.avif)

If you purchase $250,000 worth of equipment this year, you may be able to deduct the full amount from your taxable income in the same year. This tax rule is called bonus depreciation, and it can free up cash for other business needs.

In 2025, the law still allows 100% bonus depreciation, which means qualifying assets can be written off immediately instead of over several years.

This can make a big difference in cash flow and help you plan larger investments without waiting for long-term tax benefits.

In the next sections, we’ll explain how bonus depreciation works, what assets qualify, and how to use it effectively for your business or clients.

Bonus depreciation, officially called the additional first-year depreciation deduction under Section 168(k), lets you deduct the entire cost of qualifying assets in the year they’re placed in service.

Instead of spreading out write-offs across five, seven, or even twenty years, you claim the full tax benefit upfront. For U.S. businesses, this means bigger deductions and faster cash flow relief.

Traditionally, asset purchases (like machinery or computers) were written off annually. For example, a $100,000 equipment purchase would result in $20,000 deductions over five years. With bonus depreciation, you deduct the whole $100,000 in year one, putting that money back into your business immediately.

Bonus depreciation started as a stimulus measure at 30% in 2002. Over the years, Congress increased rates, reaching 100% after the Tax Cuts and Jobs Act (TCJA) in 2017.

The TCJA set up a phase-out: 100% for assets placed in service through 2022, then dropping by 20% each year, set to reach 0% in 2027.

In July 2025, the “One Big Beautiful Bill Act” permanently restored 100% bonus depreciation. To qualify, property must be acquired and placed in service after January 19, 2025.

If it was acquired before this date, even if placed in service later, it only qualifies for the previous year’s lower rate (40% for 2025).

If you want to learn which assets qualify and how to maximise this tax break, keep reading, next, we’ll break down eligibility rules and qualifying property under Section 168(k).

Also Read: Understanding Why Companies Use Accrual Accounting

Now that you know the basics, let’s look at which types of property actually qualify for bonus depreciation and what rules you’ll need to follow.

You can claim bonus depreciation only on assets classified as eligible property under IRS rules.

The key types include:

MACRS Property (Modified Accelerated Cost Recovery System): Tangible business assets with a recovery period of 20 years or less. This covers machinery, heavy equipment, furniture, computers, and vehicles.

Computer Software: Off-the-shelf software purchased for business use may qualify.

Vehicles & Equipment: Business vehicles (trucks, vans, heavy SUVs), office furniture, manufacturing gear, and more. Note: Passenger automobiles under 6,000 pounds have first-year deduction caps, check the current IRS limits.

Qualified Improvement Property (QIP): Interior improvements made by the taxpayer to non-residential (commercial) buildings, such as new HVAC, lighting, drywall, or ceilings. Building enlargements, elevators, escalators, or structural frameworks do NOT qualify.

Qualified Production Property (QPP): For manufacturing businesses, assets built or acquired specifically for production after January 19, 2025, are eligible for 100% expensing under OBBBA.

