Introduction

Singapore companies are increasingly eyeing the UAE as a strategic expansion destination. The bilateral trade relationship between Singapore and the UAE reached S$27.94 billion in 2025, driven by the UAE's role as a gateway to the GCC and Africa markets.

Zero corporate tax in UAE free zones — combined with rising opportunities across trade, fintech, and professional services — has pushed many Singapore-registered companies to establish UAE entities, particularly in free zones like DMCC and DIFC.

While setting up a UAE entity is manageable, opening a business bank account often becomes the first major operational hurdle. UAE banks apply stricter Know Your Customer (KYC) requirements on fully foreign-owned entities, requiring Singapore-specific documentation including ACRA extracts, notarized company documents, and Ultimate Beneficial Owner (UBO) declarations.

Knowing which banks are most receptive — and what they need from Singapore applicants — can be the difference between a 2-week approval and a 3-month delay.

Key Takeaways

- UAE banks scrutinize foreign-owned entities closely, requiring Singapore-specific documents like ACRA BizFile+, legalised MOA/AOA, and UBO declarations

- Five banks stand out for Singapore companies: Emirates NBD, HSBC UAE, Mashreq Bank, RAKBANK, and fully digital Wio Business

- Non-resident shareholder acceptance, multi-currency support, and minimum balance thresholds vary widely — these differences determine which bank fits your structure

- Free zone companies (DMCC, DIFC) typically face smoother account approval than mainland LLCs

- Proper corporate structure and documentation preparation improve approval chances

Why Singapore Companies Are Looking to the UAE

The Singapore-UAE business corridor has grown considerably in recent years. The two countries signed a Comprehensive Partnership in 2019, and at the Third Singapore-UAE Joint Committee meeting in June 2023, the UAE expressed interest in pursuing a bilateral Comprehensive Economic Partnership Agreement (CEPA) with Singapore.

Singapore companies are particularly active in five key sectors within the UAE:

- Food manufacturing and services

- Logistics and distribution

- Information and communications technology

- Tourism and hospitality

- Energy and water (renewable technologies)

DMCC, one of the UAE's largest free zones, has surpassed 25,000 registered companies and contributes 15% of Dubai's FDI. Singapore is listed among DMCC's key international outreach markets.

Free Zone vs. Mainland: The Structural Choice That Affects Banking

Singapore companies typically enter the UAE through two structures. Each carries distinct ownership rules, trading permissions, and — critically — different levels of scrutiny from UAE banks.

| Factor | Free Zone (FZE/FZCO) | Mainland LLC |

|---|---|---|

| Foreign Ownership | 100% — no local partner needed | 100% permitted in most sectors (post-2020) |

| Tax Status | Exempt | Subject to UAE corporate tax |

| Domestic Trading | Restricted (via agent/distributor) | Direct access to UAE market |

| Bank Approval | More predictable — standardised docs | Additional scrutiny; some banks flag foreign-owned structures |

| Popular Options | DMCC, DIFC, IFZA | DED-registered entities |

Your choice of structure directly shapes which banks will accept your application, what documents they require, and how long approval takes. UAE banks vary considerably in how they handle Singapore-headquartered companies with non-resident directors — making bank selection as important as entity selection.

Best Banks in the UAE for Singapore Company Business Accounts

The following banks were evaluated for their compatibility with foreign-owned Singapore companies. Each was assessed across five criteria:

- Acceptance of non-resident directors and shareholders

- Capacity to handle international transactions

- Minimum balance accessibility

- Digital banking quality

- Track record with free zone entities

The right choice depends on your company size, transaction volume, and how much physical UAE presence your team has.

Emirates NBD

Emirates NBD is the UAE's largest bank by assets, offering dedicated SME and corporate banking divisions with strong trade finance capabilities. For Singapore companies engaged in goods trade, distribution, or regional operations, Emirates NBD provides a solid anchor banking relationship.

Key advantages for Singapore businesses:

- Accepts fully foreign-owned free zone and mainland entities

- Dedicated relationship manager model for international businesses

- Multi-currency account support including USD, EUR, and GBP

- Full trade finance suite including letters of credit and bank guarantees

- However, requires at least one UAE-resident signatory for online applications

| Feature | Details |

|---|---|

| Minimum Balance | AED 0 (Connect package, AED 249/month fee) to AED 3.5 million (Platinum); Prime package requires AED 50,000 |

| Multi-Currency Support | USD, EUR, GBP supported; SGD transfers via SWIFT (dedicated SGD accounts not confirmed) |

| Account Opening Timeline | 10-15 business days for standard applications; complex structures may take 4-8 weeks |

| Best Suited For | Singapore trading companies, regional holding entities, businesses requiring trade finance and letters of credit |

Note: The UAE-resident signatory requirement may be a barrier for Singapore companies with no local directors.

