Introduction

Singapore businesses regularly incur UAE VAT on hotels, venues, and services during business visits — then spend months preparing refund claims that get rejected at the first eligibility check. The reason: Singapore is not currently on the UAE's approved list of countries with reciprocal VAT arrangements, which makes most Singapore-incorporated companies ineligible for the scheme no matter how much VAT they've paid in the UAE.

This guide is written specifically for Singapore-based companies operating in or visiting the UAE. Understanding the reciprocal arrangement requirement before investing time in a refund claim can save months of effort and prevent costly documentation mistakes.

We'll cover how the scheme works, whether your Singapore business qualifies, the exact steps if you do, and practical alternatives for recovering UAE VAT.

Key Takeaways

- Singapore is not on the UAE's approved reciprocal country list — most Singapore businesses cannot access the Business Visitors Refund Scheme

- Eligible foreign businesses from qualifying countries can reclaim UAE VAT by applying to the Federal Tax Authority (FTA) between 1 March and 31 August annually

- Minimum refund threshold is AED 2,000 per 12-month period

- Applications require attested tax compliance certificates, valid tax invoices with supplier TRNs, and payment proof for each claimed expense

- Singapore companies with UAE branches, subsidiaries, or local VAT registrations follow standard refund processes instead

- Cross-border eligibility and attestation requirements are complex — professional guidance from VJM Global can help navigate them

What Is the UAE Business Visitors VAT Refund Scheme?

The UAE Business Visitors VAT Refund Scheme lets foreign businesses reclaim VAT on UAE business expenses — without registering for UAE VAT or establishing a local entity. It operates under Article 67 of Cabinet Decision No. 52 of 2017, part of the Executive Regulations of Federal Decree-Law No. 8 of 2017 on Value Added Tax.

What the scheme achieves:

- Prevents double taxation on cross-border business activities

- Encourages international business engagement with the UAE

- Provides a recovery path for input VAT without UAE VAT registration

- Reduces the cost burden on foreign businesses operating temporarily in the UAE

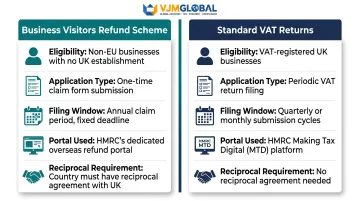

How It Differs from Standard VAT Returns

This scheme is separate from the standard VAT return process used by UAE-registered taxable persons. The key distinctions are:

| Business Visitors Refund Scheme | Standard VAT Returns |

|---|---|

| For non-resident, non-registered foreign businesses | For UAE VAT-registered entities |

| Standalone refund application | Periodic VAT201 form submissions |

| Annual filing window (1 March - 31 August) | Monthly or quarterly returns |

| Filed via FTA e-Services portal | Filed via EmaraTax portal |

| Requires reciprocal arrangement (non-GCC countries) | No reciprocal requirement |

It's also worth distinguishing this scheme from the UAE Tourist VAT Refund Scheme — the retail system run by Planet and Global Blue — which covers individual tourists buying goods for personal use, not business visitors.

Does Singapore Qualify? Understanding the Reciprocal Arrangement Requirement

The Reciprocity Gate

Article 67(3)(c) of Cabinet Decision No. 52 of 2017 establishes a critical eligibility condition: a foreign entity cannot claim under the scheme if the country does not provide similar VAT refunds to UAE entities in comparable circumstances. The UAE Ministry of Finance maintains an approved list of countries with confirmed reciprocal arrangements.

As of the most recent publicly available list (April 2021), Singapore is not included.

