Introduction

Many Singapore businesses incurring VAT on UK goods and services don't realise they're sitting on recoverable costs. Whether you've attended trade shows at ExCeL London, engaged UK law firms, or paid for business accommodation and professional services, you've likely been charged VAT at the UK's 20% standard rate. HMRC allows you to reclaim that tax without registering for UK VAT.

This guide is for Singapore-registered, GST-compliant businesses that spend money in the UK but have no UK establishment. Unlike UK-registered companies that recover VAT through quarterly returns, Singapore businesses use HMRC's overseas business refund route, a separate scheme with its own rules, deadlines, and documentation requirements.

What we'll cover:

- How the overseas VAT reclaim process works under HMRC Notice 723A

- Who qualifies for the scheme

- Which expenses are eligible for recovery

- The exact steps to file using Form VAT65A

- Critical mistakes that cause claims to be rejected

Key Takeaways

- Singapore businesses reclaim UK VAT using HMRC Form VAT65A—no UK VAT registration required

- The claim period runs 1 July to 30 June; the filing deadline is 31 December of the following year

- Qualifying expenses include accommodation, conferences, professional services, and goods imported for business use

- Client entertainment and goods for personal use are permanently blocked

- To qualify: no UK establishment, no UK VAT registration, and HMRC's reciprocity condition must be met

What Is UK VAT Reclaim for Overseas Businesses?

Value Added Tax (VAT) is a consumption tax charged on most goods and services sold in the UK. The standard rate is 20%, applicable to hotel accommodation, professional fees, conference tickets, and business equipment. Many Singapore businesses pay this tax on UK purchases without realising it's recoverable.

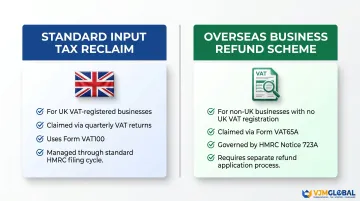

There are two distinct routes to reclaim UK VAT:

| Route | For Whom | Process |

|---|---|---|

| Standard input tax reclaim | UK VAT-registered businesses | Claim via quarterly VAT returns (Form VAT100) |

| Overseas business refund scheme | Non-UK businesses with no UK registration | Claim via Form VAT65A under HMRC Notice 723A |

Singapore businesses follow the overseas refund route because they are not VAT-registered in the UK. This route exists specifically for foreign businesses that incur UK VAT but have no UK tax registration or fixed establishment. It is governed by the Value Added Tax Act 1994 section 39 and the Value Added Tax Regulations 1995 Parts 20A and XXI.

Unlike UK-registered businesses, which recover VAT through quarterly returns, Singapore businesses must submit standalone annual claims supported by invoices and proof of foreign tax registration.

Are Singapore Businesses Eligible to Reclaim UK VAT?

Core Eligibility Conditions

Per HMRC Notice 723A, your Singapore business qualifies if it meets all of these conditions:

- Registered for GST in Singapore for business purposes with IRAS

- Not registered, liable to register, or eligible to register for UK VAT

- No fixed establishment or place of business in the UK

- Makes no taxable supplies within the UK during the claim period — narrow exceptions apply for international transport services or supplies where the UK recipient accounts for the VAT

Reciprocity Requirement

HMRC only grants reclaim rights to businesses from countries that offer "similar concessions" to UK traders. Singapore operates a GST regime with a Tourist Refund Scheme and does not restrict UK businesses from accessing GST recovery mechanisms.

Important: HMRC does not publish a formal country eligibility list. Per professional tax compliance sources, HMRC will only refuse a claim if a country operates a refund scheme but actively blocks UK traders from using it. Confirm eligibility with HMRC or a qualified tax adviser before proceeding.

Minimum Claim Thresholds

| Claim Period | Minimum VAT Amount |

|---|---|

| Interim claim (minimum 3 calendar months, less than full year) | £130 |

| Full prescribed year or remainder of year | £16 |

Claim Period and Deadline

The prescribed claim year runs from 1 July to 30 June (not the calendar year). Claims must be submitted by 31 December following the end of the prescribed year. This deadline is strictly enforced. Missing it forfeits your entire claim for that period.

Example: VAT incurred between 1 July 2024 and 30 June 2025 must be claimed by 31 December 2025.

Retrospective Claims

HMRC Notice 723A permits items "missed on earlier applications" to be included, provided they relate to VAT charged in the same prescribed year. The notice does not explicitly permit claims spanning prior prescribed years once the annual deadline has passed.

- Missed a prior year? Consult HMRC or a specialist adviser before assuming a late claim is possible.

What UK Expenses Can Singapore Businesses Claim VAT On?

