Introduction

Accrual accounting is the legally required accounting method for most UK businesses — and understanding it correctly has real financial consequences. Many business owners confuse accrual accounting with simple cash tracking — watching money flow in and out of their bank account — but the two methods operate on different principles.

The key pain points are real and expensive. Confusion around when to record income and expenses leads to surprise tax bills, cash flow mismatches, and regulatory compliance headaches. A company can appear profitable on paper while struggling to pay suppliers, or face unexpected Corporation Tax liabilities because revenue was recorded in the wrong period.

This guide breaks down everything you need to know — from the legal obligations under UK GAAP to the common mistakes that trip up even experienced business owners.

Key Takeaways

- Accrual accounting records income when earned and expenses when incurred, not when cash changes hands

- UK limited companies are legally required to use accrual accounting under UK GAAP FRS 102

- Sole traders and partnerships may use cash basis, but accrual provides a more accurate financial picture

- Corporation Tax and VAT liabilities are calculated on an accrual basis for most UK businesses

What Is Accrual Accounting?

Accrual accounting means revenue is recorded when it is earned and expenses are recorded when they are incurred, regardless of when money physically moves. A consultant who invoices a client in March records that income in March, even if payment doesn't arrive until May. This differs from cash basis accounting, where transactions are only recorded when money actually moves in or out of your account.

The Matching Principle

The foundational concept behind accrual accounting is the matching principle. This requires that revenues and the expenses incurred to generate them are recognised in the same accounting period. If you incur £2,000 in freelance costs to complete a project in March, and invoice £5,000 for that project in March, both the income and the expense appear in your March accounts — regardless of when your client pays or when you settle the freelancer's invoice.

This approach provides a "true and fair view" of business finances, now embedded in the Companies Act 2006 and UK GAAP (FRS 102).

The shift to accruals was driven by a need for transparency. Stakeholders, investors, and HMRC need to understand financial performance based on economic activity — not just the timing of payments.

How It Differs from Double-Entry Bookkeeping

Accrual accounting is not the same as double-entry bookkeeping, though it relies on it. Double-entry is a recording system; accrual accounting governs when transactions should be recognised. It's also worth noting that this isn't just a large-company concern — all UK limited companies must use accrual accounting, regardless of size.

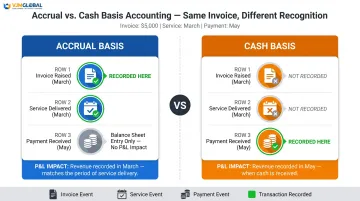

Side-by-Side Comparison: Accrual vs Cash Basis

| Transaction | Accrual Accounting | Cash Basis |

|---|---|---|

| Invoice raised 15 March for £3,000 | Income recorded in March | No entry in March |

| Payment received 10 May for £3,000 | No additional entry (already recorded) | Income recorded in May |

| Result | March P&L shows £3,000 income | May P&L shows £3,000 income |

For UK limited companies, accrual accounting is the required standard — the table above shows exactly why regulators and investors prefer it for a clear picture of business performance.

Accrual Accounting vs Cash Basis: Key Differences

Cash basis accounting records income and expenses only when money is received or paid. From 6 April 2024, cash basis became the default method for sole traders and partnerships filing Self Assessment. Businesses must now actively opt out if they prefer traditional accrual accounting.

Key Differences at a Glance

1. Timing of revenue recognition:

- Accrual: When invoice is raised or service delivered

- Cash basis: When payment is received

2. Timing of expense recognition:

- Accrual: When cost is incurred or invoice received

- Cash basis: When payment is made

3. Treatment of receivables and payables:

- Accrual: Tracked on the balance sheet as assets (debtors) and liabilities (creditors)

- Cash basis: Not tracked — only cash movements matter

4. Compliance with UK FRS/GAAP:

- Accrual: Required for all limited companies under FRS 102 or FRS 105

- Cash basis: Not permitted for limited companies

5. Suitability by business size:

- Accrual: Suitable for all business types, especially those with stock, debtors, or seeking investment

- Cash basis: Best for very small sole traders with simple operations

Advantages of Accrual Accounting

- Matches revenue with the costs that generated it, showing true business performance

- Provides visibility into future cash needs for more reliable long-term planning

- Meets statutory reporting requirements for Companies House filings

- Gives banks and investors the financial picture they need to assess creditworthiness

Disadvantages of Accrual Accounting

- More complex to maintain than cash basis, requiring additional reconciliation work

- Demands separate cash flow tracking alongside the P&L

- Can create a disconnect between reported profit and actual cash available

For example, a software consultancy that invoices £50,000 in March but doesn't receive payment until June will show strong March profit — yet may struggle to cover April payroll if cash isn't managed separately.

