%20(5).avif)

获得公司注册证书是贵公司在印度的重要里程碑。但是,这一成就标志着一个新阶段的开始。许多企业低估了随之而来的复杂合规要求。

贵公司的结构化注册后程序可确保充分的法律和运营功能。这些强制性步骤将您的注册实体转变为活跃的企业。它们确立了您在印度合法交易、雇用员工和管理财务的能力。

本指南详细介绍了印度公司的基本注册后程序。您将了解强制登记、纳税要求和法定义务。我们为贵公司在印度的业务启动提供了明确的路线图。

成立后的合规性包括公司在注册后必须立即完成的法律和监管手续。这些步骤使您的业务全面运营并获得印度法律的认可。

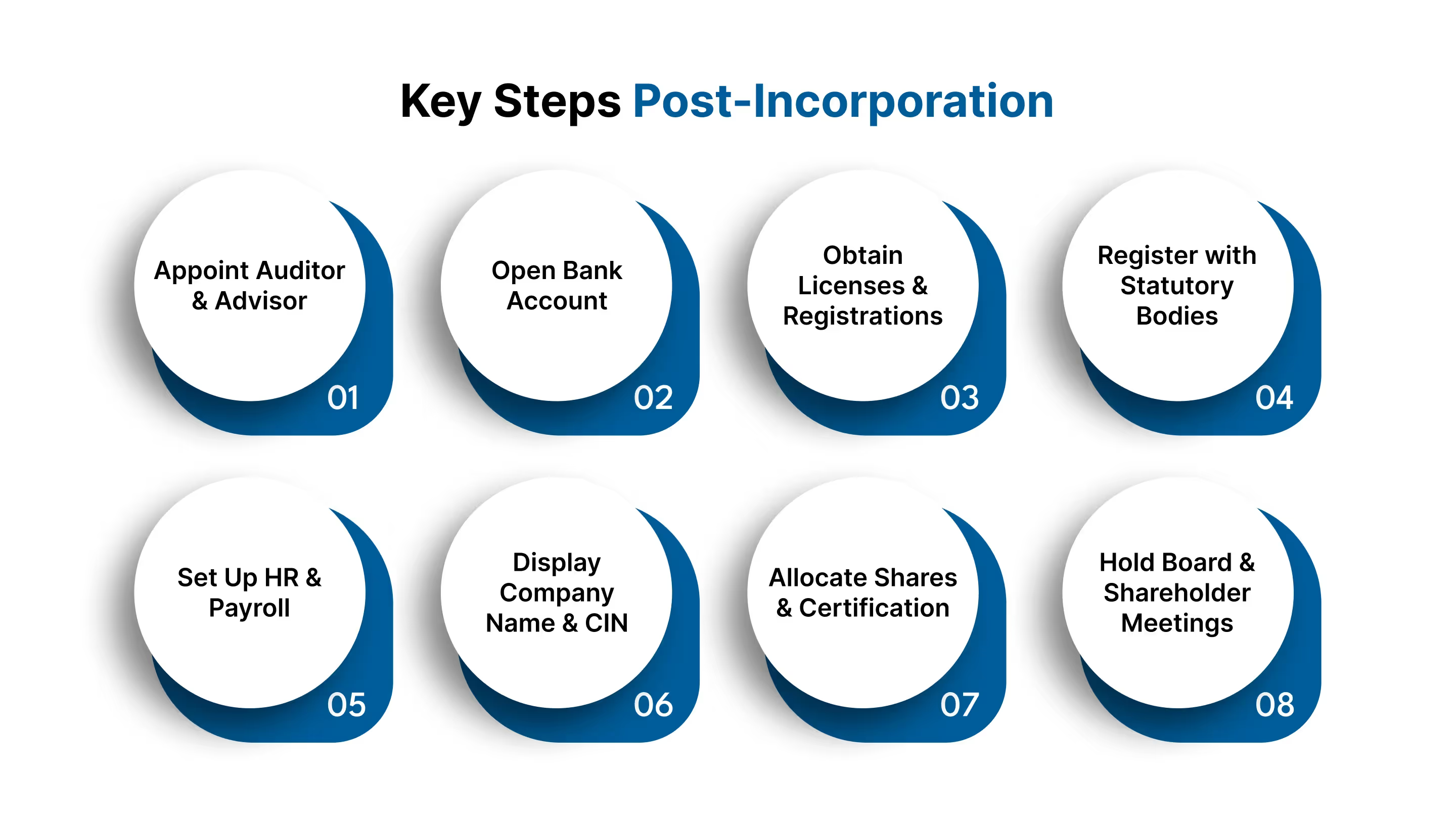

收到公司注册证书后,贵公司必须任命一名审计师,开立银行账户,向订户发行股票,并完成税务和法定登记。每一步都确认您的企业已做好合法运营、交易和招聘的准备。

简而言之,公司成立后的合规将您的公司从注册实体转变为活跃、运转良好的企业。

另请阅读: 离岸会计对企业成功的好处

这个法律基础为下一个关键阶段提供了支持。您的当务之急必须转移到激活公司的运营状态上。

了解公司注册如何影响您的下一步行动。 预约演示 与我们的专家合作,让您的游戏保持领先地位。

成功启动您的印度实体需要完成几个强制性的注册后步骤。这些程序激活了贵公司在印度市场的法律和运营能力。

他们确保从您开业的第一天起就完全遵守法律法规。适当的执行可以防止法律处罚和运营中断。以下是你需要做的:

您必须在公司成立后的三十天内任命一名合格的审计师。该专业人员将审查您的财务报表并确保遵守法规。税务顾问管理您的直接和间接税务申报和义务。根据2013年《公司法》,这些任命是强制性的。

它为何重要:

您必须为您的印度公司开设一个专门的银行账户。该账户将处理所有商业交易和资金转移。向银行提交您的公司注册证书和董事会决议。这可以将您的企业财务与个人账户完全分开。

