For developers, rental managers, brokers, and foreign investors, getting the accounting right in Dubai now means navigating four overlapping systems simultaneously: IFRS revenue standards, RERA escrow rules, FTA tax obligations, and Ministry of Economy AML requirements. Miss one, and the consequences range from disallowed input tax to license revocation.

This guide covers what makes Dubai real estate accounting different in 2025, the regulatory framework you must understand, core accounting components, VAT and corporate tax treatment, and the mistakes that cost businesses most.

Key Takeaways

- Dubai mandates IFRS as its accounting standard—non-compliance risks financial penalties and license suspension

- Off-plan escrow accounts are governed by Dubai Law No. (8) of 2007, not the commonly cited Law No. 2 of 2015

- UAE Corporate Tax at 9% (above AED 375,000 taxable income) applies to most real estate businesses

- Real estate brokers are classified as DNFBPs—AML penalties reach AED 5,000,000 per violation

- Retention rules are strict: CT records require 7 years, broker AML records require 5 years

What Makes Dubai Real Estate Accounting Unique in 2025

Most markets require businesses to follow one accounting framework. Dubai requires several at once.

Real estate businesses here must comply with IFRS (set globally), UAE Corporate Tax law (administered by the FTA), RERA rules (specific to property development and strata management), and Ministry of Economy AML obligations. These frameworks frequently conflict — IFRS 15 recognises revenue based on performance obligations, while the FTA tax point may fall at a different stage entirely. The compliance burden also varies depending on what type of real estate business you operate.

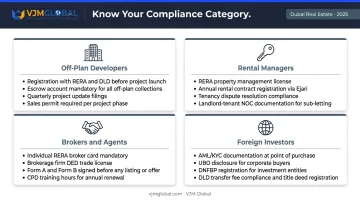

Know Your Category First

Each business type carries different obligations:

- Off-plan developers — RERA escrow accounts, IFRS 15 revenue recognition, VAT on construction milestones, CT on project profits

- Rental managers — IFRS 16 lease accounting, VAT invoicing, service charge reporting

- Brokers and agents — DNFBP/AML registration, CDD obligations, 5-year transaction record retention

- Foreign investors — CT registration, withholding tax analysis, and entity-type determination (natural person vs. licensed entity) each trigger separate filing obligations

What cuts across all these categories is a new enforcement layer. The FTA-DLD digital linkage announced in October 2024 connects Dubai Land Department transaction data directly to FTA systems, meaning tax authorities can now cross-reference property transactions against VAT filings in near real-time. Businesses that have been manually reconciling these separately face new exposure.

Regulatory Framework: RERA, FTA, IFRS, and DNFBP Requirements

Under Federal Decree-Law No. 32 of 2021, UAE companies must apply international accounting practices and standards when preparing accounts. The IFRS Foundation confirms the UAE has adopted both full IFRS and IFRS for SMEs—public companies and large developers must apply full IFRS, while smaller operators may use the SME version. Departing from IFRS without justification can trigger regulatory scrutiny during audits.

Beyond IFRS compliance, Dubai real estate businesses face sector-specific financial controls—primarily through RERA.

RERA's Financial Oversight Role

RERA governs three key financial areas for real estate businesses:

- Escrow accounts for off-plan developments (project funds segregated from operating accounts)

- Service charge auditing for strata properties

- Financial registration requirements via the Dubai Land Department

The correct legal basis for Dubai's off-plan escrow regime is Dubai Law No. (8) of 2007 (not the frequently cited Law No. 2 of 2015, which is unverified in official sources). Under this law, developers selling off-plan units must open project-specific escrow accounts. Funds are only releasable after a trustee engineer verifies construction milestones.

Two articles carry particular weight: Article 9 protects project funds from developer creditors, and Article 14 requires a 5% retention for one year post-completion.

RERA can audit these accounts at any time. Non-compliance carries serious legal and financial consequences.

DNFBP and AML Compliance for Real Estate

Real estate brokers and agents are classified as Designated Non-Financial Businesses and Professions (DNFBPs) under UAE AML law. This classification requires:

- Customer due diligence (CDD) on all clients

- Transaction record maintenance for at least 5 years

- Reporting of suspicious transactions to the Financial Intelligence Unit (FIU)

- Appointment of a designated compliance officer

The Ministry of Economy enforces DNFBP compliance and has demonstrated it will act. In Q1 2023 alone, the MoE imposed AED 65.9 million in fines on 137 DNFBP companies following 840 inspections. Current AML administrative penalties range from AED 10,000 to AED 5,000,000 per violation.

Smaller brokerages that haven't yet appointed a compliance officer or established CDD procedures are directly exposed to these penalties—making AML compliance a practical priority, not a formality.

