Introduction

UK professional services firms face a common frustration: delivering months of billable work only to discover their financials don't reflect the effort. A consultancy may have worked 300 chargeable hours in February, yet the profit and loss account shows little revenue because invoicing runs two months in arrears.

A law firm completes 60% of a major litigation matter but can't bill until the case concludes — leaving reported profit well behind actual delivery.

This mismatch is where WIP accounting becomes essential. Without proper Work in Progress recognition, your balance sheet misrepresents asset value, your P&L distorts profitability, and HMRC may question your tax computations. Partners and stakeholders are left making decisions on incomplete numbers.

This article explains what WIP is in the context of UK professional services, the exact steps to account for it correctly under FRS 102 and HMRC guidance, and the most common errors that distort financial statements. Whether you're a consulting firm, law practice, accountancy business, or creative agency, accurate WIP accounting is what keeps your revenue recognition aligned with actual delivery.

Key Takeaways

- WIP represents the value of work completed but not yet billed or recognised as revenue

- FRS 102 Section 23 requires UK firms to use the percentage-of-completion method to value WIP

- Until billed or completed, WIP sits on the balance sheet as a current asset

- Untracked WIP distorts profit margins and can trigger HMRC compliance problems

- Monthly WIP reviews paired with integrated time-tracking keep reporting accurate and audit-ready

What is WIP in UK Professional Services and When Does It Apply?

Defining WIP in the Professional Services Context

Work in Progress in professional services represents the monetary value of services delivered to clients that have not yet been invoiced or formally recognised as revenue. This differs fundamentally from accounts receivable (which covers invoiced but unpaid work) and deferred income (amounts billed before work is performed).

Consider a UK consultancy engaged on a £60,000 strategy project. By 28 February, the firm has delivered workshops, research, and interim deliverables worth £24,000 at cost, but the contract terms permit billing only at project milestones. That £24,000 of unbilled, completed work is WIP: value the firm has created but not yet converted to an invoice.

HMRC's Business Income Manual BIM33020 confirms that for professional services—lawyers, accountants, architects, and similar practices—WIP consists of "uncompleted services not represented by any significant physical asset capable of sale."

Which UK Professional Services Sectors Are Most Affected?

WIP accounting is unavoidable for firms operating on long-running or multi-phase engagements:

- Law firms: Matter-based billing often lags case completion by months; The Law Society Financial Benchmarking Survey 2026 reports median lock-up (WIP plus debtors) of 134 days

- Consulting firms: Fixed-fee projects and retainer arrangements create significant unbilled value

- Accountancy practices: Audit, tax advisory, and compliance work frequently spans multiple months before billing

- Architects and surveyors: Stage-based fee agreements defer invoicing until design milestones or project phases complete

- Marketing and creative agencies: Campaign delivery and creative development often precede billing by weeks or months

The Law Society's 2026 survey found that despite improvements, UK law firms still tie up approximately 4.5 months of working capital in WIP and receivables—a figure that underscores the scale of the issue.

Balance Sheet Classification Under UK Law

Under the Large and Medium-sized Companies and Groups (Accounts and Reports) Regulations 2008 (SI 2008/410), WIP is classified as:

C. Current assets > I. Stocks > item 2: Work in progress

This statutory classification confirms WIP sits on the balance sheet as a current asset. How it is valued and presented, however, depends on which accounting standard applies:

| Treatment | Standard | Basis |

|---|---|---|

| Valued at stage of completion | FRS 102 (current) | Recognition tied to work performed, not cash received or invoice raised |

| Presented as "Contract Asset" | FRS 102 (amended, effective 1 January 2026) | Used when the right to consideration is conditional on factors beyond the passage of time |

The 2026 amendment brings UK practice closer to IFRS 15, so firms should review whether their existing WIP disclosures will need updating before the effective date.