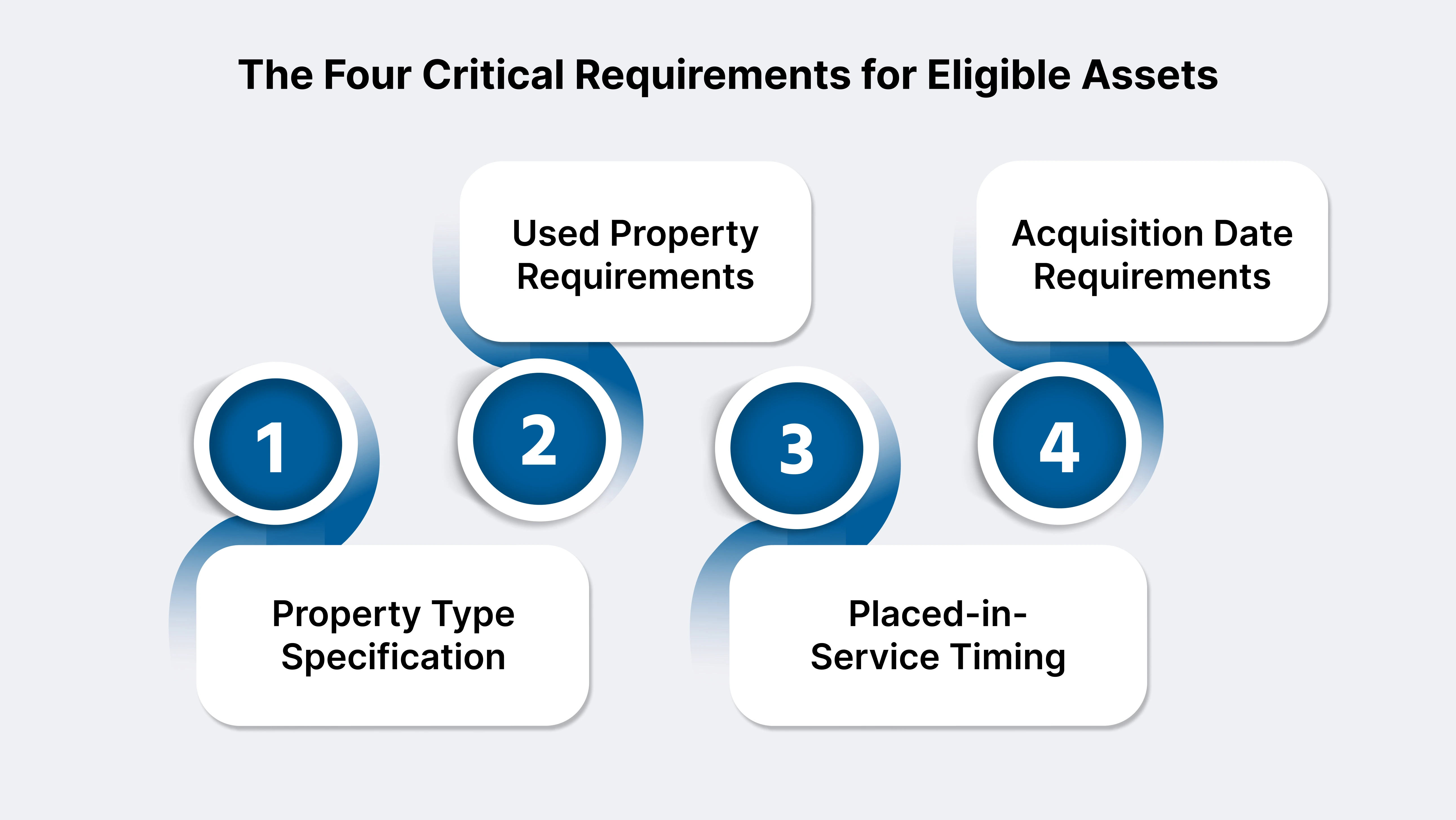

Only tangible property with a recovery period of 20 years or less, including certain software and improvements, is eligible.

The new property qualifies. Used property qualifies if acquired in an arm’s-length transaction and the taxpayer has not previously used it.

Related parties or previously used assets by the taxpayer are excluded; this avoids "churning" assets for additional deductions.

Assets must be placed in service in your business after January 19, 2025, for 100% bonus depreciation eligibility. If acquired on or before this date, the previous (reduced) rate applies.

Property acquired under a binding written contract dated before January 19, 2025, will not qualify for the 100% rate, even if placed in service after this date. it will get only the previous year’s lower rate.

The acquisition date for bonus depreciation is when the binding contract is executed, not when you take physical possession.

Certain property types are NOT eligible for bonus depreciation:

Also Read: How to Manage Accounting for Small Businesses

If you want to write off new assets fast and free up cash to invest elsewhere, confirm the asset fits IRS definitions, secure it after January 19, 2025, and never purchase from related parties.

For complex cases, like mixed-use property, building upgrades, or asset purchases through mergers, consult your tax advisor or VJM Global’s experts so your business gets the full value from bonus depreciation.

Once you know your assets are eligible, the next step is figuring out how to accurately calculate your bonus depreciation deduction.

