Introduction

Dubai tax compliance refers to the set of legal obligations — corporate tax, VAT, and Economic Substance Regulations — that all businesses operating in the UAE must meet, including those incorporated by Singapore companies.

Many Singapore businesses face a critical compliance blind spot fuelled by the outdated "tax-free Dubai" narrative. While partially true for personal income, this label misses the 9% corporate tax, 5% VAT, and dual reporting obligations that came into effect from 2023 onwards.

The Federal Tax Authority (FTA) has significantly intensified enforcement: in 2025, the FTA conducted approximately 176,000 market inspections, an 89% year-on-year increase, and identified over AED 608 million in tax dues and penalties. For Singapore businesses with UAE operations, missing these obligations means real financial exposure — not a theoretical risk.

Key Takeaways

- Dubai levies no personal income tax, but Singapore businesses must comply with 9% corporate tax (on taxable income above AED 375,000), 5% VAT, and Economic Substance Regulations

- The UAE-Singapore Double Tax Agreement prevents double taxation but requires active documentation through a Tax Residency Certificate — you must apply for it; it does not apply by default

- All businesses, including free zone entities, must register for corporate tax and file annual returns within nine months of financial year-end

- Penalties for non-compliance include a AED 10,000 late registration fee and 14% annual interest on unpaid taxes, effective from April 2026

Dubai's Tax Landscape: What Singapore Businesses Actually Face

The "Tax-Free" Label Only Applies to Personal Income

The UAE imposes no personal income tax, salary tax, or capital gains tax on individuals. Corporate entities face a different reality — they fall under the UAE corporate tax regime introduced under Federal Decree-Law No. 47 of 2022 for financial years beginning on or after 1 June 2023.

Three Core Tax Types for Singapore Businesses

Corporate Tax:

- 0% on taxable income up to AED 375,000

- 9% on taxable income exceeding AED 375,000

- Domestic Minimum Top-Up Tax (DMTT) of 15% for large multinationals with consolidated global revenues of €750 million or more

VAT:

- Standard rate of 5% on most goods and services

- Mandatory registration when annual taxable supplies exceed AED 375,000

- Voluntary registration available at AED 187,500 threshold

Economic Substance Regulations:

- Apply to holding companies, IP management entities, headquarters operations, and distribution centres

- Require genuine economic presence in the UAE

The FTA's Digital Enforcement System

The Federal Tax Authority administers all taxes through the EmaraTax digital platform for registration, filing, and payments. The FTA uses a risk-based audit approach, and enforcement has escalated sharply. In 2025, identified tax dues and penalties jumped from AED 348 million to over AED 608 million — a 75% year-on-year increase. Singapore businesses that treat UAE tax obligations as administrative formalities are now the ones receiving audit notices.

What Does NOT Apply to Singapore Businesses

That said, several tax types common in other jurisdictions simply don't exist in the UAE. Singapore businesses can disregard:

- Withholding tax on dividends, interest, or royalties (currently set at 0%)

- Inheritance tax

- Annual property tax (though a 4% transfer fee applies on property transactions in Dubai)

Key Dubai Tax Obligations for Singapore Businesses

Corporate Tax Registration: Strict Timelines

- Singapore businesses incorporated in the UAE on or after 1 March 2024 must register within three months of incorporation

- Failure to register on time triggers an AED 10,000 administrative penalty

- A waiver initiative exists for first-period filers who submit returns within their first tax period

VAT Registration and Filing

- Mandatory registration when annual taxable supplies and imports exceed AED 375,000

- Voluntary registration available above AED 187,500

- VAT returns filed quarterly through EmaraTax

Late-filing penalties (updated April 2026): Under Cabinet Decision No. 129 of 2025, effective 14 April 2026:

- Late or incorrect VAT filing: AED 500 (reduced from AED 1,000-2,000)

- Late VAT payment: 14% per annum applied monthly (replacing the old 2% immediate plus 4% monthly structure)

Economic Substance Regulations (ESR)

ESR applies to entities conducting any of these activities in the UAE:

- Holding companies

- IP management entities

- Headquarters operations

- Distribution centres

- Banking, insurance, investment fund management, lease-finance, and shipping businesses

Once you've confirmed your entity is in scope, you'll need to satisfy these ongoing requirements:

- Adequate UAE-based employees

- Sufficient operating expenditure in the UAE

- Core income-generating activities conducted locally

- Annual Notification Form and Economic Substance Report filed within 12 months of financial year-end through the MoF ESR Portal

While ESR filings were initially required for 2019-2022, substance documentation remains critical during FTA audits and continues to apply for ongoing compliance.

