管理长期项目往来会带着装完成工作并收货到付款之间的时间不匹配。这种差异可能使准确报告收集到增加、证明利润合理性与有效规划出现了金流变量困难的难度重重。对于预期限定的 Supercosia 几个月至几年的美好时光,需要一种更可靠的方法来使财务状况不佳和工作进度保持一致。成完成了这个问题提供了一次切实可行的例子。

大多数普通通和专业商业都承认,商家使用POCM来报告月份份额的目标数量增加量。这种会计方法可以让你在项目进展时确认收益,而不仅仅是在项目完成时确认收益。它可以更准确地了解你的收入,尤其是在建立、工程或定制制造行业,在某些行业,交付需要时间,每个段都很重要。

在这篇博客中,您将了解其工作原理,何时使用它,以及其如何使您更好地控制财务报告。

使用 propetrongbiach 计量方法来确认长远的期望值(通常是超出一个会期望的期望值)期望值和期望值。这样可以阻止你在项目结束之后的累积积分收集集,并让你提供真实的财务概况状况。

这种方法使美国的企业能量年份的总股东进一步确认了收入和支出,从而,在同一个期望限内提供更准确的财务状况。它对从事故长远的目的地,美国公司特别有用,在某种程度上,收集录音和成本是根据工作完成的进展进行跟踪的。

你应该使用已完成的 mubbiAccounts 方法方法,因为它可以更准确地了解目的地的财务状况。它还将获得确认认知和工作进度的相似匹配,并因此跨越多个时代的项目提供了更好的 “财务可见性”。

在长期合成或项目跨越多次会期内(例如建筑或大规格模制造)的条款如下,受限于最有效。当项目有明确定可衡量的进度并且有可靠的估计已完成情况的依据是,你应该选择这种方法。

成完美毕毕毕比核算法是一种广义的使用方法的方法方法,用于确认长期项目生命周末期内收款和支出。尽管这种方法可以对美国的企业的总裁说非常有好处,但有一些需要记住记忆的就是战争。美国公司需要准确估算完成量比和项目成本,以避免免除除高估计值或降低低估值估计收入。