Bonus depreciation can be a game-changer for your business’s tax planning. Here’s how you can confidently calculate and maximize this deduction.

Let’s break down the steps for bonus depreciation calculation:

Bonus Depreciation Deduction = (Asset Cost−Section 179 Tax Credits) × Bonus Rate

Also Read: Accounts Payable Outsourcing Costs and Savings

You buy $500,000 in manufacturing equipment. You’ve already applied $150,000 in Section 179. The 2025 bonus rate is 100% for eligible purchases under OBBBA, otherwise 40%.

Tax Savings Impact:

Your business keeps more cash for reinvesting or covering expenses.

You invest $50,000 in software and computer systems. No Section 179 applied.

Regular depreciation would split this over several years, limiting immediate savings.

Business vehicles often qualify, but passenger autos face first-year deduction caps. For luxury vehicles placed in service in 2025:

Heavy SUVs and trucks (over 6,000 pounds gross vehicle weight) aren’t limited and can leverage full bonus depreciation, but lighter passenger cars follow these IRS caps.

If you buy a mix of assets (equipment, computers, vehicles):

For purchases above the Section 179 limit (e.g., >$1.22M in 2025), apply Section 179 up to the cap, then bonus depreciation for the rest, and use regular depreciation for the final basis.

Suppose you purchase property with multiple components (buildings, fixtures, land improvements). In that case, a cost segregation study can separate eligible assets so you can apply bonus depreciation on items with recovery periods of 20 years or less.

This unlocks much larger first-year deductions and bigger cash tax savings for complex purchases.

Also Read: What is the Percentage of Completion Accounting Method?

As you plan your deductions, understanding how bonus depreciation compares with Section 179 can help you get the most out of each option.

When planning your business asset purchases, understanding how bonus depreciation stacks up against Section 179 is key for maximizing tax benefits. Here’s what you need to know:

Most businesses apply Section 179 first. Once you hit the Section 179 or income limit, apply bonus depreciation to the remaining asset basis.

This two-step approach maximizes your current-year deductions while keeping flexibility for future years.

Understanding the strengths and limits of each method helps you time major purchases, forecast tax outcomes, and support your clients with smart planning.

If you want advice on maximizing both Section 179 and bonus depreciation for your U.S. business’s unique needs, VJM Global’s team can guide you through every step, so you keep more of what you earn and reinvest in future growth.

Also Read: Notes Payable vs Accounts Payable: Key Differences Explained

Sometimes, taking every available deduction isn’t the best move—let’s explore when and why you might choose to opt out of bonus depreciation.

Choosing to elect out of bonus depreciation is a strategic move that can impact your current and future tax liability. Knowing when and how to opt out can help you maximize tax advantages, avoid surprises, and plan with precision.

Why would you skip immediate bonus depreciation and spread deductions over several years? Here are the situations where this makes sense:

1. Income Smoothing: If your business expects higher profits in future years, saving deductions by electing out allows you to offset future income rather than using them up in a low-income year.

2. Alternative Minimum Tax (AMT): Bonus depreciation can trigger or increase AMT liability. Electing out can reduce exposure, giving you more control over how depreciation impacts your tax situation.

3. Future Year Planning: If you're tracking income spikes (like large contracts, business sales, or other big events), you might want steady deductions later. Opting out gives you this flexibility.

4. State Tax Conformity Issues: Not every state allows federal bonus depreciation. Electing out prevents large federal tax deductions that may not be useful on your state return, avoiding complex adjustments.

5. Passive Activity Loss Limitations: For investors or businesses facing limits on passive losses, bonus depreciation might create losses you can’t use. Electing out preserves these deductions for more favorable years.

If you decide to elect out, here’s how to do it properly; mistakes can’t be easily reversed!

Opting out of bonus depreciation may seem counterintuitive, but it provides powerful control over when and how deductions are used.

Taking the time to analyze your year-end strategy, future growth, and state tax position will help you make the best choice for your business.

Also Read: How Much Does a CPA Charge for Tax Preparation

If you’re looking to truly optimize your tax outcomes, advanced planning strategies can make a significant difference to your bottom line.

