zone, or other free zones should verify whether their zone qualifies as a Designated Zone and understand implications for both goods and services.

UAE VAT Filing, Returns, and Invoicing Requirements

Filing Frequency and Deadlines

Most businesses file quarterly. Those with annual taxable revenue exceeding AED 150 million must file monthly.

All returns and payments are due by the 28th of the month following the tax period. For example:

- Q1 (January-March) return: due 28 April

- Q2 (April-June) return: due 28 July

- January monthly return: due 28 February

Submissions are made electronically via the FTA EmaraTax portal.

What Goes in a VAT Return (Form 201)

The UAE VAT return requires detailed reporting across multiple boxes:

Output side:

- Standard-rated supplies broken down by all seven emirates (Abu Dhabi, Dubai, Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, Fujairah)

- Zero-rated supplies (exports, healthcare, education)

- Exempt supplies (financial services, residential property)

- Reverse charge supplies

Input side:

- Input VAT on standard-rated expenses (recoverable)

- Reverse charge input VAT

- Import VAT (auto-populated from Customs data linked to your TRN)

- Adjustments and corrections

Net calculation: Output VAT minus Input VAT equals Net VAT Payable (or refundable).

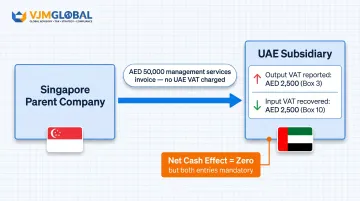

Reverse Charge Mechanism

The reverse charge shifts VAT reporting obligation from the supplier to the recipient. This applies when Singapore businesses import goods or services from outside the GCC into UAE operations.

How it works: Your UAE entity "self-accounts" for VAT by reporting the transaction as both output tax (Box 3) and input tax (Box 10) in the same return. The net cash effect is zero, but correct reporting is mandatory.

Example: A Singapore parent company invoices its UAE subsidiary AED 50,000 for management services. The Singapore parent doesn't charge UAE VAT. The UAE subsidiary reports AED 2,500 output VAT and AED 2,500 recoverable input VAT in its return, with no net payment due—but both entries must appear.

Tax Invoice Requirements

Once VAT-registered, you must issue compliant tax invoices containing:

- Supplier name, address, and 15-digit TRN

- Customer name and address (TRN required for B2B over AED 10,000)

- Unique sequential invoice number

- Invoice date

- Description of goods/services and quantity

- Net amount (before VAT)

- VAT rate applied (5%, 0%, or Exempt)

- VAT amount charged

- Total amount payable (including VAT)

Simplified invoices (for transactions under AED 10,000) may omit full customer details but must still include your TRN, total amount, and VAT breakdown.

Issuing invoices without a valid TRN is a compliance violation subject to AED 2,500 penalty per instance.

Record-Keeping Obligations

VAT-registered businesses must retain financial records, tax invoices, credit notes, import/export documentation, and all supporting materials for 5 years from the end of the tax period (15 years for real estate transactions).

Records must be available for FTA audit and can be maintained electronically. Singapore businesses using cloud accounting platforms should verify their systems can produce FTA-compliant documentation, including Arabic translations when requested.

Failure to provide records in Arabic when required carries an AED 20,000 penalty.

Zero-Rated, Exempt, and Standard Supplies: What Applies to Singapore Businesses

Zero-Rated Supplies (0% VAT, Input VAT Recoverable)

Singapore businesses most commonly encounter these zero-rated categories:

- Exports — Goods and services to customers outside the UAE and GCC are zero-rated (software, consulting, physical goods). Retain export declarations, shipping records, and customer location proof.

- International transportation — Air and sea freight on international routes qualifies.

- Investment-grade precious metals — Gold, silver, and platinum at 99%+ purity.

- Newly constructed residential property — First supply within three years of construction completion.

- Healthcare and education — Publicly funded healthcare and approved institutional education services.

Zero-rated supplies still require VAT registration and reporting—the rate is simply 0%. Businesses can reclaim input VAT on expenses tied to zero-rated supplies, which protects cash flow.

Exempt Supplies (No VAT, Input VAT NOT Recoverable)

- Financial services — Interest income, insurance premiums, and certain fund management services are exempt. Singapore financial services firms should note: no VAT is charged to customers, but input VAT on related expenses (office rent, professional fees) is also unrecoverable — making it a real cost.

- Residential property resales — Sales of residential buildings after the first supply, and residential leases.

- Bare land — Undeveloped land without buildings or infrastructure.

Unlike zero-rated supplies, exempt status means input VAT becomes a sunk cost — there is no recovery mechanism. This distinction shapes how Singapore firms should structure UAE operations, particularly in financial services.

Digital Services: A Critical Obligation for Singapore Tech Companies

The exempt and zero-rated categories above apply mainly to goods and traditional services. Digital supply chains follow different rules entirely.

Singapore SaaS companies, app developers, streaming services, and digital advertisers must register for UAE VAT with no revenue threshold. If you supply electronic services to UAE customers, registration is mandatory — regardless of physical presence in the UAE.