Approved Reciprocal Countries (25 Jurisdictions)

The UAE currently recognizes reciprocal arrangements with:

European Countries (14): Austria, Belgium, Denmark, Finland, France, Germany, Iceland, Isle of Man, Luxembourg, Netherlands, Norway, Sweden, Switzerland, United Kingdom

GCC Member States (5): Bahrain, Kuwait, Oman, Qatar, Saudi Arabia (exempt from reciprocal requirement under Article 67(10))

Other Jurisdictions (6): Korea (South), Lebanon (certain circumstances), Namibia (exported goods only), New Zealand, South Africa (goods exported within 90 days), Zimbabwe

Source: FTA Refund Guide for Business Visitors, April 2021

Practical Consequence for Singapore Businesses

A Singapore-incorporated company with no UAE establishment and no UAE VAT registration cannot file a Business Visitors Refund application. Any such application will be rejected at the eligibility assessment stage — before reviewers even examine your documents.

Alternative Route: UAE-Registered Entity

Singapore businesses can access UAE VAT recovery through a different mechanism: establishing a UAE-registered entity. If your Singapore company sets up:

- A UAE branch office

- A subsidiary incorporated in the UAE

- A free zone entity registered for VAT with the FTA

Then VAT incurred through that UAE entity becomes recoverable through the standard UAE VAT return process (Form VAT201) via the EmaraTax portal. This route has no reciprocal country requirement and follows the regular input tax credit rules applicable to all UAE taxable persons.

The CEPA Context

No Comprehensive Economic Partnership Agreement (CEPA) exists between the UAE and Singapore. At the Third Singapore-UAE Joint Committee Meeting on 8 June 2023, the UAE expressed interest in a bilateral CEPA, but no negotiations have been announced or concluded.

The existing UAE-Singapore Comprehensive Partnership (signed 28 February 2019) is a broad diplomatic framework covering education, technology, and environment. It contains no provisions on VAT or indirect tax cooperation.

Recommendation: Monitor the FTA's official approved-country list for future updates. If a UAE-Singapore CEPA is signed with tax cooperation provisions, Singapore's eligibility status may change.

Who Can Claim and What Expenses Are Eligible?

Six Core Eligibility Conditions

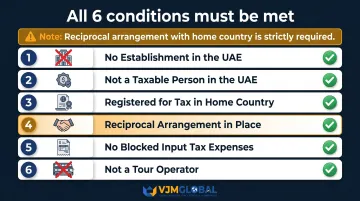

To qualify for a UAE VAT refund, your business must meet all six conditions below (Article 67, Cabinet Decision No. 52 of 2017):

- No UAE establishment : No place of establishment or fixed establishment in the UAE or any GCC Implementing State

- Not a UAE taxable person : Not carrying on business in the UAE, unless the recipient accounts for VAT under reverse charge (Article 48(1))

- Registered in home country : Carrying on a business and registered with a competent authority in the home country

- Reciprocal arrangement : From a country with a UAE reciprocal VAT refund arrangement (does not apply to GCC states)

- No blocked expenses : Input VAT claimed is not blocked from recovery under UAE VAT legislation

- Not a tour operator : Not claiming in connection with tour operator activities

Minimum Threshold and Claim Period

The minimum claim amount is AED 2,000 per 12-calendar-month claim period. Claims below this threshold will not be accepted by the FTA. This minimum threshold does not apply to GCC states per Article 67(10).

Eligible Expense Categories

Once you confirm eligibility, the following business expenses typically qualify for VAT recovery:

- Hotel accommodation for business travel

- Professional and consulting services (legal, accounting, advisory)

- Conference and exhibition fees

- Office supplies and business equipment

- Goods purchased for business use

- Business-related rental costs

All expenses must be directly connected to the business's taxable activities in its home country.

Blocked Expenses Under Article 53

Not every UAE expense is recoverable. Article 53 of Cabinet Decision No. 52 of 2017 blocks VAT recovery on three categories:

- Entertainment services for non-employees (customers, officials, shareholders): hospitality, food and drinks outside normal business meetings, event access, and pleasure trips

- Motor vehicles available for personal use: road vehicles seating up to 10 people, excluding licensed taxis, emergency vehicles, and rental fleet vehicles

- Personal employee benefits: goods or services given to employees at no charge, unless mandated by UAE labor law or contractual obligation

Input Tax Apportionment

If your business performs both taxable and exempt activities in your home country, you must declare the percentage of input tax eligible for recovery. Article 55 of Cabinet Decision No. 52 of 2017 requires apportionment where businesses make both taxable and exempt supplies. Supporting evidence from your home country tax authority may be required.

