Introduction

Singapore businesses establishing UK subsidiaries often assume their UK entity is "too small" to require a statutory audit, but that assumption ignores how UK audit exemption rules actually work. Under the Companies Act 2006, eligibility is assessed at the worldwide group level, not just the individual UK subsidiary.

That distinction matters in practice. A UK entity with modest revenues of £2 million and 15 employees may still require a full statutory audit if its Singapore parent group exceeds the size thresholds globally.

The compliance gap widens because UK audit rules for overseas-owned subsidiaries differ from those for UK-owned ones. While UK subsidiaries of UK parents can claim the parent guarantee exemption under s479A, Singapore-incorporated parents are explicitly excluded from this route.

Directors who overlook this distinction face Companies House filing penalties ranging from £150 to £1,500 (doubled for consecutive late years), plus criminal liability under s451 of the Companies Act 2006. This guide breaks down exactly which rules apply, where the common traps are, and what Singapore-based groups need to do to stay compliant.

Key Takeaways

- From 6 April 2025, UK companies qualify for audit exemption by meeting 2 of 3 thresholds: turnover ≤ £15m, assets ≤ £7.5m, or ≤ 50 employees

- Assessment is made at the worldwide group level — your Singapore parent's global operations count

- Parent guarantee exemption (s479A) requires a UK-domiciled parent — Singapore parents are ineligible for this route

- Certain entity types (public companies, banks, insurers, e-money issuers) are ineligible regardless of size

- Two consecutive years of meeting the thresholds are required — one year is not enough unless the company is in its first year of trading

UK Audit Exemption Thresholds: The Updated 2025 Rules

The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024 (SI 2024/1303) significantly raised the small company thresholds, effective for financial years beginning on or after 6 April 2025.

Pre-6 April 2025 thresholds (for financial years beginning between 1 January 2016 and 5 April 2025):

- Turnover not more than £10.2 million

- Balance sheet total not more than £5.1 million

- Number of employees not more than 50

Post-6 April 2025 thresholds (for financial years beginning on or after 6 April 2025):

- Turnover not more than £15 million

- Balance sheet total not more than £7.5 million

- Number of employees not more than 50

The "two out of three" test governs qualification: your company must satisfy at least two of the three criteria. For example, a company with £12 million turnover, 20 employees, and £6 million in assets would qualify under the new thresholds (meets two criteria: employees and assets) but would have failed under the old limits.

Applicable financial years: The new thresholds apply to financial years that begin on or after 6 April 2025. For a company with a 31 December year end, the first applicable period is the year ending 31 December 2026 (beginning 1 January 2026). For a 31 March year end, it's the year ending 31 March 2027 (beginning 1 April 2026).

How Group Size Is Measured for Overseas-Owned Companies

For companies forming part of a worldwide group, the size test applies at the group level, not the individual UK entity level. All entities under the same ultimate ownership are included — the Singapore parent, the UK subsidiary, and any other subsidiaries globally.

Under s383 of the Companies Act 2006, the group must meet two or more of these thresholds (net basis):

- Aggregate turnover not more than £15 million

- Aggregate balance sheet total not more than £7.5 million

- Aggregate number of employees not more than 50

The Companies Act 2006 doesn't prescribe a specific exchange rate methodology for the small group test. Standard practice uses the average exchange rate for the period when converting turnover figures, and the period-end rate for balance sheet totals — so Singapore businesses should apply the relevant SGD-to-GBP rate when assessing group thresholds.

A UK subsidiary with £2 million turnover and 15 employees may appear exempt in isolation. But if its Singapore parent group has combined worldwide turnover of SGD 30 million (roughly £17.5 million at mid-2024 exchange rates), the UK entity requires a statutory audit — the small entity threshold is breached at group level.

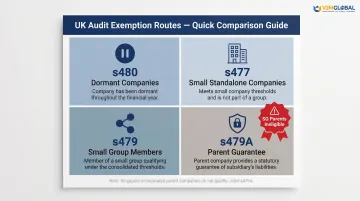

The Four Routes to Audit Exemption Under UK Law

UK law provides four exemption categories under the Companies Act 2006:

- Dormant companies (s480)

- Small standalone companies (s477)

- Small members of a small group (s479)

- Subsidiary companies with a parent guarantee (s479A)

Dormant and Small Standalone Companies

Under s1169(1), a company is dormant during any period with no "significant accounting transaction" — meaning no transaction that s386 requires to be entered in the company's accounting records. Three items are excluded from this definition:

- Shares taken by a subscriber to the memorandum

- Companies House fees for name changes or confirmation statements

- Late filing penalties

Even dormant companies must still file accounts with Companies House.