Qualifying Expense Categories

Singapore businesses commonly incur reclaimable UK VAT on:

- Business accommodation during UK trips

- Conference and exhibition fees (such as trade fairs at the NEC Birmingham or ExCeL London)

- Professional advisory fees from UK law firms, consultancies, or accounting practices

- Goods imported into the UK for business purposes

- Business equipment purchased and used in the UK

- Taxi fares with full VAT receipts (taxis are standard-rated at 20%)

Permanently Blocked Expenses

The following expenses are non-reclaimable under UK law:

Client and supplier entertainment

This is an absolute statutory block under Article 5 of the Value Added Tax (Input Tax) Order 1992 (SI 1992/3222). Entertainment includes:

- Meals, drinks, and hospitality for clients or suppliers

- Event tickets (theatre, concerts, sporting events)

- Use of hospitality assets (yachts, aircraft)

Exception: VAT may be recovered on entertainment provided to an overseas customer, provided it is "of a very basic nature" and reasonable in scale.

Other blocked items:

- Goods and services used for non-business purposes

- Most ordinary business cars (purchase or import)

- Certain second-hand goods under margin schemes

- Goods or services purchased for resale for the direct benefit of travellers (for example, hotel accommodation bought for resale)

Zero-Rated and Exempt Supplies (No VAT Charged)

You cannot reclaim VAT where none was charged. Common examples:

| Item | VAT Status |

|---|---|

| Public transport (rail, bus) with 10+ passenger capacity | Zero-rated (0%) |

| Scheduled domestic flights | Zero-rated (0%) |

| Insurance premiums | Exempt |

| Royal Mail postal services | Exempt |

Taxis and hire cars with fewer than 10 seats are standard-rated at 20% and are reclaimable.

Mixed-Use Apportionment

If a purchase covers both business and personal use (for example, a mobile phone plan), you can only reclaim the business proportion of VAT. HMRC requires you to:

- Document how the split was calculated (for example, usage logs or time records)

- Keep supporting evidence

- Apply the 50% VAT cap on car hire or lease vehicles used for mixed business and private purposes

Singapore-Specific Use Cases

Singapore businesses typically generate recoverable UK VAT through:

- Trade fairs and exhibitions at UK venues

- Professional service engagements with UK consultancies or legal advisers

- Goods temporarily held in the UK before onward shipment

- Employee travel costs during UK client visits (accommodation, taxis, meals away from a fixed work location)

At a standard rate of 20%, a Singapore company spending £50,000 annually on qualifying UK expenses could recover up to £10,000 — worth tracking and claiming systematically.

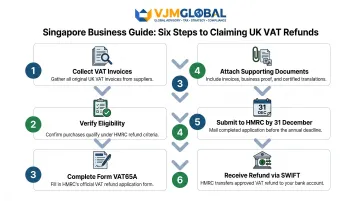

How to Claim UK VAT Back: Step-by-Step Process for Singapore Businesses

The process follows six stages: collect eligible VAT invoices, verify eligibility, complete Form VAT65A, attach supporting documents, submit to HMRC by 31 December, then await the refund decision.

Step 1: Collect and Organise VAT Invoices

For supplies over £250 (VAT-inclusive):

Your invoice must show:

- Supplier's VAT registration number

- Business name and address of buyer (your Singapore company, not an individual employee)

- Unique invoice number

- Description of goods or services

- VAT amount

- Date of supply

For supplies under £250 (VAT-inclusive):

A simplified invoice is acceptable, showing:

- Supplier's name, address, and VAT number

- Description of goods or services

- Total cost including VAT

Not acceptable: Pro forma invoices, purchase orders, delivery notes, credit card statements.

Step 2: Complete HMRC Form VAT65A

Download Form VAT65A (Application for refund of VAT by a business person not established in the UK).

The form requires:

- Business name, address, and GST registration number in Singapore

- Description of business activities

- Total VAT amount being claimed

- Details of the claim period (1 July to 30 June)

- Signature of an authorised representative

HMRC requests that the form be completed electronically and that the schedule at question 9 be typed (not handwritten).

Step 3: Prepare Supporting Documentation

Submit with your VAT65A:

- Original VAT invoices (or certified copies if originals unavailable)

- Certificate of GST registration from IRAS or equivalent official proof of business status in Singapore

- Import documents (if claiming on goods imported into the UK)

- Additional evidence of business purpose (if requested by HMRC)

All documents should be in English or accompanied by certified translations.

Step 4: Submit the Claim to HMRC Before the Deadline

Send your completed claim by post to:

HM Revenue and Customs VAT Overseas Repayment Unit S1250 Benton Park View Newcastle upon Tyne NE98 1YX United Kingdom

Key submission notes:

- Deadline: 31 December following the end of the prescribed year — strictly enforced, no exceptions

- If HMRC requests additional information: They will notify you with a specific response deadline. Missing that deadline typically results in rejection.