遵循循环循环此流程,您可以继续努力确认收益,从中获得更稳定的利润,并及时了解每份同事的财务状况。

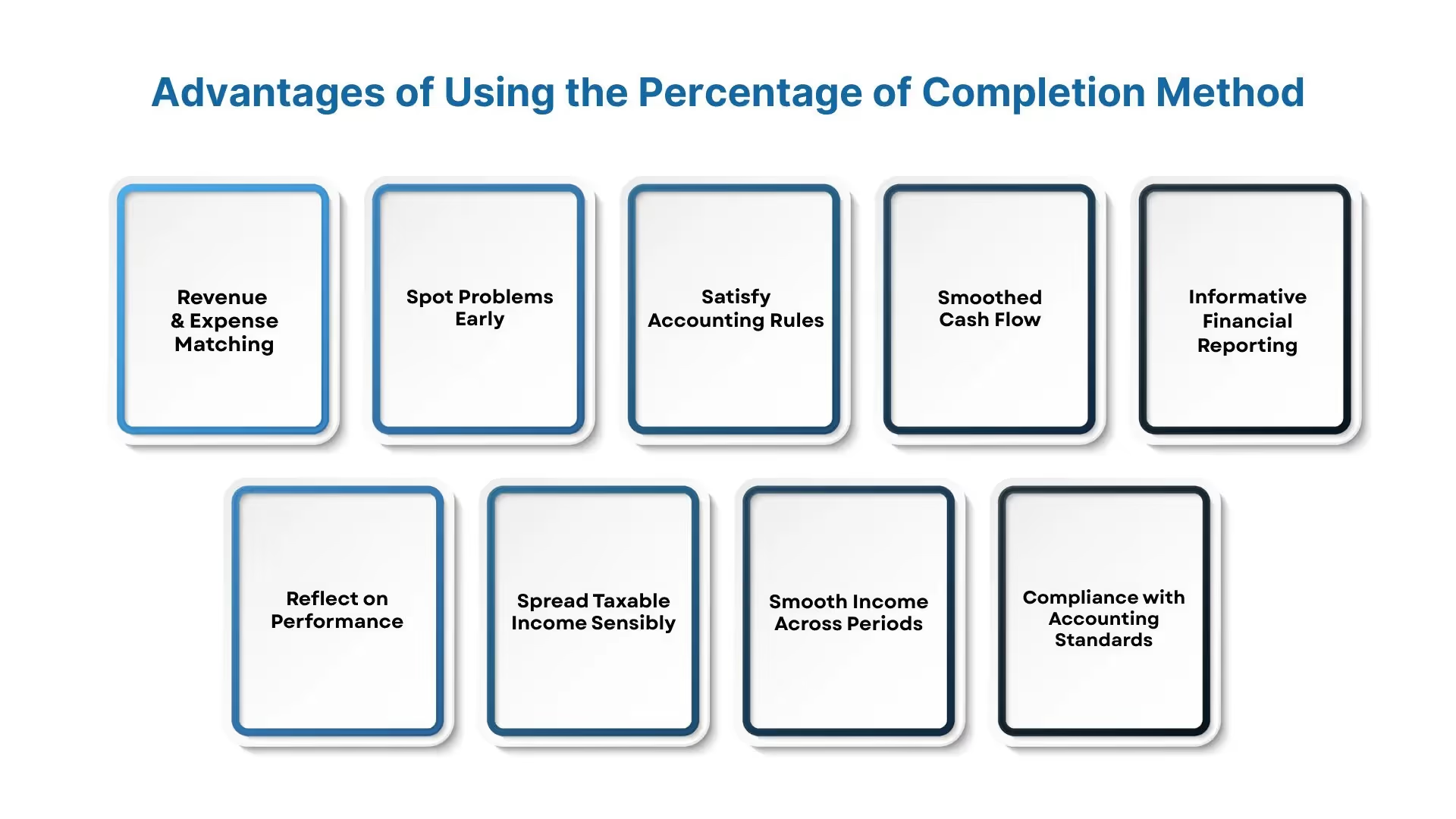

那么,用这个方法你能得到什么?让我们分解一下除了 “选中” 规格性方框以外面的实际好处。

成已经 makbi会计方法提供了多次会期间收款的真实视图。在计会中完成使用pubbifa的好处如下所示:

另请阅读: 转让定价:成本加法

应用这种方法,您可以通过收取和成本累计对其进行报告,而从那时起,您可以提供更可预测的财务状况,提高透明度,并增强强化利益相关者的信誉。

在了解了好处之后,让我们来看看这个方法是如何跟踪和报告项目进度的机制。

这种行为已经完成了在项目跨越多个财政政权期限的行业中运营的美国公司特别有利。美国企业可以用这种方法来反馈影合的持续进展,而确认保财务报告更准确地与实际完成的工作相机匹配。展后,您可以按自己的意愿来确认收益。以下是你的操作方法法:

将你的工作划分为可衡量的阶段,按月或按时间顺序记下录音进度。这些阶段段是收取确认的基础。

首先,制片定一份在建计划(WIP),以跟进同名价格(包括批的变量更名单)、总预计成本、迄今为止的实际成交以及提交给客户的账单。该时间表将确认您的收款计算,并显示任何超额或少量付款账户清单。

使用以下公式计算机进度:

完成成绩百分比 = 迄今为止的成绩 ÷ 预期总成本

这告诉你你已经完成了工作的哪一部分。

通过将完成pubbi乘以合伙总价值来确认收益:

确认收益 = 完成百分比 × 合成价格

因为,如果你在一份价值12万美金的合伙人上完成了50%,那么你的收入将达到6美元。

按以下公式计算机超额或少量计费计算:

已确认收款——进度账单

正面结果(向下开单)显示为资产;负数(超额计费用)显示为资产负债表上的负债。

将相机同伴的完成了 protengbiPayPiege 以总估计成本,以计算机本期费用为准。然而之后,你将从收款中减去以获得利润。

在每一个报告中,期末结束时更新成本、账户户单和进度,重复第 2 步到第 5 步以保持最新财务状况。

这种方法使你的收集集合报告与实际完成的工作保持同步。在工作中继续保持准确性的同时,您可以更新新估计计算机的值。

计算机进度的方程不止一种。让我们研究一下确定的项目进度的不同方法法。

受试者非常适合的管理者需要一年以上的才华能完成的美国企业(例如大型建筑项目或多阶段段软件开发等)。对于这些目的地,美国注册会计师事务也是如此,这种方法可以确立在工作中继续展出中原创的终结如一地确定的收购和成本,从而,降低低成本财务异常的程度。您可以根据您的项目 A 类和可靠度测量量来选择计算机方法法:

完成以支出本与预期总成本的比对比比比较为基对比。这是最广泛使用的方法,尤其是在施工中,因为成了本反馈的进度。

完成成绩百分比 = 产出成绩 ÷ 预期总成本

示例实例: 如果你在估计的8万美金的预付金额中等于4美元,那么你已经完成了50%。

另请阅读: 在印度注册公司的费用

按摩工作量(例如劳动力或机器人时间)除非以估计计的总工作时间来衡量量量进度。如果工时与结果密切相关,这就是 TradeGongures 来了。

完成百分比 = 工作时数 ÷ 预计计数总工时

示例实例: 如果你的队伍记忆了预期的 2,400 个小时中有 1,200 个字符,那你的比如 50%。

将你交付的交付金额从合成同的总数中算出来的。当输出均值可数次使用此选项。

完成成交百分比 = 已交付的商品数量 ÷ 总商品数量

示例实例: 如果你完成了 10 个相机同义屋中那个 6 个,你完成了 60%。

在现代之下 会计 边框架(ASC 606/IFRS 15),这两种方法适用:

pubbi完成方法的不同方程式之间的比对比如下:

选择一种与你跟踪项目进展的方形相容的方法方法,并且,在你的合伙人中坚持使用这种方法方法。segwork 的进展,这将为你提供一致、清晰的收货报告。

VJM Global 根据可靠的项目数据,帮助辅助软件和服务型企业应用正确定已完成的pubbi方法法,即成本对成本、基于 nufuchnufline或基于产出的方法法。我们负有责任跨里程碑的收藏,确认认可和成就本的跟踪,帮助帮助客户准确报告合成进度。我们的会计支持帮助帮助管理印度和国外多人段的目的地 cuximpointaCrectionaldewardenceInfectionald crection