Private companies that are not part of a group and meet the small company thresholds qualify for audit exemption under s477. The balance sheet must carry a specific statutory statement above the director's signature confirming:

- Entitlement to exemption under s477

- That members have not required an audit under s476

- Directors' responsibility for maintaining adequate accounting records and preparing accounts that give a true and fair view

Small Group Members and the Parent Guarantee Route

A company that is part of a group can claim exemption under s479 if the entire group qualifies as small under the two-of-three threshold test on an aggregate basis. The group must not include any "ineligible" entities — publicly traded companies, banks, or regulated financial services firms.

A UK subsidiary of any size can be exempt from audit under s479A if:

- Its UK parent provides a formal guarantee over all outstanding liabilities

- The subsidiary is included in consolidated audited accounts filed at Companies House

- All non-controlling shareholders consent

- The parent discloses the exemption in consolidated accounts notes

- Directors deliver Form AA06 and supporting documents to the Registrar

Critical restriction: This route is only available when the parent company is established under UK law. Section 479A(1)(b) explicitly requires the parent undertaking to be "established under the law of any part of the United Kingdom."

Singapore-incorporated parents are excluded. This wording was introduced on 31 December 2020 via SI 2019/177, narrowing eligibility from EEA parents to UK-only parents post-Brexit.

Why Singapore-Owned UK Subsidiaries Face Different Rules

Because s479A requires the parent to be established under UK law, Singapore companies owning UK subsidiaries cannot use the parent guarantee route — regardless of how large, well-capitalised, or compliant the Singapore parent is. This is the single most frequent compliance error made by Singapore directors of UK entities.

The Ineligible Group Barrier

Even if a UK subsidiary qualifies as small on its own, belonging to a group that includes any of the following entities anywhere in the worldwide group renders it ineligible for exemption:

- Publicly traded companies

- Banks or authorised insurance companies

- E-money issuers

- MiFID investment firms

- UCITS management companies

- Master Trust scheme funders

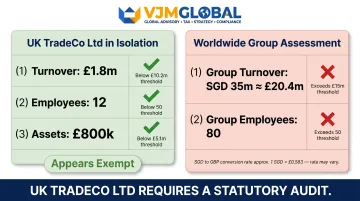

Case Study: When "Small" Isn't Small Enough

Consider SG Holdings Pte Ltd — a Singapore-based technology distributor with SGD 35 million in group revenue, 80 employees globally, and SGD 20 million in assets.

The group's UK trading subsidiary, UK TradeCo Ltd, looks straightforwardly small: £1.8 million turnover, 12 employees, £800,000 in assets. At first glance, it appears well below the small company thresholds. The worldwide group assessment tells a different story:

- Group turnover: SGD 35 million ≈ £20.4 million (approximate; exceeds £15 million threshold)

- Group employees: 80 (exceeds 50 threshold)

Because the worldwide group breaches two of the three thresholds, UK TradeCo cannot claim audit exemption under s479. The s479A route is also blocked — SG Holdings is Singapore-incorporated, not UK-established. UK TradeCo requires a full statutory audit despite appearing small in isolation.

Compliance Consequences of Getting This Wrong

Missing this distinction carries serious consequences:

- Companies House rejection of unaudited accounts

- Late filing penalties: £150 (up to 1 month late), £375 (1–3 months), £750 (3–6 months), £1,500 (over 6 months) — doubled for consecutive late years

- Director criminal liability under s451 of the Companies Act 2006 (conviction can result in fines and daily default penalties)

- Reputational damage and potential covenant breaches with lenders

When a Statutory Audit Is Still Required

Even where a Singapore business technically falls below group thresholds, a statutory audit may still be required. Lender covenants, shareholder agreements at the Singapore parent level, or the UK entity's role as a material component in the group's external audit can each independently trigger this obligation.

The "2-Year Rule" and Other Conditions Businesses Often Miss

The Two-Consecutive-Years Rule

Under s382(2) and s383(3), qualifying for audit exemption requires meeting the size conditions for the current year and the preceding year. A single qualifying year is not enough unless it is the company's first year of trading.