HSBC UAE

HSBC UAE offers the most internationally familiar banking experience for Singapore businesses, given HSBC's strong commercial presence in Singapore. HSBC's "one bank" global relationship model is a real advantage here. Directors who already bank with HSBC Singapore can benefit from smoother cross-border KYC and expedited account referrals.

What works in its favor:

- International business account infrastructure designed for foreign-headquartered entities

- Global network across 60+ countries facilitates international payments

- Multi-currency accounts with broad currency support

- Potential for faster KYC for existing HSBC global clients (verify directly with bank)

| Feature | Details |

|---|---|

| Minimum Balance | Reportedly AED 100,000 (Advance Business) to AED 350,000 (Premier Business); Flexi Business has no minimum requirement |

| Key Advantage | Existing HSBC Singapore banking relationship may accelerate UAE KYC and account opening |

| Account Opening Timeline | Flexi: instant online opening; standard business accounts: potentially 8-12 weeks due to global compliance checks |

| Best Suited For | Singapore companies with existing HSBC relationships, businesses with high international payment volumes, firms needing trade finance |

Important: Minimum balance figures could not be verified on HSBC UAE's official website. Confirm current requirements directly with the bank.

Mashreq Bank

Mashreq is one of the UAE's most digitally advanced banks, offering both traditional business accounts and a digital-first SME product called NeoBiz. It's widely used by startups and SMEs across various nationalities and has a relatively flexible approach to free zone entity account opening.

Strengths for Singapore companies:

- Lower minimum balance requirements make it accessible to SMEs and startups

- Faster account approval timelines (typically 2-5 business days)

- Digital platform integrates with accounting software

- Well-suited for Singapore companies managing UAE accounts remotely

| Feature | Details |

|---|---|

| Minimum Balance | Zero (NeoBiz Pro: AED 99/month; NeoBiz Pro Plus: AED 199/month); Express Prime: AED 50,000 with fee waiver |

| Digital Banking Quality | 24/7 mobile banking, API integration with accounting platforms, WPS payroll, bulk payments |

| Multi-Currency Support | EUR, CAD, USD, GBP, AUD, NZD, JPY, SAR (SGD not listed) |

| Best Suited For | Singapore SMEs, tech startups, consulting firms needing fast setup and strong digital tools |

RAKBANK

RAKBANK focuses on SME banking with lower barriers to entry and faster onboarding compared to larger banks. It's a cost-effective entry point for Singapore companies establishing initial UAE operations, particularly those with a free zone license and limited early transaction volumes.

Where RAKBANK delivers value:

- Among the lowest minimum balance requirements in the traditional banking segment

- Simplified document checklist with clear requirements for foreign-owned companies

- Suitable for Singapore companies in their UAE entry phase

| Feature | Details |

|---|---|

| Minimum Balance | AED 25,000 (Business Current Account); RAKstarter: Zero balance for first year |

| Currencies | AED, USD, EUR, GBP, CHF, JPY (SGD not listed) |

| Account Opening Timeline | 5-7 business days |

| Best Suited For | Singapore startups and small businesses in UAE free zones needing cost-effective entry-level accounts |

Wio Business

For Singapore companies that want the fastest possible setup with no capital tied up in minimum balances, Wio Business is worth serious consideration. It's a UAE-licensed digital bank backed by ADQ (Abu Dhabi sovereign wealth entity) and First Abu Dhabi Bank, offering fully app-based account opening with zero minimum balance.

Why it appeals to Singapore-based founders:

- Zero minimum balance eliminates capital tie-up requirements

- Significantly shorter approval timelines (48 hours to 5 business days)

- 100% online/mobile account opening with video KYC

- Spending analytics and multi-currency capabilities

- Integrated invoicing and payment links

Important limitations:

- No trade finance or letters of credit

- No physical chequebooks (significant for UAE rent payments)

- Limited credit facilities

- No physical branches (all support via digital channels)

| Feature | Details |

|---|---|

| Minimum Balance | Zero |

| Account Opening Speed | 48 hours to 5 business days |

| Currencies | Dedicated IBANs for AED, USD, EUR, GBP (SGD not supported) |

| Best Suited For | Singapore-based digital businesses, freelancers, tech companies needing fast setup with no upfront capital |

Wio Business is best suited as either a primary account for service-based businesses or as a secondary account alongside a traditional bank for trade-focused companies.

