This guide covers what UK VAT exemption actually means, which goods and services qualify, when Singapore companies must register, and the crucial distinction between exempt and zero-rated supplies that determines whether you can reclaim input VAT on your UK business costs.

TLDR:

- UK VAT exemption means no VAT charged but no input VAT recovery — unlike zero-rated supplies at 0% where full recovery is possible

- Singapore companies must register from the first pound of taxable UK supplies — the £90,000 threshold doesn't apply to overseas businesses

- Financial services, education, healthcare, and residential property are typically exempt, blocking input VAT recovery on related costs

- B2B services often use reverse charge (UK customer accounts for VAT), while B2C digital services require immediate UK VAT registration

- Partial exemption rules apply when making both taxable and exempt supplies, requiring careful tracking and annual adjustments

How UK VAT Works: A Quick Overview for Singapore Businesses

UK Value Added Tax is charged at every stage of the supply chain. UK-registered businesses collect VAT on behalf of HMRC and can reclaim VAT paid on their business purchases — a mechanism similar in principle to Singapore's GST.

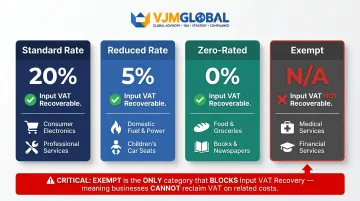

The structural difference that catches most Singapore companies off guard: the UK operates four VAT categories, not three. That fourth category — exempt — sits entirely outside the VAT system and blocks input VAT recovery.

The four VAT categories are:

| VAT Category | Rate | Can Reclaim Input VAT? | Common Examples |

|--------------|------|----------------------|-----------------|

| Standard | 20% | Yes | Most goods and services |

| Reduced | 5% | Yes | Children's car seats, home energy |

| Zero-rated | 0% | Yes | Most food, books, children's clothing |

| Exempt | N/A | No | Financial services, insurance, healthcare, education |

The exempt category is the most consequential distinction in the table. Zero-rated supplies carry a 0% rate but still sit inside the VAT system — meaning businesses can reclaim input VAT on related costs. Exempt supplies generate no VAT charge but also block input VAT recovery entirely, which directly affects margins on UK operations.

UK-established businesses must register for VAT when their taxable turnover exceeds £90,000 in the last 12 months or is expected to cross that threshold within 30 days. Businesses below this level can register voluntarily.

Singapore companies face a different rule. The £90,000 threshold does not apply to non-UK established businesses — overseas companies must register from the first pound of taxable UK supply, regardless of turnover. That zero-threshold rule means VAT registration is not a future milestone; for most Singapore businesses making UK sales, it is an immediate obligation. Understanding which supplies are exempt — and which only appear exempt — determines whether registration triggers at all.

What Is UK VAT Exemption? (And How It Differs from Zero-Rated)

Exempt Supplies: Outside the VAT System Entirely

VAT exemption means no VAT is charged to customers — but no input VAT on related business costs can be reclaimed from HMRC either. VAT Notice 700 states: "Some supplies are exempt from VAT, which means that no tax is payable — but, equally, the person making the supply cannot normally recover any of the VAT on their own expenses."

If your Singapore company exclusively sells exempt services in the UK — such as insurance or certain financial services — you cannot register for VAT and cannot recover any UK VAT incurred on business purchases.

Zero-Rated Supplies: Taxable at 0% with Full Recovery Rights

Zero-rated supplies are taxable at 0%, which means businesses can register for VAT and reclaim all input tax on associated costs. VAT Notice 700 confirms: "Zero-rated supplies are treated as taxable supplies in all other respects, including the right of the person making the supply to recover the VAT on their purchases."

The Cash-Flow Consequence

If a Singapore company sells exempt financial services to UK clients, any VAT paid on UK business costs becomes an unrecoverable expense. If the same company sold zero-rated goods — such as exported books — it could reclaim every pound of that VAT.

Example:

- Company A (exempt insurance services): Pays £12,000 VAT on annual UK office rent. Cannot reclaim. Lost cost: £12,000.

- Company B (zero-rated book exports): Pays £12,000 VAT on annual UK office rent. Reclaims in full. Net cost: £0.

For Singapore companies with mixed UK operations, understanding which category applies to each revenue stream directly affects how you structure costs and whether UK VAT registration is worth pursuing.

Out of Scope Supplies

Beyond exempt and zero-rated, a third category sits completely outside the UK VAT framework. VAT Notice 741A explains: "If the supply is in the UK it is subject to UK VAT. If the supply is in an EU member state or another country it is said to be 'outside the scope' of UK VAT."

Examples include statutory fees, goods a business purchases and uses entirely outside the UK, and services where the place of supply is not the UK. Out of scope supplies don't count toward UK taxable turnover and don't trigger UK VAT registration obligations.