Working with a cross-border tax adviser experienced in HMRC compliance can help Singapore businesses prepare documentation that meets HMRC standards. Invoice formatting errors, apportionment mistakes, and missing certificates are among the most common reasons claims are rejected or delayed. VJM Global works with Singapore businesses on exactly these cross-border compliance requirements, helping ensure claims are complete before submission.

Step 5: Receive the Refund

Once HMRC accepts your application, the waiting period begins. HMRC commits to processing refunds within 6 months of receiving a satisfactory claim.

Payment: Refunds are issued in pound sterling (£) via SWIFT bank transfer to your nominated account.

If HMRC rejects or partially disallows your claim:

- You may request a review by a different HMRC officer

- You have 30 days to appeal to an independent tribunal

Common Mistakes and Misconceptions About UK VAT Reclaim

Misconception: VAT Retail Export Scheme Still Operates

The UK's VAT Retail Export Scheme (tax-free shopping for visitors) was abolished on 31 December 2020. Singapore travellers and businesses can no longer claim VAT refunds at UK airports on goods taken out of the country. Any service claiming to offer airport VAT refunds for UK purchases post-2020 is not operating within HMRC's current rules. The overseas business refund scheme (Form VAT65A) remains fully operational and is the correct route for Singapore businesses.

Documentation and Process Errors

The most common causes of rejected or reduced claims:

Invoice errors:

- Submitting simplified invoices for purchases over £250

- Invoices addressed to an individual employee instead of the registered business entity

- Missing VAT registration numbers or invoice dates

Blocked expense claims:

- Claiming VAT on client entertainment (an absolute statutory block)

- Attempting to reclaim VAT on zero-rated or exempt supplies (rail tickets, insurance, flights)

Deadline failures:

- Missing the 31 December submission deadline (no extensions are granted)

Apportionment errors:

- Failing to document how mixed-use expenses were split between business and personal

Mixing Up the Two Claim Routes

Singapore businesses that assume they must register for UK VAT to reclaim incurred VAT risk triggering unnecessary UK tax obligations. Once voluntarily registered for UK VAT, you must:

- Submit a VAT return for every tax period, even if you have no VAT to pay or reclaim

- Account for VAT on all taxable supplies from the registration date

- Use Making Tax Digital (MTD) compatible software

- Maintain UK VAT records

These obligations don't disappear — HMRC Notice 700/1 confirms that once you voluntarily register, the registration date "cannot be changed later" and "does not carry a right of appeal."

The overseas business VAT refund scheme exists precisely so non-established businesses avoid this. If you only have UK expenses to reclaim — not UK taxable supplies to report — use Form VAT65A and keep your compliance obligations to a minimum.

Frequently Asked Questions

How do I claim back VAT in the UK?

Singapore businesses claim UK VAT using HMRC Form VAT65A, submitted with original VAT invoices and proof of GST registration from IRAS. The claim covers the prescribed year (1 July to 30 June) and must be filed by 31 December of the following year.

Can overseas businesses reclaim VAT in the UK?

Yes. Non-UK businesses, including Singapore-registered companies, can reclaim UK VAT under HMRC's overseas business refund scheme, provided they have no UK establishment, are not UK VAT-registered, and satisfy reciprocity conditions under Notice 723A.

What can you claim VAT on in the UK?

Singapore businesses commonly reclaim VAT on accommodation, business travel (taxis, meals during trips), conference and exhibition fees, professional services (legal, accounting, consulting), and goods imported for business use. Client entertainment is specifically excluded and cannot be reclaimed under any circumstances.

Can tourists still claim VAT back in the UK?

No. The UK's VAT Retail Export Scheme (tax-free shopping for visitors) was abolished on 31 December 2020. Tourists can no longer claim VAT refunds on goods purchased in the UK and taken home.

Is it worth claiming a VAT refund?

With UK standard VAT at 20%, even moderate spending generates meaningful refunds. A Singapore business spending £10,000 on UK conferences and professional services could recover £1,667 in VAT — making a formal claim well worth the administrative effort.

Can I claim VAT back at Heathrow?

No. Since the abolition of the VAT Retail Export Scheme in 2021, VAT refund desks at UK airports — including Heathrow — no longer process claims for goods purchased in the UK.

Need help preparing your UK VAT claim? VJM Global specialises in cross-border tax compliance and can assist Singapore businesses with invoice review, Form VAT65A preparation, and HMRC liaison to ensure your claim meets documentation standards and maximises recovery. Get in touch at info@vjmglobal.com or call us at +91 98915 76441.