Record-Keeping Requirements

- All businesses must retain financial records, invoices, and supporting documents for seven years after the end of the applicable tax period

- Failure to maintain records: AED 10,000 fine (first violation); AED 20,000 for repeat violations within 24 months

Five-Step Compliance Calendar

With these obligations in mind, here's how to translate them into a practical action sequence:

- Register for corporate tax via EmaraTax within 3 months of incorporation or based on your trade licence date

- Complete VAT registration if annual taxable supplies exceed AED 375,000

- Prepare financial statements per IFRS standards — audited statements are mandatory if revenue exceeds AED 50 million or your entity qualifies as a QFZP

- File your corporate tax return and settle any tax payable within nine months of financial year-end (a 31 December year-end means a 30 September deadline)

- File VAT returns on your FTA-assigned frequency (quarterly for most businesses) and pay within the deadline

The Singapore-UAE Double Tax Agreement: Protecting Your Business from Double Taxation

What the DTA Covers

The Singapore-UAE DTA is a bilateral agreement that prevents the same income from being taxed in both jurisdictions. The original agreement entered into force on 30 August 1996, with MLI modifications effective from 1 September 2019.

Income types covered:

- Business profits

- Dividends (treaty rate: 0% for government/qualified entities with 10%+ ownership; 5% for other cases)

- Interest (treaty rate: 0%)

- Royalties (treaty rate: 5%)

- Capital gains

Singapore is among the 130+ countries with which the UAE has concluded a DTA — meaning your business has direct treaty access, not just a general framework.

How to Claim DTA Benefits Operationally

Singapore businesses must hold a UAE Tax Residency Certificate (TRC) issued by the FTA to claim treaty benefits. Apply for the TRC through the FTA's online platform. This certificate confirms UAE tax residency status and is the primary documentation required to avoid double taxation on cross-border income flows.

The Singapore Side: Territorial Tax System with Caveats

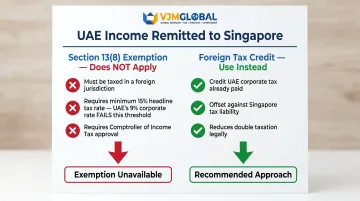

Singapore uses a territorial tax system, meaning income earned and taxed in a foreign jurisdiction is generally not re-taxed by IRAS when remitted to Singapore. However, Section 13(8) of the Singapore Income Tax Act requires three conditions for foreign-sourced income exemption:

- Income was subject to tax in the foreign jurisdiction

- The headline corporate tax rate of the foreign jurisdiction is at least 15% at the time income is received in Singapore

- The Comptroller is satisfied the exemption is beneficial to the company

UAE income gap: The UAE's 9% corporate tax rate falls below the 15% threshold. Singapore companies remitting UAE income will generally not qualify for the Section 13(8) exemption. Instead, claim foreign tax credits for UAE corporate tax paid against Singapore tax payable on the same income.

The Practical Risk

Many Singapore businesses assume the DTA automatically protects them without any filing action. It doesn't. Failing to obtain a TRC — or to document treaty claims properly — means losing that protection and facing tax exposure in both jurisdictions.

Getting this right requires proactive documentation: the TRC, evidence of income sourcing, and correctly filed positions in both jurisdictions. Professional cross-border tax advisors can help structure this before issues arise — not after.

Free Zone vs. Mainland: How Business Structure Affects Compliance

Mainland Companies: Full 9% Tax on All Income

Mainland companies incorporated under the UAE Commercial Companies Law are fully subject to 9% corporate tax on all taxable income above AED 375,000.

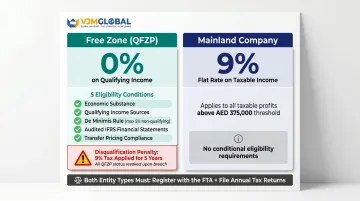

Free Zone Entities: Conditional 0% Rate

Free zone entities (DMCC, DIFC, Jebel Ali, etc.) may qualify for 0% corporate tax on qualifying income if they meet Qualifying Free Zone Person (QFZP) conditions. However, they remain within the scope of UAE corporate tax law and must register and file returns.

QFZP eligibility conditions:

- Maintain adequate substance in the free zone (sufficient employees, assets, operating expenditure)

- Derive qualifying income (manufacturing, trading qualifying commodities, holding shares, headquarters services, etc.)

