Introduction

Singapore has established itself as a major business hub in Asia, drawing UK companies with its political stability, pro-business tax framework, and strategic position in ASEAN. Yet for all its advantages, Singapore's financial audit and compliance landscape differs in material ways from UK requirements under the Companies Act 2006 and FRC standards. UK finance directors cannot assume that their home-country compliance knowledge transfers directly.

A UK subsidiary incorporated in Singapore faces statutory obligations under the Singapore Companies Act, reporting standards issued by Singapore's Accounting Standards Council, and a dual-regulator model spanning ACRA and IRAS.

Misjudging audit exemption thresholds, financial year-end alignment, or the prohibition on FRS 102 for Singapore statutory accounts creates compliance gaps — gaps that trigger penalties, court summons, and consolidation headaches for the UK parent.

This guide walks UK companies through Singapore's audit regulations, key governing bodies, statutory requirements, accounting standards, and filing deadlines—so finance leads understand exactly what's required, where the key differences lie, and how to manage cross-border reporting obligations without gaps.

Key Takeaways

- Singapore mandates annual statutory audits for most private limited companies unless exemption criteria are met

- Financial statements must follow SFRS(I) — aligned to IFRS but not interchangeable with UK-adopted IFRS or FRS 102

- ACRA oversees audit registration, compliance monitoring, and annual filing including XBRL submissions

- Penalties reach S$600 (ACRA) and S$5,000 per offence (IRAS); persistent non-filing can trigger court-imposed penalties of twice the tax assessed

- UK parent companies need to align Singapore FYE dates and reporting standards with group consolidation requirements

Singapore's Regulatory Landscape: What UK Companies Should Know

UK-Singapore bilateral trade reached £26.7 billion in the four quarters to Q3 2025, up 19.6% year-on-year, with UK outward FDI stock in Singapore standing at £11.6 billion at the end of 2024. Approximately 4,000 British businesses now operate in Singapore alongside 45,000 British citizens resident in the country. The UK-Singapore Free Trade Agreement, signed December 2020 and in force since February 2021, provides tariff elimination and enhanced services market access—but it does not exempt UK subsidiaries from Singapore's domestic audit framework.

Entity Structure Choices

UK companies typically enter Singapore through one of two structures:

- Wholly owned subsidiary (private limited company) – a locally incorporated entity subject to full Singapore Companies Act obligations

- Branch office – an extension of the foreign parent, with modified audit and filing requirements

Each carries different regulatory burdens. A Singapore subsidiary may qualify for audit exemption if it meets size thresholds; a branch generally cannot, even if it operates at similar scale. This structural choice has direct cost and compliance implications that should be evaluated before incorporation.

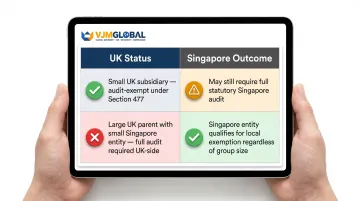

UK Exemption Rules Don't Apply in Singapore

Unlike the UK, where smaller private companies benefit from Section 477 audit exemptions and FRS 102 simplified reporting, Singapore applies its own independent exemption tests. UK small company treatment does not transfer automatically.

The practical results can run in either direction:

| Scenario | UK Status | Singapore Outcome |

|---|---|---|

| Small UK subsidiary below home thresholds | Audit exempt under Section 477 | May still require full statutory audit if Singapore thresholds not met |

| Large UK parent with small Singapore entity | Full audit required at home | Singapore entity may qualify for local audit exemption regardless of group size |

Key Bodies and Standards Governing Financial Audits in Singapore

ACRA (Accounting and Corporate Regulatory Authority)

ACRA serves as Singapore's primary regulator for company audits, accounting, and corporate governance. Established under the Accounting and Corporate Regulatory Authority Act 2004, ACRA merged the Registry of Companies and Businesses with the Public Accountants' Board to create a unified regulator responsible for:

- Registering public accountants and approving Public Accounting Entities (PAEs) under the Accountants Act 2004

- Monitoring audit quality through the Practice Monitoring Programme (PMP), which inspects audit firms and reviews findings through the Public Accountants Oversight Committee (PAOC)

- Enforcing compliance with the Companies Act (Cap. 50), including annual return filings, financial statement submissions, and XBRL format requirements

ACRA's 2022 amendments to the Accountants Act expanded its powers to mandate remediation of audit lapses and impose sanctions for significant deficiencies discovered during inspections.

Accounting Standards Council (ASC)

The ASC issues Singapore Financial Reporting Standards (International) – SFRS(I) – and SFRS(I) Interpretations. These standards are based on IFRS Accounting Standards issued by the IASB, with copyright held by the IFRS Foundation. Singapore maintains its own adoption timeline through the ASC, meaning SFRS(I) follows IFRS substantively but may diverge on timing and transitional provisions.