How to Account for WIP in UK Professional Services

Step 1: Identify and Capture All Project Costs

Accurate WIP accounting begins with comprehensive cost capture for every active engagement. Direct cost components include:

- Direct labour: Staff time at cost or billable rate, tracked via time-recording systems

- Subcontractor and third-party costs: External consultants, expert witnesses, freelance specialists

- Directly attributable overheads: Project-specific software licenses, travel, research subscriptions

General overhead allocation should follow a consistent, documented method—whether allocated by headcount, revenue share, or direct labour hours.

Everything hinges on robust time-tracking. If billable and project-related hours aren't logged daily against the correct engagement, WIP figures will be inaccurate from the outset. Research from Consultancy.uk found that 44% of UK professional services firms missed revenue targets, with 30% citing inaccurate forecasting—a direct consequence of poor cost visibility.

Step 2: Determine the Stage of Completion

FRS 102 Section 23 recognises two methods for measuring stage of completion:

Input methods (most common in UK professional services):

- Cost-to-cost method: Costs incurred to date ÷ estimated total costs = percentage complete

- Labour hours method: Hours expended to date ÷ estimated total hours

Output methods:

- Milestones or deliverables completed

- Surveys of work performed

- Appraisals of results achieved

Worked Example:

A UK consultancy secures a £60,000 fixed-fee contract. Estimated total cost: £40,000. By 31 March, the firm has incurred £16,000 in costs.

- Percentage complete: £16,000 ÷ £40,000 = 40%

- Revenue to recognise: £60,000 × 40% = £24,000

- WIP asset value: £16,000 (costs incurred)

- Profit recognised to date: £24,000 – £16,000 = £8,000

This approach aligns revenue recognition with delivery progress, not billing timing.

Step 3: Recognise Revenue and Record the WIP Journal Entries

Two primary journal entries drive WIP accounting:

1. As work is performed (building the WIP asset):

| Account | Debit (£) | Credit (£) |

|---|---|---|

| WIP (Balance Sheet – Current Asset) | 16,000 | |

| Staff Costs / Overheads (P&L) | 16,000 |

2. When revenue is recognised based on stage of completion:

| Account | Debit (£) | Credit (£) |

|---|---|---|

| Accrued Income / Contract Asset (Balance Sheet) | 24,000 | |

| Revenue (P&L) | 24,000 |

| Account | Debit (£) | Credit (£) |

|---|---|---|

| Cost of Sales (P&L) | 16,000 | |

| WIP (Balance Sheet) | 16,000 |

The distinction between underbilling and overbilling determines whether a balance sheet entry becomes an asset or a liability:

Underbilling vs. Overbilling:

- Underbilling (asset position): Revenue recognised exceeds amounts invoiced → creates accrued/unbilled income (asset)

- Overbilling (liability position): Amounts invoiced exceed recognised revenue → creates deferred income or contract liability

| Scenario | Revenue Recognised | Invoiced | Balance Sheet Entry |

|---|---|---|---|

| Underbilled | £24,000 | £15,000 | £9,000 accrued income (asset) |

| Overbilled | £24,000 | £30,000 | £6,000 deferred income (liability) |

Step 4: Close WIP at Billing or Project Completion

When an invoice is raised or the project completes:

Closing entry:

| Account | Debit (£) | Credit (£) |

|---|---|---|

| Trade Debtors (Balance Sheet) | 60,000 | |

| Accrued Income (Balance Sheet) | 24,000 | |

| Revenue (P&L) | 36,000 |

Revenue previously recognised via accrued income (£24,000) is matched against the invoice; the remaining £36,000 is recognised as new revenue.

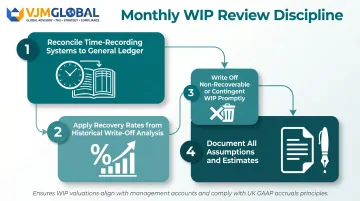

Monthly WIP Review Discipline:

Firms should conduct monthly WIP reviews aligned with management accounts cycles to:

- Update cost and completion estimates

- Write off unrecoverable WIP promptly

- Ensure balance sheet values reflect realistic, realisable amounts

For firms managing multiple concurrent engagements, the most common failure point is inconsistent review cadence—WIP that isn't reviewed monthly tends to accumulate errors that compound at year-end, distorting both reported profit and cashflow forecasts. VJM Global works with 250+ UK businesses on exactly this challenge, supporting WIP reconciliation as part of ongoing accounting and financial reporting services.