Quick Comparison: Exempt vs. Zero-Rated vs. Out of Scope

| Supply Type | VAT Charged to Customer | Input Tax Recoverable | Counts Toward UK VAT Turnover |

|---|---|---|---|

| Exempt | No | No | Yes |

| Zero-Rated | No (0%) | Yes | Yes |

| Out of Scope | No | No | No |

What Is Exempt from VAT in the UK? Full Category Breakdown

Financial and Insurance Services

Most banking, credit, insurance, and securities services are exempt under VAT Notice 701/49. This includes:

- Dealing with money and payment transfers

- Account operation charges

- Granting credit, loans, and overdrafts

- Interest on outstanding balances

- Sale or transfer of securities (shares, bonds)

- Investment fund management for qualifying Special Investment Funds

- Insurance underwriting and brokerage

Notable exceptions that attract standard-rate VAT:

- Debt collection services

- Credit checking and creditworthiness assessment by third parties

- Safe custody and safe deposit facilities

- Provision of financial data or software

- Rental of card terminals

- General financial advice where no specific product is arranged

For Singapore fintech companies, the exempt/taxable boundary runs through the middle of many revenue models. Payment processing is generally exempt, but software licensing, data services, and credit management services are taxable. Misclassifying these streams blocks legitimate input VAT recovery.

Education, Training, and Healthcare

VAT Notice 701/30 confirms that education and vocational training are exempt only when supplied by an "eligible body" — schools, colleges, universities, local authorities, non-profit organisations, and certain registered commercial providers.

Critical limitation: Not all training providers qualify. A for-profit training company that doesn't meet the eligible body criteria must charge VAT at the standard rate. Private tuition by individual teachers is exempt if the subject is taught regularly in schools or universities.

Private school fees: 20% VAT from 1 January 2025

From 1 January 2025, all education and boarding services provided by private schools are subject to VAT at the standard rate of 20%. Previously exempt, this change affects Singapore ed-tech companies supplying content or services to UK private schools.

Healthcare follows a similar registered/unregistered divide. Services are exempt when provided by registered health professionals — doctors, nurses, dentists, physiotherapists, and pharmacists — where the primary purpose is protecting, maintaining, or restoring health.

The following attract VAT at the standard rate:

- Services by unregistered therapists

- Cosmetic procedures

- Medical reports prepared for insurance purposes

Land, Property, and Other Exempt Categories

VAT Notice 742 confirms that selling or leasing land and buildings is normally exempt. However, landlords can opt to tax commercial property, waiving the exemption and charging VAT instead. This "option to tax" directly affects Singapore companies leasing UK office space — if the landlord has opted to tax, you'll pay 20% VAT on rent but can reclaim it (if you're VAT-registered for taxable supplies).

Other exempt categories:

- Postal services (Royal Mail specifically)

- Betting, gaming, and lotteries

- Membership subscriptions to eligible non-profit organisations

- Charitable fundraising events

- Burial and cremation services

Does Your Singapore Company Need to Register for UK VAT?

No Registration Threshold for Overseas Businesses

Unlike UK-based businesses, overseas companies must register for UK VAT from the first pound of taxable UK supplies. The £90,000 threshold does not apply.

HMRC defines a Non-Established Taxable Person (NETP) as any business that makes taxable supplies in the UK without a fixed UK establishment. Your Singapore company qualifies as an NETP — and must register immediately — if it:

- Makes any taxable supply of goods located in the UK

- Sells digital services directly to UK consumers

- Ships goods into the UK for sale to UK customers

Place of Supply Rules

Whether UK VAT applies depends on where the supply is deemed to take place:

For goods: VAT applies if goods are located in the UK at the point of sale.

For services (B2B): The general rule under VAT Notice 741A is that "the supply is made where the customer belongs." If your UK customer is VAT-registered, the supply takes place in the UK.

For services (B2C): The general rule is that "the place of supply is where the supplier belongs." If you're a Singapore supplier selling to a UK consumer, the supply is outside the UK — unless specific exceptions apply.

Reverse Charge Mechanism for B2B Services

When a Singapore company sells B2B services (consulting, professional services, software development) to a VAT-registered UK business, the UK customer accounts for VAT under the reverse charge. You do not charge UK VAT on these supplies, and you generally will not need to register for UK VAT.

This is the primary compliance simplification for Singapore professional services firms selling B2B into the UK.

Digital Services to UK Consumers Require Registration

The reverse charge relief does not extend to consumer sales. Singapore companies selling digital services directly to UK consumers must register for UK VAT with no threshold — because the place of supply is where the consumer is located. Digital services include software, streaming, e-books, online magazines, VoIP, and live streaming. If your Singapore SaaS company sells subscriptions to UK consumers, you must register and charge UK VAT from the first sale.

Platform relief: If you supply digital services via a third-party marketplace (such as app stores), the platform is responsible for accounting for VAT, not you.