The ASC also issues the SFRS for Small Entities framework, a simplified standard analogous to IFRS for SMEs and structurally similar to the UK's FRS 102 (which is also based on IFRS for SMEs). UK finance teams should not assume the two are directly comparable without professional review.

Auditor Registration: A Critical Practical Point

Only public accountants registered with ACRA may conduct statutory audits in Singapore. UK-based audit firms—including Big Four and mid-tier firms—cannot directly sign off on Singapore statutory audits unless their Singapore entity employs an ACRA-registered public accountant.

This has a direct structural implication for UK parent companies using a global audit firm: the London office cannot simply extend its UK audit engagement to cover the Singapore subsidiary. The Singapore entity must be audited by the firm's Singapore member, which must hold ACRA registration and comply with local audit standards.

Singapore Standards on Auditing (SSAs)

Audit conduct in Singapore is governed by SSAs, which are based on International Standards on Auditing (ISAs) issued by the IAASB, with local amendments applied where considered appropriate. UK finance teams will find the methodology familiar — risk assessment, materiality, substantive testing — even if the regulatory framing differs from FRC requirements.

Audit Quality Indicator (AQI) Framework

ACRA's voluntary AQI framework comprises 10 indicators designed to help audit committees select and evaluate auditors. Revised in 2025, the framework covers:

- Quality control systems and culture surveys

- Training investment and staff experience levels

- Inspection findings and restatement history

- Staff oversight ratios and attrition rates

- Audit hours and use of technology

ACRA publishes industry averages twice yearly — in June and December — grouped by Big Four and non-Big Four firms. For UK companies establishing governance structures in Singapore for the first time, this benchmarking data provides a practical starting point for auditor selection.

Statutory Audit Requirements and Exemptions for UK-Owned Entities

Default Rule: Statutory Audit Required

All private limited companies incorporated in Singapore—including Singapore subsidiaries of UK parent companies—are required to have their financial statements audited annually by an ACRA-registered public accountant, under the Companies Act. This obligation applies regardless of the UK parent's audit status.

Small Company Audit Exemption (Section 205C)

A private company qualifies for audit exemption if it meets at least 2 of 3 quantitative criteria for the immediate past two consecutive financial years:

- Total annual revenue ≤ S$10 million

- Total assets ≤ S$10 million

- Number of full-time employees ≤ 50 (measured at end of FY)

Newly incorporated companies (operating less than two years) qualify if the criteria are met in the current financial year. A UK-owned subsidiary can qualify based solely on its own Singapore entity figures, not the UK parent group's consolidated results.

This exemption has applied to financial years beginning on or after 1 July 2015, superseding the previous Exempt Private Company (EPC) framework. One key change: companies with corporate shareholders can now qualify, removing the prior restriction to all-individual shareholder bases.

Small Group Exemption: The Overlooked Test

If the Singapore entity is part of a group (UK parent + Singapore subsidiary), both conditions must be met:

- The individual Singapore company must qualify as a small company

- The entire group (including the UK parent and all foreign entities) must meet at least 2 of the same 3 thresholds on a consolidated basis for the immediate past two consecutive financial years

This group test is where many UK companies lose the exemption. A Singapore subsidiary that looks "small" on its own may fail once the UK parent's consolidated figures are factored in. For example:

- Singapore subsidiary: S$8M revenue, S$7M assets, 40 employees → qualifies standalone

- UK parent group (consolidated): £50M revenue (S$85M equivalent), £30M assets, 200 employees → fails group test

- Result: Singapore subsidiary does not qualify for audit exemption despite its small local footprint

Dormant Company Exemption (Section 205B)

A dormant company is exempt from audit requirements if it has no significant accounting transactions and total assets not exceeding S$500,000. This exemption is not limited to private companies.

UK companies that have incorporated a Singapore entity without yet commencing active operations—for instance, holding a shell ahead of planned expansion or maintaining a dormant subsidiary post-cessation—can rely on this exemption to avoid audit obligations in the interim.

Auditor Appointment Obligation

Even if a company qualifies for audit exemption, directors must appoint an ACRA-registered public accountant within three months of incorporation unless the company meets the exemption criteria from the outset.

UK company directors serving as Singapore directors must be aware this is a personal obligation under Singapore law, distinct from UK directors' duties. Failure to appoint an auditor within the statutory timeframe constitutes a breach of the Companies Act and can expose individual directors to personal penalties under Singapore law.