UK Accounting Standards and HMRC Rules Governing WIP

FRS 102 Section 23: The Primary UK Standard

For periods beginning before 1 January 2026, FRS 102 Section 23 requires revenue from service contracts to be recognised by reference to the stage of completion at the reporting date. The outcome can be estimated reliably when:

- The amount of revenue can be measured reliably

- Economic benefits will probably flow to the entity

- Stage of completion can be measured reliably

- Costs incurred and costs to complete can be measured reliably

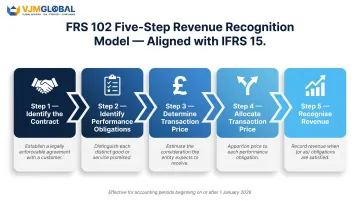

From 1 January 2026, the amended FRS 102 introduces a five-step revenue recognition model aligned with IFRS 15:

- Identify the contract(s) with a customer

- Identify the performance obligations

- Determine the transaction price

- Allocate the transaction price to performance obligations

- Recognise revenue when (or as) performance obligations are satisfied

Revenue is recognised "over time" (replacing "stage of completion" terminology) using input or output methods. Notably, Section 13 Inventories will no longer be disapplied from WIP, which introduces additional measurement and impairment considerations firms must plan for.

HMRC's Position: BIM33165

HMRC BIM33165 explicitly states:

"Valuing professional work-in-progress follows GAAP. The proper valuation depends on the correct application of generally accepted accounting principles to the facts."

The manual confirms that revenue for service contracts is accounted for under the percentage of completion method. HMRC also acknowledges that firms in similar sectors may legitimately adopt different WIP valuation bases where their circumstances differ — for example, a surveying-focused firm versus a property sales practice.

Tax Computation Follows Accounting Treatment

Taxable trading profits must be calculated in accordance with GAAP:

- Unincorporated businesses (partnerships, LLPs): ITTOIA 2005 s25

- Companies: CTA 2009 s46

In practice, the WIP figure in your FRS 102-compliant accounts feeds directly into the Corporation Tax or income tax computation. Where WIP is correctly valued under FRS 102, no separate tax adjustment is required. Your accounting WIP policy therefore has a direct bearing on tax liability.

IFRS 15 (For Larger Firms)

Larger UK firms or those applying full IFRS use IFRS 15 Revenue from Contracts with Customers, which applies the same five-step model now adopted by amended FRS 102. The main practical difference is the extent of disclosure and contract disaggregation required — full IFRS demands considerably more granular reporting than FRS 102.

Key Variables That Affect Your WIP Valuation

Contract and Billing Structure

Different contract types require different WIP approaches:

Fixed-fee engagements:

- Require careful estimates of total costs

- Demand consistent tracking against percentage of completion

- Create higher estimation risk if scope changes

Time-and-material contracts:

- WIP grows incrementally as hours and expenses are logged

- Revenue recognition is more straightforward

- Lower estimation complexity

Retainer arrangements:

- Blur the line between deferred income and WIP

- Require clear definition of services per period

- May trigger "over time" revenue recognition under amended FRS 102

Estimating Total Contract Costs Accurately

The percentage-of-completion calculation is only as reliable as the underlying cost estimate. If estimated total costs are set too low at the outset, revenue will be over-recognised early and write-downs will be needed later. To avoid this, best practice requires:

- Documented cost estimates at project inception

- Regular estimate updates throughout the engagement

- Formal change control when scope expands

- Historical analysis of estimation accuracy by project type

The Consultancy.uk survey found that 14% of firms identified project over-runs or write-offs as significant issues—a direct consequence of poor cost estimation.

Recoverability and Write-Down Decisions

WIP should only be carried as an asset to the extent it is reasonably expected to be recovered through billing or contract settlement. If there is doubt about recoverability, the affected WIP must be written down.