Core Accounting Components for Dubai Real Estate Businesses

Revenue Recognition for Property Sales and Rentals

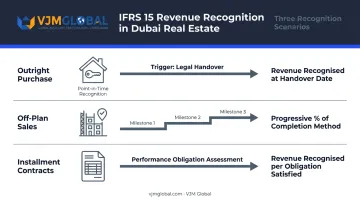

Revenue recognition in Dubai real estate follows IFRS 15, which focuses on when control transfers—not when cash is received. Three scenarios apply:

- Outright purchase — Revenue recognized at legal handover (point-in-time recognition)

- Off-plan sales — Revenue recognized progressively using the percentage-of-completion method as construction milestones are verified; this requires meeting specific IFRS 15 over-time criteria (such as the developer having an enforceable right to payment for work completed)

- Installment contracts — Payment terms must be assessed against performance obligations; cash received does not equal revenue earned under IFRS 15

For rental income, the accrual basis applies: rent is recorded in the period it falls due, matched with corresponding expenses (service charges, maintenance) in the same period.

Revenue treatment tells only part of the story. How a business accounts for the spaces and assets it occupies is equally consequential — and that's where IFRS 16 comes in.

Lease Accounting under IFRS 16

Under IFRS 16, most leases exceeding 12 months must appear on the balance sheet.

The lessee records:

- A right-of-use (ROU) asset for each leased property or equipment item

- A corresponding lease liability for future payment obligations

- Depreciation on the ROU asset (income statement)

- Interest expense on the lease liability (income statement, separate from depreciation)

This matters practically because it changes key financial ratios — debt-to-equity, EBITDA, and return on assets — that lenders and investors use to assess real estate businesses. Property managers leasing office space or equipment can no longer keep these obligations off-balance-sheet.

Chart of Accounts and Escrow Management

A well-structured chart of accounts for Dubai real estate should include these primary categories:

| Category | Examples |

|---|---|

| Revenue | Rental income, sales proceeds, commissions |

| Cost of Sales | Maintenance, legal fees, contractor payments |

| Contract Assets | Land, buildings, receivables |

| Contract Liabilities | Deposits, advances, loans |

| Equity | Share capital, retained earnings |

Escrow accounts must be maintained separately from operating accounts, with detailed records of every inflow, disbursement, and milestone-triggered release. RERA auditors specifically examine these records; gaps in documentation can trigger fines, license suspensions, or forced project halts — not simply a note in the audit report.

VAT and Corporate Tax: Key Considerations for 2025

VAT Treatment for Real Estate Transactions

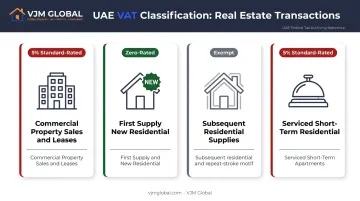

VAT classification varies by property type and transaction stage:

| Transaction | VAT Treatment |

|---|---|

| Commercial property sales and leases | 5% standard-rated |

| First supply of new residential property (within 3 years of completion) | Zero-rated |

| Subsequent residential property supplies | Exempt |

| Serviced/short-term residential accommodation | 5% standard-rated |

Getting this wrong creates two problems: over-charging VAT on exempt supplies exposes you to customer disputes, while under-charging on taxable supplies creates a liability with penalties.

VAT registration is mandatory once taxable supplies exceed AED 375,000 — voluntary registration opens at AED 187,500. Missing the mandatory threshold triggers backdated VAT liability and penalties, so monitor your taxable supply thresholds closely.

Every FTA-compliant tax invoice must include the supplier's Tax Registration Number (TRN), transaction date, description, and VAT amount. Non-compliant invoices disallow input tax recovery.

Corporate Tax Implications for Real Estate Businesses

UAE Corporate Tax applies to financial years starting on or after 1 June 2023:

- 0% on taxable income up to AED 375,000

- 9% on taxable income above AED 375,000

Developers, property managers, and brokers are all subject to CT. Natural persons earning passive real estate investment income may be exempt—but only where no UAE business licence or permit is required for that activity. Licensed real estate activity is generally taxable.

Free Zone status doesn't automatically mean lower tax on property income. Businesses in a Free Zone may access the 0% rate on qualifying income, but income from UAE mainland real estate — including sales or rentals to mainland customers — is generally treated as non-qualifying income and taxed at 9%.

Key deductible expenses under CT for real estate include:

- Interest on financing (subject to the 30% of EBITDA interest limitation rule where net interest exceeds AED 12 million)

- Depreciation on investment property

- Maintenance and operating costs

Under FTA audit, each deduction must be supported by documentation — invoices, contracts, depreciation schedules, and financing statements. Gaps in records translate directly into disallowed deductions and increased tax exposure.