SFRS vs UK GAAP: Key Differences UK Companies Must Know

The Three-Way Framework Distinction

SFRS(I) is based on IFRS as issued by the IASB, but Singapore maintains its own adoption timeline through the Accounting Standards Council. Meanwhile, UK-adopted IFRS follows IFRS as retained in UK law via the UK Endorsement Board, which may diverge from both IASB IFRS and SFRS(I) over time, particularly post-Brexit.

This creates a three-way distinction:

- IASB IFRS – the global baseline

- UK-adopted IFRS – UK's endorsed version, potentially with UK-specific amendments or timing differences

- SFRS(I) – Singapore's adopted version, with its own timing and transitional provisions

For UK companies, SFRS(I) and UK-adopted IFRS share the same IFRS foundation — but they are not identical. Timing mismatches and transitional relief provisions can still create reconciliation issues that require active management.

FRS 102 Is Not Acceptable for Singapore Statutory Accounts

Many UK private companies, subsidiaries, and SMEs prepare accounts under FRS 102 (UK GAAP) rather than full IFRS. FRS 102 is not an acceptable reporting framework for Singapore statutory accounts.

ACRA requires all Singapore-incorporated companies to prepare financial statements under frameworks issued by the ASC:

- SFRS(I) (full IFRS-aligned framework)

- SFRS for Small Entities (simplified framework)

- FRS (legacy framework, being phased out)

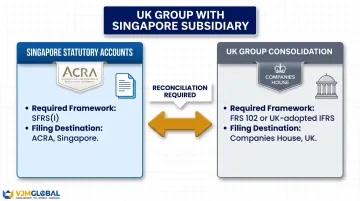

FRS 102 does not appear on this list. This creates a dual reporting obligation for UK groups:

- Singapore statutory accounts – prepared under SFRS(I) for ACRA filing

- UK group consolidation – prepared under FRS 102 or UK-adopted IFRS for Companies House filing and UK audit

UK finance teams must maintain dual accounting capability or engage advisors who can reconcile between frameworks.

SFRS for Small Entities: Structural Similarities to FRS 102

The SFRS for Small Entities framework is a self-contained standard for smaller entities without complex transactions and no public accountability. Eligibility mirrors the small company concept: entities must meet 2 of 3 quantitative thresholds (annual income ≤S$10M, gross assets ≤S$10M, employees ≤50).

UK companies familiar with FRS 102 — which is also based on IFRS for SMEs — will find structural similarities in recognition, measurement, and presentation. However, direct comparability should not be assumed. Differences in scope, specific exemptions, and disclosure requirements require professional review before concluding that FRS 102 accounts can be ported to SFRS for Small Entities with minimal adjustment.

Components of Singapore Financial Statements

Financial statements prepared under SFRS(I) must include:

- Statement of comprehensive income

- Balance sheet (statement of financial position)

- Cash flow statement

- Statement of changes in equity

- Company and shareholder details

- Notes to the accounts

UK companies must ensure their Singapore accounting function produces all required components — not just a profit and loss summary for group reporting purposes.

This is especially relevant where UK parents delegate Singapore bookkeeping to local staff or outsourced providers who may not be familiar with full statutory reporting requirements.

Emerging Sustainability Reporting Obligations

Singapore is phasing in mandatory sustainability/ESG disclosures aligned with IFRS S1 and S2:

| Entity Type | Reporting Starts | Assurance Required From |

|---|---|---|

| Listed companies | FY2025 | FY2029 |

| Large non-listed companies | FY2030 | FY2032 |

External limited assurance is required for Scope 1 and Scope 2 GHG emissions. Assurance providers must be ACRA-registered audit firms or accredited Testing, Inspection, and Certification (TIC) firms.

UK companies already subject to TCFD-aligned reporting will recognise the framework logic here. That said, Singapore's threshold definitions and phase-in timelines differ from UK requirements — UK-owned private subsidiaries should confirm whether and when these obligations apply to their specific entity type and size.

Annual Filing Obligations, Deadlines, and Penalties

Deadlines and Key Filing Requirements

Annual Return (AR) Filing

| Company Type | AR Filing Deadline |

|---|---|

| Listed company | Within 5 months after FYE |

| Non-listed company | Within 7 months after FYE |

| Company with overseas branch register | 6 or 8 months after FYE (listed/non-listed) |

If an AGM is held, the AR must be filed within one month of the AGM. Most companies must submit financial statements in XBRL format; exempt private companies (EPCs) may qualify for simplified filing or complete exemption via online solvency declaration.

UK companies should align Singapore FYE selection with UK group reporting cycles. Many choose 31 December or 31 March for administrative consistency, reducing the reconciliation burden at consolidation.