What Singapore Companies Should Look for in a UAE Business Bank

Acceptance of Non-Resident Foreign Ownership

The most common mistake Singapore companies make is choosing a UAE bank based on brand recognition alone. Some major UAE banks have informal policies that make onboarding fully foreign-owned entities with non-UAE-resident shareholders slow or likely to fail.

Before applying, confirm:

- Does the bank accept companies with 100% foreign shareholders?

- Can all directors be non-UAE residents, or is a UAE-resident signatory required?

- Does the bank have experience with your specific free zone (DMCC, DIFC, etc.)?

Multi-Currency and SGD/AED Corridor Support

Singapore companies repatriating profits, paying Singapore-based staff, or invoicing Singapore parent companies need efficient cross-border transfers.

Key considerations:

- No UAE bank examined explicitly lists SGD as a supported business account currency — multi-currency accounts typically cover AED, USD, EUR, and GBP

- Look for competitive AED-SGD exchange rates via SWIFT, transparent international transfer fees, and foreign exchange solutions

- HSBC's global network can simplify Singapore-to-UAE transfers through linked accounts — confirm current SGD corridor terms with the branch directly

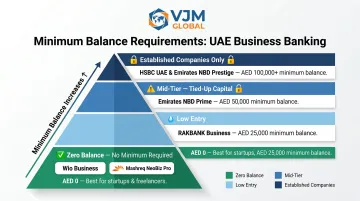

Minimum Balance Requirements

Unlike established UAE businesses, Singapore companies entering the UAE often have limited initial AED liquidity.

Calculate the true cost:

- Minimum balance requirement (capital tied up)

- Monthly account fees

- Penalties if balance falls below minimum

- Free zone vs. mainland: some banks apply different requirements

Options by budget:

- Zero balance: Wio Business, Mashreq NeoBiz Pro (with monthly fees)

- Low entry: RAKBANK (AED 25,000)

- Mid-tier: Emirates NBD Prime (AED 50,000)

- Established companies: HSBC UAE, Emirates NBD Prestige (AED 100,000+)

Digital Banking Quality for Remote Management

Singapore company directors who are not UAE residents need robust online and mobile banking to manage their UAE account from Singapore.

Essential digital features:

- Real-time transaction notifications

- Remote document upload for compliance

- Bulk payment capabilities

- Accounting software integrations (Xero, QuickBooks, Naqood)

- Multi-user access with permission controls

- Mobile app functionality for approvals

Among the banks reviewed, Wio Business and Mashreq NeoBiz lead on digital capability — both are built for remote account management from day one.

Ongoing Compliance Expectations

UAE banks require ongoing compliance beyond initial account opening:

- Periodic KYC refresh (typically annually)

- Proof of business activity and transaction justification

- Updated company documents when changes occur

- Minimum transaction thresholds to avoid dormancy fees

Accounts can be frozen due to inactivity or insufficient documentation during KYC reviews. Confirm the bank's ongoing compliance expectations before opening to ensure your Singapore-based team can realistically meet them.

How to Open a UAE Business Bank Account as a Singapore Company

Prerequisite: UAE Entity Registration

A UAE business account can only be opened by a legally registered UAE entity—free zone company, mainland LLC, or branch. Singapore companies cannot open a UAE business account under their Singapore registration alone.

Before approaching any bank, you must:

- Establish a UAE subsidiary or branch

- Obtain a UAE trade license

- Have a registered UAE address (physical office or virtual office agreement)

Documentation Requirements

UAE Entity Documents:

- Valid UAE trade license or certificate of incorporation

- Memorandum and Articles of Association (MOA/AOA) issued by UAE authority

- Tenancy contract or virtual office agreement

Singapore Parent/Shareholder Documents:

- ACRA BizFile+ company profile

- Singapore company's MOA/AOA (legalised—see below)

- Board resolution authorizing UAE account opening

- Passport copies of all Ultimate Beneficial Owners (UBOs)

- Proof of address for all directors and shareholders

- 6 months' bank statements (company or personal if new entity)

For corporate shareholders (Singapore company owns UAE entity):

- Additional corporate structure charts

- Singapore company's audited financials

- Directors' resolutions from Singapore parent company

Singapore Document Legalisation Process

The UAE uses a legalisation/attestation process (not apostille) for foreign documents.