Common triggers for write-down:

- Client disputes over scope or quality

- Scope changes without formal approval

- Financial distress at the client

- Time recorded significantly exceeds budget without client agreement

Write-down decisions require documented reasoning — your auditors or HMRC will expect evidence that recoverability was assessed against specific facts, not general optimism.

Common Mistakes UK Professional Services Firms Make with WIP

Conflating WIP with Unbilled Revenue

Many firms treat all accrued income as WIP or merge the two on the balance sheet — a distinction that matters more than it might appear. WIP is the cost-side accumulation of effort on an incomplete contract; unbilled (accrued) revenue represents the income side once recognised under FRS 102. Mixing these distorts financial statements and can misrepresent the firm's position to lenders, investors, or HMRC.

Correct Presentation:

- WIP: Current asset – Stock (or Contract Asset under amended FRS 102)

- Unbilled revenue: Current asset – Accrued income / Contract Asset

- These must be separately disclosed

Applying Inconsistent Revenue Recognition Methods

Applying percentage-of-completion to some contracts and completed-contract to others — without documented justification — is a common and costly misstep. It breaches the consistency principle under UK GAAP, makes profitability comparison across projects or periods impossible, and can invite HMRC scrutiny during tax investigations.

If your firm switches methods between years, that decision must be documented, disclosed in the notes, and justified against the accounting policy framework.

Armstrong Watson identifies inconsistent WIP valuation policies year-on-year as one of the seven most common accounting issues for UK law firms.

Carrying Stale or Inflated WIP Without Regular Review

Letting WIP accumulate on the balance sheet without checking whether it remains recoverable is one of the fastest ways to overstate assets. WIP relating to disputed work, unapproved scope creep, or projects that have quietly ended without formal sign-off can inflate your balance sheet — sometimes significantly.

Monthly WIP reviews are a regulatory and commercial necessity, not optional housekeeping. Firms should:

- Reconcile time-recording systems to general ledger monthly

- Apply recovery rates based on historical write-off analysis

- Promptly write off non-recoverable or contingent WIP

- Document all assumptions and estimates

Frequently Asked Questions

What is the accounting treatment of WIP?

WIP is recorded as a current asset by debiting the WIP account and crediting the relevant cost accounts. The balance is cleared when the engagement is billed or completed.

What is WIP in accounting for a service industry?

In service industries, WIP represents the value of work delivered to a client that has not yet been invoiced. It sits on the balance sheet as an asset and is converted to revenue as the service contract progresses toward completion.

How is WIP valued under FRS 102 in the UK?

Under FRS 102 Section 23, UK firms value WIP using the percentage-of-completion method—measuring progress either by costs incurred relative to total estimated costs (input method) or by outputs such as milestones reached.

What is the difference between WIP and unbilled revenue in professional services?

WIP is the accumulated costs on a partially complete engagement. Unbilled (accrued) revenue is income recognised but not yet invoiced. Both appear on the balance sheet but must be recorded as separate line items.

How does HMRC treat WIP for tax purposes?

Per HMRC's Business Income Manual BIM33165, professional WIP is valued in accordance with GAAP. The accounting treatment under FRS 102 generally determines the taxable amount, though firms must ensure their valuation basis is consistent and documented.

How often should a UK professional services firm review its WIP?

Monthly reviews aligned with the management accounts cycle are recommended. High-value or fast-moving engagements may warrant more frequent checks to keep estimates current and unrecoverable balances written off promptly.

Conclusion

Accurate WIP accounting in UK professional services is not merely a compliance exercise—it is the mechanism that aligns revenue recognition with actual delivery, gives firms a true picture of profitability, and keeps financial statements credible with HMRC and stakeholders.

The key success factors are consistent application of FRS 102's percentage-of-completion method, disciplined time-tracking, and monthly WIP reviews. Most errors stem from inconsistent methods, inflated estimates, or failing to write down irrecoverable balances promptly.

Getting WIP accounting right requires both technical knowledge and consistent execution — two areas where firms often need outside perspective. VJM Global works with 250+ UK businesses on accounting, compliance, and financial reporting, helping them build WIP policies that hold up under FRS 102 scrutiny and HMRC review.