When Cash Basis May Still Be Appropriate

Cash basis suits very small sole traders below the VAT threshold (currently £90,000) with simple operations and no stock. However, these entity types are explicitly excluded from using cash basis:

- Limited companies

- Limited liability partnerships (LLPs)

- Partnerships with one or more corporate partners

- Businesses that have claimed research and development allowance

- Businesses with herd basis elections or averaging claims

- Mineral extraction trades

Who Must Use Accrual Accounting in the UK?

All UK limited companies must use accrual accounting under the Companies Act 2006. Section 393 requires directors to prepare accounts that give a "true and fair view" of the company's assets, liabilities, financial position, and profit or loss. This is not optional.

FRS 102 and FRS 105

FRS 102 is the principal financial reporting standard for UK entities. Paragraph 2.36 states: "An entity shall prepare its financial statements, except for cash flow information, using the accrual basis of accounting."

FRS 105 is a simplified version for micro-entities. To qualify as a micro-entity or small company, a business must meet at least 2 of the 3 criteria for two consecutive financial years. From 6 April 2025, new thresholds apply:

| Category | Turnover | Balance Sheet Total | Avg. Employees |

|---|---|---|---|

| Micro-entity (FRS 105) | ≤ £1 million | ≤ £500,000 | ≤ 10 |

| Small company (FRS 102 Section 1A) | ≤ £15 million | ≤ £7.5 million | ≤ 50 |

| Medium-sized | ≤ £54 million | ≤ £27 million | ≤ 250 |

When Sole Traders Must Use Accrual Accounting

Sole traders excluded from the cash basis must use accrual accounting. This applies to businesses that:

- Claim R&D allowances, mineral extraction allowances, or business premises renovation allowances

- Hold significant stock as part of their trade

- Operate in certain financial activities where traditional accounting is mandatory regardless of turnover

Foreign Companies Operating in the UK

Overseas companies that open a UK establishment must register with Companies House under the Overseas Companies Regulations 2009. UK-incorporated subsidiaries of foreign companies must comply fully with the Companies Act 2006 and UK accounting standards.

For international businesses navigating these cross-border obligations, VJM Global supports UK entities and overseas companies with UK operations — providing teams experienced in UK GAAP, Companies Act compliance, and the specific challenges that arise when accounting spans multiple jurisdictions.

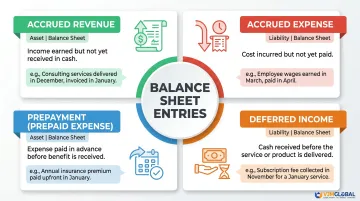

The Two Types of Accruals Explained

Accruals fall into two main categories:

1. Accrued Revenue (Accrued Income) Income earned but not yet invoiced or received. Example: A marketing agency completes a campaign worth £5,000 on 28 March but doesn't raise the invoice until 5 April. The £5,000 is recorded as accrued revenue in March to reflect the work completed in that period.

2. Accrued Expenses Costs incurred but not yet billed or paid. Example: A business uses £800 of electricity in March, but the utility bill doesn't arrive until 15 April. The £800 is recorded as an accrued expense in March to match the cost with the period in which it was consumed.

Related Concepts: Prepayments and Deferred Income

Two closely related entries work in the opposite direction to accruals:

Prepayments — expenses paid in advance for a future period. A business pays £12,000 for annual insurance in January. Rather than expensing the full £12,000 in January, £11,000 is recorded as a prepayment (current asset) and £1,000 per month is expensed across the year.

Deferred income — cash received before the service is delivered. A software company receives £6,000 upfront for a 12-month subscription. The £6,000 is recorded as deferred income (current liability) and recognised as revenue monthly at £500.

Where these entries sit on the balance sheet depends on their type — which leads to a common question.

Is an Accrual an Asset or a Liability?

It depends on the type:

- Accrued revenue (money owed to the business) = current asset on the balance sheet

- Accrued expense (money the business owes) = current liability on the balance sheet

Journal entry examples:

- Accrued expense: Debit Expense Account £2,000 / Credit Accrued Expenses (liability) £2,000

- Accrued revenue: Debit Accrued Income (asset) £3,000 / Credit Revenue Account £3,000

UK Tax Implications: Corporation Tax and VAT

Corporation Tax on an Accrual Basis

HMRC's Company Taxation Manual (CTM01105) states: "The charge to CT is made on the profits arising in a company's accounting period." This means Corporation Tax liability is determined on an accrual basis: HMRC taxes profits based on when income is earned and expenses incurred, not when cash moves.