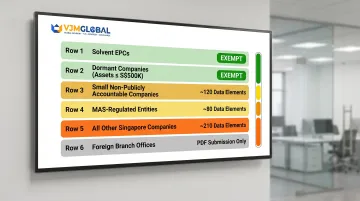

XBRL Filing Requirements by Entity Type

| Company Category | Filing Requirement |

|---|---|

| Solvent EPCs | Exempt (online solvency declaration only) |

| Dormant companies (assets ≤S$500K) | Exempt |

| Small, non-publicly accountable companies | Simplified XBRL (~120 data elements) |

| Banks/finance/insurance (MAS-regulated) | XBRL FSH (~80 data elements) |

| All other Singapore companies | Full XBRL (~210 data elements) |

| Foreign companies (branches) | PDF only (exempt from XBRL) |

Estimated Chargeable Income (ECI) Filing

Companies must file ECI with IRAS within 3 months from the end of the financial year, unless the company qualifies for the ECI filing waiver (annual revenue ≤S$5M and ECI is nil for the year of assessment).

This is a tax filing, not an audit filing, but it runs in parallel with audit timelines. Many UK companies managing Singapore subsidiaries remotely fail to calendar ECI deadlines, assuming it forms part of the annual audit cycle. It does not—ECI is an independent obligation with its own penalty regime.

AGM Rules for Private Companies

A private company need not hold an AGM for a financial year if it sends financial statements to members within 5 months after the FYE. Alternatively, all members may pass a resolution to dispense with AGMs entirely.

This flexibility is particularly useful for UK parent companies managing Singapore subsidiaries remotely, where convening a physical AGM would be operationally burdensome.

Penalties for Non-Compliance

ACRA Penalties

Late annual return filing attracts penalties of up to S$600. Persistent non-compliance can escalate to:

- Court summons

- Director disqualification

- Striking off the company register

- Enforcement action under Section 197 of the Companies Act

IRAS Penalties

Failure to file Corporate Income Tax Returns (Form C-S/C-S Lite/C) by the due date (30 November each year) is an offence. Penalties include:

- Composition amount: up to S$5,000 per offence

- Court fine upon conviction: up to S$5,000 per offence

- If a company fails to file for 2 years or more, the Court may impose a penalty of twice the amount of the tax assessed in addition to the fine

- Court summons may be issued to the company and/or directors; failure to attend court can result in a warrant of arrest

UK companies handling Singapore compliance remotely face elevated exposure here. Unlike ACRA's administrative penalty model, IRAS operates a prosecutorial enforcement framework — penalties stack across each year of non-filing, and directors can face personal liability alongside the company.

Missing a single ECI or corporate tax deadline can trigger a chain of enforcement actions that compounds well beyond the original tax amount. Building a dedicated compliance calendar for Singapore obligations — separate from UK group reporting cycles — is the most direct way to avoid this risk.

Frequently Asked Questions

How much does a financial audit cost in Singapore?

Audit fees in Singapore vary based on company size, complexity, transaction volume, industry sector, and the audit firm engaged. Small private companies typically pay from S$3,000 to S$10,000+. Companies should request proposals from multiple ACRA-registered firms to benchmark fees accurately.

Are IFRS and SFRS the same?

SFRS(I) is based on IFRS but is not identical. Singapore follows its own adoption timeline through the Accounting Standards Council and retains local variations in transitional provisions. UK companies using UK-adopted IFRS or FRS 102 must prepare separate statutory accounts under SFRS(I) for Singapore filing — automatic compliance cannot be assumed.

Do UK companies need a Singapore-registered auditor for their Singapore subsidiary?

Yes. Only public accountants registered with ACRA may sign off on Singapore statutory audits. UK-based auditors cannot conduct the Singapore statutory audit directly — even if they audit the UK parent — and the engagement must go through an approved Public Accounting Entity in Singapore.

Can a UK company's Singapore subsidiary qualify for audit exemption?

Yes, if the subsidiary meets at least 2 of 3 thresholds (revenue ≤S$10M, assets ≤S$10M, employees ≤50) for two consecutive financial years. However, if the Singapore entity is part of a larger UK group, the consolidated group figures must also meet the same thresholds. A locally small subsidiary may fail the exemption when the UK parent's size is factored in.

Does a Singapore branch office of a UK company have different audit obligations than a subsidiary?

Yes. A Singapore branch is generally not subject to the same statutory audit requirement as a locally incorporated subsidiary, but must still file two sets of financial statements (head office and branch). Active branches must file audited branch statements unless relief is granted under Section 373(13A), in which case the UK parent's home country audit may satisfy the head office filing requirement.

How does Singapore's financial year-end affect UK parent company consolidation reporting?

UK parent companies should align their Singapore subsidiary's FYE with the UK group's accounting reference date to simplify consolidation. Misaligned year-ends are permitted but add complexity to intercompany eliminations, foreign exchange translation, and audit timing. Common practice is to choose 31 December or 31 March for both jurisdictions where operationally feasible.