Required steps:

Singapore Academy of Law (SAL) legalisation: Submit documents to SAL at legalisation.sal.sg. Computer-generated documents like ACRA Business Profiles must first be certified by the issuing department. Fee: S$10.70 per document (including GST).

UAE Embassy/Consulate attestation: After SAL processing, submit to:

- UAE Embassy in Singapore, OR

- Consulate-General of Singapore in Dubai (+971 4 321 9498)

- Embassy of Singapore in Abu Dhabi (+971 2 222 2083)

Both steps are mandatory — UAE banks will reject documents with only SAL legalisation or an apostille stamp.

Account Opening Process

Typical timeline:

- Document submission to bank's corporate banking team

- Compliance/KYC review (1-8 weeks depending on bank and entity complexity)

- Interview with relationship manager (in-person or video)

- Approval and account activation

In-person attendance varies by bank, so confirm this before you begin:

- Most traditional UAE banks require at least one director or authorized signatory to appear at a UAE branch

- Digital-first banks (Wio Business, Mashreq NeoBiz) offer remote or video-based KYC as an alternative

- Confirm in-person requirements directly with your chosen bank before applying

Professional Support

Getting the documentation and entity structure right before you approach a bank significantly lowers the risk of KYC rejection. VJM Global supports Singapore companies through this process by:

- Preparing a complete, legalised documentation package

- Advising on UAE entity structure to meet bank compliance expectations

- Providing ongoing accounting and regulatory support post-account opening

- Flagging common rejection triggers before you submit your application

Conclusion

Choosing the right UAE bank for your Singapore company comes down to three practical factors: whether the bank accommodates non-resident foreign shareholders, whether it supports AED transfers back to Singapore, and whether its compliance expectations are realistic for a remotely managed entity.

Align your bank selection with your specific setup rather than defaulting to the most-advertised option:

- Entity type: Free zone entities and mainland companies face different account opening requirements

- Business model: Trade, services, and digital businesses carry different transaction profiles banks scrutinize

- Remote management: A bank suited to a UAE-resident SME may not fit a Singapore-headquartered company managing operations from abroad

Before finalizing your UAE banking decision, consult with a business setup and compliance advisor like VJM Global. Having your entity structure, shareholder documentation, and compliance obligations properly prepared significantly improves your chances of account approval — and keeps the account in good standing long-term.

Contact VJM Global at info@vjmglobal.com or +91 98915 76441 to discuss your UAE entity setup and banking preparation needs.

Frequently Asked Questions

Which is the best bank for business in the UAE?

The best bank depends on company size and nationality. For international and foreign-owned companies, Emirates NBD and HSBC UAE are commonly recommended for their international business infrastructure. Wio Business and Mashreq offer faster onboarding for SMEs with lower balance requirements.

Which bank is best for a small business account in the UAE?

RAKBANK and Mashreq NeoBiz are among the most accessible for small businesses, with lower minimum balance requirements (AED 25,000 and zero respectively) and faster approval timelines compared to larger banks.

Which bank is best for a business account in Dubai?

Dubai-based businesses, especially in free zones like DMCC or DIFC, commonly use Emirates NBD, Mashreq, and HSBC UAE. Digital options like Wio Business are gaining traction for companies wanting fast, low-cost setup.

Which are the top 5 banks in the UAE?

By assets, the top 5 UAE banks are First Abu Dhabi Bank (FAB), Emirates NBD, Abu Dhabi Commercial Bank (ADCB), Dubai Islamic Bank (DIB), and Mashreq Bank, per S&P Global Market Intelligence 2025 data.

Can a Singapore company open a UAE business bank account remotely?

Most traditional UAE banks require at least one in-person visit for corporate account opening. Digital banks like Wio Business offer remote and video KYC options, and some traditional banks accept video interviews with relationship managers as an alternative.

What documents does a Singapore company need to open a UAE business bank account?

Documents fall into two categories:

- UAE entity documents: trade license, Memorandum of Association, tenancy contract

- Singapore parent/shareholder documents: ACRA BizFile+ extract, legalised company documents, UBO declarations, passport copies of all directors and beneficial owners

Note: legalisation via SAL and UAE embassy attestation is required — apostille is not accepted.