它为何重要:

您的公司必须根据其业务活动获得特定的许可证。其中可能包括商店注册或特定行业的许可证。您还需要注册商品和服务税 (商品及服务税)。专业税务登记是雇主的另一项常见要求。

它为何重要:

另请阅读: 美国企业如何从印度研发的税收优惠中受益

在雇员公积金组织(EPFO)注册您的企业。一旦您雇用了第一位员工,就必须进行注册。您还必须在雇员国家保险公司(ESIC)注册。这些社会保障登记保护您的员工的利益。

它为何重要:

为您的员工创建正式的雇佣合同和公司政策。建立结构化的工资发放处理系统。实施适当的出勤和休假管理程序。这些系统确保了有组织且合规的人力资源管理。

它为何重要:

您必须在所有营业地点显示您的公司名称和 CIN。这包括您的注册办公室和任何分支机构。该信息应在醒目位置可见。此要求适用于公司官方文件和网站。

它为何重要:

从第一天起就确保公司顺利合规。与VJM Global合作,为您的印度公司提供端到端的注册后支持。 立即预订演示。

您必须在六十天内正式向公司的订阅者发行股票。分配后准备并向每位股东分发实物股票证书。保留一份详细的成员登记册,记录所有股票交易。此过程在法律上确认了您公司的所有权。

它为何重要:

您必须在公司成立后的三十天内举行第一次董事会会议。在正式会议记录中记录所有决议和决定。在九个月内安排并举行第一次年度股东大会。这些会议从一开始就建立了适当的公司治理惯例。

它为何重要:

这些初始步骤使您的公司从第一天起就开始运营。保持这种地位需要持续的法定义务。

另请阅读: 如何从美国在印度开展制造业务

保持法定合规性是您的印度公司的持续要求。这些义务确保您的企业在当局面前保持良好的法律信誉。定期申报和审计表明了透明的公司治理做法。它们保护您的公司免受处罚和运营限制。