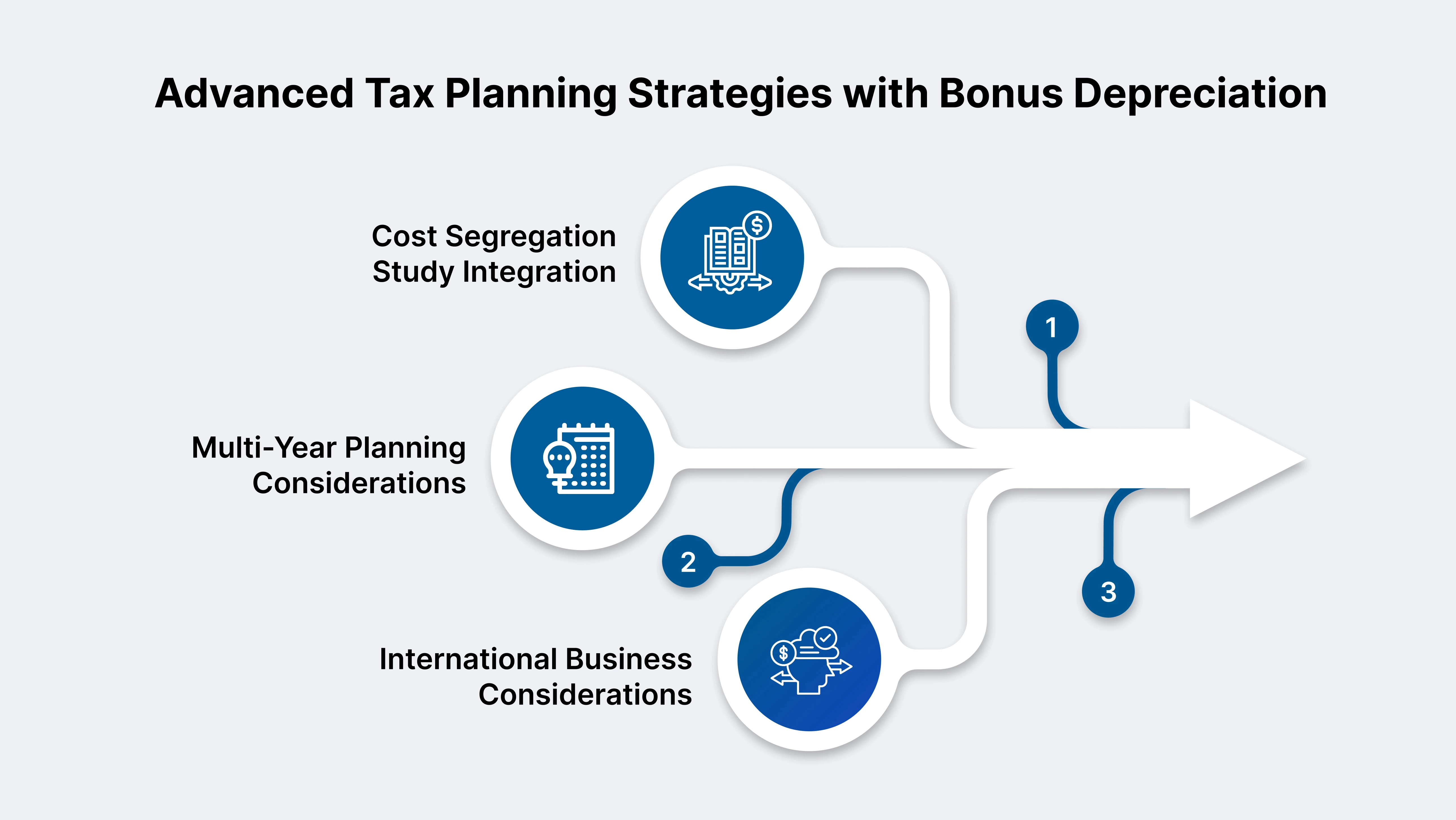

Bonus depreciation tax planning unlocks powerful opportunities for U.S. businesses to supercharge cash flow, strategically time deductions, and optimize real estate and international expansions. Here’s how to level up your strategy:

Wondering how to get maximum upfront deductions on your property investments? A cost segregation study is your answer.