- Meet the de minimis threshold: non-qualifying revenue must not exceed 5% of total revenue or AED 5 million, whichever is lower

- Prepare audited IFRS financial statements

- Comply with transfer pricing rules

Miss these conditions and the penalty is severe. Failure disqualifies the entity from the 0% rate for the current year plus the following four years — at the full 9% rate. Re-testing for QFZP status only becomes available in the sixth year.

VAT: No Difference Between Free Zones and Mainland

Corporate tax structure has no bearing on VAT obligations. Both free zone and mainland entities follow the same registration rules:

| Threshold Type | Amount | Obligation |

|---|---|---|

| Mandatory registration | AED 375,000 taxable turnover | Required |

| Voluntary registration | AED 187,500 taxable turnover | Optional |

One exception exists for designated free zones (Jebel Ali, Dubai Aviation City, Dubai Textile City, and others). These zones carry special VAT treatment for goods traded within them — but this exemption does not extend to services, which are taxed under standard UAE VAT rules regardless of location.

Common Misconceptions Singapore Businesses Have About Dubai Tax Compliance

Misconception 1: "Free Zone = Zero Tax and Zero Compliance"

Even if taxable income is zero or the 0% QFZP rate applies, companies must still register for corporate tax, file annual returns, and maintain IFRS-compliant records. Non-filing is penalised regardless of the tax amount owed. The AED 10,000 late registration penalty applies to all entities — including those with zero profit or those qualifying for 0% rates.

Misconception 2: "The DTA Eliminates All Tax Exposure Automatically"

The Singapore-UAE DTA is a tool, not a blanket exemption. It requires deliberate documentation:

- Obtaining a UAE Tax Residency Certificate

- Filing treaty elections with IRAS

- Maintaining proper supporting documentation

The DTA does not protect against VAT obligations, ESR requirements, or penalties for procedural non-compliance. Singapore businesses must actively claim treaty benefits through proper filing and documentation.

Misconception 3: "Compliance Is a One-Time Setup Task"

That documentation effort doesn't end after setup. Dubai tax compliance is an ongoing obligation:

- VAT filing recurs quarterly

- Corporate tax returns are due annually

- Record retention runs for seven years

- The April 2026 penalty reform changed how interest and fines are calculated

Businesses that treat compliance as a one-time checkbox frequently fall behind and face disproportionate penalties. From April 2026, the 14% per annum interest rate on unpaid taxes is applied monthly — meaning delays compound quickly.

Frequently Asked Questions

Do you have to file taxes in Dubai?

While Dubai has no personal income tax, businesses — including those owned by foreign nationals or incorporated by Singapore companies — must register for corporate tax and file annual returns. Companies exceeding AED 375,000 in taxable supplies must also register for and comply with VAT.

Does Singapore have a Double Tax Agreement with the UAE?

Yes, Singapore is among the 130+ countries with a DTA with the UAE. This agreement prevents the same income from being taxed in both countries, but businesses must actively claim treaty benefits by obtaining a UAE Tax Residency Certificate (TRC) from the FTA.

Do Singapore companies in Dubai free zones need to pay corporate tax?

Free zone companies must register and file corporate tax returns regardless. Those qualifying as Qualifying Free Zone Persons (QFZP) may apply a 0% rate on qualifying income, but non-qualifying income is taxed at 9%. Failure to meet QFZP conditions disqualifies the entity for five years.

What is the UAE corporate tax rate for foreign businesses?

The UAE applies 0% on taxable income up to AED 375,000 and 9% on income above that threshold. Large multinationals with consolidated global revenues of €750 million or more face an additional 15% Domestic Minimum Top-Up Tax from 1 January 2025.

What are the penalties for non-compliance with UAE tax obligations?

Key penalties include AED 10,000 for late corporate tax registration, 14% annual interest (accrued monthly) on unpaid taxes, AED 500 for late VAT filings, and AED 10,000–20,000 for failure to maintain records. Cabinet Decision No. 129 of 2025, effective April 2026, replaced the previously capped penalty structure with ongoing monthly interest charges.

Do US citizens pay income tax in Dubai?

Dubai levies no personal income tax on any individual, regardless of nationality. However, US citizens remain subject to US worldwide income reporting and must file federal returns regardless of where they live — though the Foreign Earned Income Exclusion may reduce the actual US tax liability.