您每年必须对财务报表进行法定审计。合格的注册会计师必须进行这项独立审查。经审计的报表真实反映了贵公司的财务状况。这些文件提交给公司注册处。

主要业务影响:

您的公司必须根据营业额提交每月或每季度的商品及服务税申报表。您还需要提交年度企业所得税申报表。全年需要分四次预付税款。这些申报必须在特定的截止日期之前提交。

主要业务影响:

您必须使用 MGT-7 表格向公司注册处提交年度申报表。财务报表在指定的时间表内使用 AOC-4 表单提交。董事会的任何变更都必须更新董事识别号。这些文件保持了贵公司在官方记录中的活跃状态。

主要业务影响:

您必须每月从员工工资中扣除和存入TDS。所有雇主都必须进行专业税务登记和申报表。ESI 和 PF 供款需要按月付款和申报。这些义务贯穿贵公司的整个运营周期。

主要业务影响:

从国外管理这一持续周期带来了重大挑战。这就是专业支持成为战略优势的地方。

管理您的印度实体在美国的持续合规性非常复杂。您必须跟踪不同监管机构的众多申请截止日期。了解不断变化的印度公司法需要当地的专业知识。这些挑战可能会将您的注意力从核心业务运营上转移开。

VJM Global 为美国公司提供全面的注册后合规管理。我们的团队确保您的印度实体准确履行所有法定义务。我们代表您处理从纳税申报到年度申报表的所有事宜。这项服务使您的公司保持良好的法律地位。

我们的服务包括几个关键功能:

我们管理贵公司的完整合规日程表和法定文件。这包括每月商品及服务税申报表、TDS付款和年度ROC申报。我们的团队会跟踪所有截止日期并及时提交文件。您会定期收到合规状态报告。

您将获得一位了解您业务的指定客户经理。该专家与我们的审计和税务团队协调,提供无缝服务。他们是您处理所有合规事宜的单一联系人。这确保了持续和可靠的支持。

我们持续监控印度公司法、税法和劳动法的变化。我们的团队会就必要的流程或政策调整为您提供建议。这种主动的方法可以防止由于监管变化而导致的合规漏洞。它可以帮助您避免处罚并维持运营。

与VJM Global合作可确保您的印度公司保持完全合规,同时您可以专注于增长。

一个另请阅读: 向印度外包税务服务:美国公司指南

公司成立后的程序涉及几个强制性的合规步骤。其中包括税务登记、法定审计和持续的监管申报。适当的管理可确保您的印度实体合法高效地运营。了解这些要求对于长期成功至关重要。

VJM Global 专门管理在印度的美国公司的注册后合规性。我们的团队代表您处理所有法定要求和监管文件。我们提供针对您的特定业务运营量身定制的专家指导。这可确保您的公司完全遵守印度法律。

立即联系 VJM Global 确保您的印度公司满足所有注册后要求。

您必须在收到公司注册证书后的三十天内任命一名法定审计师。您还必须在同一三十天内举行第一次董事会会议。这些是印度公司法下最直接的法律要求。

注册成立后,您应立即开设公司银行账户。此项行动没有具体的法定截止日期。但是,如果没有专门的公司账户,您就无法开展业务或接收付款。延迟此步骤将导致您的运行启动停止。

如果您的公司在常规计划下注册,则必须提交每月的商品及服务税申报表。您还必须每月从工资和某些供应商付款中扣除和存入TDS。如果您有员工,则公积金和ESI供款需要每月申报和付款。

如果您的年营业额超过2000万卢比(或特殊类别州的1000万卢比),则需要进行商品及服务税登记。电子商务和州际供应等某些活动,无论营业额如何,也需要进行商品及服务税登记。大多数企业在成立后立即注册商品及服务税。

逾期申报会受到严厉处罚,罚款随着延迟时间的推移而增加。董事可能因严重不遵守年度申报表而被取消资格。公司注册处长还可以将您的公司归类为因长期违规行为而已停业。