Common Accounting Mistakes to Avoid in Dubai Real Estate

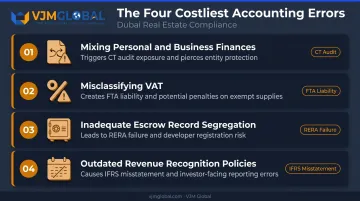

The Four Costliest Errors

- Mixing personal and business finances — Particularly common among individual investors managing multiple properties; this complicates CT computations and creates audit exposure

- Misclassifying VAT — Treating exempt residential supplies as taxable, or failing to apply zero-rating correctly on first residential supplies; both create FTA liability

- Inadequate escrow record segregation — Each project requires separate escrow records; commingled records across projects is a direct RERA compliance failure

- Outdated revenue recognition policies — Failing to update policies when transitioning between project phases (pre-sale to construction to handover) leads to misstatement under IFRS 15

Record Retention: The Numbers That Matter

UAE record retention requirements are not uniform—they differ by obligation type:

| Record Type | Retention Period |

|---|---|

| Corporate Tax records | 7 years after end of tax period |

| Real estate broker AML records | 5 years |

| VAT records (invoices, credit notes, adjustments) | As required under VAT Decree-Law Article 78 |

The FTA has confirmed the 7-year CT record retention requirement applies to both taxable and exempt persons. Failure to maintain required records carries penalties of AED 10,000 for a first violation and AED 20,000 for repeat violations under Cabinet Decision No. 40 of 2017.

Incomplete records during an FTA audit can result in estimated assessments (where the FTA imposes tax based on available data rather than actual figures). In practice, estimated assessments almost always land higher than what accurate records would have produced.

DNFBP Compliance Is Not Optional

Record-keeping failures can compound quickly when AML obligations are also unmet. Real estate agents who haven't registered AML policies, appointed a compliance officer, or implemented CDD procedures face mounting enforcement risk. The MoE's Q1 2023 campaign — AED 65.9 million in fines across 137 companies — shows the Ministry is auditing and penalizing, not just issuing warnings.

Choosing the Right Accounting Approach: Methods, Tools, and Expert Support

Accrual vs. Cash Accounting

| Method | Best For | IFRS Compliant? |

|---|---|---|

| Accrual | Developers, large managers, off-plan projects | Yes |

| Cash | Small agencies, straightforward transactions | No |

Only accrual accounting satisfies IFRS requirements and provides the financial picture that RERA auditors and lenders expect. Cash accounting may simplify day-to-day bookkeeping for a sole agent, but it won't hold up to scrutiny.

Accounting Software for UAE Real Estate

Several platforms support UAE compliance requirements:

- Xero — FTA-confirmed accredited software; supports VAT return automation and EmaraTax field alignment

- Zoho Books — Documents UAE VAT return support including standard-rated, zero-rated, exempt, and reverse-charge transactions

- QuickBooks Online — Widely used for VAT tracking; UAE FTA accreditation status not formally confirmed

- Yardi / MRI Software — Property-specific platforms with Middle East presence and real estate-specific GL, lease accounting, and AP/AR tools; UAE FTA accreditation status not formally verified

Before selecting software, verify current FTA accreditation status directly with the vendor—the accredited software vendor list on the FTA website is the authoritative source.

When to Bring in Expert Support

Software handles the mechanics, but navigating UAE tax law, IFRS, RERA, and AML obligations simultaneously requires human expertise. For foreign investors and international businesses, building an in-house accounting team fluent in all these frameworks is expensive and slow to scale.

Outsourcing to a firm already operating across these requirements is the faster path to compliance.

VJM Global provides outsourced accounting and compliance services for real estate businesses operating in the UAE, covering:

- Transaction recording and financial reporting under IFRS

- VAT compliance and tax filing management

- Cloud platform integration via QuickBooks and Xero

Their team has supported foreign investors navigating UAE real estate accounting, including publishing a U.S. Investors' Guide to Real Estate Accounting in the UAE. Reach them at info@vjmglobal.com.

Frequently Asked Questions

Which accounting standard is used in Dubai?

Dubai follows International Financial Reporting Standards (IFRS) as the mandated framework under Federal Decree-Law No. 32 of 2021. Public companies and large developers must apply full IFRS, while smaller businesses may adopt IFRS for SMEs.

Is CA or ACCA better in Dubai?

Both qualifications are recognized in Dubai. ACCA carries broad international recognition and is widely accepted by UAE firms, while Indian CAs are commonly employed given the large Indian professional community in the UAE. Your choice should align with your target employers — multinational firms typically favor ACCA; regional or Indian-owned firms often prefer CA.

What is the VAT rate on commercial properties in Dubai?

Commercial property sales and leases are subject to 5% VAT. Residential properties are zero-rated on first supply (within 3 years of completion) and VAT-exempt on subsequent supplies. FTA registration is mandatory once taxable supplies exceed AED 375,000.

Do real estate developers in Dubai need to maintain escrow accounts?

Yes. Dubai Law No. (8) of 2007 mandates separate project escrow accounts for all off-plan developments. Funds are only releasable upon trustee engineer verification of construction milestones and are subject to RERA audit at any time.

Are real estate businesses subject to UAE Corporate Tax?

Developers, brokers, and property managers are subject to 9% CT on taxable income above AED 375,000. Free Zone businesses may access the 0% rate on qualifying income, but mainland real estate income is taxable at the standard rate.

How long must real estate businesses retain financial records in Dubai?

Corporate Tax records must be retained for 7 years after the end of the relevant tax period. Real estate broker AML records must be kept for at least 5 years. All records must be available for FTA or MoE inspection upon request.