Example: A consultancy raises a £10,000 invoice on 30 March (year-end 31 March). Payment arrives on 15 April. The £10,000 falls into the March year-end's Corporation Tax liability, even though cash arrived in the next tax period.

Knowing when that liability is due matters just as much as knowing what's included. Corporation Tax is normally due nine months and one day from the end of the accounting period. Large companies pay in quarterly instalments instead.

VAT and the Tax Point Concept

For standard VAT accounting, the tax point is usually the invoice date. VAT Guide Notice 700 defines:

- Basic tax point for goods: Date goods are sent or taken away

- Basic tax point for services: Date service is performed

- Actual tax point: If a VAT invoice is issued or payment received before the basic tax point, that earlier date becomes the tax point

- 14-day rule: If a VAT invoice is issued within 14 days after the basic tax point, the invoice date becomes the actual tax point

This means VAT becomes due on the return covering that period regardless of when the customer pays.

VAT Cash Accounting Scheme

The VAT Cash Accounting Scheme offers relief for small businesses with cash flow concerns:

- Joining threshold: VAT taxable turnover ≤ £1.35 million

- Exit threshold: Must leave if turnover exceeds £1.6 million

- Allows businesses to account for VAT based on payments received and made, not invoices issued

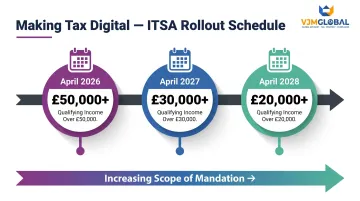

Making Tax Digital (MTD)

Businesses filing VAT returns digitally under MTD for VAT must use compatible software that supports accrual-based recording. MTD applies to all VAT-registered businesses with no turnover threshold.

The same digital discipline is extending to income tax. MTD for Income Tax Self Assessment (ITSA) rolls out in phases:

- From 6 April 2026: Qualifying income over £50,000

- From 6 April 2027: Qualifying income over £30,000

- From 6 April 2028: Qualifying income over £20,000

For sole traders and landlords in these bands, digital accrual-based record-keeping will shift from best practice to a legal requirement.

Common Accrual Accounting Mistakes to Avoid

Confusing Profit with Cash

The most dangerous mistake is assuming that a strong profit on your accrual-based P&L means you have cash to spend. A business can show £50,000 profit while having insufficient cash to meet payroll if customers haven't paid their invoices yet. Always maintain a separate cash flow forecast alongside accrual-based accounts to track actual liquidity.

Leaving Bad Debts on the Books

When a customer is unlikely to pay, the accrued revenue must be written off as a bad debt to prevent the P&L from overstating income. HMRC's Business Income Manual (BIM42701) requires that bad debt deductions be based on a separate valuation of each individual debt — a flat percentage reserve is not allowed.

The correct process:

- Review aged debtors regularly

- Assess recoverability of each debt individually

- Write off irrecoverable amounts promptly

- For VAT purposes, bad debt relief can be claimed if the debt is at least 6 months old and written off in day-to-day accounts

Incorrect Expense Timing

A common error: A business pays £12,000 for annual insurance in January and expenses the full amount in January. This overstates January's expenses and understates the remaining 11 months.

Correct treatment: Record £1,000 as January expense and £11,000 as a prepayment (current asset). Amortise £1,000 per month across the policy period. Getting this right keeps both the P&L and balance sheet accurate — and prevents HMRC queries arising from distorted profit figures across reporting periods.

Frequently Asked Questions

Does the UK use accrual accounting?

Yes. The UK uses accrual accounting as the standard method. All limited companies must follow it under UK GAAP, and it forms the basis for Corporation Tax and VAT reporting for most businesses.

What is accrual accounting in simple terms?

Accrual accounting means recording income when it is earned and expenses when they are incurred, regardless of when cash actually changes hands. This gives a more accurate view of business performance than just tracking cash transactions.

Who should not use accrual accounting?

Very small sole traders and partnerships below the HMRC cash basis eligibility threshold with simple operations may opt for cash basis instead. However, limited companies and LLPs cannot use cash basis and must use accrual accounting.

Is an accrual an asset or a liability?

It depends on the type. Accrued revenue (income earned but not yet received) is recorded as a current asset. An accrued expense (cost incurred but not yet paid) is recorded as a current liability on the balance sheet.

What are the two types of accruals?

The two types are accrued revenue (earned income not yet received or invoiced) and accrued expenses (costs incurred but not yet billed or paid). Both affect how profit is reported in a given period, independent of when cash moves.