This analysis breaks down a building’s cost into shorter-lived components, think carpets, electrical, and HVAC. Even specialty equipment, which can be depreciated over five, seven, or fifteen years instead of the standard 39 or 27.5 years.

With 100% bonus depreciation now permanent for most eligible assets placed in service after Jan. 19, 2025. Every dollar allocated to short-life property through cost segregation can be written off immediately.

That means real estate investors and business owners can unlock sizable first-year tax deductions and accelerate cash flow.

For best results, engage specialists who understand both engineering and IRS compliance to ensure assets are classified correctly and documentation stands up to audit scrutiny.

Getting the timing right on asset purchases and deductions is crucial. Here’s how to plan for continuous savings, year after year:

Don’t forget state-level planning: Some states decouple from federal bonus depreciation, so coordinate federal and state schedules to avoid unwanted surprises.

Cross-border asset investments require careful planning to capture bonus depreciation benefits and avoid complications:

1. U.S. Subsidiary Structures for Foreign Companies: Setting up a U.S. subsidiary allows foreign businesses to utilize bonus depreciation on qualified assets if placed in service domestically. Structure acquisitions to maximize eligibility and document all contracts and placed-in-service dates.

2. Cross-Border Acquisition Planning: When acquiring assets for a global expansion, check U.S. and foreign-country depreciation rules. Bonus depreciation can make U.S. expansion much more attractive from a tax and cash-flow standpoint.

3. India Expansion Implications: If your U.S. business is expanding into India, VJM Global guides you through navigating local depreciation rules and synchronizing asset purchases and entity structures on both sides.

This ensures your cross-border investment is tax-optimized and compliant with both IRS and Indian regulatory requirements.

Also Read: Strategic Tax Planning Services for Businesses

With these strategies in mind, you’re ready to put a concrete action plan in place to maximize your bonus depreciation benefits in 2025.

As you plan your investments for 2025, these steps can help you maximize bonus depreciation and keep more cash in your business:

Also Read: Comprehensive Cross-Border Tax Planning Strategies

Deciding when to engage with tax experts is crucial:

With these strategies in mind, you’re ready to put a concrete action plan in place to maximize your bonus depreciation benefits in 2025.

Bonus depreciation remains one of the most effective tax tools for U.S. businesses, especially with the permanent 100% rate for qualifying assets acquired after January 19.

From accelerating deductions on equipment, vehicles, and QIP to leveraging cost segregation for real estate, the opportunities extend far beyond a single tax year.

The right strategy can boost cash flow, support expansion, and lower overall tax liability while keeping your operations fully compliant.

However, bonus depreciation planning requires precision; missteps in timing, documentation, or asset classification can reduce or eliminate the benefit. Professional guidance ensures every deduction is optimized, every rule followed, and every opportunity captured.

Ready to maximize your bonus depreciation benefits?

Contact VJM Global's expert team for personalized strategies that align with your business goals and ensure full compliance. With expert planning, you can invest confidently today and enjoy sustainable tax savings for years to come.

Bonus depreciation doesn’t apply directly to land or buildings, but qualified improvement property (QIP), like interior upgrades to nonresidential buildings, does qualify. A cost segregation study can help identify eligible building components.

Yes. Taxpayers can elect out of bonus depreciation on a class-by-class basis. This election must be made when filing your return with Form 4562, and is generally irrevocable for that year.

The OBBBA permanently reinstated 100% bonus depreciation for assets acquired and placed in service after January 19, 2025, eliminating the previous phaseout. This means you can fully deduct qualifying property without yearly reductions.

Yes. If bonus depreciation exceeds your taxable income, it can create a net operating loss, which can be carried forward to offset future income.

Section 179 lets you selectively expense assets up to $2.5M (2025 limit) and is limited by taxable income, while bonus depreciation has no dollar or income cap and applies automatically to all eligible assets unless you opt out.

Report bonus depreciation on IRS Form 4562 when filing your federal tax return for the year the property is placed in service. Attach documentation for acquisition and the placed-in-service dates.