This guards against businesses claiming exemption after an unusually poor year. It also works in your favour: if your group exceeds the thresholds in one year after previously qualifying, you retain small company status for that year. Exceed them again the following year, and the exemption no longer applies.

Shareholder Veto (s476)

Even if your company qualifies on size grounds, shareholders holding at least 10% of shares (by number or value, in any class) can demand a statutory audit. They must submit written notice to the company's registered office at least one month before the financial year end. This applies whether shareholders are based in Singapore or elsewhere.

Articles of Association Override

If your company's articles of association require an audit, you cannot claim the exemption regardless of size. You must either amend the articles or fulfil the audit obligation.

Regulated Industry Requirements

Certain industries carry mandatory audit requirements regardless of size. These "excluded companies" under s478 of the Companies Act 2006 include:

- Banking companies

- Authorised insurance companies

- E-money issuers

- MiFID investment firms

- UCITS management companies

- Companies carrying on insurance market activity

Practical Steps: How Singapore Businesses Should Assess Their UK Audit Position

Follow this four-step assessment process annually:

1. Determine the relevant financial year and threshold set

- Identify your UK subsidiary's financial year end

- Determine whether the year begins before or after 6 April 2025

- Apply the appropriate threshold set (£10.2m/£5.1m/50 or £15m/£7.5m/50)

2. Aggregate worldwide group size

- Calculate total group turnover (convert SGD at average exchange rate for the period)

- Calculate total group balance sheet assets (convert SGD at period-end exchange rate)

- Count total group employees across all entities globally

- Apply the two-of-three test to the aggregate figures

3. Check for ineligible group status

- Review whether any entity in the worldwide group (including in Singapore) is publicly traded, regulated, or otherwise ineligible

- If yes, the UK subsidiary cannot claim exemption regardless of size

4. Confirm parent domicile before considering s479A

- If your parent is Singapore-incorporated, do not attempt to claim s479A exemption

- Your only exemption path is the small group route (s479), and only if worldwide thresholds are met

Run this assessment every year, not just once. Group size and structure shift, and the 2025 threshold changes mean some businesses previously above the limit may now qualify for exemption — while others may have grown past it.

Getting these steps wrong carries real cost — missed exemptions mean unnecessary audit fees; misclaimed exemptions risk Companies House penalties. VJM Global has worked with 250+ UK businesses and provides compliance support for foreign-owned UK entities, with access to UK-specialist resources through its EAI International membership.

Frequently Asked Questions

Who is eligible for audit exemption in the UK?

UK private limited companies qualify if they meet at least two of three size thresholds (turnover, assets, employees), operate outside ineligible sectors, and are not part of an oversized group. Dormant companies and qualifying subsidiaries with UK parent guarantees have their own separate exemption routes.

What are the audit exemption thresholds in the UK?

For financial years beginning before 6 April 2025: turnover ≤ £10.2 million, assets ≤ £5.1 million, ≤ 50 employees. For financial years beginning on or after 6 April 2025: turnover ≤ £15 million, assets ≤ £7.5 million, ≤ 50 employees. A company must meet at least two of the three criteria.

Is audit mandatory for small companies in the UK?

Audit is not automatically mandatory for small companies. Those qualifying as small under the Companies Act 2006 may be exempt. However, small companies forming part of a larger worldwide group, or operating in regulated sectors (banking, insurance, e-money, MiFID), may still require a statutory audit.

What is the 2-year rule for audit exemption in the UK?

To claim audit exemption as a small company or small group, the relevant size conditions must be met for both the current and the preceding financial year. An exception applies for companies in their first year of trading.

What is the small group audit exemption in the UK?

Under s479 of the Companies Act 2006, a group member can claim audit exemption if the entire worldwide group qualifies as small under the two-of-three threshold test. The group must also exclude ineligible entities — such as publicly traded companies or regulated financial institutions.

Can a small UK subsidiary of an overseas parent qualify for audit exemption?

A UK subsidiary of an overseas parent — including a Singapore parent — can qualify for size-based exemption only if the worldwide group stays within the size thresholds. The s479A parent guarantee route is not available here; it is reserved for subsidiaries with a UK-domiciled parent.