How to Submit a UAE VAT Refund Claim

Step 1 — Create an FTA Account

Navigate to the FTA's EmaraTax platform and authenticate using UAEPass. Within your Dashboard, select "SPECIAL REFUNDS" → "Business Visitor Refunds" to access the application form.

You'll need to create a taxable person profile within the user dashboard, even though your business is not UAE-registered. This profile serves as the gateway to submitting the refund application. Estimated time: approximately 15 minutes.

Step 2 — Complete and Submit the Refund Application

The Business Visitor Refund form requires:

- Business name and registered address

- Nature of business activities

- Home country registration details and tax identification number

- Reasons for incurring UAE expenses

- Description of activities undertaken in the UAE

- Total VAT amount being claimed

- Calendar year covered by the claim

- Percentage of input tax eligible for recovery (if applicable due to exempt/non-business activities)

- Bank account details in AED for refund payment

Step 3 — Prepare and Upload Mandatory Documents

Required documents include:

(a) Original Tax Compliance Certificate — Business status certificate or equivalent issued by your home country's tax authority in Arabic or English, reflecting your Tax Registration Number. Must be attested by the UAE Embassy in your country of registration.

For Singapore businesses (if eligibility is established):

- The Inland Revenue Authority of Singapore (IRAS) issues a Certificate of Residence or Letter of Residence

- Processing time: 7 working days (online) or 14 working days (written application)

- The certificate must then be attested by the UAE Embassy in Singapore — Phone: +65 6238 8206, Email: SingaporeEmb@mofa.gov.ae

(b) Valid UAE tax invoices showing the supplier's Tax Registration Number (TRN). Verify each supplier TRN using the FTA's online verification tool before submitting.

(c) Proof of payment for each invoice (receipts or invoices stamped "paid" with supplier details).

(d) Authorized signatory documentation — passport copy and proof of authority.

(e) Input tax recovery declaration — required if you have exempt or non-business activities; must state the eligible recovery percentage with supporting evidence from your home tax authority.

Step 4 — Submit Physical Documents to the FTA

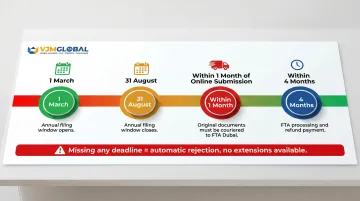

Critical deadline: Within one month of submitting your online application, courier original hard-copy documents to:

Federal Tax Authority P.O. Box 2440 Dubai, UAE

Or email scanned copies to: ForeignBusiness@tax.gov.ae

Note: the original attested Tax Compliance Certificate must be a physical hard copy regardless of whether other documents are sent electronically. Missing the one-month deadline results in automatic rejection.

Step 5 — Track the Application and Respond to Queries

The FTA processes refund applications within 4 months of receiving all relevant documents. Key timelines to monitor:

- Approved refunds are paid in UAE Dirhams (AED) within 10 business days

- FTA clarification requests must be answered within one month — missed responses trigger automatic rejection

Monitor your FTA dashboard regularly throughout this period.

New 5-Year Limitation Period

Federal Decree-Law No. 17 of 2025, effective 1 January 2026, introduces a 5-year statutory limitation on refund claims. Refund requests must be submitted within 5 years from the end of the relevant tax period. A transitional provision allows claims for older credits to be submitted by 31 December 2026.