在了解您的选择之后,让我们使用计算机数字并计算您的收入。

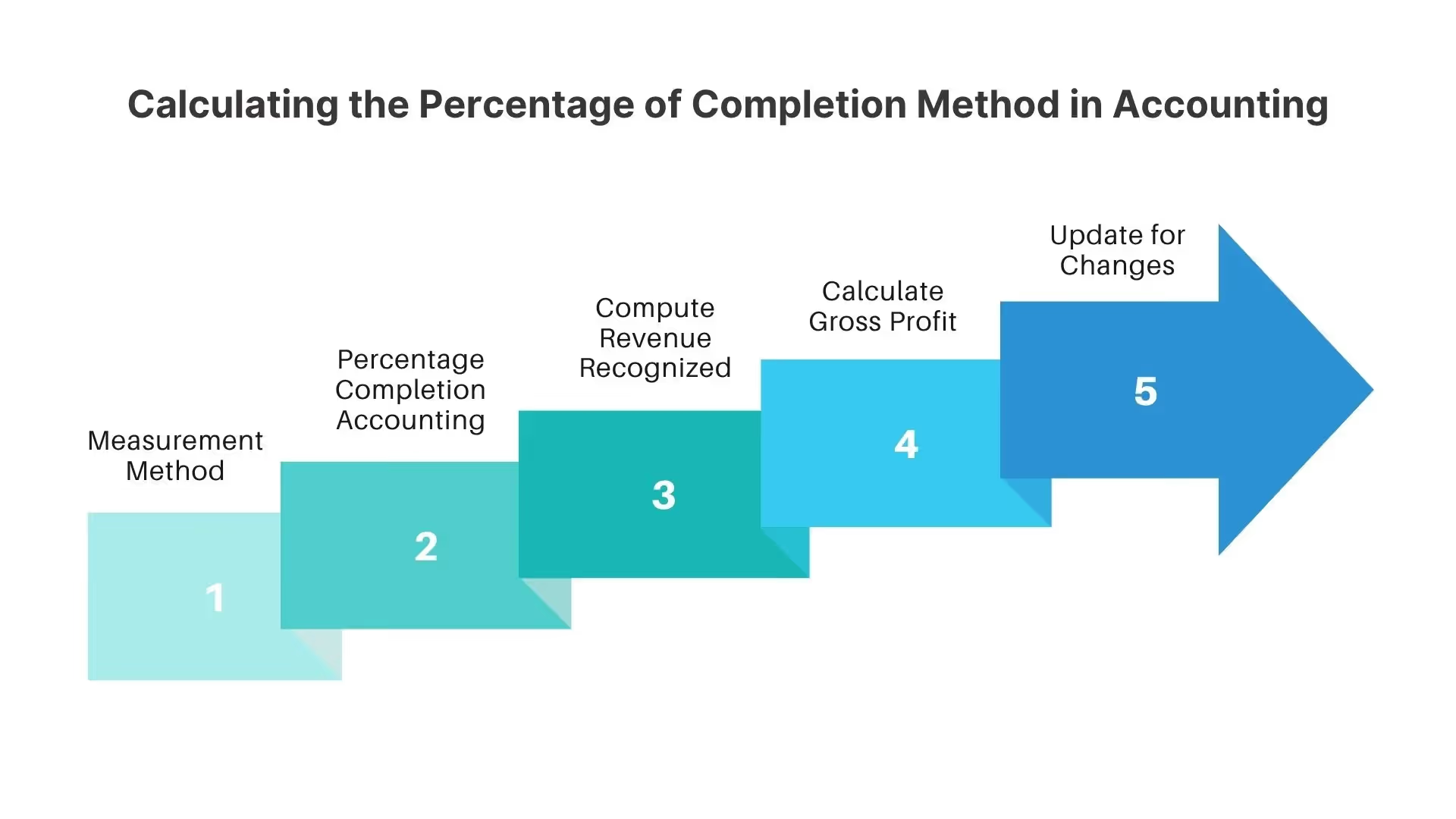

年进展的目的地,遵循循环,直截了当的结构化流程来自计算机收件确认。计算机完成了 mubbi 的关键步骤是:

选择最准确的地点跟踪进度的方法法:

选择您的进度衡量标的标准(成本对比、付款的金额或交付金额的单位)并计算:

完成百分比 =(产量或工作量 ÷ 估计总额)

然而之后,他的应用将用于收款和总支出。

或者:

= 工作时间 ÷ 预计总工时

或者:

= 已交付的商品数量 ÷ 预期的总商品数量

例如,如果你在8,000美元的估计费用计算中花费再加上4,000美元,那么你已经完成了50%。

将完成pubbi乘以合同总价值:

迄今为止的收益 = 完成百分比 × 合成价格

例如,如果你的合成等于12,000美元,而你已经完成了50%,那么你将记入6,000美元的收入。

你也可以使用计算机取款的利润:

取的毛利润 = 迄今为止的收益 — 迄今为止的收益 — 迄今为止发生的成本

例如,如果是6,000美元至4,000美元,则该期限的毛利润为2,000美元。

重新估算每个周末期望的总成绩和收益。当估计值发生变化时,调整整理计算机结果。

通过遵循这些步骤,您可以使收款和支出与实际工作保持一致。使用这种方法的公司会逐步报告收入,避免免除不定期的激增并提供清晰的财务状况。

下一步是将您的计算机结果应用于报表。以下是在账号上收款和支出的显示方式。

在计会完成中,您可以根据项目进度确认收款和支出,无需等到最终交付即可。

将完成的pigbi乘以合成总价格,以确认今日为止获得的收入。

示例实例:如果你在一份价值12,000美元的合约上花费了8,000美元的估计值为中等于4,000美元(50%),则将确认兑现6,000美元的收入。

使用以下公式:

迄今为止的收益 = 完成百分比 × 合成价格

迄今为止的费用 = 完成百分比 × 预计总成本

示例实例: 因为这个,如果合伙总额为10美元,而你已经完成了30%,那么你将确认兑现3万美元的收入和支出。

使用相机同的mubbi来确认总估计成本的等值部分:

迄今为止的费用 = 预计总成本 × 完成百分比

如果总估计成本为8,000美元,完成后为50%,则将记录为4,000美元的支出。

另请阅读: ITC 没有资格 SEGPUND 付款企业社会责任活动产妇的费用。

从累计总额中减去前期确认的金额,以确认您在此期间的收入和支出支出预算。

将取消的收款与您的账户单进行比对比:

示例实例:如果你在一份价值10万美元的合约上完成了50%,但账户单价为60%,那么你已经开了10美元(10%×10美元)。

您可以通过记住工作进展中的收入和成本,将财务报告与实际效果相匹配。这种清晰度避免了项目结束时的突然波动,并使资产负债表数据保持最新状况。

在深度研究之前,值得知道我会在哪儿出来不错。以下是需要注意的事件,以及如何避免免除常见问题。

使用 prometplengbiCural 方法法,将使其漏洞、保激和保激施加在内部。通过采取这些步骤,您可以保持收据的准确性,防止其使用,并在使用过程中完成了 pubbiAccountePractionfacture pefraghtePorsePearenseRespearenseReconeflow。

根据成本和进度估算我获得的收入。如果你低估了总成本或者夸大了进度,那么你就有机会报利润。你现在的面前肯定会有过多收款的机会了,以后需要转账收款。

由于您的收款是根据估计值来记录的,因为此不准确的成本跟踪或乐观的假设能会导致。错报成本的公司可能有机会获得收益;臭名昭著的是,东芝在监控管道机构构架中介绍其前任就夸大了利润。

将单一账户金额度与确认收款进行比较:

你可能会在前面确认收取收入。这种情况可能会给流动性带带来压力,尤金是在客户延期付款或计费周末延期长的情况下。

你必须坚持使用一种方法:成本对比、花费的工时或交割付款的单位,并每个周末更新新估计算法值。修改变量方法或不修改修改估计值会带来不一致和审计风险。

调整范围或成本时,必须重新调整计算机的进度。频率繁或延期的变量更单会使报告复杂化,可能需要补时调整;这会影响利润和资产/负债余额。

由于这种方法法取决于管理层次的估计,因为此时你的意志或意思是外界操纵的行为,跨时转向移植或进入成本以稳定收益。知名企业用了这一点,受到了监控管道部件的审查。

根据公认会原则(ASC 606)和《国际财务报告准则第15号》,只有在以下情况才可以适用此条款:

详细的 WIP 跟踪、需要实时成就本记事录音和定时估计计算机审计调试。如果没有强大控制和集成系统,就难以保证准确性和审计准备就绪性。

通过关注这些领域,您可以降低低成本财务和监控管道风险并保护利益相关者的信任。

但不管怎么说,已经开始了,下一节将介绍这个方法在业务环境中占有一席之地。

通过更新的财务报表并与其实际目标进行相似匹配,美国企业将从该方程式中受益,这对于需要实时查看财务业务的投资者或利益相关者尤其有用。这些示例例子演示了POCM如何实时跟踪收入和成本。

Gendascalfacl 进展将此方法应用于法案中。例如,作为一个8万美元的项目承认,你作为一个8万美元的项目承认,我们估计成交量的一半,那你将在该期的记忆录入中占50%(40美元)。请在 WIP REPORT 中跟踪进度并相应地调整整理账户户口单位和收益。

其用途是为期一年的软件构想的定义自多阶段的合一。与其等级待交付,不如记录进度(例如模块完成情况或花费的时间),并根据该进度每月确认收益。

另请阅读: 如何在印度创办软件公司

其用途是跨越多个时代的大型制造或造船的类产品。当达到里程碑或段落时,你报告相应的收获和成本。

税收和申报如下;

这些应用程序是如何让人们满意的监控管道的同时,在建立、技术和重型机械等行业的实际工作中,使用了这个方法提供切实可行的见解。

你可能想知道为什么要使用这个方法来替换已完成的合约方法。以下部分将帮助你在 POC 和 CCM 之间做选择。

当你想在整个项目中分配收集录入和成本时,而等到项目完成时,你应该选择完成prosepeceProsepecepecepecepeceturenprosepecepecuturenprocepecetrenproceproceProncePronceProncePronceProncePronceProncePronceProncePr以下是许多人喜欢它的原因:

使用 POCM,收取和支出将随着您的进步而逐步确认,从而提供更稳定的财务成绩。相比之下,已完成的合成同法(CCM)将保留所有内容直到项目结束,从 “导入” 急剧收集集。

您可以向利益的相关者、投资者、贷款人和审计师展示您在项目中的表格。CCM 使你在项目中途很难评测你的财务状况。

在 POCM 下,您可以按年龄收益 PanaTax。CCM可能,将所有纳税意思推广到一年,如果税率上升,这可能对你创造出更大的打击。

另请阅读: 购买软件时没有 TDS。

Gaap和IRS的定价是你使用POCM来订阅的标签长远不一样,除非不是你的模版小,否则就有资格获得CCM的例外情况。这使得 DEPOCM 在大多数数千种情况中成了你的默认选择。

CCM 通过等等待实际成分和收集来避免估计算法计算,但是 POCM 提供了更准确、更相关的财务状况。需要在简单性(CCM)和力度(POCM)之间进行权衡。

如果你的估计是合理的,那么进展是可以量化的,那么 POCM 可以提供 bicccm更清晰、更及时光的见解。当估计值不可靠或者你的法律规格模比较时,CCM 然是一种选择。否则规则,POCM 会使您的报告更具信息性和一致性。

你不必独自管理这个问题。您正在或管理流程设置面板,需要帮助,我们的 VJM 全球团队可以通过以下方式进行介绍。

你管理的长远不一样,尤其是在持续数月的软件开发或服务中,那么我已经完成了 mubbiubcount 计数方法可以确认你的收货情况。报告 VJM Global 不管在何处运营,HelpsafidAsduzSware企业无论在何处运营,都能够准确、合规地应用这种会计方法法法。

借在美国公认会计原则和印度会计准则的深厚专业知识,VJM Global通过以下方位方式为您的业务提供支持:

从初始设置到月度报告,VJM Global使管理长期收益,变量更容易,无需检测检测。 预约 看看他们的团队如何简化POC会计,并让您的业务审计做好准备。