When Exemption Benefits You (and When It Doesn't)

If your Singapore company exclusively makes exempt supplies in the UK (such as financial intermediation services), you will not need to register for UK VAT. The trade-off is significant, though:

- No registration means no ability to reclaim UK input VAT

- Office space, equipment, and professional fees become 20% more expensive

- Businesses with substantial UK costs often find voluntary registration worthwhile

The right answer depends on your supply mix, cost base, and customer type — making a VAT classification review a practical first step before trading in the UK.

Partial VAT Exemption: What It Means for Mixed-Supply Businesses

Definition and Impact

A business is partially exempt when it makes both taxable and exempt supplies. Only a portion of input VAT on shared costs (overheads, rent, admin) can be reclaimed. The recoverable proportion is typically calculated using the standard method: the ratio of taxable supplies to total supplies.

The De Minimis Rule

HMRC allows businesses to reclaim exempt input tax if it doesn't exceed £625 per month on average (£7,500 per year) AND is less than 50% of total input tax. Both tests must be satisfied.

Many Singapore companies with mixed supplies miss this entirely. If your exempt input tax falls below both thresholds, you can reclaim it in full — so it's worth checking before writing off that input VAT.

Knowing when you qualify for de minimis relief matters, but it doesn't reduce the record-keeping obligations that come with partial exemption status.

Record-Keeping Obligations

Partially exempt businesses must:

- Maintain separate records for taxable and exempt activities

- Apportion shared costs using an HMRC-approved method

- Perform an annual adjustment to correct provisional quarterly attributions

- Reconsider the use of goods and services over the full year

Non-compliance with partial exemption record-keeping is a common audit trigger.

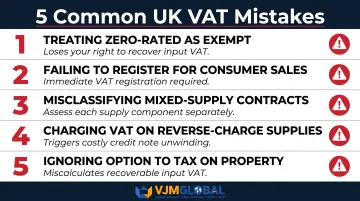

Common UK VAT Mistakes Singapore Companies Make

These five mistakes account for the majority of UK VAT compliance failures VJM Global sees among Singapore companies — each one avoidable with the right classification from the start.

Treating Zero-Rated Supplies as Exempt

This error prevents businesses from reclaiming input VAT they are legally entitled to. A Singapore company exporting zero-rated goods from the UK that incorrectly treats the supplies as exempt will fail to register for VAT and lose full input VAT recovery on UK business costs.

Failing to Register When Selling Taxable Supplies to UK Consumers

Singapore companies often assume the £90,000 threshold applies to them. It does not. Any taxable supply to UK consumers — especially digital services — triggers immediate VAT registration for non-UK businesses.

Misclassifying Mixed-Supply Contracts

When a single contract includes both exempt and taxable elements (such as a training package bundled with software), the VAT treatment of each component must be assessed separately. Applying a single VAT treatment to the entire contract is one of the most frequently flagged errors in HMRC compliance reviews.

Charging VAT on Reverse-Charge Supplies

When the reverse charge applies to B2B services, the Singapore supplier should not charge UK VAT. Charging VAT in error forces both parties to unwind the transaction through credit notes — delaying payment and triggering HMRC scrutiny.

Ignoring the Option to Tax on Property

Not all UK office rent is VAT-exempt — and assuming otherwise produces incorrect input VAT calculations. If the landlord has opted to tax the property, VAT is chargeable on rent — but becomes recoverable input tax for the tenant (if VAT-registered for taxable supplies).

Frequently Asked Questions

What does VAT exempt mean?

VAT exempt means the supply falls entirely outside the VAT system. No VAT is charged to the customer, but equally, no input VAT on related business costs can be reclaimed from HMRC.

What is the difference between 0% VAT and VAT exempt?

Zero-rated supplies are taxable at 0%, allowing businesses to register for VAT and reclaim input tax on all associated costs. Exempt supplies are outside the VAT system entirely, blocking any input VAT recovery.

Who is VAT exempt in the UK?

Businesses that exclusively make exempt supplies — such as certain healthcare providers, financial services firms, educational institutions, and residential property landlords — are VAT exempt and cannot register for VAT.

What is exempt from VAT in the UK?

Main exempt categories include:

- Financial and insurance services

- Education and training by eligible bodies

- Healthcare services by registered professionals

- Residential property sales and leases

- Postal services, charity fundraising events, and betting and gaming

What is a VAT exemption for a small business?

A small business selling only exempt goods or services does not need to register for VAT regardless of turnover. However, it cannot reclaim any VAT paid on business purchases, making costs effectively 20% higher.

How do I get a VAT certificate in the UK?

Once HMRC approves your online VAT registration, it issues a VAT registration certificate. Overseas businesses, including Singapore companies, should confirm the specific documents required with HMRC or a UK VAT adviser before submitting.

Need help with UK VAT? VJM Global advises Singapore and international businesses on UK VAT registration, supply classification, and ongoing compliance. Reach us at info@vjmglobal.com or +91 9891576441.