Electronic services include:

- Cloud software subscriptions

- Mobile applications

- Streaming media (video, audio, games)

- Online advertising

- Digital downloads

- Web hosting and domain services

B2C digital services: Singapore provider must register for UAE VAT and charge 5% to UAE consumers.

B2B digital services: Reverse charge applies—UAE business customer self-accounts for VAT.

Many Singapore technology companies discover this obligation only after UAE customers are already on their books. Audit your customer base now: if UAE end-users are present, registration must happen before the first transaction, not after.

Penalties for UAE VAT Non-Compliance

The UAE enforces VAT compliance through a structured penalty regime under Cabinet Decision No. 49 of 2021, which became effective 28 June 2021.

Key Administrative Penalties

| Violation | Penalty |

|---|---|

| Late VAT registration | AED 10,000 (one-time) |

| Late VAT return filing (first offence) | AED 1,000 |

| Late VAT return filing (repeat within 24 months) | AED 2,000 |

| Late VAT payment (immediate) | 2% of unpaid tax |

| Late VAT payment (monthly thereafter) | 4% per month (capped at 300% of unpaid amount) |

| Failure to maintain proper records (first offence) | AED 10,000 |

| Failure to maintain proper records (repeat) | AED 20,000 |

| Failure to issue compliant tax invoice | AED 2,500 per instance |

| Failure to display VAT-inclusive prices | AED 5,000 |

The late payment structure is particularly severe: a 2% penalty applies immediately upon missing the deadline, followed by 4% monthly compound charges. An AED 100,000 tax payment delayed six months accumulates AED 26,000 in penalties (2% immediate + 4% × 6 months).

Tax Evasion: Criminal Exposure

Administrative penalties are serious — but deliberate evasion escalates the consequences entirely. Under Article 25 of Federal Decree-Law No. 28 of 2022, the FTA can pursue criminal action:

- Imprisonment and/or

- Fine not less than the evaded tax amount and not more than three times the evaded tax amount

Providing false information or destroying tax documents can result in imprisonment and/or fines up to AED 1,000,000. The FTA treats repeat offences within five years as aggravating circumstances.

Singapore businesses that underreport supplies, fail to register when required, or deliberately misstate VAT obligations face criminal prosecution, not just administrative penalties.

Reducing Compliance Risk Proactively

Given these stakes, prevention is far cheaper than remediation. Key steps to stay ahead:

- Use cloud accounting software that tracks UAE VAT by emirate, maintains compliant invoice formats, and integrates with Customs data feeds

- Appoint UAE tax agents with proven experience supporting non-resident businesses as your fiscal representatives

- Prioritize the 28th-of-the-period deadline — late payment penalties compound rapidly and are difficult to reverse

- Work with cross-border tax specialists who can identify compliance gaps before they become penalties

VJM Global, with 30+ years of experience in cross-border tax compliance, helps Singapore businesses build reliable VAT systems aligned with FTA requirements from the outset.

Frequently Asked Questions

Do Singapore businesses need to register for UAE VAT?

Yes. Singapore businesses making any taxable supply in the UAE must register for UAE VAT immediately, regardless of turnover amount. The AED 375,000 threshold applies only to UAE-resident businesses. Non-residents face a zero-threshold registration obligation under Article 18 of the VAT Decree-Law.

What is the difference between UAE VAT and Singapore GST?

UAE VAT is 5% versus Singapore's 9% GST, and both use input tax credit mechanisms. The key difference is registration rules: UAE requires immediate registration with no threshold for foreign businesses, while Singapore applies specific thresholds and reverse charge provisions. UAE also mandates fiscal representatives for non-resident registrants — Singapore does not.

Does a Singapore company exporting goods to the UAE need to pay UAE VAT?

Exports from Singapore to the UAE are zero-rated for Singapore GST purposes. However, UAE import VAT (5%) applies when goods arrive in the UAE and is typically paid by the UAE importer through Customs. Singapore exporters don't charge UAE VAT unless they're registered in the UAE for other taxable activities.

What is a fiscal representative and does a Singapore business in the UAE need one?

A fiscal representative is a UAE-based agent jointly responsible for VAT compliance — filing returns and paying tax due on your behalf. All non-resident businesses registering for UAE VAT, including Singapore companies, must appoint one under Article 18 of the VAT Decree-Law and Executive Regulations.

How often do Singapore businesses need to file UAE VAT returns?

Most businesses file quarterly, with returns and payments due by the 28th of the month following the quarter end. Businesses with annual taxable turnover exceeding AED 150 million must file monthly. All filings are submitted electronically through the FTA EmaraTax portal.

What records must Singapore businesses keep for UAE VAT compliance?

Businesses must retain tax invoices, credit notes, financial records, import/export documentation, and all supporting materials for 5 years from the end of the tax period (15 years for real estate). Records must be available for FTA audit and can be maintained electronically, but must be producible in Arabic if requested.

Have questions about UAE VAT obligations for your Singapore business? VJM Global's cross-border tax advisors bring 30+ years of international tax experience to complex multi-jurisdiction compliance questions. Reach us at info@vjmglobal.com or +91 9891576441.