Professional Support

VJM Global can assist Singapore businesses with every stage of this process — from assessing eligibility and coordinating IRAS and UAE Embassy attestations, to preparing compliant documentation and liaising with the FTA. With 30+ years of experience in international tax compliance and cross-border advisory, the team has supported businesses across the USA, UK, Australia, and beyond in navigating complex foreign tax recovery processes.

Common Mistakes Singapore Businesses Should Avoid

Proceeding Without Confirming Reciprocal Status

The most costly assumption: filing a Business Visitors Refund application without first verifying that Singapore has a reciprocal arrangement with the UAE. This leads to automatic rejection regardless of documentation quality.

Action: Always verify the current MOF-approved country list before investing time in the application process.

Documentation Failures

Tax Compliance Certificate errors:

- Must be an original document in Arabic or English

- Must be issued by IRAS (for Singapore businesses)

- Must be attested by the UAE Embassy in Singapore

- Copies, unattested certificates, or certificates in other languages will be rejected

Tax invoice requirements:

- Must display the UAE supplier's valid Tax Registration Number (TRN)

- Invoices with incorrect or missing TRNs are treated as invalid

- Verify each TRN using the FTA's online verification tool before submitting

Missing Critical Deadlines

Annual filing window: 1 March to 31 August of the year following the calendar year in which VAT was incurred. Missing this deadline means losing the refund entirely for that year.

Physical document deadline: Many businesses submit the online form correctly but forget to courier original documents within the mandatory one-month follow-up window. This results in automatic rejection, with no extension mechanism available. Factor in international courier transit time from Singapore to Dubai when scheduling dispatch.

Including Blocked Expenses

Beyond timing, expense eligibility is another common stumbling block. Claiming VAT on Article 53 blocked categories — entertainment services, personal-use motor vehicles, or personal employee benefits — leads to partial or full rejection. Review each expense against the blocked categories list before including it in your claim.

Frequently Asked Questions

How to claim VAT refund in UAE for business online?

Foreign businesses submit a Business Visitor Refund application through the FTA's e-Services portal, uploading required documents including attested tax compliance certificates and tax invoices. Original documents must then be couriered to the FTA within one month of online submission.

Who is eligible for VAT refund in the UAE?

Eligible businesses must meet all six of these conditions:

- No UAE establishment or fixed place of business

- Not registered as a UAE taxable person

- Registered for tax in their home country

- Home country has a reciprocal arrangement with the UAE

- VAT claimed is not blocked under UAE law

- Not a tour operator

The minimum claim threshold is AED 2,000 of input VAT per 12-month period.

What purchases or expenses are eligible for a VAT refund in the UAE?

Eligible expenses include UAE business-related purchases such as accommodation, professional services, conference fees, and goods used for business purposes. VAT on entertainment, personal expenses, motor vehicles for non-business use, and exempt supplies is not recoverable.

Does Singapore have a reciprocal VAT arrangement with the UAE?

Singapore is not on the UAE Ministry of Finance's approved list of countries with reciprocal arrangements, so Singapore businesses generally cannot access the Business Visitors Refund Scheme. Verify the current list with the FTA, or explore standard VAT refund routes if your business has a UAE-registered entity.

What is the deadline to submit a UAE VAT refund application?

The annual filing window runs from 1 March to 31 August of the year following the calendar year in which VAT was incurred. Under 2026 rules, a five-year limitation period also applies to any unclaimed credit balances.

What is the minimum refund amount under the UAE Business Visitors Refund Scheme?

The minimum threshold is AED 2,000 of input VAT per 12-calendar-month claim period. Claims below this amount will not be accepted by the FTA.

Singapore businesses face eligibility barriers to the UAE Business Visitors VAT Refund Scheme for now, but keeping compliant invoices and tracking UAE VAT exposure remains prudent. The five-year limitation window protects potential future claims if reciprocity is established through bilateral agreements or CEPA negotiations. Businesses with significant UAE operations may find that establishing a UAE entity opens immediate VAT recovery options — VJM Global can advise on UAE entity setup and cross-border tax compliance.